Worldpay Pricing

Pricing model: Interchange-plus (negotiated). Based on publicly available information from Worldpay's official site. Contact Worldpay directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | Interchange-plus pricing. Small-business plan publishes interchange + 0.4% + $0.08 in-person or interchange + 0.5% + $0.25 online for merchants under $50,000/month in card volume. |

| Markup | Negotiated per account for enterprise and ISV integrations. Typical markup band runs 0.30% to 0.50% plus $0.10 to $0.20 per transaction, with the rate tied to aggregate volume, vertical risk, and partnership tier. |

| Setup | Implementation fees may apply. Amounts vary by integration complexity, channel (in-person vs. online vs. omnichannel), and whether the ISV is using Worldpay's embedded payments toolkit or direct API. |

| Monthly | $50 to $100+ monthly service fee typical for full-service accounts. A $35/month minimum processing fee was added across non-flat-rate accounts effective January 2026. |

Hidden Costs to Watch

- ⚠ Early termination fee: $295 to $495 per contract. Some contracts calculate the fee as remaining months multiplied by average monthly fees, which can exceed $1,000.

- ⚠ PCI non-compliance fee: $19.95 to $79 per month if you fail to complete PCI validation.

- ⚠ Chargeback fee: roughly $20 per dispute, charged regardless of outcome.

- ⚠ Cross-border and international card transaction premiums (non-UK/US cards often carry higher fees).

- ⚠ Three-year initial contract with automatic renewal unless you provide 90 days' written notice before expiration.

- ⚠ Fee increases permitted on 30 to 90 days' notice. Negotiated rates are not locked by default.

Alternatives

Worldpay Pricing in 2026: The Global Payments Era

Worldpay is now a subsidiary of Global Payments (NYSE: GPN). The $24.25 billion acquisition closed on January 9, 2026 — the date Global Payments records in its Form 10-Q — and was announced complete on January 12, ending Worldpay’s brief independent run under private-equity owner GTCR and reshaping the processor landscape at the enterprise and ISV tier.

For ISVs evaluating Worldpay today, this matters in three specific ways. First, existing Worldpay contracts stay in force — the brand did not disappear overnight, and worldpay.com still trades under its own name while carrying a “Worldpay is now part of Global Payments” banner. Second, Global Payments put software partners in a named channel of their own. In the same press release announcing the close, the company said it “will go to market through three channels: Enterprise, SMB, and Integrated & Platforms,” each with “tailored sales strategies and distinct product roadmaps.” ISVs live in the third. Third, that channel is real but the plumbing behind it is unfinished: in its Form 10-Q for the quarter ended March 31, 2026, Global Payments told the SEC it “was still in the process of modifying the design of our operating structure to combine the operations of the acquired Worldpay business with our existing Merchant Solutions business,” and that it would not report against a new segment structure until that work completed. The channel exists on the org chart and in the sales motion; the financial reporting has not caught up. An ISV signing in 2026 should ask which entity holds the paper, and who owns the relationship in two years.

