Stripe vs PayPal

A feature-by-feature comparison for ISVs integrating payments.

Stripe vs PayPal stops being a payment-processor question the moment your software embeds someone else's payments. The fork is between Stripe Connect's three account models and PayPal for Platforms' Build, White-Label, and Marketplaces tiers — and whether you run a hybrid stack that captures consumer-trust conversion alongside platform-grade margin. SERP articles aimed at single-merchant SMBs answer the wrong question for ISVs.

Feature Comparison

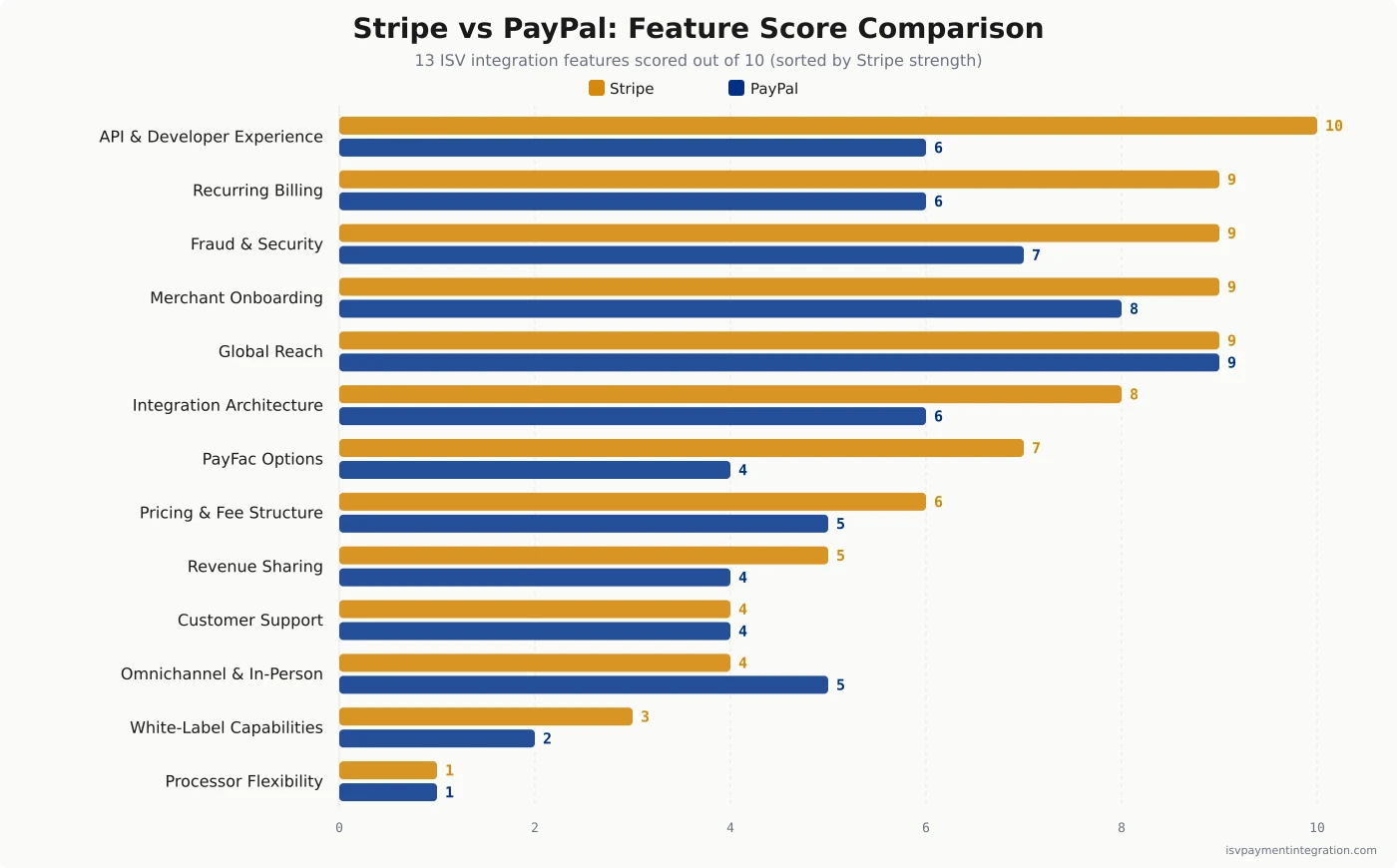

| Feature | Stripe | PayPal |

|---|---|---|

| Integration Architecture | 8 | 6 |

| API & Developer Experience | 10 | 6 |

| White-Label Capabilities | 3 | 2 |

| Processor Flexibility | 1 | 1 |

| Pricing & Fee Structure | 6 | 5 |

| Omnichannel & In-Person Payments | 4 | 5 |

| Fraud & Security | 9 | 7 |

| Revenue Sharing | 5 | 4 |

| Merchant Onboarding | 9 | 8 |

| Global Reach | 9 | 9 |

| Recurring Billing | 9 | 6 |

| Customer Support | 4 | 4 |

| PayFac Options | 7 | 4 |

Get this comparison as a shareable PDF

We'll send the Stripe vs PayPal breakdown to your inbox — ready to share with your team.

Best for

Stripe

ISVs at $1M-$50M annual processed volume building white-label SaaS, multi-tenant marketplaces, or subscription products that need Stripe Connect Express or Custom plus Stripe Billing in one stack — international merchant base, developer-led team, willingness to accept Stripe as merchant of record.

Best for

PayPal

ISVs whose merchants sell to checkout-trust-sensitive consumers (event ticketing, donation platforms, single-purchase B2C retail under $200 AOV) where PayPal's Nielsen-measured conversion lift on logged-in buyers materially changes merchant unit economics — typically deployed as a second button alongside Stripe rails, not standalone.

Every list-style comparison of these two payment processors aimed at small businesses asks the wrong question for software platforms. If you’re an ISV embedding payments — not a coffee shop choosing a card reader — the decision is which sub-merchant model carries your software’s brand, your revenue share, and your underwriting risk. This guide rewrites the comparison from that angle, with one concession most production ISVs end up making: you’re probably running both.

