Stripe Pricing

Pricing model: Flat-rate (with custom Interchange-plus available at scale). Based on publicly available information from Stripe's official site. Contact Stripe directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | 2.9% + $0.30 per successful online card transaction (US domestic). Manually entered cards add +0.5%. International cards add +1.5%. Currency conversion adds +1%. Stripe Terminal in-person payments are 2.7% + $0.05. ACH Direct Debit is 0.8% capped at $5. |

| Markup | Flat-rate by default; no interchange passthrough. Custom Interchange-plus pricing available for businesses with large payments volume — typically discussed once aggregate processing exceeds roughly $100,000 per month. |

| Setup | No setup fee on Standard pricing. Custom plans can include implementation work, multi-product packages, and country-specific rates. |

| Monthly | $0 monthly fee on Standard pricing. Stripe Billing adds 0.5% (Starter) or 0.7% (Scale) on recurring revenue. Stripe Tax adds 0.5% per calculated transaction. Custom domain hosting is $10 per month. |

Hidden Costs to Watch

- ⚠ Disputes now carry two $15 fees: a non-refundable 'received fee' charged on every dispute, and a 'counter fee' that is refunded if you win — meaning a contested win still costs $15, and a contested loss costs $30 (effective June 17, 2025).

- ⚠ Refunding a payment does not return the original 2.9% + $0.30 processing fee. Stripe sunset fee returns on refunds for new accounts in April 2020 — every refund is a permanent margin leak.

- ⚠ Instant Payouts in the US cost 1.5% of payout volume with a $0.50 minimum. Stripe raised this from 1% effective June 1, 2024 — non-US accounts (EU, UK, Canada, Singapore) still pay 1%.

- ⚠ Stripe Connect platforms that deploy their own payments pricing pay a 0.25% application fee starting threshold. Express and Custom connected accounts add $2 per active account per month plus $0.25 per payout.

- ⚠ International card transactions and currency conversion stack: a US merchant accepting an EU card paid in EUR pays 5.4% + $0.30 (2.9% base + 1.5% international + 1% FX) on every transaction.

- ⚠ Radar for Fraud Teams costs $0.02 per screened transaction on Standard pricing or $0.07 on custom pricing. Standard Radar ML is included; the version with custom rules and review queues is the line that adds up at million-transaction scale.

- ⚠ Managed Payments (Stripe's merchant-of-record solution) adds 3.5% per successful transaction on top of the standard payments fee — useful for global tax compliance, costly if you don't need it.

- ⚠ Volume discounts and custom rates require multi-year commitments and often include exclusivity clauses that prevent splitting volume across multiple processors.

Alternatives

Stripe Pricing in 2026: The Headline vs. Your Real Effective Rate

Stripe pricing shows one number: 2.9% + $0.30 per successful transaction. That number is technically correct and almost universally misleading.

A US merchant accepting US-issued credit cards in USD, with no recurring billing, no tax automation, and no platform layer on top, pays close to that headline. For everyone else — especially ISVs and SaaS platforms embedding a payment processor into software — the real effective payment processing rate stacks well above 2.9%.

A US-based SaaS company selling globally in USD, using Stripe Billing for subscriptions, Stripe Tax for VAT compliance, accepting EU-issued credit card payments, and protecting against chargebacks pays a blended 7.8% per transaction — almost three times the published rate. That number comes from Freemius’s 2026 model and matches independent calculations from Dodo Payments and Swipesum.

This page breaks down every Stripe fee that touches an ISV deal in 2026: what Stripe pricing actually covers across payment methods, where the hidden payment processing costs hide, how Connect changes the math for platforms, and what your real total cost looks like once the full fee stack is in view.

How Much Does Stripe Charge as a Fee?

