Global Payments Pricing

Pricing model: Interchange-plus (negotiated). Based on publicly available information from Global Payments's official site. Contact Global Payments directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | Interchange-plus with custom markup |

| Markup | Negotiated based on volume and ISV partnership tier |

| Setup | Implementation fees may apply |

| Monthly | Monthly account and gateway fees vary by product line |

Hidden Costs to Watch

- ⚠ Infrastructure Fee (~$450/year as of 2025, up from $229 in 2024)

- ⚠ PCI non-compliance fee (monthly, amount varies by account)

- ⚠ Early termination fee up to $500 on three-year contracts

- ⚠ Annual fee introduced December 2024 (amount not disclosed in advance)

- ⚠ Rate increases bundled with interchange updates (0.20% hike in January 2026)

Alternatives

How Global Payments Prices ISV Partnerships

Global Payments does not publish ISV pricing. That’s the first thing you need to know.

Unlike Stripe (2.9% + $0.30 flat-rate) or Adyen (interchange-plus with published markups), Global Payments negotiates every ISV deal individually through its Global Payments Integrated (GPI) division. Your rate depends on your aggregate platform volume, vertical market, and which partnership tier you fall into.

The base model is interchange-plus with a negotiated markup. Interchange fees are set by Visa and Mastercard, plus the other card networks. Global Payments adds a per-transaction markup on top. For ISVs, that markup is the number you’re negotiating, and it varies widely. A platform processing $50M annually across its merchants will get a very different rate than one processing $2M.

What this means in practice: you can’t comparison-shop Global Payments pricing from their website. You need to talk to their sales team, get a term sheet, and compare it against actual quotes from competitors. If they won’t put specific rates in writing before you sign, that’s a red flag.

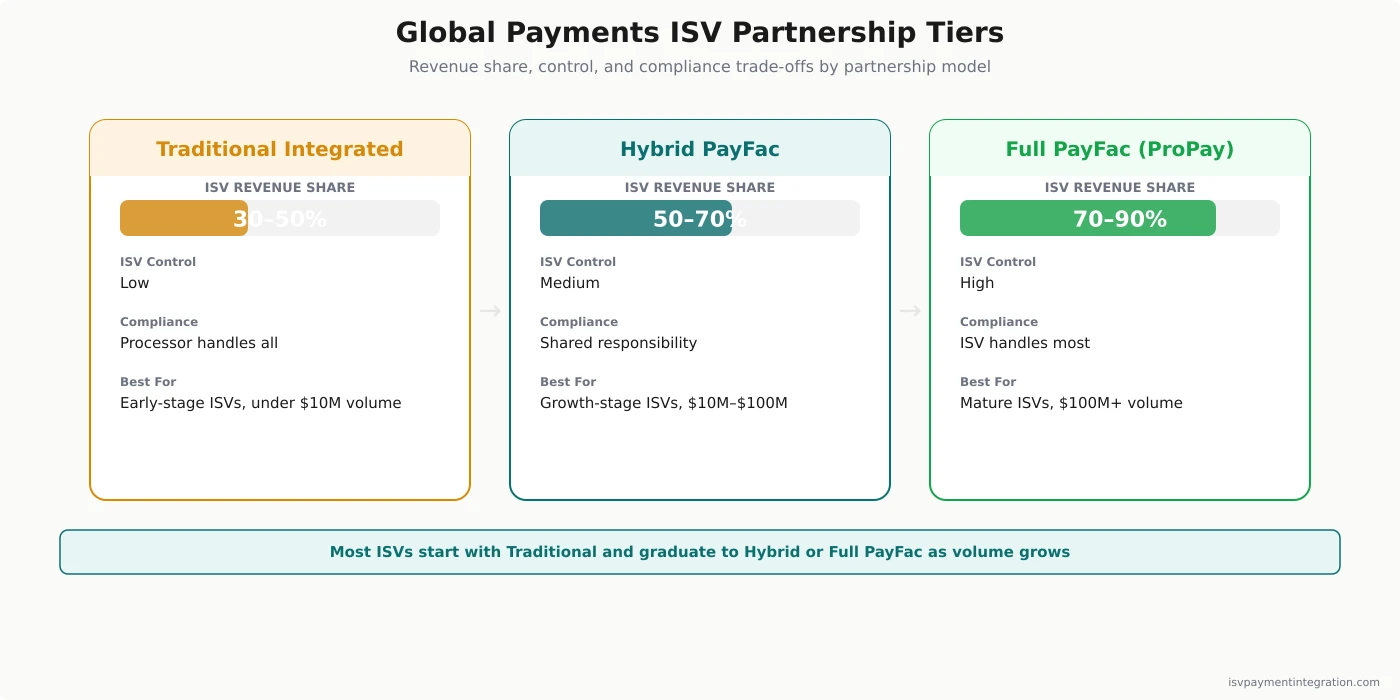

The Three Partnership Models (and What Each Costs)

Global Payments offers ISVs three distinct partnership structures, each with different economics:

Traditional integrated payments puts your ISV in a referral or agent-style relationship. You embed payments, your merchants process through Global Payments, and you earn 30 to 50 percent of the processing revenue. This is the simplest model but leaves the most money on the table.