The short version. For ISV channel-product comparison: Stripe Connect (Standard, Express, Custom) vs PayPal for Platforms (Build, White-Label, Marketplaces) is the actual fork, not the headline rates. For platform economics: Stripe Connect’s 0.25% application fee captures platform margin on Stripe-routed transactions only — every PayPal-button-routed dollar bypasses your application fee entirely. For checkout reality: the US version of the hybrid stack runs as two parallel SDKs, because Stripe-orchestrated PayPal is restricted to European merchant locations and explicitly excluded for platforms onboarding sub-merchants. We’ll show the math, the operator patterns, and the decision tree.

For deeper coverage of each vendor in isolation, see our Stripe pricing analysis and PayPal pricing analysis.

The Quick Take: What Stripe and PayPal Actually Are in 2026

Stripe is a unified API platform. Connect is the ISV surface — 16,000+ platforms and marketplaces actively running it, 11M+ active onboarded accounts paid through it, and over $1B in payments processed across 104 different platforms in the last year alone. Named operators by Connect tier: Custom (full PayFac-on-Connect) — Shopify (1M+ merchants, ~10-year partnership), Lightspeed (~115,000 locations globally; migrated off legacy processor in 90 days), Mindbody (40 countries, 97.4% authorization rate, 0.04% fraud rate), Substack (5M+ paid subs, 50,000+ paid publications), Housecall Pro (20,000+ home-services pros, +40% LTV over two years, full Connect + Issuing + Capital + Data Pipeline). Express (instant-payout marketplaces) — Lyft (700K+ drivers, 40% of all payouts went through Express Pay within six months of launch), DoorDash (per its S-1 SEC filing, Stripe-built Dasher payouts), Instacart (Instant Cashout for shoppers). Standard — Twilio (+10% authorization rate vs prior provider). The thirteen-year lead on embedded-payments tooling shows in the documentation, the SDKs (seven-plus languages), the sandbox, and the breadth of adjacent products — Billing, Tax, Issuing, Capital, Treasury — that ISVs can layer on a single account.

