Fiserv Review

Legacy-scale acquirer with three different ISV doors — CardConnect for embedded payments, Clover for POS-attached SaaS, Carat for enterprise — sitting on a seven-bank distribution moat that no independent gateway can replicate.

Overview

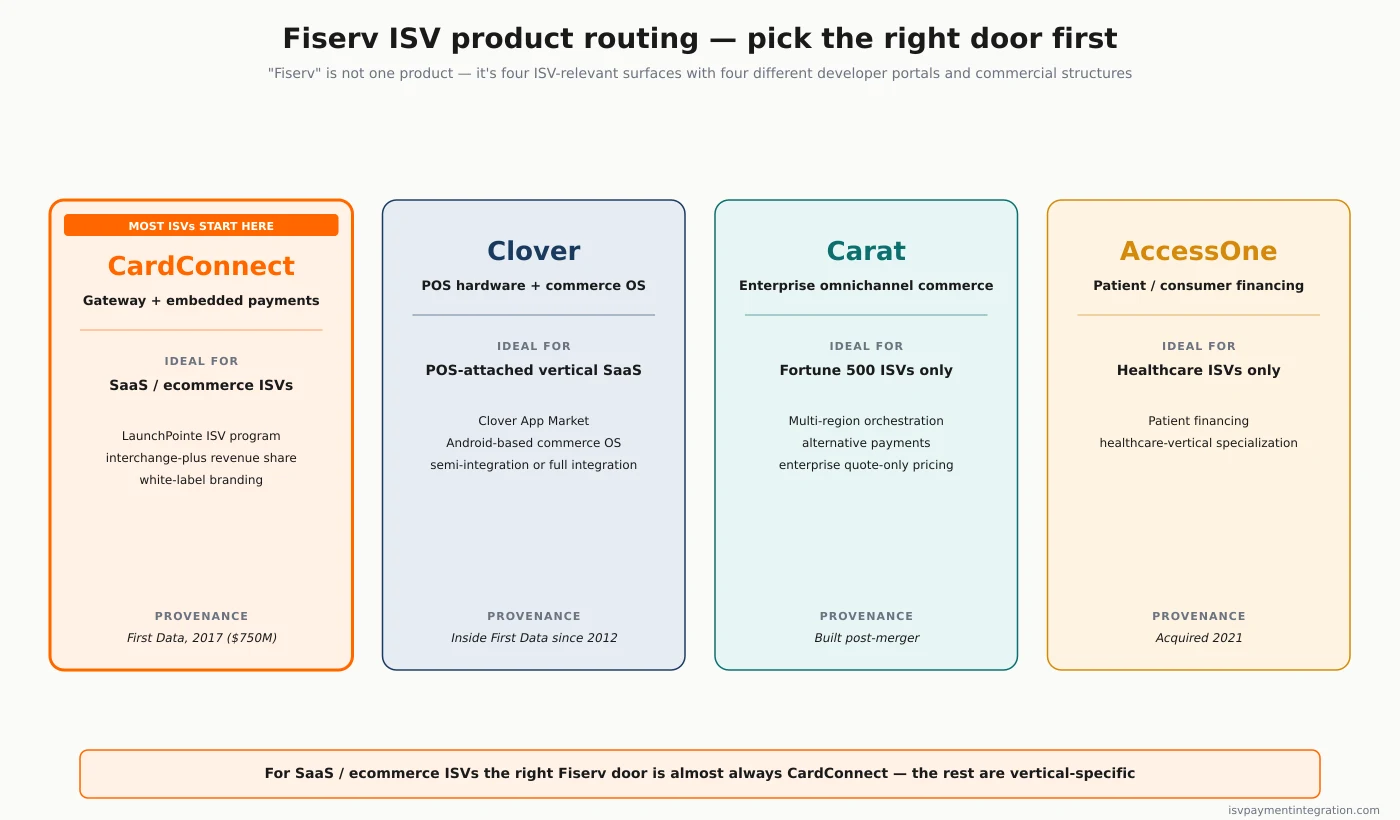

Fiserv is a Brookfield, Wisconsin-based fintech holding company that combined with First Data in July 2019 in a $22 billion all-stock merger, creating one of the largest payment-processing platforms in the world. The company reported $21.19 billion in 2025 GAAP revenue and operates four distinct ISV-relevant product lines acquired or built over decades: CardConnect (gateway and embedded payments for ISVs), Clover (POS hardware and commerce OS for SMB verticals), Carat (enterprise omnichannel orchestration), and AccessOne (consumer/patient financing). For ISVs, Fiserv is not one product — it's four product surfaces with four different developer portals, four different commercial structures, and four different right-fits depending on the platform's target merchant profile.

For the latest on Fiserv's ISV capabilities, documentation, and partner programs, visit fiserv.com.

Pricing

Negotiated interchange-plus (no published rate sheet)

Fiserv does not publish a consumer-facing rate card for any of its ISV-relevant product lines. Fiserv's ISV Partner Program is interchange-plus with performance-tied revenue share; specific basis points and per-transaction fees are partner-negotiated. Clover pricing is a stack — hardware purchase, monthly software subscription tiers, and per-transaction processing — each negotiated by merchant. Carat is enterprise-quote-only. CardConnect raised processing rates by 0.10% plus $0.05 per transaction across all major card networks effective April 1, 2024; that increase passes through to ISV revenue-share margins.