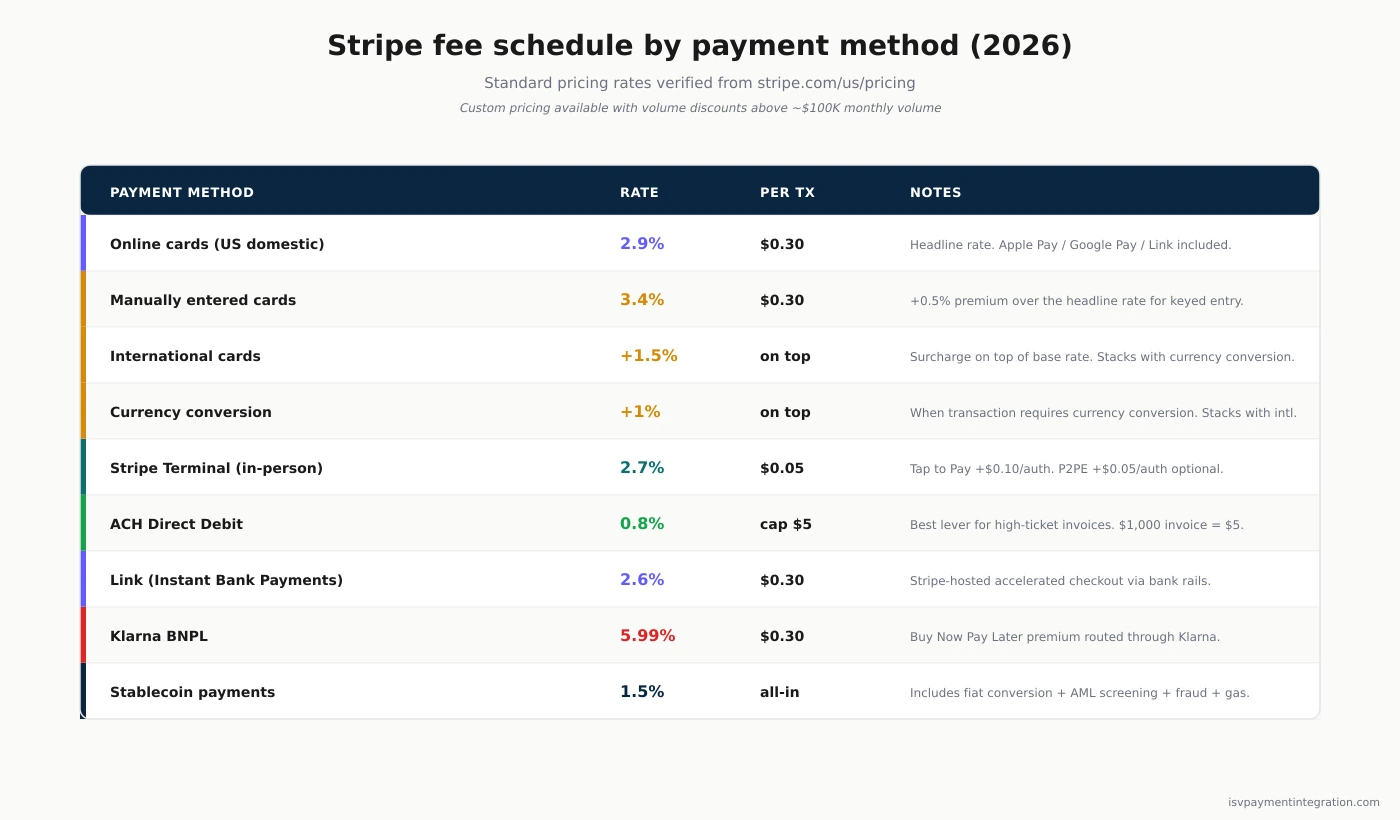

Stripe charges different transaction fee rates by payment method, channel, and card origin. The Standard plan covers all major payment methods with published processing fees and no monthly fees on the base plan.

Online credit card payments (the headline rate)

2.9% + $0.30 per transaction for domestic credit and debit cards, including Apple Pay, Google Pay, and Link (Stripe’s accelerated checkout). This rate applies to US-issued credit card transactions processed online with no manual keying. It is the number every “Stripe fees” article quotes.

Manually entered cards

2.9% + $0.30 + 0.5% when the credit card is keyed by hand instead of dipped, tapped, or autofilled. Many guides round this up to “3.4% + $0.30,” which is the same math expressed as a single rate. The 0.5% premium reflects elevated fraud risk on keyed credit card transactions.