PayPal is a 434M-active-account consumer wallet bolted onto a merchant-services business — those numbers are from PayPal’s 2024 10-K filing, where PayPal also reports $1.68 trillion total payment volume in 2024 (+10% YoY), 26.3 billion transactions (+5%), 200+ markets, 130+ currencies, and 25+ years of merchant-services operations. PayPal for Platforms (formerly PayPal Complete Payments / PPCP) is the genuine ISV surface: Build (developer-led integration), White-Label (PayPal-as-processor with platform branding), and PayPal for Marketplaces (split payments and marketplace flows). The named-platform roster is thinner than Stripe Connect’s: BigCommerce is the marquee partner (10+ year partnership; “BigCommerce Payments powered by PayPal” launching 2026), Wix expanded its partnership in July 2025 so PayPal becomes the PSP for Wix Payments card processing, Eventbrite uses PayPal alongside Stripe and Adyen, and Patreon offers PayPal as one of three creator payout rails. PayPal for Platforms also serves home and field services, fitness and wellness, food and beverage, professional services, and giving-and-faith verticals at scale.

Stripe sells you primitives. PayPal sells you a wallet network. The strategic-frame zinger: at this point in 2026, the ISVs winning at embedded payments are the ones who stop choosing.

Stripe and PayPal at a Glance: Payment Processor, Payment Gateway, or Both?

The vocabulary trips ISVs evaluating these vendors. Stripe is a payment processor and payment gateway combined — a unified payment processor handling card-network routing plus a payment gateway tokenizing credit card data on the merchant side, plus a developer ecosystem layered on top. PayPal is a payment processor with a consumer-wallet brand bolted on — its merchant services arm processes credit card data and supports the same payment methods other processors accept (credit and debit cards, ACH, digital wallets, pay later through PayPal Pay Later, and Venmo for US merchants), but the payment processor identity is fused with the consumer-facing PayPal account ecosystem in ways that affect the checkout experience.

Both vendors handle the full set of online payment methods small businesses and ISVs need: credit and debit cards, alternative payment methods (Apple Pay, Google Pay, Samsung Pay, Klarna, Afterpay), digital wallets, and pay-later instruments. The functional difference is brand recognition. PayPal’s checkout page brand recognition compounds with checkout experience optimization in ways the Stripe brand doesn’t — Stripe is invisible to most consumers, which is a feature for white-label ISVs and a constraint for ISVs serving merchants whose conversion depends on customer-side trust signals.

For ISVs, the operational shorthand: think of Stripe as a payment processor + payment gateway + developer toolkit (Stripe Elements, Stripe.js, the developer tools layer). Think of PayPal as a payment processor + consumer wallet + branded checkout experience. Each one solves different parts of the embedded payments problem, which is exactly why they end up running side by side. The key features ISVs evaluate — accept payments online, support multiple payment options, handle international transactions, integrate with bank account payouts, and provide developer tools for embedding the flow — are covered by both vendors at different depths and on different ease-of-use curves.

What Stripe and PayPal Actually Are (For an ISV)

The “Stripe vs PayPal” question collapses three distinct comparisons into one. Pulling them apart is the first step to making a defensible choice.

Stripe Connect for ISVs has three account types. Standard is the lightest integration — your sub-merchant signs up directly with Stripe, sees the Stripe brand, and you collect a referral relationship. Express is the embedded onboarding flow most platforms use; the merchant signs up through your software, sees your brand on the surface and Stripe inside the legal layer, and you handle the user experience while Stripe handles compliance. Custom is full white-label — your merchants never see the Stripe brand, you own the dashboard, and you take on more of the underwriting conversation. Across all three, Stripe is the merchant of record (or close to it) and your platform earns through the application-fee mechanism.

PayPal for Platforms has three corresponding tiers, though PayPal positions them differently. Build is the developer-first integration where your platform calls PayPal’s APIs and merchants log in with their existing PayPal accounts — fast for ISVs whose merchants are already on PayPal. White-Label is the embedded experience where your software handles the surface and PayPal handles the processing underneath. PayPal for Marketplaces adds split-payment, escrow, and seller-payout primitives for true marketplace use cases. There’s no published rate card for any of them — paypal.com is explicit: “Platform transaction rates and fees are negotiable across any of our integration models. Contact Sales to discuss the right pricing for your business.”