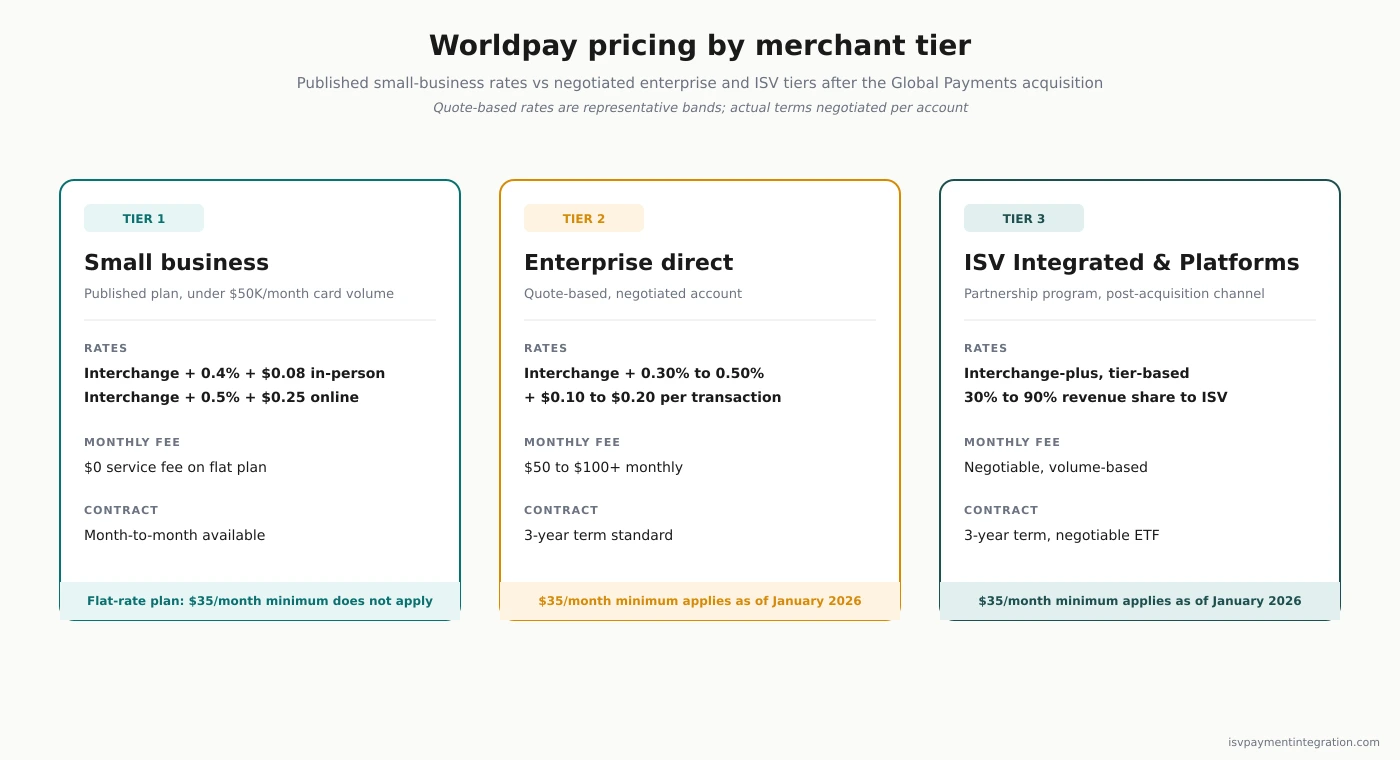

The practical implication: Worldpay pricing in 2026 is a layered conversation. There’s the published small-business plan (transparent, flat-ish). There’s the traditional enterprise interchange-plus plan (quote-based, negotiable). And there’s the newly consolidated ISV partnership program sitting on top of both. The rest of this page breaks down what you actually pay at each layer, the hidden costs that catch ISVs off guard, and how Worldpay’s pricing compares to alternatives worth considering.

How Much Does It Cost to Use Worldpay?

Worldpay publishes two rates for its small-business online plan and negotiates everything else.

For merchants processing $50,000 or less per month in card volume, the published rates are:

- Interchange + 0.4% + $0.08 per in-person transaction

- Interchange + 0.5% + $0.25 per online or manually keyed transaction

Interchange itself depends on the card type and transaction method. A regulated debit card tapped in person costs around 0.05% + $0.22 at interchange. A premium rewards credit card keyed online can cost 2.4% + $0.10 at interchange. Add Worldpay’s markup on top, and effective rates run 1.5% to 3.5% depending on the mix.

For merchants above $50,000 per month, and for ISV partnerships, Worldpay moves to a quote-based interchange-plus model. Typical markups land between 0.30% and 0.50% plus $0.10 to $0.20 per transaction, with the rate tied to aggregate volume, vertical, and partnership tier. Those numbers are negotiating starting points, not floors.