Hybrid payment facilitation is Global Payments’ middle-ground offering, launched specifically for ISVs who want PayFac-level economics without building compliance infrastructure. You get more control over merchant onboarding and funding, plus better revenue splits than the traditional model. Global Payments handles the compliance, risk management, and underwriting. CEO Cameron Bready described it as getting “all of the gain ISVs perceive come from being payment facilitation businesses, without the pain of actually being a payments company.” The exact revenue share is negotiated, but expect something between 50 and 70 percent.

Full PayFac via ProPay gives ISVs 70 to 90 percent of processing revenue. ProPay (acquired by Global Payments in 2018) provides the payment facilitation infrastructure. You control the full merchant experience, handle more of the compliance burden, and keep the majority of the payment margin. This model makes sense for larger ISVs with dedicated payments teams and enough volume to justify the operational overhead.

The right model depends on where you are as an ISV. Early-stage platforms with under $10M in annual processing volume usually start with the traditional model and graduate to hybrid or full PayFac as volume grows.

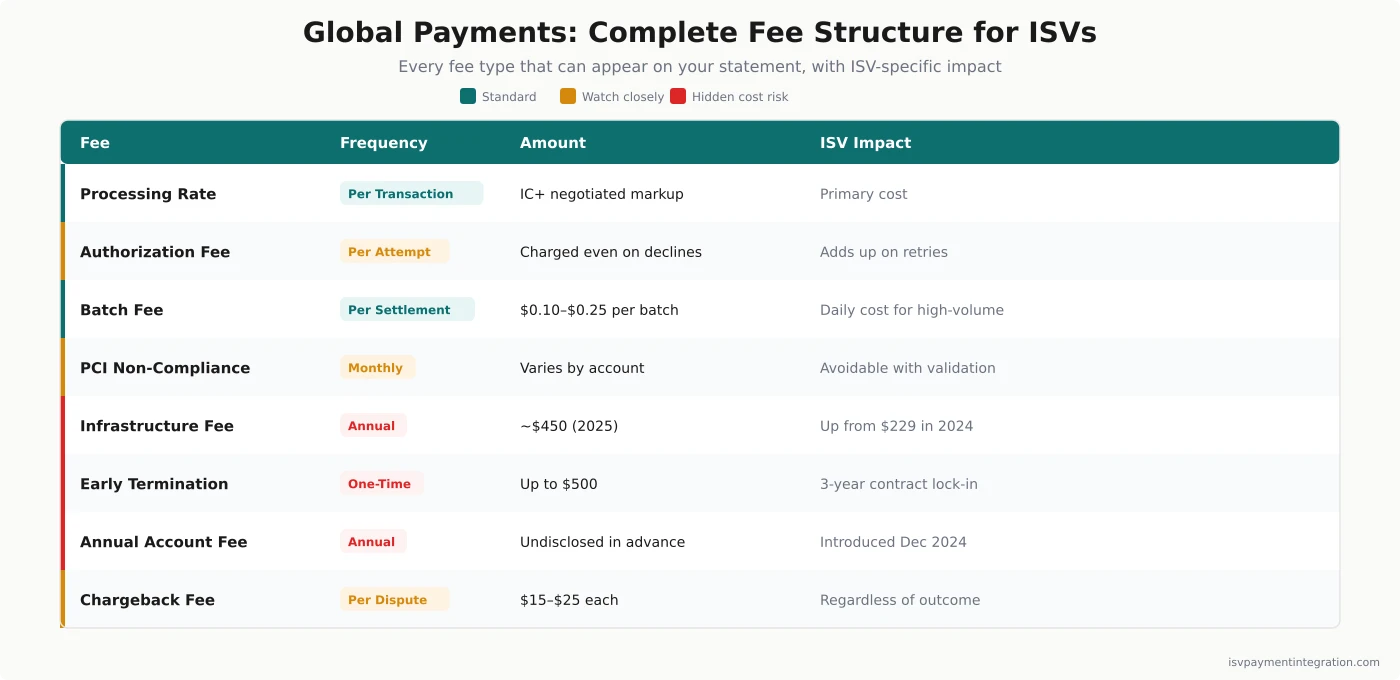

Beyond the Rate: What Else Shows Up on Your Statement

Beyond the per-transaction processing rate, Global Payments charges several recurring and one-time fees. Some appear on your monthly statement. Others show up as separate line items that are easy to miss.