Full pricing breakdown →Pros

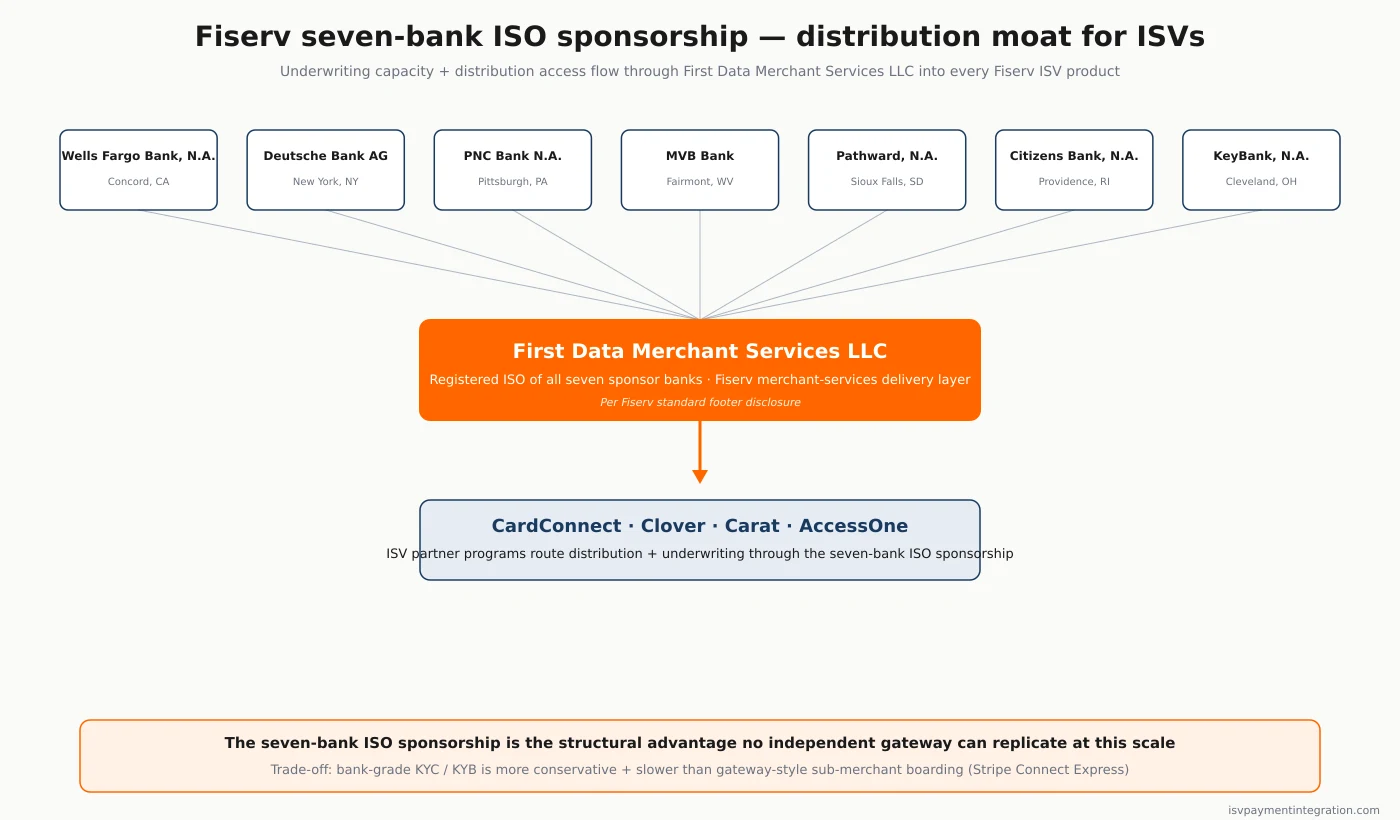

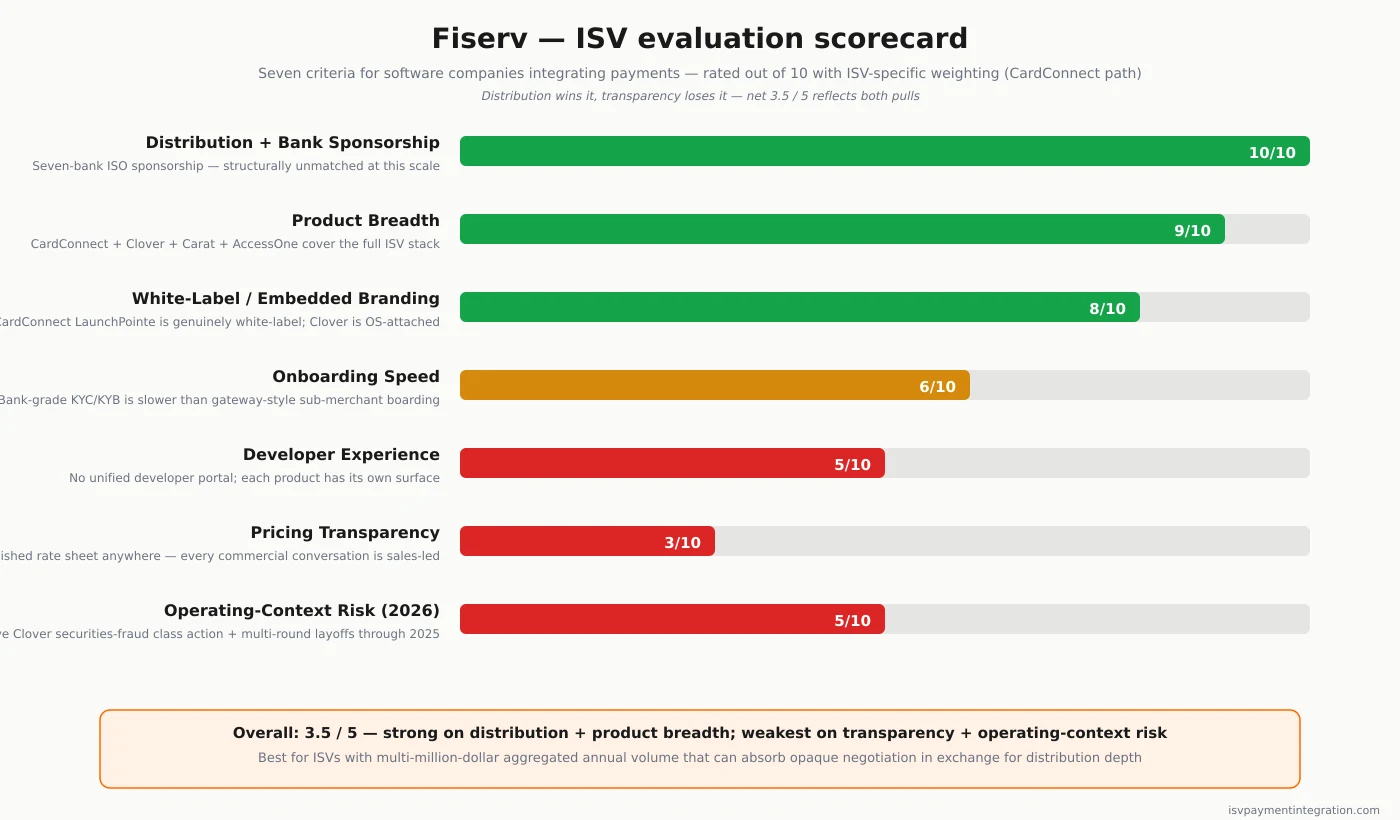

- ✓ Seven-bank ISO sponsorship (Wells Fargo, Deutsche Bank, PNC, MVB, Pathward, Citizens, KeyBank) gives Fiserv distribution depth and underwriting scale no independent gateway matches

- ✓ Fiserv's ISV Partner Program runs a real embedded-payments channel with white-label processor branding, embedded boarding APIs, and performance-tied revenue share for SaaS platforms

- ✓ Clover ecosystem covers POS hardware, the Clover App Market, and an Android-based commerce OS — the strongest in-person stack for vertical SaaS in restaurant, retail, salon, and service

- ✓ Carat enterprise commerce engine handles Fortune 500 omnichannel orchestration — useful for ISVs with Fortune-1000 merchants on their roster

- ✓ International expansion underway — Clover Japan launches via Sumitomo Mitsui partnership in late 2026, broadening the ISV-deployable footprint beyond the US

- ✓ Multi-year IBM AI partnership targets Clover and four other business areas, signaling continued product investment despite the operating-environment turbulence

Cons

- ✗ No unified developer portal — CardConnect, Clover, and Carat each have separate documentation surfaces and integration models, forcing ISVs to self-route the right product before integrating

- ✗ Clover securities-fraud class action filed July 2025 (covering July 24, 2024 – July 22, 2025) alleges forced merchant migration from legacy Payeezy POS inflated reported Clover revenue and GPV — adjudication pending, but the litigation surface is real and ongoing