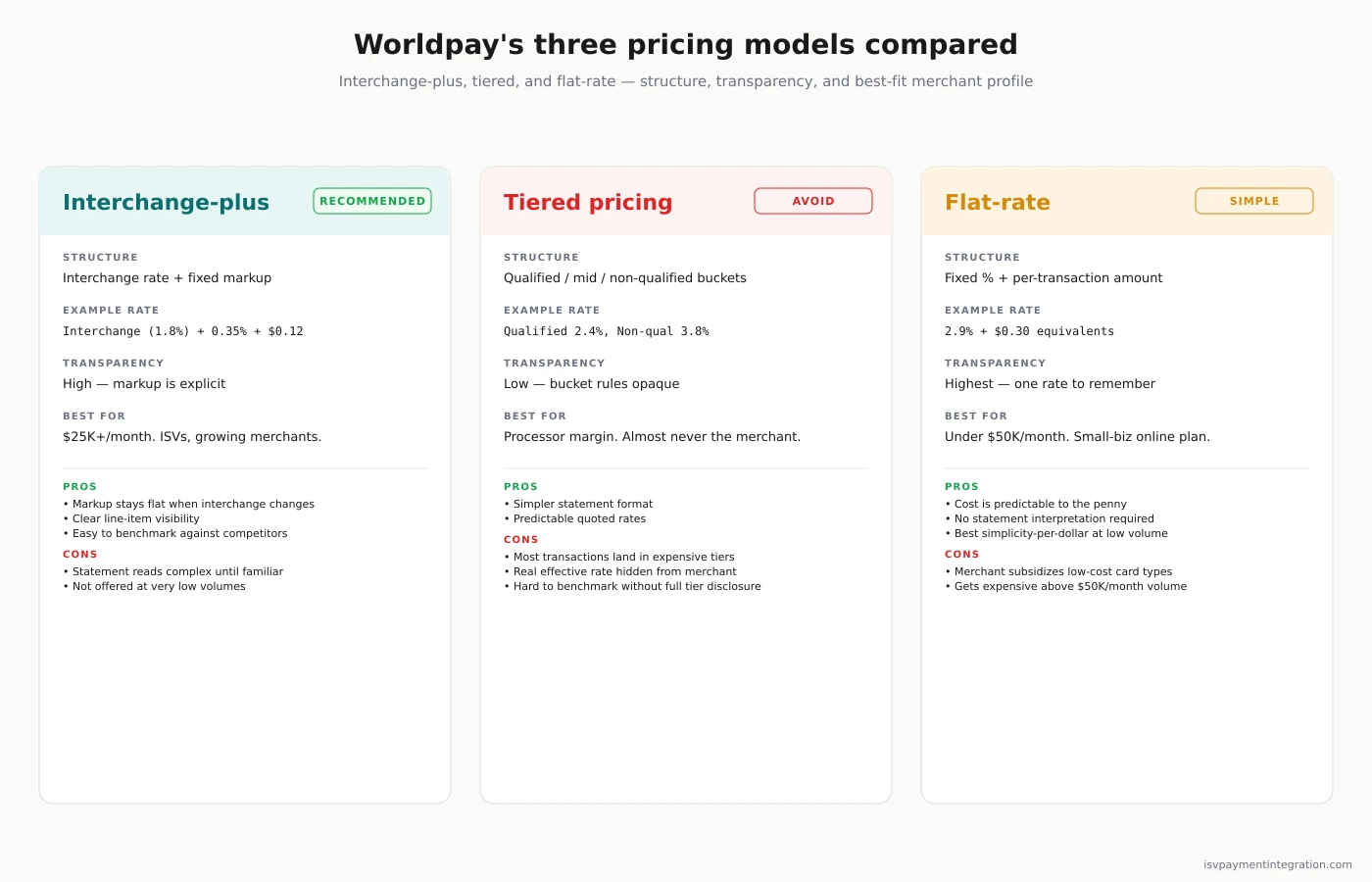

Worldpay’s Three Pricing Models

Worldpay offers — or has historically offered — three distinct pricing structures. Which one you end up on has a bigger impact on your total cost than the per-transaction rate.

Interchange-plus is the most transparent model and the right choice for almost every merchant above $25,000 per month in volume. You pay the exact interchange rate set by Visa, Mastercard, and the other networks, plus Worldpay’s fixed markup. When interchange changes (twice a year, every April and October), your cost changes too — but the markup stays put unless Worldpay sends a separate rate-increase notice. This is the model ISVs should insist on.

Tiered pricing bundles transactions into “qualified,” “mid-qualified,” and “non-qualified” buckets with progressively higher rates. The bucket a transaction lands in depends on the card type and how it was processed, and the classification rules are opaque enough that most merchants never fully understand why their effective rate is higher than the “qualified” rate they were quoted. If your Worldpay statement shows these three tiers, you are almost certainly paying more than you should. Demand a switch to interchange-plus at renewal.