International cards

+1.5% surcharge on top of the base rate when a customer pays with a card issued outside the merchant’s country. Every European, Asian, or Latin American card adds 1.5% before currency conversion enters the picture. International cards from any non-domestic issuer trigger this surcharge.

Currency conversion

+1% if the transaction requires currency conversion (for example, a US merchant pricing in USD but accepting EUR settlement). This stacks with the international card surcharge.

In-person payments (Stripe Terminal)

2.7% + $0.05 per transaction for credit cards and digital wallets accepted through Stripe Terminal. International cards still add 1.5%. Tap to Pay adds $0.10 per authorization. Point-to-point encryption adds $0.05 per authorization. Hardware: $59 (Reader M2) or $299 (S700 / S710), with cellular at $10 per reader per month.

ACH Direct Debit

0.8% capped at $5 per transaction. For a $1,000 invoice, ACH Direct Debit costs $5 versus $29.30 on a card — a $24 swing per payment. ACH is the single biggest lever for businesses with high-ticket invoices billed to a customer’s US bank account.

Link, Klarna, and other payment methods

Link (instant bank account payments through Stripe’s wallet) is 2.6% + $0.30. Klarna Buy Now Pay Later is 5.99% + $0.30. Stablecoin payments are 1.5% all-in including conversion to fiat. Bank transfers, Boleto, OXXO, and other locally relevant payment methods carry their own published rates. Each payment method has its own per transaction fee structure.

How Much Is the Stripe Fee for $100?

A $100 transaction is the easiest way to see how the per transaction fee structures stack across payment methods.

| Scenario | Stripe fee | Effective rate |

|---|---|---|

| US credit card, paid in USD | $3.20 | 3.2% |

| Manually entered credit card | $3.70 | 3.7% |

| International card, paid in USD | $4.70 | 4.7% |

| EU card, paid in EUR (US merchant) | $5.70 | 5.7% |

| Stripe Terminal in-person | $2.75 | 2.75% |

| ACH Direct Debit, $100 invoice | $0.80 | 0.8% |

| Klarna BNPL | $6.29 | 6.29% |

The 5.7% effective on the EU-card-paid-in-EUR case is the one most ISVs underestimate. It’s 2.9% base + 1.5% international + 1% currency conversion + the $0.30 fixed fee. For a SaaS company with 20% European volume, that single line moves the blended rate 50 basis points or more.

