What Is an ISV in Payments

Definition

An ISV (Independent Software Vendor) in payments is a software company that builds payment acceptance into its product so merchants can take card, ACH, and digital payments inside the application they already use to run the business — instead of bouncing out to a separate terminal or gateway.

How It Works

The ISV integrates a payment processor, gateway, or PayFac-as-a-Service partner directly into its software. The partner handles transaction processing, settlement, and most compliance work; the ISV controls the merchant's experience — onboarding, checkout UX, reporting — and earns a share of every transaction the platform sends through. Depending on the integration model the ISV chooses, that revenue share can range from 10 basis points (referral) to 100+ basis points (full PayFac).

Why ISVs Care

Payments has become the largest revenue line for many vertical software companies, often eclipsing subscription income. ISVs already generate roughly 60% of US small-and-mid-business acquiring revenue, and McKinsey projects the channel will reach $16 billion in 2025 — up from $6.5 billion in 2020. The integration model an ISV picks decides how much of that economic value it captures, how much compliance burden it carries, and how the merchant experiences onboarding and settlement.

What Does “ISV” Actually Stand For?

ISV stands for Independent Software Vendor. The “independent” part is doing real work in the name — it signals that the software company makes software but does not manufacture the hardware it runs on, and is not owned by the platform vendor whose ecosystem it lives inside. An ISV building a restaurant POS system is independent from Apple, Microsoft, and the card networks the software solutions eventually touch. In banking and payments, the term carries an additional connotation: the ISV is the software provider that uses a payment processor, not one that is a payment processor.

What Is an ISV in Payment Processing?

The short answer to what is an ISV in payments: it’s a software company that has built integrated payments directly into its own platform so merchant customers never have to leave the application to take payment. A field-service ISV embeds a checkout flow into the technician’s mobile app. A salon-management ISV embeds card-on-file billing and recurring payments into the appointment screen. A property-management ISV embeds rent collection into the tenant portal. The merchant signs up for the software, and payments are part of the same product — same login, same dashboard, same support team. When payments are delivered as a built-in feature rather than a referral, the resulting model is also called embedded payments or integrated payments — the two terms are used interchangeably across the industry.

This model has become the dominant distribution channel in US merchant acquiring. ISVs now drive an estimated 60% of US SME acquiring revenue, and the channel is on pace for $16 billion in processing revenue in 2025, up from $6.5 billion in 2020 — a 20% compound annual growth rate over five straight years. TSG (The Strawhecker Group) reports that 82% of the top 50 payments volume listings used the ISV channel in 2025, up ten points from the prior year. Bain projects more than $7 trillion in US payments will flow through software platforms by 2026, compared to $2.6 trillion in 2021.

ISV vs ISO: The Critical Distinction

Independent Software Vendors are routinely confused with Independent Sales Organizations (ISOs), and the distinction matters because the two play very different roles in the payments ecosystem.

| Role | What they sell | Who they work with | Revenue model |

|---|---|---|---|

| ISO | Payment processing services and merchant accounts on behalf of an acquirer | Merchants directly, often with hardware bundles | Residual on transaction fees |

| ISV | Software that includes integrated payment processing | Merchants who buy the software for non-payment reasons | Software fees + payments revenue share |

An ISO sells the payment processing relationship as the product. An ISV sells software where payments are a feature inside it. A growing class of hybrid ISO-ISV providers blends both, but the two pure-play archetypes solve different merchant problems. (For more on the ISO side, see our PayFac vs ISO and payment facilitator entries.)