- ✗ No published rate sheet anywhere across CardConnect, Clover, or Carat — every commercial conversation starts from sales qualification, which adds quote-cycle friction for ISVs that just want to model unit economics

- ✗ April 2024 CardConnect rate increase (+0.10% / +$0.05) compressed ISV residual margins; no public schedule for whether/when further pass-through increases will hit

- ✗ Bank-grade underwriting through the seven sponsor banks is more conservative and slower than gateway-style provisioning — expect days-not-minutes for sub-merchant boarding outside the most automated CardConnect paths

- ✗ Multiple rounds of layoffs through 2024 and 2025 (analyst-estimated 1,000-1,500+ employees in Dec 2024 alone) raise account-coverage continuity questions for partners that depend on relationship management

ISV Fit

Fit depends on which Fiserv door the ISV walks through. CardConnect fits SaaS and ecommerce ISVs that want embedded interchange-plus economics, white-label payment branding, and the seven-bank distribution moat — accepting longer negotiation cycles and opaque residual structures in exchange. Clover fits POS-attached vertical SaaS in restaurant, retail, salon, and service where the commerce-OS lock-in is a feature, not friction. Carat fits enterprise ISVs with Fortune-1000 merchant rosters needing omnichannel orchestration. AccessOne fits healthcare ISVs offering patient financing. Weak fit for early-stage ISVs that prioritize self-serve speed (Stripe), API-first developer ergonomics (Stripe / Adyen), single-vendor simplicity (any bundled platform), or transparent published rates (Square / Stripe).