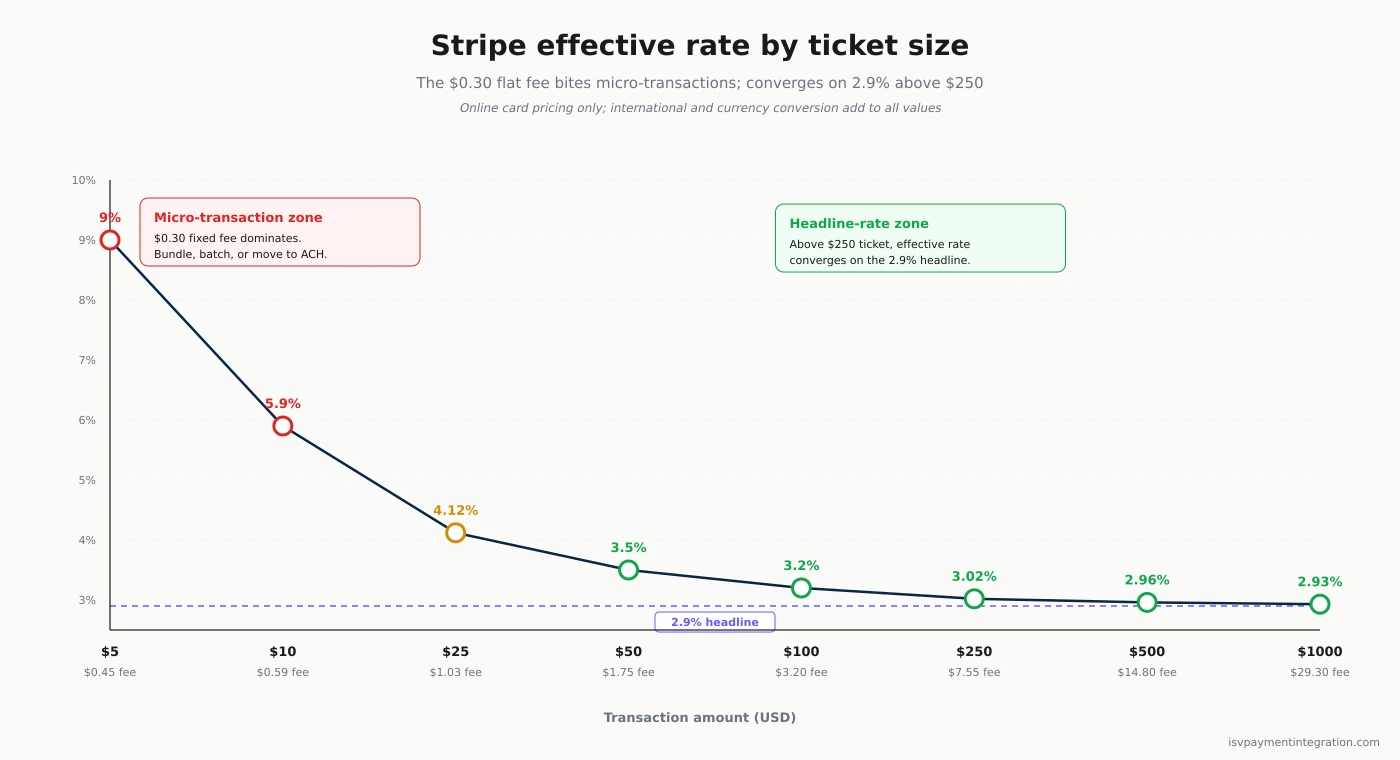

The small-ticket trap

The 30-cent fixed fee bites hardest at low transaction values. A $5 sale costs $0.45 in Stripe fees — a 9% effective rate. A $10 sale costs $0.59, or 5.9%. For micro-transaction businesses (pay-per-use APIs, low-cost digital goods, tipping platforms), the flat fee makes the published rate look nothing like the real cost. Bundle small credit card transactions, set minimum order amounts, or move recurring invoices to ACH to escape the trap.

How Expensive Is It to Use Stripe?

The honest answer depends on credit card transaction mix, not headline rate.

A US e-commerce store doing $25,000 in monthly volume with a $75 average ticket pays roughly $824 per month in Stripe charges — about $9,900 per year. A SaaS business at $50,000 MRR with a $99 average subscription pays around $1,600 per month. A service business invoicing $100,000 monthly at a $500 average ticket pays roughly $2,960 per month.

Those numbers assume domestic credit card payments, no international payments, no recurring billing fees, no tax automation, no disputes. The moment any of those assumptions break, payment processing cost climbs.

The single biggest variable is product mix. A merchant using only Stripe’s payment processing on the Standard plan stays close to the 2.9% + $0.30 headline. Merchants using Stripe Billing, Stripe Tax, Radar for Fraud Teams, and Connect — what most modern SaaS platforms actually need — add 1.5% to 5% on top before international payments or currency conversion surcharges. The next section breaks the stack down line by line.

The Hidden Stripe Fees That Compound at Scale

These hidden Stripe fees don’t show up in pricing comparisons but do show up on your monthly statement, and they materially shift the per-transaction math at scale.

Disputes and chargeback fees (the new dual-fee model)

As of June 17, 2025, Stripe restructured dispute pricing. Every chargeback carries a non-refundable $15 received fee, charged whether you contest or not — a flat transaction fee on top of the original processing cost. If you contest, Stripe adds a separate $15 counter fee, refunded only if you win and forfeited if you lose. The math:

- Dispute you don’t contest: $15 (received fee, lost regardless)

- Dispute you contest and win: $15 (the counter fee comes back)

- Dispute you contest and lose: $30 (both fees forfeited)

The old structure was a single $15 chargeback fee returned on a win. The new structure means even the most disciplined dispute response operation pays $15 per case.