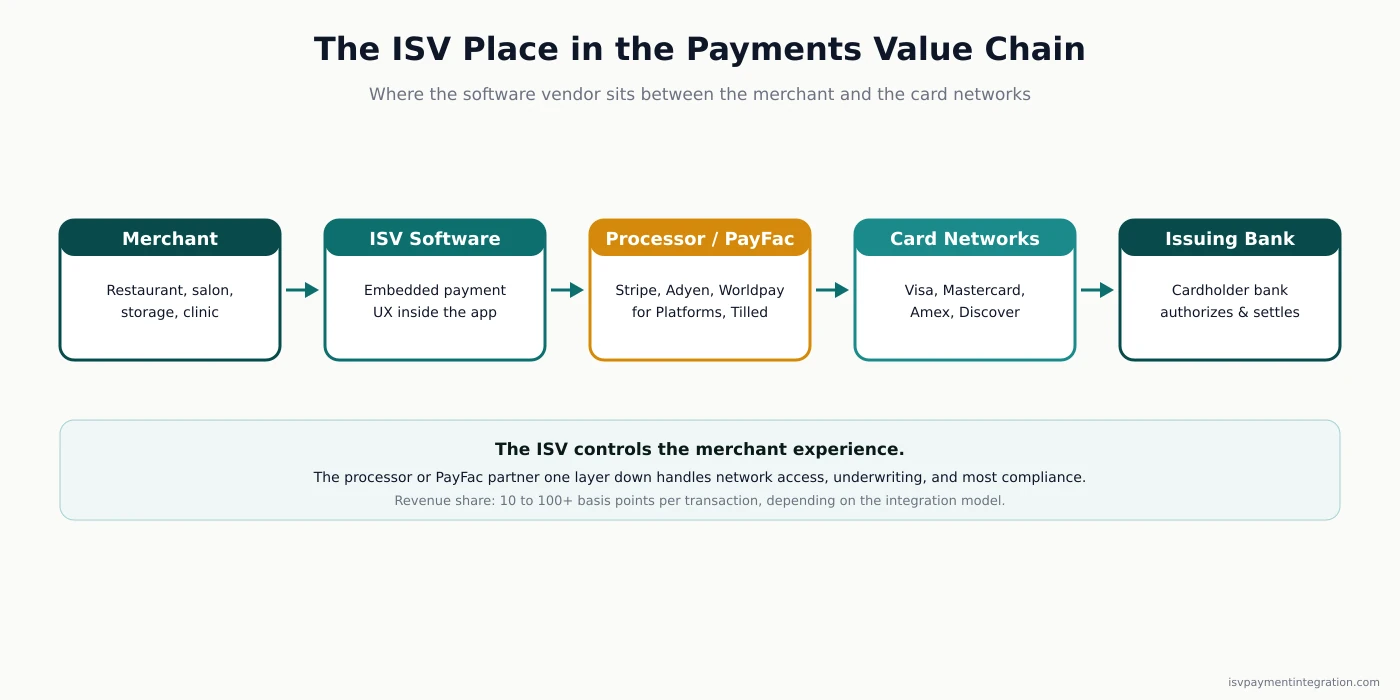

The ISV’s Place in the Payment Ecosystem

ISVs sit between merchants and processors in the integrated payments value chain. Money and data flow through this sequence on every transaction:

Merchant → ISV Software → Payment Processor / PayFac → Card Networks (Visa, Mastercard, Amex, Discover) → Issuing Bank

The software provider’s job is to make that chain invisible to the merchant. Whether the merchant is closing out a dinner ticket, taking a tip, refunding a chargeback, or running a payout to a contractor, the ISV is the surface — and the payment processor or PayFac partner sitting one layer down handles the network access, the underwriting, and most of the compliance work.