Monthly fees include account maintenance, gateway access, and statement fees. The exact amounts depend on your product line (GPI, Heartland, or ProPay) and your negotiated agreement. Heartland’s published entry-level rate for direct merchants is 2.6% + $0.10 per transaction, but ISVs should be getting rates well below that.

Authorization fees are charged per transaction attempt, whether the charge succeeds or not. Failed authorizations still cost you.

Batch fees apply each time you settle your daily transactions. These are usually small ($0.10 to $0.25 per batch) but add up for high-volume platforms settling multiple times per day.

PCI non-compliance fees hit merchants who haven’t completed PCI validation. If your merchants aren’t staying PCI compliant, you’ll see these on their statements, and they’ll ask you about them.

Chargeback fees are charged per dispute regardless of outcome. Expect $15 to $25 per chargeback. For ISVs in higher-risk verticals (travel, events, subscription services), these add up fast.

Three Costs That Catch ISVs Off Guard

These are the ones that show up after you’ve already signed:

The Infrastructure Fee. In September 2025, Global Payments added a new “Infrastructure Fee” to merchant statements. The notice didn’t specify the amount (a pattern with Global Payments), but most merchants reported being charged around $450. This is up from $229 when similar fees appeared in late 2024. The fee is not tied to any visible infrastructure change on your end.

Early termination fees. Global Payments contracts typically run three years. Walk away early and you could face an ETF of up to $500. That’s not unusual in the industry, but it’s worth knowing before you sign. Ask to negotiate the ETF down or remove it entirely, especially if you’re bringing significant volume.

The annual fee. Starting December 2024, Global Payments introduced an annual fee for merchant accounts. In typical fashion, the notice didn’t include the fee amount. Merchants only found out what they owed when it appeared on their statement. If you’re running hundreds of sub-merchants through your ISV platform, an annual per-account fee adds real cost.

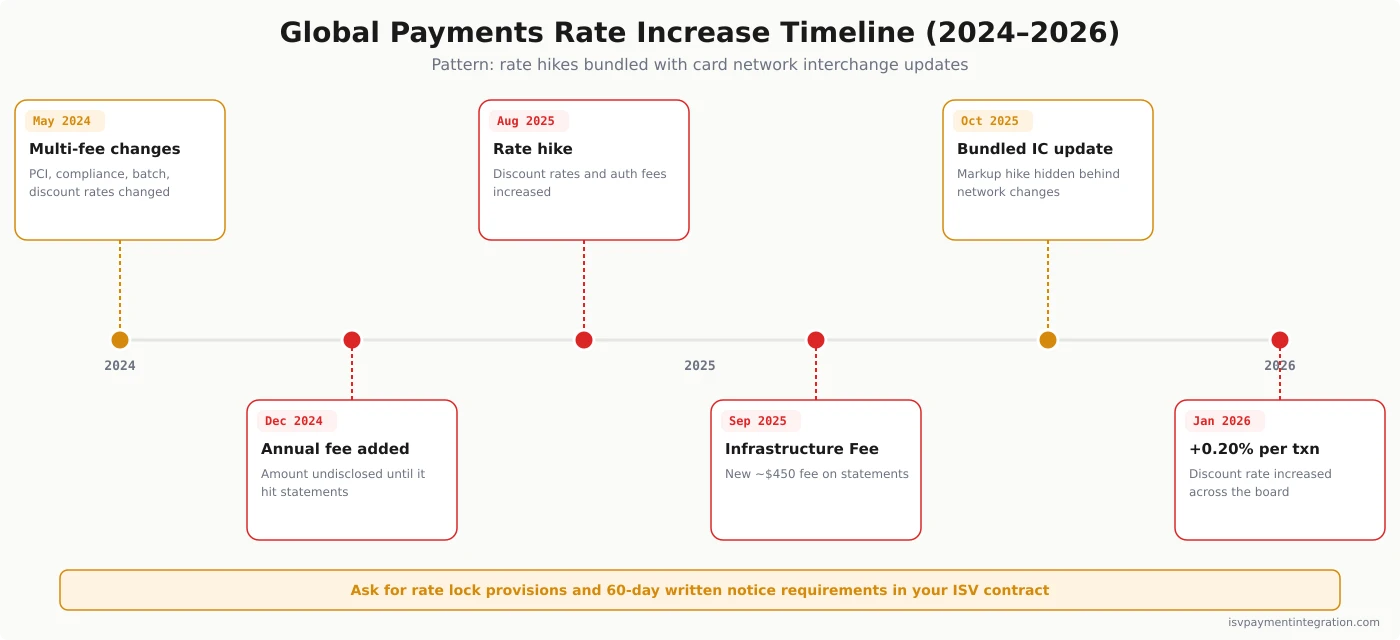

Rate Increase History: What to Watch For

Global Payments raises rates regularly, and the way they do it is worth understanding.