Refund fees: the original processing fee never comes back

When you refund a customer, Stripe keeps the original 2.9% + $0.30 transaction fee. This policy went into effect April 2020 for new accounts and was sunset for legacy accounts on September 1, 2020. For high-refund verticals — apparel, event ticketing, SaaS trials that cancel late — every refund is a permanent margin leak. A 5% refund rate on $1M annual processing is roughly $1,450 in unrecovered Stripe fees. See Stripe’s policy on refunded payments for the official statement.

Instant Payouts: 1.5% (and yes, it went up)

Stripe raised US Instant Payouts from 1% to 1.5% of payout volume effective June 1, 2024 — a 50% rate increase. The minimum stayed at $0.50 per payout. Non-US accounts (EU, UK, Canada, Singapore) remained at 1%. The change drew sustained complaints in Hacker News thread 40423035, with one founder noting the new rate “killed the motivation to use it entirely.”

For high-frequency payout businesses — creator marketplaces, gig platforms, content monetization — the change moved real money. Plan your payout cadence around the standard schedule (free) unless the cash flow benefit truly clears 1.5%.

Other line items that add up

- Wire payments funding Treasury balances: $2 per wire (separate from credit card processing)

- Custom domain hosting on Payment Links or Checkout: $10 per month

- Post-payment invoices: 0.4% on transaction total, capped at $2 per invoice

- Foreign Exchange Quotes API: 1% per transaction, plus 0.07% rate locking

- Shared Payment Tokens: $0.15 per token issued

None of these wire payments and ancillary fees are large in isolation. Together, they explain the gap between the published rate and the line items on your monthly Stripe statement.

Stripe’s Pricing Model: Standard vs. Custom

Stripe runs two pricing tiers for the underlying payments product.

Standard pricing

Pay-as-you-go with no setup fees, no monthly fees, no minimums. The rates published on stripe.com/pricing are what you pay. Standard works well for businesses under roughly $100,000 in monthly card volume, single-currency operations, and merchants who value transparency over rate optimization.

Custom pricing

Stripe offers custom pricing for businesses with large payments volume or unique business models. A custom package typically includes:

- Interchange-plus (IC+) pricing — pass-through interchange + a fixed Stripe markup

- Volume discounts at defined tiers; the bigger volume discounts unlock once aggregate volume crosses key breakpoints

- Country-specific rates and tailored fee structures for global businesses with multi-currency settlement

- Custom payment processing terms for unusual settlement, payout, or risk profiles

The published threshold (“large payments volume”) is loose, but practitioner reports put the real bar at roughly $100,000 per month in processed volume, with meaningful rate concessions starting closer to $1M+ annual processing. Multi-year commitments of 24 to 36 months typically unlock lower effective rates.

The negotiation reality (a case study)

The most-cited public negotiation post-mortem is Ajay Goel’s GMass story, which documents a 12-month back-and-forth that produced a headline rate cut from 2.9% to 2.2%. The catch: Stripe layered a Billing surcharge, kept the refund non-return policy, and required a 36-month exclusive. Goel’s net effective rate barely moved. The playbook for any ISV negotiating a custom package: model total cost, not the per-transaction rate.

Stripe Billing: What ISVs Pay for Subscription Management

Stripe Billing is priced as a percentage of recurring revenue on top of standard processing fees.

The two Billing plans

- Starter: 0.5% of recurring revenue

- Scale: 0.7% of recurring revenue

Both Stripe Billing plans include subscription management, invoicing, dunning, proration, customer portal, and the metered-billing primitives that drive usage-based pricing models.

When Billing stings

At $1M ARR, the 0.5% Starter rate adds $5,000 per year. At $5M ARR, the 0.7% Scale rate adds $35,000 — often more than a full Chargebee or Recurly seat with comparable functionality. SaaS companies past $5M ARR routinely evaluate migrating billing infrastructure (not payments) off Stripe to recover the percentage point.

The decision isn’t purely cost. Stripe Billing’s deep integration with Stripe Tax, Sigma reporting, and Connect creates operational lock-in. For ISVs reselling subscription billing, the Billing fee is part of the cost basis being recovered through platform fee structures — build it into the pricing model from day one.