Alternatives

Fiserv Review: An ISV’s Perspective (2026)

Most published Fiserv reviews are written by direct merchants comparing card-present rates against Square or PayPal. This review is for ISVs and SaaS platforms evaluating Fiserv as a payments-infrastructure choice — and the analysis only makes sense if you understand that “Fiserv” is not one product. It’s a holding company that owns CardConnect, Clover, Carat, and AccessOne, each of which is a different ISV proposition with a different developer portal, a different commercial structure, and a different right-fit profile.

Fiserv scores 3.5/5 in our ISV-focused evaluation. The score reflects two pressures pulling in opposite directions: the platform has structural advantages (seven-bank ISO sponsorship, $21.19 billion in 2025 revenue, the strongest in-person commerce stack in the SMB market) and structural friction (product fragmentation, no unified developer portal, opaque pricing across every line, and the active Clover securities-fraud class action). Where you land on whether 3.5 is generous or conservative depends entirely on which Fiserv product door you intend to walk through.

What Fiserv Actually Is — Four Different ISV Products

The single most important fact for any ISV evaluating Fiserv: there is no unified Fiserv ISV path. When a sales rep says “Fiserv supports ISVs,” they’re using “Fiserv” as a corporate brand spanning four distinct products:

| Product | What it is | Who acquired it | The ISV path |

|---|---|---|---|

| CardConnect | Gateway and payment-processing infrastructure for ISVs | Acquired by First Data in 2017 for $750M; carried into Fiserv via the 2019 merger | ISV Partner Program — embedded payments, white-label, interchange-plus |

| Clover | POS hardware plus commerce OS for SMB verticals | Acquired by First Data in 2012 (NOT a separate Fiserv 2019 acquisition); came inside the First Data deal | Semi-integration (your software talks to Clover hardware) OR full integration (your app runs on Clover’s Android OS via the Clover App Market) |

| Carat | Enterprise omnichannel commerce engine | Built post-merger from First Data + Fiserv enterprise assets | Fortune 500 / large-merchant orchestration only |

| AccessOne | Consumer and patient financing | Acquired 2021 | Healthcare and patient-financing vertical only |

ISVs must pick one. Building a “Fiserv integration” without specifying which product is comparing apples to a fruit basket — the integration model, the commercial structure, the developer experience, and the underwriting flow all differ. For most SaaS and ecommerce ISVs reading this review, the right Fiserv product is CardConnect.

Why this fragmentation exists

Fiserv’s product surface is the result of forty years of acquisitions, then a once-in-a-decade combination. The First Data merger closed July 29, 2019 as an all-stock transaction valued around $22 billion in equity (with First Data’s roughly $17.5 billion in assumed debt pushing total enterprise value substantially higher). Fiserv shareholders ended up with 57.5% of the combined company, First Data shareholders 42.5%, in a deal struck at a 29.6% premium to First Data’s pre-deal share price. Each Fiserv share was exchanged for 0.303 First Data shares.

The strategic logic was a “bank-to-merchant flywheel” — sell Clover into Fiserv’s 12,000+ financial-institution clients, sell merchant services into Fiserv’s bank-distribution network. The acquisitions stacked through both halves of the company brought CardConnect (First Data, 2017), Clover (First Data, 2012), STAR debit network (First Data), and dozens of bank-software assets (Fiserv) into a single roof. The trade-off was the fragmentation. Industry trade analysis through 2025 has consistently described the developer experience as “disconnected” — each product has its own portal, its own authentication, its own residual structure, its own underwriting flow, and no federation spans them.

For ISVs, the practical implication is to treat the Fiserv evaluation as four separate evaluations and pick the one that matches the platform’s merchant profile.

Ownership, Scale, and Leadership

Fiserv is a publicly traded company on NYSE: FI. Full-year 2025 GAAP revenue came in at $21.19 billion (1% Q4 growth and 4% adjusted full-year growth versus 2024 — adjusted revenue $19.80 billion). Net cash provided by operating activities was $6.06 billion in 2025, and the company repurchased 32.2 million shares for $5.6 billion across the year. By scale measures, Fiserv is among the most financially solvent payment infrastructure providers an ISV can build on — the bear-case argument against Fiserv has never been existential risk.

The leadership picture is where the turbulence is. Fiserv has now had three chief executives inside eighteen months. Frank Bisignano, who led the First Data merger and ran Fiserv for years afterward, left to head the U.S. Social Security Administration. His successor, Michael Lyons, resigned as CEO and from the board on June 12, 2026, effective immediately — receiving only accrued base salary, with no severance, no accelerated equity vesting, and no benefits continuation. Fiserv’s Form 8-K states the departure “was not the result of any disagreement with the Company,” language that sits uneasily beside an exit package of nothing.