The legacy artifacts still in PayPal’s docs — Payments Standard, Payments Pro, Express Checkout — are direct-merchant products. Don’t confuse them with PPCP. Payments Pro at $30/month is rarely the right choice for ISVs in 2026.

The practical takeaway: when you read “Stripe vs PayPal,” translate it. For your software platform, the comparison is Stripe Connect Express vs PayPal for Platforms White-Label in most cases, or Stripe Connect Custom vs PayPal for Marketplaces if you’re running a true split-payment marketplace.

Fee Architecture: Where Each Pricing Model Breaks for ISVs

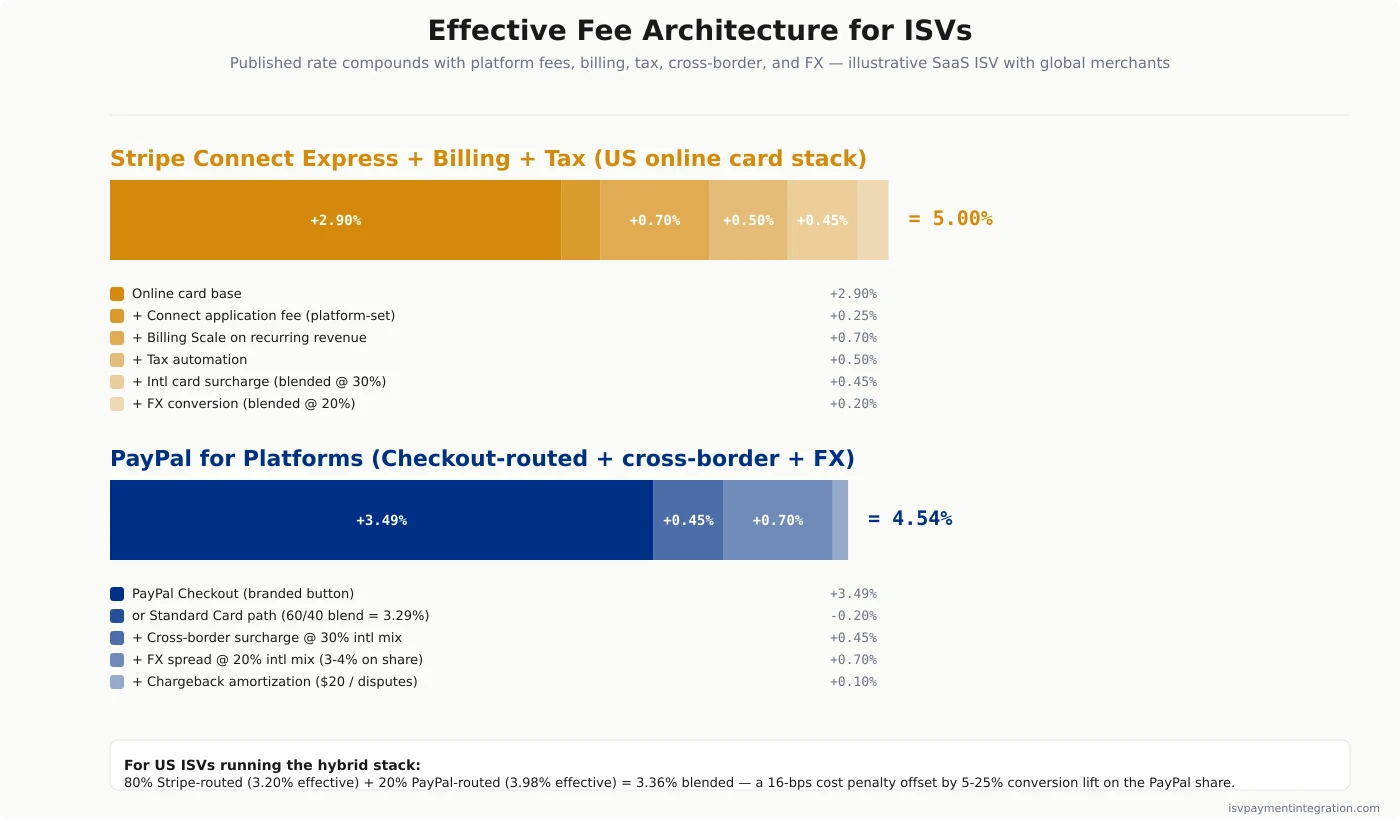

Headline rates first, then the real ISV economics. Both vendors run flat rate pricing on standard tiers, with no monthly fees on entry plans (Stripe Standard has no monthly fees; PayPal’s standard accounts also have no monthly fees, with PayPal Payments Pro at $30/month being the legacy exception). Stripe charges 2.9% + $0.30 as its base credit card transaction fees with a fixed fee per transaction; PayPal charges 3.49% + $0.49 on its branded Checkout, with PayPal charges varying by product line and Stripe charges following a more uniform flat rate model for transaction fees. Both publish online flat rate transaction fees with no additional fees for major credit card brands at the standard tier; both add additional fees for cross-border, currency conversion, and certain alternative payment methods. The right payment processor for accepting payments at scale depends on the payment options your merchants offer their customers — and whether the headline payment processing rate or the all-in payment processing economics matter more to your model. Both payment processors expose payment options that include credit and debit cards, ACH from a US bank account, digital wallets, and pay later instruments; the long-term cost difference is a function of mix.

Stripe US online cards: 2.9% + $0.30 per successful charge. Manually entered cards: 2.9% + 0.5% + $0.30. International cards: +1.5% on top of base. Currency conversion: +1% on top. Stripe Terminal in-person: 2.7% + $0.05. ACH Direct Debit: 0.8% capped at $5. Klarna BNPL: 5.99% + $0.30.