Flat-rate pricing is uncommon on Worldpay but appears on the small-business online plan (where the markup is a fixed percentage + per-transaction amount). Flat-rate is predictable but rarely the cheapest option above small merchant volumes.

Monthly Fees, Minimums, and Recurring Charges

The per-transaction rate is only part of your cost. Worldpay full-service accounts carry a stack of recurring fees that add up fast, particularly at low monthly volumes.

Monthly service fee: $50 to $100 per account is typical for enterprise and ISV accounts. This covers account maintenance, gateway access, and standard reporting. The exact amount is negotiable and should be itemized on your contract.

Monthly minimum processing fee: Effective January 2026, Worldpay applies a $35 monthly minimum to accounts not on the flat-rate small-business plan. If your interchange + markup + other per-transaction fees don’t exceed $35 in a given month, the minimum is assessed to make up the difference. For ISVs with seasonal merchants or new sub-accounts ramping up volume, this adds real cost on low-activity months.

PCI compliance and non-compliance fees: Worldpay assesses a monthly fee for PCI compliance administration (typically included in the service fee) and a separate non-compliance fee — $19.95 to $79 per month — if a merchant fails to complete their annual PCI validation. For ISVs running dozens or hundreds of sub-merchants, non-compliance fees turn into a recurring operational burden.

Chargeback fee: Roughly $20 per dispute, charged regardless of whether you win or lose. Higher-risk verticals (travel, events, subscription services) should budget for these explicitly.

Batch and authorization fees: Small ($0.05 to $0.25 per batch, or per failed authorization) but meaningful for high-volume merchants settling multiple times per day.

Hidden Costs ISVs Should Watch For

The fees above appear on your statement. These next ones are the ones that catch ISVs off guard because they’re either buried in contract language or added through notices most people never read.

Cross-border and international card premiums. Transactions from cards issued outside your home country (non-US for US merchants, non-UK for UK merchants, etc.) carry additional markup on top of standard interchange. For ISVs serving international merchant bases, this is a material line item.

Statement and reporting fees. Some Worldpay contracts charge monthly statement fees ($5-$15) and fees for specific reports beyond the standard set.

Fee-increase clauses. Most Worldpay contracts allow fee increases with 30 to 90 days’ written notice. Without an explicit rate-lock provision in your contract, your “negotiated” rate is a negotiated starting point, not a ceiling. Insist on a rate-lock clause and require written notice with exact dollar amounts — not just “fees may increase.”

Integration and maintenance costs. Developer time for initial integration and ongoing API updates is not a Worldpay line item, but it’s a real ISV cost. Newer gateways (Stripe, Adyen) generally ship fewer breaking changes and have more responsive sandboxes. If your ISV is resource-constrained, factor integration friction into the total cost comparison.

Worldpay Contract Terms: The Three-Year Trap

Worldpay’s standard contract runs three years with automatic renewal unless you provide 90 days’ written notice before the initial term expires. Miss that window and you are locked in for another three years on the same terms.

Early termination fees typically run $295 to $495 per account. Some contracts calculate the ETF as the remaining months in the term multiplied by the average monthly fees for the account — which can push the total well above $1,000 for merchants who leave in year one or two. Read the ETF clause carefully before signing, and negotiate it down or out if you’re bringing meaningful volume.

The three-year term combined with fee-increase clauses is the structural issue for ISVs. Your merchants are locked in, but Worldpay can adjust rates during the term. Counter this by negotiating (a) a written rate-lock provision, (b) an extended notice period for any fee change (60-90 days rather than 30), and (c) a right to terminate without ETF if Worldpay raises the markup beyond a defined threshold during the term.

Is Stripe Cheaper Than Worldpay?

For most small and mid-size merchants, yes — but the answer flips at volume.

Stripe charges a flat 2.9% + $0.30 per online card transaction with no monthly fee, no contract, no PCI non-compliance fee, and no ETF. Worldpay’s published small-business online rate (interchange + 0.5% + $0.25) is comparable on paper — a regulated debit card transaction costs less through Worldpay, and a premium rewards credit card transaction costs more. But Worldpay adds a $50-$100 monthly service fee, the new $35 monthly minimum, and a three-year contract.