Two days later, on June 14, 2026, the board appointed Takis Georgakopoulos as Chief Executive Officer. Georgakopoulos had been Fiserv’s Co-President and Head of Merchant and Technology since December 2025, and Chief Operating Officer before that. What matters more for ISVs is where he came from: seventeen years at JPMorgan Chase, the last seven (2017–2024) as Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank. He is, in other words, the executive who spent most of a decade building the payments franchise that absorbed WePay and now competes with Fiserv for exactly the ISV embedded-payments business this page is about.

Then, on July 7, 2026, President Dhivya Suryadevara resigned “for good reason” — the contractual language that signals a constructive termination rather than a voluntary departure. Fiserv lost its chief executive and its president inside four weeks.

For ISVs, the practical implication is blunt. The people who negotiate and honor partner economics have turned over at the top, twice, in a single quarter. Any ISV partner agreement signed under prior leadership deserves re-reading against current ISV Partner Program terms, and any forward commitment — roadmap, rate lock, residual structure — is worth getting in writing from someone who will still be there to honor it.

Operating context for 2025 included multiple rounds of layoffs — Wolfe Research analysts estimated 1,000-1,500 employees in December 2024 alone, with additional rounds reported in July 2025 and December 2025. The financial logic (projected $100-150 million in annualized savings) is real, but the partner-relationship implication — turnover among account managers, residual-team contacts, and ISV-program operators — is a friction worth surfacing in any due-diligence call.

The Clover Securities-Fraud Class Action

This is the elephant in the room, and an honest ISV review has to engage it without overstating it.

There is not one lawsuit. There are two securities class actions and a cluster of shareholder derivative suits, and the cleanest source for all of them is Fiserv’s own Form 10-Q for the quarter ended March 31, 2026, where the company describes the claims against it.

The first action was filed July 24, 2025 in the U.S. District Court for the Southern District of New York against Fiserv, former Chairman and CEO Frank J. Bisignano, Michael P. Lyons, former CFO Robert W. Hau, and Kenneth F. Best. It is brought on behalf of a putative class of purchasers of Fiserv securities from July 22, 2024 to July 24, 2025, and alleges violations of Section 10(b) of the Securities Exchange Act, Rule 10b-5, and Section 20(a). The complaint alleges that statements Fiserv made about the growth of its Clover business-management platform were false or misleading and led to a decline in the share price. Lead plaintiffs were appointed on November 17, 2025, and the case now carries the caption In re Fiserv, Inc. Securities Litigation, No. 1:25-cv-06094.

The second action began as complaints filed on November 4 and November 14, 2025 in the Eastern District of Wisconsin against Fiserv, Lyons, and Hau, covering a different and later class period — July 23, 2025 through at latest October 29, 2025 — and alleging that statements made in connection with Fiserv’s second-quarter 2025 earnings were false or misleading. Those complaints were consolidated on February 5, 2026 under No. 25-cv-1716, and on April 28, 2026 the consolidated action was transferred to the Southern District of New York.

Separately, at least six shareholder derivative complaints have been filed — in the Eastern District of Wisconsin and in the Wisconsin Circuit Court for Milwaukee County — naming Bisignano, Lyons, and other current and former officers and directors, with Fiserv as nominal defendant. They allege breaches of fiduciary duty, Exchange Act violations, and that certain individual defendants are liable for trading in Fiserv stock at artificially inflated prices. Fiserv has also received litigation demands from shareholders directed at its board, and says it may receive more.

Fiserv disclosed an accrual of $26 million for its various legal proceedings as of March 31, 2026, and estimates possible exposure in excess of amounts accrued at $0 to approximately $160 million. Management’s position is that resulting liabilities are “not expected to have a material adverse effect” on its financial statements.

For ISVs, the procedural posture matters more than the headline. As of Fiserv’s most recent quarterly filing, “the defendants have not yet answered or otherwise responded to any of the complaints in these actions.” No motion to dismiss has been briefed, let alone decided. No class has been certified. Nothing has been adjudicated, and Fiserv states it intends to vigorously defend. Any page that presents these allegations as established fact is misreading the docket — the allegations are serious, unproven, and now being litigated by a company whose CEO and president both departed while they were pending.

The lawsuit also targets Clover specifically — not CardConnect. CardConnect operates on a different commercial model (interchange-plus negotiated revenue share, not POS-platform migration economics) and has its own ISV partner program independent of Clover’s POS transition mechanics. ISVs evaluating CardConnect for SaaS embedded payments should know the broader Fiserv operating context but should not let the Clover litigation become a primary objection to the CardConnect path. The risks are not identical.

What ISVs should do: read the partner agreement carefully for language around migration mechanics, ramp commitments, and merchant-attribution disputes; ask the Fiserv partner rep directly whether CardConnect’s ISV partner economics have any cross-dependency on Clover GPV reporting (the answer, based on partner-program structure, should be no, but the question is worth asking explicitly).