Stripe Terminal Pricing for In-Person Payments

Stripe Terminal is the in-person payments product, useful for ISVs whose software touches a physical point of sale and accepts contactless payments alongside chip-and-PIN.

Per-transaction rates

- 2.7% + $0.05 per transaction for domestic cards and wallets

- +1.5% for international cards

- +$0.10 per authorization for Tap to Pay (Apple Pay / Google Pay on phone)

- +$0.05 per authorization for optional point-to-point encryption (P2PE)

Hardware

- Stripe Reader M2: $59

- Stripe Reader S700 / S710: $299

- Cellular data on enabled readers: $10 per reader per month

When Terminal makes sense for ISVs

For software platforms whose merchants accept in person payments alongside online — restaurant POS, field service, retail SaaS, ticketing — Terminal lets you maintain a single Stripe integration across channels. The in-person rate beats online by 20 to 25 basis points on percentage and 25 cents on the fixed fee. For high-volume merchants who accept in person payments daily, the gap is material. The trade-off is hardware logistics: ISVs distributing readers at scale need to budget device cost, shipping, replacement cycle, and cellular into the embedded payments offering.

Stripe Radar Pricing: Free vs. Fraud Teams

Stripe Radar is the fraud prevention layer that ships with Stripe Payments. The pricing splits into two tiers.

Standard Radar (machine learning) — Included at no additional charge for accounts on Standard payments pricing. Radar’s baseline ML scores every transaction using signals from Stripe’s network and blocks high-risk payments automatically. Custom-pricing accounts pay $0.05 per screened transaction.

Radar for Fraud Teams (custom rules and review) — The version with custom rule logic, allow/block lists, and a manual review queue costs $0.02 per screened transaction on Standard plans or $0.07 on custom pricing. A 30-day free trial is available.

At 1 million screened transactions per year, Fraud Teams costs $20,000 (Standard) or $70,000 (custom) — material annual line items. Most ISVs budget Radar for Fraud Teams as a fixed cost per merchant served, then decide whether to absorb it or pass it through based on risk vertical.