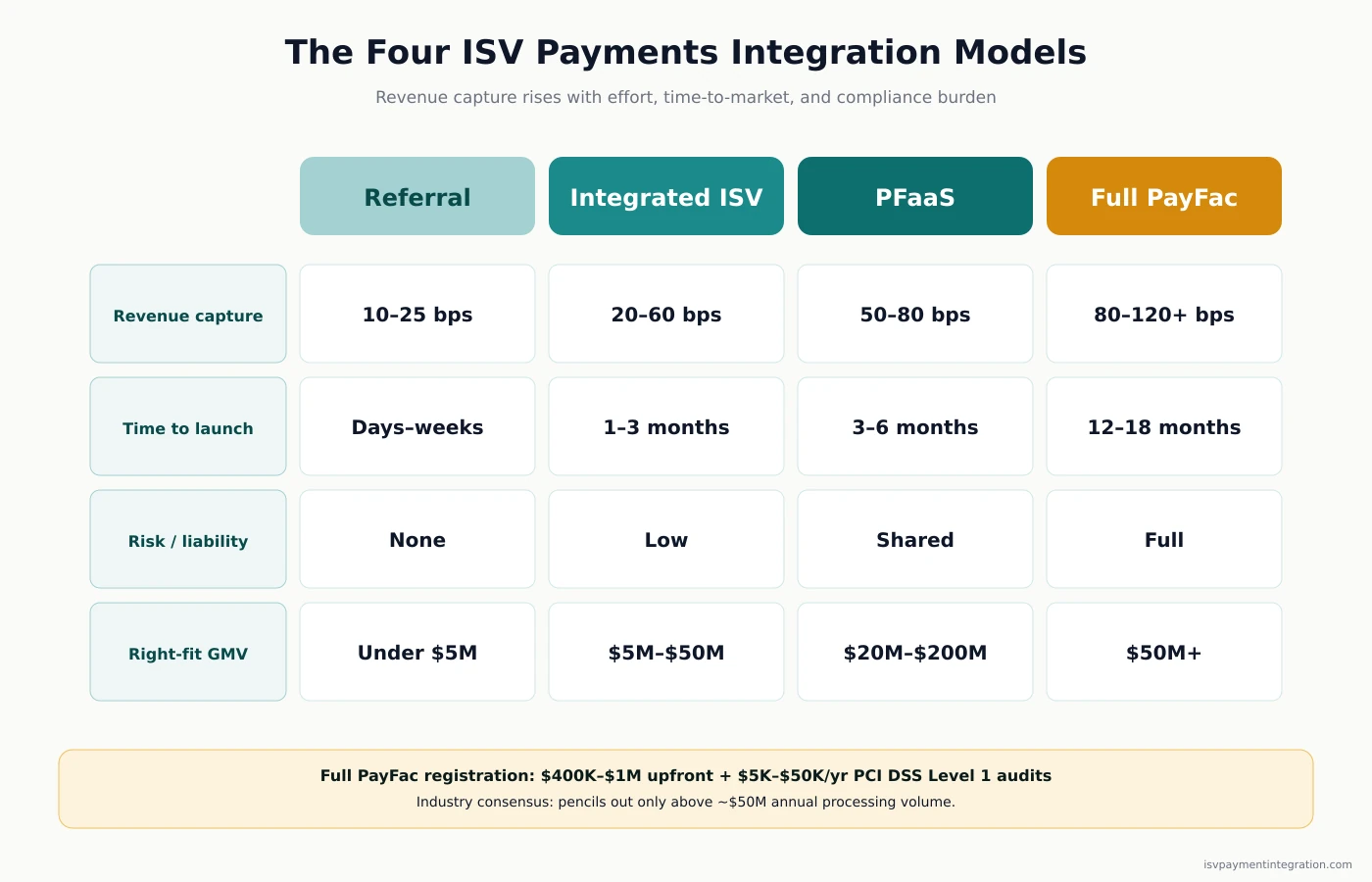

The Four ISV Payment Integration Models

How much of the payments revenue an ISV captures — and how much risk it carries — depends entirely on which integrated payments model it picks. The four ISV payments models map cleanly to a spectrum of effort versus economics.

Referral Partner

The simplest model. The ISV refers merchants to a payments provider and takes a small residual cut, typically 10–25 basis points. The payments provider handles onboarding, underwriting, settlement, and support. The ISV earns money but doesn’t own the relationship. Best fit: ISVs under $5M GMV with no engineering bandwidth for a deeper integration.