Stripe Connect layers on top. If Stripe sets the pricing for your connected accounts, you pay $0 in additional Connect fees. If your platform deploys its own pricing model — the standard ISV pattern — Stripe charges a 0.25% application fee on each transaction. Express and Custom accounts add $2 per monthly active account + $0.25 per payout to your platform’s bill. Stripe Billing is 0.5% on Starter / 0.7% on Scale of recurring revenue. Stripe Tax is 0.5% per calculated transaction. Stripe Radar is included on Standard pricing; Radar for Fraud Teams with custom rules is $0.02 per screen on Standard pricing or $0.07 on Custom.

The post-2020 Stripe refund policy: when you refund a customer, Stripe keeps the original 2.9% + $0.30. The dual-fee dispute model effective June 2025: $15 received fee per dispute regardless of outcome, plus $15 counter fee if you contest (refundable on win, forfeited on loss). Instant Payouts US: 1.5% min $0.50 — raised from 1% in June 2024.

PayPal US standard online: 3.49% + $0.49 for the branded PayPal Checkout button. Standard Credit/Debit Card: 2.99% + $0.49 when buyers type a card directly. Pay with Venmo: 3.49% + $0.49. PayPal Pay Later: 4.99% + $0.49. QR Code (Zettle in-person): 2.29% + $0.09. Cross-border: +1.50% on every international commercial transaction. Currency conversion: 3-4% spread above the mid-market rate. Chargeback fee: $20 per dispute regardless of outcome. Standard dispute fee: $15 (escalating to $30 for high dispute-rate accounts).

PayPal for Platforms revenue share isn’t published. Practitioner-reported rates: PPCP-negotiated rates typically run 30-80 basis points below list at $5M annual processing, with meaningful tier step-downs at $50M+. Every deal is custom, and the platform’s lever is aggregate volume across all sub-merchants.

The fee comparison ISVs miss most often. PayPal Checkout is 50 basis points more expensive than direct card processing through PayPal — the wallet experience commands a premium. ISVs whose merchants surface both options pay a blended rate that depends on the Checkout-vs-direct mix. A merchant running 60% Checkout / 40% direct cards bills at a blended 3.29% + $0.49, not the headline 2.99%.