The pattern works like this: Visa and Mastercard adjust interchange categories in April and October each year. Global Payments uses those announcements to send merchants a combined notice that mentions both the network-level changes and their own markup increases in the same communication. The network changes are pass-through costs that every processor forwards. But by bundling their own rate hikes into the same notice, Global Payments makes it look like the entire increase comes from the card networks.

Here’s the recent timeline:

- January 2026: Merchant discount rate increased 0.20% per transaction across accounts not hit by the August 2025 increase

- October 2025: Rate increases bundled with card network interchange adjustments (discount rates, authorization fees, per-item fees)

- September 2025: New Infrastructure Fee added (~$450)

- August 2025: Discount rates, per-item fees, and authorization fees increased (exact amounts not disclosed in advance)

- May 2024: PCI non-compliance fee, network security fee, compliance fee, risk assessment fee, batch fees, discount rates, and per-item fees all changed

If you’re evaluating Global Payments, ask for rate lock provisions in your contract. Get specific language about how and when they can increase your markup, and require written notice with exact amounts at least 60 days before any change takes effect.

How Global Payments Compares on Price

Pricing comparisons between payment processors are misleading if you only look at the per-transaction rate. For ISVs, the math that matters is your net payment revenue after all fees, revenue share, and operational costs.

Here’s how Global Payments stacks up on the dimensions that affect your bottom line:

vs. Stripe: Stripe’s 2.9% + $0.30 flat-rate is simple but expensive at scale. Stripe Connect gives ISVs more transparent revenue sharing, and the API is significantly easier to integrate. But Global Payments can offer lower per-transaction costs for high-volume ISVs willing to negotiate, and the hybrid PayFac model bridges the gap on revenue share.

vs. Adyen: Adyen publishes its interchange-plus markups, making cost modeling straightforward. Adyen’s ISV offering is stronger for platforms with international merchants. Global Payments has deeper vertical expertise in specific U.S. markets (restaurants, healthcare, education).

vs. Finix: Finix offers a pure PayFac infrastructure play where ISVs own the full payment stack. Higher revenue share potential, but you take on more compliance and operational burden. Global Payments’ hybrid model targets ISVs who want better economics than traditional without Finix-level responsibility.

The cheapest processing rate doesn’t always produce the best outcome. A processor charging 5 basis points more per transaction but offering 20% better revenue share will generate more payment revenue for your ISV at any meaningful volume.

Which Product Line Fits Your ISV

Global Payments has grown through acquisitions, and each acquired brand serves different ISV needs. Picking the wrong product line wastes months of integration work.

Global Payments Integrated (GPI) is the primary ISV division. Start here. GPI processes over 1 billion transactions annually and serves 580,000+ merchant customers across 70+ vertical markets. If you’re building a new ISV payment integration, this is your entry point.

Heartland brings deep vertical expertise in restaurants, education, and retail. If your software serves one of these verticals, Heartland’s pre-built integrations and existing merchant base can accelerate your go-to-market.

ProPay is the PayFac infrastructure. If you want to act as a payment facilitator and control the full merchant experience, ProPay handles the underwriting, compliance, and settlement infrastructure. Cross-border capabilities and multiple payout options (wire, debit card, prepaid, globalEFT) make it the right choice for ISVs with international merchants. Use our revenue calculator to model how each partnership tier affects your payment revenue.

Frequently Asked Questions

What revenue share does Global Payments offer ISVs?

It depends on your partnership model. Traditional integrated partnerships pay 30 to 50 percent of processing revenue. The hybrid PayFac model offers better splits (roughly 50 to 70 percent, negotiated). Full payment facilitation through ProPay can reach 70 to 90 percent, but you take on more operational responsibility.

How long are Global Payments ISV contracts?

Most contracts run three years. Early termination fees can reach $500. Negotiate the contract length and ETF before signing, especially if your platform is still validating product-market fit.

Can you negotiate Global Payments’ rates?

Yes, and you should. Rates are not published, and everything is negotiable. Your negotiating position gets stronger with higher aggregate platform volume. Bring competing quotes from Stripe, Adyen, or Finix to the negotiation. Ask for rate lock provisions and written notice requirements for future increases.

What hidden fees should ISVs watch for?

The Infrastructure Fee (~$450/year), PCI non-compliance fees, annual account fees, and bundled rate increases are the most common surprises. Request a complete fee schedule in your contract, and audit your first three statements line by line.