Integrated ISV (Gateway Integration)

The ISV integrates the payment processor’s API into its own software so merchants process payments inside the ISV’s interface. Onboarding still flows through the payments provider, but the software vendor controls the user experience and earns 20–60 basis points of split economics. Time-to-market for a typical payment integration lands at 1–3 months. Best fit: ISVs in the $5M–$50M GMV range that want branded integrated payment solutions without taking on PCI DSS Level 1 audit scope.

PayFac-as-a-Service (PFaaS)

The ISV partners with a managed PFaaS provider — Finix, Tilled, Worldpay for Platforms, Xplor Pay’s new platform, Stripe Connect (Custom or Express) — that holds the master merchant ID and absorbs underwriting and compliance, while the software vendor owns the merchant relationship and the user experience. Revenue typically lands at 50–80 basis points of net margin (buying at interchange-plus 10–15bps and charging merchants 2.5–2.9%). Time to launch: 3–6 months. Best fit: ISVs in the $20M–$200M GMV range that want PayFac economics and integrated payments without the registration burden.

Full PayFac (Registered)

The ISV registers as a payment facilitator with the card networks and onboards sub-merchant accounts under its own master merchant ID. Revenue capture is the highest — 80–120+ basis points — but the time-to-market wall is substantial: $400K to $1M in upfront infrastructure and compliance investment, an additional $5K–$50K per year on PCI DSS Level 1 audits, and a 12–18 month launch timeline. The software provider also assumes 100% of fraud and chargeback liability across its sub-merchant portfolio. Industry consensus: registered payment facilitation status only pencils out for software companies above roughly $50M in annual payments volume.

| Model | Revenue (bps) | Time to Launch | Risk / Liability | Right For |

|---|---|---|---|---|

| Referral | 10–25 | Days to weeks | None | Under $5M GMV |

| Integrated ISV | 20–60 | 1–3 months | Low | $5M–$50M GMV |

| PFaaS | 50–80 | 3–6 months | Shared | $20M–$200M GMV |

| Full PayFac | 80–120+ | 12–18 months | Full | $50M+ GMV |

What Makes a Software Company a Good Payment ISV

Not every software vendor should embed payments. Many software companies look at the integrated payments revenue numbers and assume their software solutions are a fit for the model — but only a subset of independent software vendor businesses actually clear the bar. The software companies that succeed as payment ISVs almost always share four characteristics:

- High payments frequency. Their merchants process payments daily or weekly, not occasionally. A restaurant POS software platform sees thousands of payments a week per location; a wedding-planning software platform might see one payment per merchant per quarter.

- Sticky software. The product is mission-critical to the merchant’s day-to-day operations, so switching software providers carries real friction.

- Vertical focus. The software vendor serves a defined industry — restaurants, healthcare, field services, self-storage — well enough to design payments and value-added services around that vertical’s specific needs (tipping, deposits, recurring billing, IOLTA, cash discounting).

- Aggregate scale. Enough merchants and payments volume to make ISV payments revenue meaningful and to negotiate favorable interchange-plus rates with the underlying payments provider or acquirer.

Miss two or more of these and the integrated payments line item rarely earns back the engineering and operational investment.