The breakeven math for most merchants lands somewhere between $50,000 and $100,000 per month in processing volume. Below that, Stripe’s simplicity and lack of fixed costs usually win. Above it, Worldpay’s interchange-plus markup starts beating Stripe’s flat rate on average transactions — assuming the merchant negotiates well.

For ISVs specifically, the calculation is different. Stripe Connect publishes its platform economics and onboards you in minutes. Worldpay for Platforms publishes its ladder — Referral payments, PayFac-as-a-Service, and PayFac® developer — and invites you to “set your own payments fees,” but it attaches no number to any of it and negotiates the economics deal by deal. That cuts both ways: the ceiling is higher because it is not fixed, and the floor is whatever you fail to negotiate. Expect weeks or months of partnership discussion and integration work rather than an afternoon. See our Stripe vs. Worldpay comparison for the full ISV-lens breakdown.

What Is a 3.5% Transaction Fee?

A 3.5% transaction fee is an effective rate — the total cost of a single transaction divided by the transaction amount. For Worldpay merchants, several scenarios produce a 3.5% effective rate:

- Premium credit cards: Corporate cards, business rewards cards, and signature cards carry higher interchange. A transaction on a Visa Signature Preferred rewards card can hit 2.4% + $0.10 at interchange before any processor markup.

- International cards: A card issued outside your home country adds a cross-border premium on top of standard interchange, often pushing the effective rate above 3.5%.

- Manually keyed transactions: Card-not-present transactions without full verification (AVS, CVV, 3DS) trigger higher interchange categories. A keyed transaction on a rewards card routinely lands at 3.3%-3.8%.

- Low-volume statement fee drag: When a $50 monthly statement fee is spread across $1,000 of processing volume, that alone adds 5% to the effective rate.

A 3.5% rate on specific card types is defensible. A 3.5% average rate across all cards usually indicates a tiered-pricing contract with expensive mid/non-qualified downgrades, or an interchange-plus contract with markup well above market. Both are negotiable.

Is It Legal to Charge a 3% Fee on a Debit Card?

No. Surcharging debit card transactions is prohibited by both Visa and Mastercard network rules, and the Durbin Amendment to the Dodd-Frank Act caps debit interchange for regulated issuers. The prohibition applies to both PIN debit and signature debit.

Credit card surcharging is a different matter. Merchants may legally surcharge credit card transactions in most U.S. states up to 3% (some states cap lower, New York allows up to 4%, and Connecticut and Massachusetts prohibit surcharging entirely). Surcharging requires card network registration, clear disclosure at point of sale, and surcharge amounts that do not exceed the actual processing cost.

For merchants who want to offset processing costs without running afoul of debit surcharge rules, Worldpay supports cash discount programs and dual-pricing models. These reward customers who pay with cash rather than penalizing card users, and they sidestep the debit-surcharge prohibition entirely. If offsetting processing cost matters to your merchants, ask Worldpay’s ISV team about their surcharging and cash discount toolkits before committing to a pricing model.

Worldpay for ISVs: The Integrated & Platforms Channel

Worldpay’s ISV-facing business is Worldpay for Platforms, which lives at platforms.worldpay.com and now absorbs Payrix — the payrix.com domain redirects there, and Payrix survives as a product name rather than a company one. Inside Global Payments, this business sits in the Integrated & Platforms channel. That is not a label we invented for this page: Global Payments used it in the press release announcing the Worldpay close, and again in May 2026 when it announced that “its Integrated and Platforms business has secured the renewal and expansion of its partnership with Lightspeed DMS,” rolling Payrix Pro embedded payments out to Lightspeed’s 4,500-plus dealership customers. That release is the clearest public evidence of what the combined ISV motion actually looks like in practice.

Worldpay’s own site describes three ways a software platform can take payments, and it is worth using its names rather than the generic industry ones:

- Referral payments. Your platform refers merchants; Worldpay owns the merchant relationship, the onboarding, and the risk. The lightest integration and the smallest share of the economics.

- PayFac-as-a-Service. Your platform gets payment-facilitator economics and control over the merchant experience without standing up the compliance and underwriting apparatus yourself. This is where most growing ISVs should be looking.

- PayFac® developer. Your platform becomes the payment facilitator, owning underwriting, compliance, and the merchant experience end to end. The richest economics and by far the heaviest operational and regulatory burden.