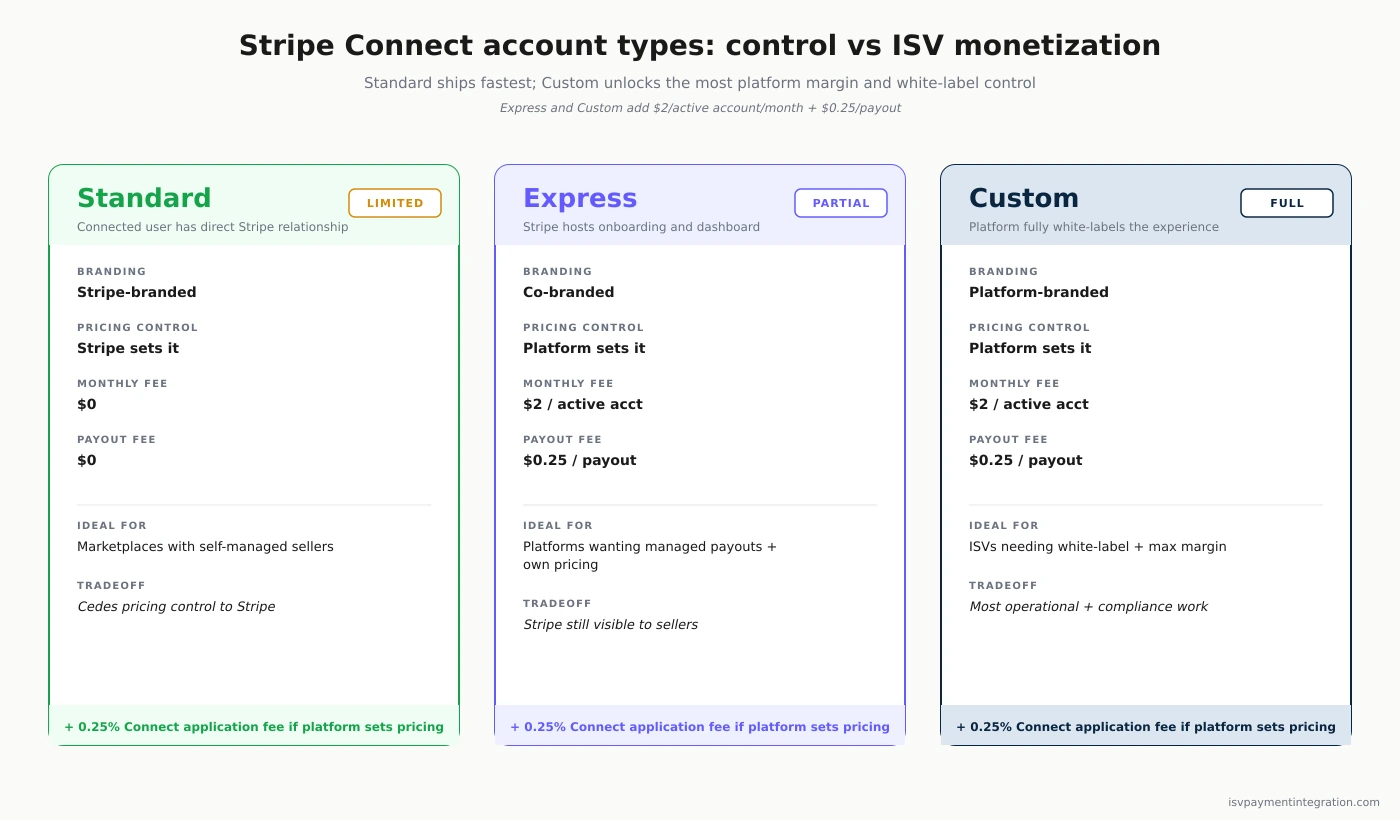

Stripe Connect Pricing for ISVs

Connect is Stripe’s platform product, and its pricing model is the most important Stripe pricing detail for ISVs embedding payments. The Connect fee schedule depends on who sets pricing for connected accounts and which account model the platform uses.

Three Connect account types

- Standard accounts — connected users have a direct Stripe relationship and bank account on file. Fastest to integrate, lightest platform overhead. Limited control over branding and pricing.

- Express accounts — Stripe hosts onboarding and most of the seller dashboard. The platform owns the integration. Lighter ops with managed payouts.

- Custom accounts — the platform controls almost everything, including a fully white-labeled experience. More flexibility, more operational work.

Connect fees and monthly fees

- If Stripe sets and collects payments pricing from connected accounts: $0 in additional Connect fees and no monthly fees. The platform pays nothing on top of standard processing fees.

- If the platform deploys its own payments pricing (marking up the rate sellers see and earning the spread): 0.25% application fee starting threshold charged to the platform on each transaction.

- Express and Custom accounts: $2 per monthly active account (one that processes at least one charge or payout) plus $0.25 per payout to a connected account’s bank account. These per-account monthly fees are the only flat-rate per-seat charge in Stripe pricing.

A worked example

A connected account sells a $100 service through your platform. Your platform takes a 10% application fee, keeping $10. Stripe credit card processing costs $3.20 (2.9% + $0.30). That leaves $86.80, and the $0.25 Express payout fee brings it to $86.55 in the connected account’s bank account. Your platform earns the $10 fee less any 0.25% Connect application fee that applies.

The “should have negotiated earlier” pattern

The most common Connect pricing regret: founders default to Standard accounts for integration speed, ship the platform, watch volume scale, then realize the platform has ceded the most monetizable surface — markup pricing — to Stripe. HN founder Ben (Show HN: Zoneless, item 47704260) reported burning $9,400 per month in opaque Connect fees before building an alternative platform. Design the pricing relationship up front, before volume gives Stripe leverage.