CardConnect — The ISV Path Most ISVs Should Evaluate

For SaaS platforms and embedded-payments ISVs, the Fiserv door that almost always matters is CardConnect, accessed through the ISV Partner Program.

What CardConnect is, structurally

CardConnect was acquired by First Data in 2017 for $750 million, and carried into Fiserv via the 2019 merger. The product is a payment gateway plus payment-processing platform with embedded-payments tooling, sub-merchant onboarding APIs, and white-label branding for ISV partners. Within Fiserv, CardConnect is the ISV-facing front of the house — its developer portal lives at developer.cardconnect.com, its sales conversation is partner-led, and its commercial framing is “we make your software a payments product.”

The Fiserv ISV Partner Program

The ISV Partner Program is the formal channel that gives software platforms three things:

- Embedded payments infrastructure — APIs and SDKs for tokenization, sub-merchant boarding, transaction processing, and PCI-scope reduction patterns (hosted iframes, tokenized checkout, redirect flows).

- Performance-tied revenue share — interchange-plus pricing where the ISV earns a portion of the spread between the merchant-facing rate and Fiserv’s cost basis. The exact share is negotiated per partner; it is, in Fiserv’s partner materials, “flexible,” “performance-tied,” and “never set in stone.”

- White-label processor branding — the merchant sees the ISV’s brand on the payment experience, not Fiserv’s. This matters for white-label embedded payments where the platform’s brand owns the merchant relationship.

The program’s named recognitions tell you it’s active and ongoing — CardConnect’s Circle of Excellence 2025 recognized 100GROUP on January 13, 2026 (BusinessWire). That’s a genuine ISV partner roster, not a marketing skin.

What CardConnect doesn’t publish

CardConnect publishes no consumer-facing rate sheet. None of the standard pricing surfaces (a /pricing page with tiers, a /rates page with basis points, a public partnership-economics PDF) exist. Every commercial conversation starts at sales qualification.

The honest editorial take: at high platform-aggregated processing volume (multi-million-dollar annual volume, multi-thousand merchant counts), CardConnect’s interchange-plus typically beats flat-rate alternatives like Stripe Connect’s bundled platform fee — but the negotiation cycle is long and the residual structure is opaque. The April 2024 rate increase (+0.10% + $0.05 across all card networks) is the kind of pass-through change that ISVs should be modeling into their LTV/CAC math; it’s the recurring data point that ISV partners ask about during contract renewals.

For more on the model architecture and what’s actually published, see our Fiserv pricing breakdown.

Clover — The Different Animal

Clover is the most visible Fiserv product, and the one driving most public Fiserv news. For ISVs, it’s also the most situational fit.

What Clover is

Clover is a POS hardware and commerce-OS platform — Android-based countertop terminals, mobile and handheld devices, and a commerce operating system that runs apps on top. The Clover App Market lets third-party developers publish full integrations that run on the merchant’s Clover device, and the Clover developer portal gives ISVs direct access to the OS APIs.

The two ISV integration paths

ISVs interact with Clover in one of two patterns:

- Semi-integration — your software sends payment requests to a connected Clover terminal at the merchant’s location. Your software keeps its own POS/order-management UX; Clover handles only the payment. This is the path for restaurant POS ISVs, salon-management SaaS, fitness platforms, and any vertical where the merchant already wants Clover hardware in front of the customer.

- Full integration via the Clover App Market — your software runs as a Clover-installable app on the merchant’s terminal. The merchant gets the integrated experience without leaving the Clover ecosystem. This is the path when the ISV’s value proposition is “we extend the Clover OS” rather than “we replace it.”

Where Clover wins, where it loses

Clover wins when the merchant base is in-person, vertical-SMB, and benefits from a turnkey hardware-plus-software bundle. The hardware is genuinely good. The Clover App Market has tens of thousands of apps. Vertical SaaS — restaurant POS extensions, retail integrations, service-business scheduling-plus-payments — has a clean integration story.

Clover loses when the ISV is online-first or omnichannel — the OS-level lock-in becomes friction rather than a feature. It also loses when the ISV needs single-pricing transparency — Clover’s pricing is hardware purchase + monthly software-tier subscription + per-transaction rate, all negotiated. And the litigation context (the securities-fraud class action) means ISVs evaluating Clover should read the partner-program economics with extra care around volume-attribution and migration mechanics.

Carat — Enterprise Only

Carat is Fiserv’s omnichannel commerce engine for Fortune-500-class merchants. It orchestrates payment routing, alternative payment methods, fraud, and reporting across web, mobile, in-store, and call-center channels for global merchant programs.

For ISVs, Carat is the right product only if the platform’s merchant roster includes Fortune-1000 enterprises with multi-region, multi-channel, multi-currency programs. Most SaaS ISVs are not in this segment. Carat is what Fiserv built to compete with Adyen at the enterprise-orchestration tier — its target buyer is a global retailer’s payments architect, not a vertical SaaS founder.