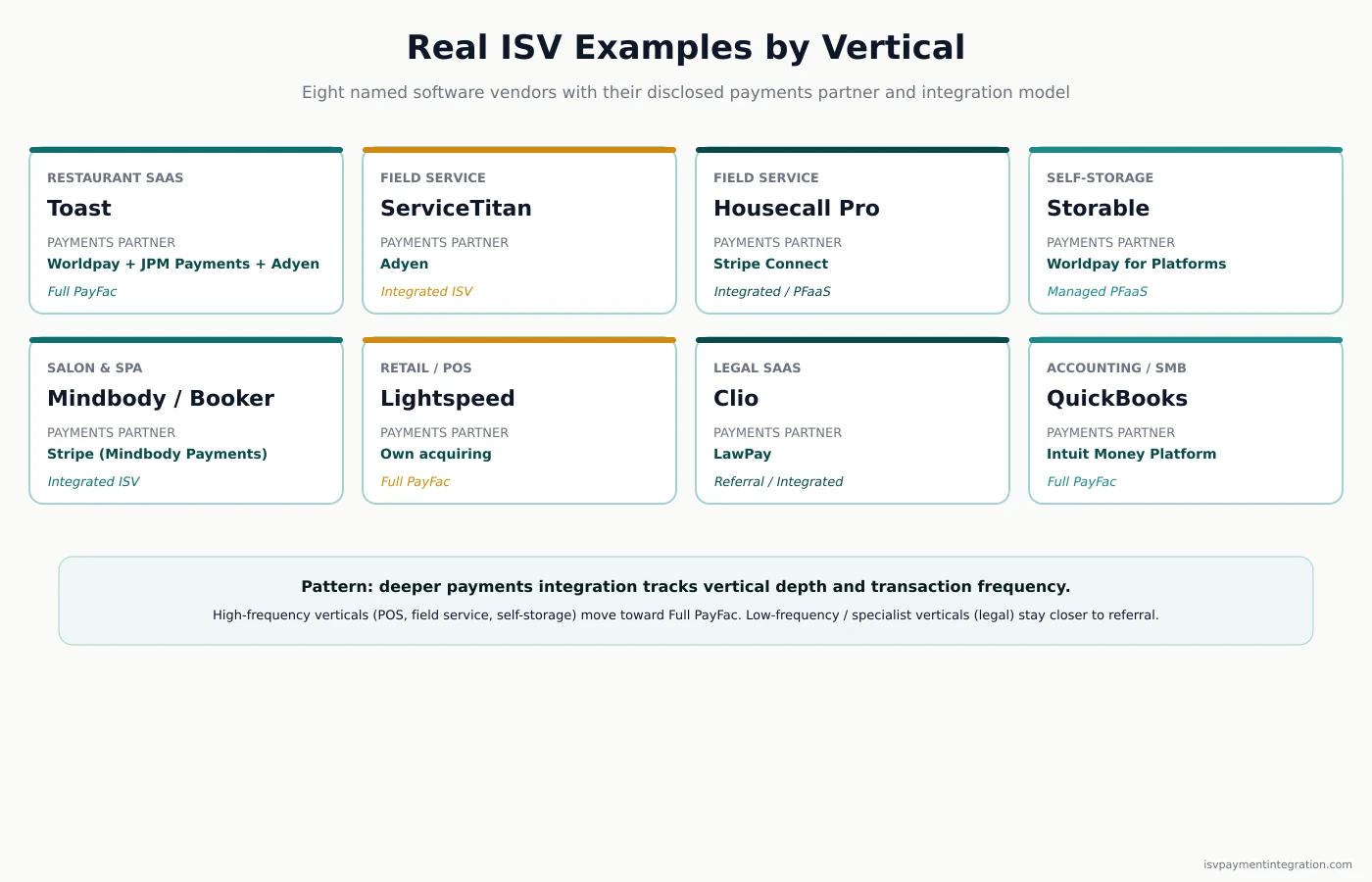

Real ISV Examples by Vertical

The clearest way to understand what an ISV in payments looks like is to name them. These are eight ISVs that have publicly disclosed their payments architecture, with the integration model and the named processor or PFaaS partner each one runs on.