Worldpay’s product page advertises configurable fees — the ability for a platform to set its own payments pricing to its merchants — which is the mechanism by which an ISV actually earns on payments rather than collecting a referral cheque.

What Worldpay does not publish is any number attached to any of this. There is no rate card, no revenue-share table, and no public tier threshold for Worldpay for Platforms. The familiar “30-50% / 50-70% / 70-90%” revenue-share ladder that circulates on comparison sites appears in no Worldpay or Global Payments material we can find — not in SEC filings, not in earnings releases, and not on either company’s own product pages. We removed it from this page for that reason. The only number that matters is the one in your quote.

For ISVs evaluating their options, the most important question is not Worldpay’s published rate — there isn’t one — but the effective revenue share after all markup splits and fees. Use our revenue calculator to model the scenarios, and read our full Worldpay ISV review for the capability-side evaluation.

How Worldpay Pricing Compares to ISV-Friendly Alternatives

Worldpay is a scale processor with global acquiring reach and enterprise capability. It’s not a fit for every ISV. Here’s how its pricing compares to alternatives at the dimensions ISVs actually care about.

vs. Stripe: Stripe wins on speed, simplicity, and self-serve onboarding. Worldpay wins on enterprise-scale pricing flexibility, global acquiring reach, and vertical depth. For ISVs under $50M in aggregate platform volume, Stripe is usually the faster and cheaper path. Above that, Worldpay becomes competitive.

vs. Adyen: Adyen publishes its interchange-plus markups (around 0.60% + $0.13 per transaction base), making cost modeling straightforward. See the Adyen vs. Worldpay comparison for the ISV-lens breakdown. Adyen generally offers better API quality and a more modern developer experience; Worldpay has deeper U.S. vertical specialization.

vs. Global Payments: Post-acquisition, these are the same company and the same Integrated & Platforms channel — but not yet the same brand. Worldpay for Platforms and Global Payments Integrated still sell under separate names, and Global Payments Integrated’s own site now carries a banner reading “Global Payments Integrated is transitioning to the Global Payments brand.” Worldpay’s branding has no announced retirement date. If you’re evaluating one, evaluate the other in the same sales conversation, and ask directly which entity holds your contract and who owns the relationship in two years. See Worldpay vs. Global Payments for the current state of the two brands.

vs. Stax: Stax’s subscription-style pricing model (flat monthly fee plus true cost + pass-through interchange) is structurally different. For merchants processing more than $50,000/month, Stax often ends up cheaper on total cost. Worldpay has deeper enterprise capability and international acquiring; Stax is simpler for focused U.S. SMB platforms.

How to Negotiate Worldpay Pricing

Worldpay’s published rates are a starting point, not a ceiling. Here’s how ISVs actually lower the number.

Bring aggregate volume, not a single merchant’s volume. Worldpay prices per account, but ISVs bringing $10M+ in combined platform processing volume have meaningfully more leverage than a single $500K/month merchant. Present your platform’s aggregate numbers upfront.

Demand interchange-plus, not tiered. If a Worldpay contract quote uses “qualified,” “mid-qualified,” and “non-qualified” language anywhere, push back. Insist on interchange-plus with a single, explicit markup.

Request a rate-lock provision. Worldpay’s standard contract allows fee increases on 30 days’ notice. Counter with 60 or 90 days, a dollar cap, and a termination right if Worldpay raises markup during the term.

Negotiate the ETF to zero — or to a specific graduated schedule. Bringing meaningful volume? Ask for no ETF in years two and three.

Get specific about monthly minimums. The new $35 monthly minimum (effective January 2026) applies by default. For ISVs with dormant sub-accounts or seasonal merchants, negotiate it down or out.

Benchmark against live quotes. Get written quotes from Stripe, Adyen, and at least one ISV-friendly alternative like Finix or Payrix. Real competing numbers matter more in Worldpay negotiations than industry benchmarks.

Audit your first three statements. Fees appear on statements that weren’t mentioned in the contract conversation. Line-item the first three months and push back immediately on anything unexpected.

Worldpay can be the right processor for the right ISV — particularly at enterprise scale, with international merchant bases, or in verticals where Global Payments’ depth matters. But the default contract terms favor the processor, not the platform. Walk in knowing the numbers above and what to negotiate, and Worldpay pricing becomes workable. Go in on their terms, and it won’t.