Stripe Connect vs PayPal for Platforms: The Three-Tier Cross-Walk

This is the comparison the SERP doesn’t surface. The mapping isn’t perfectly clean, but it’s close enough to drive a decision.

| Stripe Connect tier | PayPal for Platforms tier | Who’s MoR | Onboarding owner | Dashboard owner |

|---|---|---|---|---|

| Standard | Build (with merchant’s existing PayPal) | Stripe (or merchant) | Sub-merchant directly | Stripe (visible to merchant) |

| Express | White-Label (limited) | Stripe-of-record + platform-of-record split | Platform via Stripe-hosted onboarding | Platform-branded surface, Stripe legal layer |

| Custom | White-Label (full) + PayPal for Marketplaces | Platform (or splits) | Platform | Platform fully |

Standard / Build — fastest to integrate, lightest platform involvement. Your platform refers; the processor onboards. Best when your merchants are already on the processor and recognize the brand.

Express / White-Label limited — the dominant ISV pattern in 2026. Your software handles the merchant experience; the processor handles the legal and compliance layer. Stripe’s Express onboarding gets merchants live in minutes; PayPal’s negotiated White-Label onboarding is comparable but typically measured in business days because PayPal’s underwriting tracks more risk data.

Custom / White-Label full + Marketplaces — full-control platform. Your brand is the only one merchants see. You take on more of the regulatory conversation, you negotiate the floor on rates, and your application-fee structure is bespoke. This is where SaaS-platform-as-merchant-of-record patterns live, and where the negotiation between platform-margin and merchant-conversion really happens.

There’s a structural exclusion ISVs need to know about. Stripe-orchestrated PayPal — where PayPal renders as a payment-method tile inside the Stripe Payment Element — is restricted to merchant locations in supported European countries (EUR, GBP, CHF, plus a few others) per Stripe’s docs. And explicitly: “PayPal isn’t available for platforms that onboard other businesses and enable them to accept payments directly, such as Shopify or Squarespace.” Translated: the canonical SaaS-platform-with-sub-merchants pattern — the exact ISV use case — is excluded from Stripe-orchestrated PayPal even when the business location qualifies. Marketplaces where the platform itself is the merchant of record can request manual approval; software platforms onboarding sub-merchants cannot.

For US ISVs running Stripe Connect, this means PayPal can’t ride inside Stripe’s Payment Element. The hybrid stack runs as two parallel SDKs. Which is the next section.

The Hybrid-Stack Pattern: Why Most Production ISVs Run Both

The pattern the SERP doesn’t frame. Three regional realities, in operator-preference order.

Pattern A — Stripe Payment Element with PayPal as a Stripe-orchestrated payment method. Available natively only when the merchant’s business location is in a supported European country. Stripe’s PayPal-via-Stripe path includes Direct, Destination, and Separate-charges-and-transfers under Connect — but excludes platforms onboarding sub-merchants. So for a UK/EU/CH-based platform serving its own marketplaces, this is the cleanest integration. For most US ISVs, it’s not on the menu.

Pattern B — Stripe Custom Payment Method (CPM) adapter for PayPal. Released as a private-preview adapter on API version 2025-03-31.basil and later. The merchant hosts the adapter, which orchestrates PayPal’s own merchant account inside the Stripe Checkout / Element UI. This is the path for US merchants who want PayPal to render as a tile inside Stripe’s UI without using Stripe-orchestrated PayPal directly.

Pattern C — Two parallel SDKs. The dominant US pattern in 2024-2026. Stripe Elements / Checkout for cards plus the PayPal JavaScript SDK rendering a separate <paypal-buttons> block. Two merchant accounts. Two webhooks. Two dashboards. Two reconciliation pipelines. Hyperswitch’s engineering writeup on integrating both: “Since PayPal is not available as a payment method within Stripe, you would have to render the PayPal checkout button separately… simple functionality like being able to reorder payment methods is simply not possible because Stripe’s Payment Element methods do not apply to PayPal.” This is the engineering reality most US ISVs sit with.