| Vertical | ISV | Payment Partner | Model |

|---|---|---|---|

| Restaurant SaaS | Toast | Worldpay (US) + JPMorgan Payments (US) + Adyen (Europe) | Full PayFac, self-acquiring |

| Field Service | ServiceTitan | Adyen | Integrated ISV (with PayEngine for SoftPOS, Affirm for BNPL) |

| Field Service | Housecall Pro | Stripe Connect (+ Stripe Capital, Stripe Issuing) | Integrated ISV / PFaaS hybrid |

| Self-Storage | Storable | Worldpay for Platforms (formerly Payrix Pro) | Managed PFaaS |

| Salon & Spa | Mindbody / Booker | Stripe (under Mindbody Payments brand) | Integrated ISV |

| Retail / Hospitality POS | Lightspeed | Own acquiring | Full PayFac |

| Legal SaaS | Clio | LawPay | Referral / Integrated |

| Accounting / SMB | QuickBooks | Intuit’s own money platform | Full PayFac |

The pattern across these eight ISV examples: the larger the software vendor’s payments volume and the more central payments are to the product, the deeper into the four-model spectrum it goes. Toast and Lightspeed run their own PayFac registrations because vertical depth and payments frequency justify the compliance overhead. ServiceTitan and Housecall Pro run integrated ISV / PFaaS-hybrid integrated payment solutions that capture most of the economics without the registration timeline. Clio runs a tighter referral-style payment integration with LawPay because the legal vertical’s IOLTA and trust accounting requirements are best handled by a specialist payments provider.

The ISV Payment Revenue Opportunity

The economics of embedded payments are simple and powerful. Take an ISV with 5,000 merchants averaging $30,000 per month in card payments, capturing 30 basis points per payment — a typical integrated payments arrangement.

- Monthly payments revenue: 5,000 × $30,000 × 0.003 = $450,000

- Annual payments revenue: $5.4 million

That payments revenue is incremental to subscription fees and scales with merchant growth without additional sales effort. TSG research has documented cases where ISVs earn up to 10 times more revenue from monetizing payments volume than from software license fees alone. At the same $50M GMV, a referral-only ISV captures roughly $100,000 a year in payments revenue, while a PFaaS-model ISV captures roughly $450,000 — a 4–5x revenue delta, generated by the same underlying payments flow.

Adyen’s platforms business shows the curve at the high end: 31 ISV partners now each process more than €1 billion annually in integrated payments through Adyen for Platforms, and platform integrated payments volume grew 80% year-over-year in the first half of 2025.

PCI Compliance and Chargeback Liability

Embedding payments hands an ISV a compliance and risk burden that most software companies underestimate. PCI DSS Level 1 audits run $5K–$50K a year on top of any registration fees, and the scope of what counts as “card-data environment” expands every time the product evolves. ISVs that go the full PayFac route absorb 100% of fraud and chargeback liability for every sub-merchant on their master merchant ID — a single bad-actor merchant with elevated chargebacks can trigger a portfolio-wide reserve hold by the underlying acquirer, freezing settlement cash flow for the entire book of business. PFaaS providers exist precisely to abstract this burden away in exchange for a basis-point spread.

The 2025–2026 ISV Payments Landscape

The vendor landscape ISVs evaluate today looks materially different from the one they would have evaluated 18 months ago. Five events reshaped the field.

Global Payments closed its $24.25 billion acquisition of Worldpay on January 9, 2026 (announced January 12). The combined entity now serves 6M+ merchant locations, 94B transactions a year, and $3.7T in annual volume across 175+ countries. For ISVs, this matters because Payrix — rebranded to Worldpay for Platforms in September 2022 — is now part of Global Payments’ ISV stack, intensifying competitive pressure on Fiserv’s Clover/CardConnect offering.

Worldpay for Platforms expanded to Canada, the UK, and Australia in July 2025, with CampLife (a Canadian camping vertical SaaS) named the first Canadian customer. Multi-national ISVs that had been limited to US-only Payrix now have a single platform partner across four English-speaking markets.

Clearent by Xplor rebranded to Xplor Pay on July 8, 2025, and used the rebrand to launch a brand-new PayFac-as-a-Service platform aimed at vertical SaaS — moving Xplor Pay from a referral-only legacy footprint into direct competition with Tilled and Finix in the mid-market.

WePay was fully absorbed into J.P. Morgan Payments by mid-2025. The standalone WePay brand is gone; go.wepay.com redirects to J.P. Morgan Payments. JPMorgan positions the integrated offering as an enterprise-tier PFaaS where the bank’s balance sheet absorbs counterparty risk.