The Stack: How Global SaaS Hits 7.8% Effective

Here is the per transaction math behind the 7.8% blended rate cited at the top of this page, from the Freemius 2026 payment processing model:

| Layer | Rate added | Running blended rate |

|---|---|---|

| Stripe Payments (base, US card) | 2.9% + $0.30 | 2.9% |

| Stripe Billing (Starter) | +0.5% on recurring revenue | 3.4% |

| Stripe Tax | +0.5% per calculated transaction | 3.9% |

| International card surcharge | +1.5% (on foreign-issued share) | ~4.4% blended |

| Currency conversion | +1% (on FX share) | ~5.0% blended |

| Stripe Chargeback Protection (optional) | +0.4% on volume | 5.4% |

| Dispute and refund leakage (modeled) | ~+0.5–1% | 5.9–6.4% |

| Connect platform pricing fees (if applicable) | +0.25% application fee | 6.2–6.7% |

| Radar for Fraud Teams (custom pricing) | $0.07 per screen ≈ +0.5% at avg ticket | ~6.7–7.2% |

| Per-transaction fixed fee impact (variable AOV) | +0.5–1% effective | ~7.2–7.8% blended |

The Freemius reference scenario — a US-based SaaS selling globally in USD, issuing invoices, handling tax — lands at 7.8% effective on real workload mix. Independent calculators from Dodo Payments and Swipesum produce comparable blends in the 5–8% range.

The point isn’t that Stripe is overpriced. ISVs need to model the actual mix — international payments share, average ticket, recurring vs one-time, currency conversion exposure, Connect markup — to know the rate they’re really paying across all payment methods. Quoting 2.9% when your blended rate is 6.5% is a payment processing model that breaks the moment a merchant audits Stripe charges line by line.

What ISVs Should Watch For Before Committing

Beyond the fee schedule, four operational risks deserve scrutiny before integrating Stripe at the platform level.

Account stability. Stripe’s risk engine flags sudden volume spikes, elevated chargeback rates, and certain verticals (CBD, telemedicine, gaming, supplements) for automatic payout pauses. Holds can extend up to 180 days without human review unless escalated. Multiple Hacker News threads — including item 41861473 — document founders losing access to processed funds without a stated reason. For ISVs whose merchants accept card payments daily, hold risk needs to be in the contingency plan.

Token portability. Stripe stores tokenized credit card credentials and offers no self-service export. Migrating means either re-collecting card details (catastrophic for subscriptions) or running a token project with Stripe support. The single largest reason economics-driven decisions to leave get deferred.

Multi-year exclusivity. Custom pricing typically comes with 24–36 month commitments and exclusivity language preventing volume splits across processors. The headline rate cut is rarely free.

Refund non-return. For verticals running 5%+ refund rates — apparel, event tickets, generous-refund SaaS — the 2.9% + $0.30 retained on every refund is a margin leak invisible in any rate comparison. Model your real refund rate first.

How Stripe Pricing Compares to Alternatives for ISVs

The practical question isn’t whether Stripe is the cheapest payment processor — it’s which payment processing partner produces the right combination of economics, control, and operational fit for the platform’s specific shape.

- Adyen — Interchange-plus default, negotiated markups around 0.6% + €0.10 for enterprise. Better economics at >$10M annual processing for global businesses; weaker developer experience. See Stripe vs Adyen.

- Finix — Grew 4× in 2024 selling transparent IC+ pricing to platforms, positioning against Stripe’s blended fee structures. Strong fit for ISVs who want cost basis line by line. See Stripe vs Finix.

- Braintree — Published US rate 2.59% + $0.49. PayPal Complete Payments (PPCP) adds platform revenue share. Stronger when merchants want PayPal and Venmo. See Stripe vs Braintree.

- PayPal — Checkout 3.49% + $0.49 (branded button premium); Standard Card 2.99% + $0.49. PPCP gives ISVs negotiated platform pricing. Right when PayPal brand trust drives conversion. See Stripe vs PayPal.

Why most ISVs stay on Stripe anyway

Despite cleaner economics elsewhere, migration cost — token portability, integration rebuild, team retraining — defers the decision indefinitely for most platforms. Stripe’s developer experience, merchant-of-record optionality through Managed Payments, and the broader ecosystem (Atlas, Issuing, Treasury, Capital) create operational lock-in that pure rate math doesn’t capture. The right answer depends on the rate gap, the migration cost, and the option value of the Stripe stack you’d lose.