The Seven-Bank ISO Sponsorship — Distribution Moat

Per Fiserv’s standard footer disclosure, Fiserv merchant services are delivered through First Data Merchant Services LLC, a registered ISO of:

- Wells Fargo Bank, N.A. (Concord, CA)

- Deutsche Bank AG (New York, NY)

- PNC Bank N.A. (Pittsburgh, PA)

- MVB Bank (Fairmont, WV)

- Pathward, N.A. (Sioux Falls, SD)

- Citizens Bank, N.A. (Providence, RI)

- KeyBank, N.A. (Cleveland, OH)

This is the structural advantage independent gateways cannot replicate at this scale. Each sponsorship contributes underwriting capacity, distribution access, and merchant-program reach. Wells Fargo and PNC alone account for tens of millions of merchant-side and consumer-side relationships that Fiserv can route into.

For ISVs, the practical translation is that Fiserv’s distribution can absorb merchant volume at a scale that pure-play platforms (Stripe at the high end, Adyen at the enterprise tier) compete with but don’t dominate the SMB end of. The trade-off is the underwriting cadence — bank-grade KYC/KYB is more conservative and slower than the gateway-style sub-merchant boarding ISVs get from Stripe Connect Express. ISVs evaluating CardConnect should expect days-not-minutes for the harder sub-merchant approvals, especially in higher-risk verticals.

Where Fiserv Lands Against the Alternatives

Every ISV evaluating Fiserv should benchmark against at least two or three alternatives, and the right comparison depends on which Fiserv product is in scope. The full head-to-head analysis — feature scoring, pricing math, integration depth, and ISV-fit verdicts — lives on the dedicated comparison pages:

- Stripe vs Fiserv — bundled developer-first platform vs. negotiated interchange-plus with seven-bank distribution

- Global Payments vs Fiserv — direct enterprise-acquiring rival, newly enlarged after the January 2026 Worldpay close

- Adyen vs Fiserv — single-platform global enterprise orchestration vs. US-centric multi-product distribution

- NMI vs Fiserv — gateway-first processor-agnostic alternative vs. vertically integrated CardConnect

- WePay vs Fiserv — JPMorgan Payments’ ISV channel vs. Fiserv’s ISV Partner Program

Use those for the actual decision math. Within this review, the high-level shape: pick CardConnect when interchange-plus economics, partner-tied revenue share, and the seven-bank distribution moat outweigh developer-tooling polish. Pick Clover when the merchant base wants Android-OS commerce attachment in restaurant, retail, salon, or service. Pick Carat when the merchant roster is Fortune 1000. Pick anything else when none of those three structural advantages applies to the platform’s roadmap.

Who Fiserv Fits — and Who It Doesn’t

Strong fit for CardConnect

- SaaS and ecommerce ISVs that want embedded payments with interchange-plus economics and partner-tied revenue share

- Platforms that need white-label processor branding so the ISV’s brand owns the merchant relationship

- ISVs with sufficient platform-aggregated volume (typically multi-million-dollar annual processing) to negotiate meaningful CardConnect rates

- Platforms that benefit from seven-bank ISO sponsorship for underwriting reach into hard-to-serve verticals

- ISVs willing to accept longer commercial-negotiation cycles and opaque residual structures in exchange for high-volume economics

Strong fit for Clover

- POS-attached vertical SaaS in restaurant, retail, salon, fitness, and service segments

- ISVs whose value proposition is extending the Clover OS rather than replacing the merchant’s existing POS

- Platforms whose merchants will buy or already own Clover hardware as part of the experience

- Vertical SaaS with a developer team that can publish to and maintain a Clover App Market integration

Strong fit for Carat

- ISVs serving Fortune-1000 enterprise merchants with multi-region, multi-channel, multi-currency programs

- Platforms that need omnichannel orchestration spanning web, mobile, in-store, and call-center

Weaker fit

- Early-stage ISVs prioritizing self-serve speed and developer ergonomics — Stripe, Adyen, or Finix are usually faster

- ISVs whose merchants are price-sensitive on transparent published rates — Square, Stripe, and PayPal publish; Fiserv does not

- Online-first or omnichannel-first SaaS where Clover’s POS-OS lock-in is friction, not a feature

- ISVs without internal sales bandwidth to navigate partner-negotiated commercial structures

- Platforms whose due-diligence buyers will read the Clover securities-fraud class action and decide that’s the headline they need to underwrite — the lawsuit is real, even if it’s not adjudicated, and ISVs whose merchant base is litigation-aware should plan to address it directly in evaluation

Frequently Asked Questions

Is Fiserv a payment processor? Fiserv is a financial technology holding company that owns four ISV-relevant products: CardConnect (gateway and embedded payments), Clover (POS hardware and commerce OS), Carat (enterprise omnichannel orchestration), and AccessOne (consumer/patient financing). Fiserv merchant services run through First Data Merchant Services LLC, a registered ISO of seven sponsor banks (Wells Fargo, Deutsche Bank, PNC, MVB, Pathward, Citizens, KeyBank). For ISVs, the relevant question is which Fiserv product fits — not whether Fiserv as a corporate brand is a “processor.”