A securities class action against Fiserv was filed in the Southern District of New York on July 24, 2025, alleging that Fiserv’s statements about Clover’s growth were false or misleading. The class period runs July 22, 2024 to July 24, 2025, and lead plaintiffs were appointed on November 17, 2025. A second action, over Fiserv’s second-quarter 2025 earnings statements, was consolidated in the Eastern District of Wisconsin and transferred to New York on April 28, 2026. Fiserv’s chief executive and president both departed in June and July 2026. Nothing has been adjudicated. ISVs evaluating Fiserv or Clover should treat the contested migration history as a known platform-stability risk when comparing payment processing options and integrated payments providers.

How to Choose Your ISV Payment Partner

Once an ISV has decided which integration model fits, the payment partner choice within that model comes down to four questions: how much margin do you want to capture, how much compliance burden can you carry, how important is the payments user experience to product differentiation, and what is your aggregate payments volume and trajectory? The current short list of payment solutions competing for ISV business — payments providers, gateways, and PayFac platforms alike — breaks down roughly like this:

- Stripe Connect — developer-first, fastest time to a working integration, broadest ecosystem of value-added services (Capital, Issuing, Tax).

- Adyen for Platforms — enterprise-grade, single integration across 30+ countries, best-in-class card-network direct connections. 31 partners now exceed €1B/year on the platform.

- Worldpay for Platforms — three integration modes (Referral, PFaaS, Full PayFac Developer), now part of Global Payments, expanded to four English-speaking countries.

- Finix — “PayFac without registering” with the Finix Flex stepping-stone path from light integration to full payment facilitation on the same infrastructure.

- Tilled — PayFac-economics-without-registration positioning, ready-made enrollment flows and value-added services.

- NMI — payment gateway-first and acquirer-agnostic, lets ISVs compose their own payment processing stack per vertical.

- Xplor Pay — historical referral footprint plus the 2025 PFaaS platform, increasingly competitive in vertical SaaS.

The right payments partner is the one whose business model makes the ISV’s integrated payments model profitable at the ISV’s actual volume — not the one with the prettiest documentation at sign-up time. Software companies should evaluate every payment partner against their projected payments mix (cards, ACH, recurring), their target geographies, and the integrated payment solutions roadmap they expect to need over the next three years, not just at MVP.

Frequently Asked Questions

What does ISV stand for?

ISV stands for Independent Software Vendor — a company that builds and sells software independent of the hardware it runs on or the platforms it integrates with.

What does ISV stand for in banking?

In banking and payments, ISV refers to a software company that has integrated payment acceptance into its product so merchants can process card, ACH, and digital payments inside the application. The “independent” part of the name distinguishes ISVs from in-house bank software and from Independent Sales Organizations (ISOs), which sell processing services rather than software.

What is an ISV in payment processing?

An ISV in payment processing is a software vendor whose product includes embedded payment acceptance and integrated payments for its merchant customers. The ISV partners with a payments provider, gateway, or PayFac-as-a-Service provider to handle the underlying integrated payments flow, and earns a share of every payment routed through its software — typically anywhere from 10 to 100+ basis points depending on the integrated payments model.

What is an ISV example?

Public examples of ISVs in payments include Toast (restaurant SaaS, full PayFac with Worldpay and JPMorgan Payments), ServiceTitan (field service software, integrated with Adyen), Housecall Pro (field service, on Stripe Connect), Storable (self-storage, on Worldpay for Platforms), Clio (legal SaaS, with LawPay), and QuickBooks (accounting, with Intuit’s own PayFac platform).

Do ISVs need to register as PayFacs to embed payments?

No. Registering as a PayFac is one of four options. Many ISVs use referral, integrated, or PFaaS arrangements where a partner handles registration and risk. Full PayFac registration typically only makes financial sense above $50 million in annual processing volume.