The conversion-lift evidence for running both. PayPal’s commissioned Nielsen study (behavioral panel of 408,000 large-enterprise desktop transactions across 25,000 consumers Jan-Dec 2022, plus a February 2023 attitudinal survey of n=3,999 recent purchasers) found that “within the software and electronics industries, PayPal customers are 54% more likely to buy when they pay online with PayPal.” That 54% is a vertical-specific lift in a PayPal-commissioned study — software and electronics, US, desktop only — not a sitewide checkout uplift. The all-vertical average from the same Nielsen work is 33%. Independent measurements come in lower than 54%: Baymard Institute’s checkout research puts PayPal-routed checkout completion at 88.7% vs an industry average around 76% — a real lift that confirms the directional claim without reaching PayPal’s headline number. Operator-side numbers are smaller still: Paddle’s data puts adding one extra payment method at ~5.5% conversion lift, full localized stack ~8%. Real-world bootstrap data from indie SaaS: Shuffle’s published stats at $30K MRR show 41.59% of payments routing through PayPal, with country-specific shares of 75% Netherlands, 67% Italy, 62% Germany, 52% France, 40% Canada — strong evidence that PayPal is meaningfully more than a vestigial alt-payment-method outside the US.

The math for the hybrid stack. Take a typical US ISV running 80% Stripe / 20% PayPal-button uptake at $100 average order value:

- Stripe-routed: 80 transactions × ($2.90 + $0.30) = $256 in fees on $8,000 volume, effective 3.20%

- PayPal-routed: 20 transactions × ($3.49 + $0.49) = $79.60 in fees on $2,000 volume, effective 3.98%

- Blended effective rate: 3.36% versus 3.20% Stripe-only — a 16-basis-point cost penalty in exchange for 5-25% conversion lift on the PayPal-routed share.

The math only fails if PayPal uptake is small AND the lift is at the low end. At 20% uptake plus 10% lift, blended cost rises 16 bps but revenue rises 200 bps. Net positive across most consumer verticals.

Here’s the load-bearing fact for ISVs. Stripe Connect’s application fee fires only on Stripe-routed transactions. Every PayPal-button-routed dollar bypasses your platform’s application_fee_amount mechanism entirely. For a platform on a 0.5% application fee at $100M annual GMV with 20% PayPal-button uptake, that’s $100,000/year in foregone platform revenue — dollars routing through the PayPal SDK never touch the Stripe Connect ledger. To monetize PayPal-routed volume, you have to negotiate revenue share separately through the PayPal Partner Program. That’s the actual ISV decision lever the SERP misses.

Developer Experience and Integration Surface

For most engineering teams, this is decided in the first afternoon of evaluation.

Stripe’s developer experience is the industry benchmark. The API docs are the example everyone else copies. SDKs in seven-plus languages, copy-paste sample code, a sandbox that mirrors production, and the most active developer community in fintech. Most engineers process a test transaction in under an hour. Stripe.js and Elements handle client-side tokenization with minimal PCI scope; the same primitives extend to mobile via iOS and Android SDKs. Stripe CLI gives you fixtures and webhook forwarding from day one. For developer-led ISV teams especially, Stripe is the better choice on time-to-first-transaction.

PayPal’s developer experience is functional but layered. PPCP’s JavaScript SDK is solid, the REST APIs work, and the sandbox is comprehensive. The friction comes from surface area: PayPal’s docs cover modern PPCP plus legacy NVP/SOAP plus Braintree (PayPal-owned, separate SDK) plus Express Checkout plus Payments Standard, and figuring out which surface to build against takes longer than anything else. The Braintree-PayPal overlap is a separate decision in itself — many ISVs evaluating “Stripe vs PayPal” should actually be evaluating Stripe vs Braintree if they want PayPal’s processing without the consumer-wallet UX.

A B2B note: neither vendor is best-in-class for Level II/III interchange data. ISVs serving B2B merchants who want to pass purchase-order numbers and line-item data to qualify for lower interchange rates should look at gateway-first stacks. Our NMI vs Stripe comparison covers that pattern.

Recurring Billing, Recurring Payments, and Subscription ISVs

This is where the architectural gap is largest.

Stripe Billing is a dedicated platform for recurring payments — usage-based metering, hybrid pricing models, dunning with machine learning payment recovery, an embeddable customer portal, proration, trials, coupons, and an invoicing surface for subscription invoicing on top of recurring payments. Pricing: 0.5% Starter / 0.7% Scale on recurring revenue. For SaaS ISVs, Stripe Billing is system-of-record for recurring payments and subscription state. The fee compounds on top of base processing, which is a real consideration at scale, but the alternative is building recurring payments infrastructure yourself.