Did Fiserv acquire Clover in 2019? No — and this is one of the most common factual errors in published Fiserv coverage. Clover was acquired by First Data in 2012, not by Fiserv. When Fiserv and First Data combined in their July 2019 all-stock merger (~$22 billion equity value), Clover came inside the First Data side of the deal as an existing business. Fiserv did not separately acquire Clover.

Who is Fiserv’s CEO? Takis Georgakopoulos, appointed June 14, 2026. He replaced Michael P. Lyons, who resigned as CEO and director on June 12, 2026, effective immediately, receiving no severance and no accelerated equity vesting. Georgakopoulos previously spent seventeen years at JPMorgan Chase, including seven years as Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank. Fiserv’s president, Dhivya Suryadevara, separately resigned “for good reason” on July 7, 2026.

What is the Clover lawsuit? There are two securities class actions. The first was filed July 24, 2025 in the Southern District of New York against Fiserv, former Chairman and CEO Frank J. Bisignano, Michael P. Lyons, former CFO Robert W. Hau, and Kenneth F. Best, on behalf of purchasers of Fiserv securities from July 22, 2024 to July 24, 2025; it alleges statements about Clover’s growth were false or misleading. Lead plaintiffs were appointed November 17, 2025 and it is captioned In re Fiserv, Inc. Securities Litigation, No. 1:25-cv-06094. A second action, filed in November 2025 in the Eastern District of Wisconsin over Fiserv’s second-quarter 2025 earnings statements, was consolidated as No. 25-cv-1716 and transferred to the Southern District of New York on April 28, 2026. At least six shareholder derivative complaints are also pending. Per Fiserv’s Q1 2026 Form 10-Q, defendants have not yet answered any complaint; nothing has been adjudicated and Fiserv intends to vigorously defend.

Does the Clover lawsuit affect CardConnect? The securities actions center on statements about Clover’s reported growth, and name Fiserv corporate along with current and former executives. CardConnect operates on a different commercial model — interchange-plus, partner-negotiated revenue share, not POS migration economics — and is not directly implicated by the specific allegations. ISVs evaluating CardConnect should understand the broader Fiserv operating context, including the June–July 2026 departures of the CEO and president, but the litigation itself is a Clover question rather than a CardConnect question.

How does Fiserv’s pricing work for ISVs? Fiserv does not publish a rate card for any of its ISV-relevant product lines. Fiserv’s ISV Partner Program is interchange-plus with performance-tied revenue share, partner-negotiated. Clover pricing stacks hardware purchase, monthly software-subscription tiers, and per-transaction rates, all negotiated by merchant. Carat is enterprise quote-only. CardConnect raised processing rates by 0.10% plus $0.05 per transaction across all major card networks effective April 1, 2024.

Who owns Fiserv? Fiserv is a publicly traded company on NYSE under ticker FI. The company merged with First Data in July 2019 in an all-stock transaction valued at approximately $22 billion in equity, with Fiserv shareholders ending at 57.5% and First Data shareholders at 42.5% of the combined entity. Takis Georgakopoulos has been Chief Executive Officer since June 14, 2026, succeeding Michael P. Lyons, who succeeded Frank Bisignano (now head of the U.S. Social Security Administration).

What is Fiserv’s annual revenue? Fiserv reported $21.19 billion in 2025 GAAP revenue (approximately $19.80 billion adjusted, +4% year-over-year) per the company’s Q4 and full-year 2025 earnings release. Net cash provided by operating activities in 2025 was $6.06 billion. Growth has since stalled: in the first quarter of 2026, total revenue fell 2.0% year-over-year to $5.027 billion and operating income fell 34.2% to $918 million, with the Merchant Solutions segment flat at $2.373 billion.

The Bottom Line for ISVs

Fiserv is not one decision — it’s four. The right Fiserv evaluation starts with which product fits the platform’s merchant base, then drills into the commercial structure of that specific product, then layers on the broader operating-context risks: two securities class actions, the layoffs, a first quarter of 2026 in which revenue fell and operating income fell by a third, and a chief executive and president who both left in a four-week window.

For SaaS and embedded-payments ISVs, CardConnect via the ISV Partner Program is almost always the right Fiserv door. The interchange-plus economics, the seven-bank ISO sponsorship distribution, and the white-label branding are real advantages — at the cost of a longer commercial-negotiation cycle and an opaque residual structure. The Clover lawsuit is real but not directly implicating to CardConnect’s ISV channel.

For POS-attached vertical SaaS, Clover remains one of the strongest in-person commerce platforms in the market — provided the ISV is comfortable with the operating-context risk and has the developer bandwidth to maintain a Clover App Market integration.

For Fortune-1000 enterprise commerce, Carat is the right tool. For everything else — early-stage ISVs prioritizing developer speed, online-first platforms, ISVs whose buyers want transparent published rates — Stripe, Adyen, or NMI usually win on operational simplicity even when they cost more on the margin.

For the full pricing model and what’s actually published, see the Fiserv pricing breakdown. For head-to-head decisions, the Stripe vs Fiserv, Global Payments vs Fiserv, and NMI vs Fiserv comparisons map the platform-vs-bundle decision in detail.