PayPal’s recurring payments tooling exists but isn’t a billing platform. PayPal Subscriptions handles fixed or variable pricing per billing cycle for recurring payments; there’s no metered billing, no usage-based pricing, no first-class proration, and no embeddable customer portal at the depth Stripe Billing provides for recurring payments. ISVs serving SaaS merchants almost universally pair PayPal-button-on-PPCP with Stripe Billing as the system of record for recurring payments — and that’s a structural reason hybrid stacks emerge in subscription verticals specifically.

For ISVs whose merchants run heavy on subscriptions (B2B SaaS, professional services, recurring fitness or wellness), the answer is Stripe primary with PayPal as an alternate payment method, full stop. For ISVs whose merchants are predominantly one-time-purchase B2C retail, the calculation changes.

Fraud Protection, Fraud Detection, and PCI Posture

Both vendors are PCI DSS Level 1 compliant — the highest level for handling credit card data. Both run fraud protection and fraud detection layers that screen credit card data before authorization, and both expose their fraud protection rules to ISVs at higher pricing tiers. The differences are upstream of fraud detection itself.

Stripe Radar is a competitive advantage. Standard machine learning fraud detection is included with Standard pricing at no per-screen cost. Radar for Fraud Teams adds customizable fraud protection rules, a centralized review queue, and chargeback management — $0.02 per screen on Standard pricing or $0.07 on Custom pricing. Smart Disputes adds 30% of disputed amount on win, free on loss. The baseline machine learning fraud protection — trained on billions of transactions across Stripe’s network — is meaningful out-of-the-box defense for ISVs that don’t want to build or tune fraud detection rules themselves.

PayPal’s risk infrastructure runs on the network signal of 434 million wallet relationships and 26 billion 2024 transactions. Buyer protection is a business advantage your merchants benefit from at checkout; reserve and hold patterns are a business risk your merchants bear after the sale. Sub-merchants in higher-risk verticals routinely see rolling reserves of 5-15% held for 60-180 days. PayPal’s chargeback fee is $20 per dispute, regardless of outcome. The Fraud Protection Advanced product layers AI fraud prevention on top of network-level signal; Chargeback Protection covers eligible transactions; automatic retries improve authorization rates; least-cost routing is offered for platforms at higher tiers.

For ISV operations, the difference shows up in how each vendor handles risk events. Stripe Radar can quietly account-hold merchants on risk signals — your platform inherits the cash-flow gap until the merchant clears review. PayPal’s reserves are scoped per-merchant and explicit — the merchant sees the reserve and the timeline upfront. Stripe is faster to onboard, slower to communicate when things go sideways. PayPal is slower to onboard, more conservative once underwritten.

In-Person and Omnichannel for ISV Verticals

The reframe section. Single-merchant comparisons land here on “$29 PayPal Zettle card reader vs Stripe Terminal hardware ecosystem.” For ISVs, the question is different — your platform is bundling hardware programs into starter merchant tiers and routing high-volume merchants to the deeper integration.

Stripe Terminal is the embedded in-person stack: BBPOS WisePOS readers, Stripe Reader M2 ($59), S700 / S710 ($299), Tap-to-Pay-in-app for iOS and Android, and partnerships with vertical-specific hardware manufacturers. Stripe Terminal pricing is 2.7% + $0.05 per in-person card transaction. For ISVs running multi-location restaurant SaaS, salon SaaS, or multi-location retail, Stripe Terminal partnerships and Tap-to-Pay-in-app are the architectural lever.

PayPal Zettle is the packaged in-person product, with the card reader at the well-known $29 entry price plus terminal options for higher-volume merchants. ISV deployment is typically a wrap — your platform bundles Zettle’s $29 card reader into starter tiers for solo-merchant or low-volume merchant accounts and routes higher-volume merchants to Stripe Terminal or to a direct merchant-services hardware program. Tap to Pay using the merchant’s phone is supported via the PayPal app and accepts contactless card payments, Apple Pay, Google Pay, and Samsung Pay. POS systems and POS software for ISV-distributed point-of-sale stacks integrate with both vendors via SDK; PayPal’s POS systems support is broader for low-volume merchants while Stripe’s POS software ecosystem skews toward higher-volume verticals.

The point-of-sale software layer matters more than the hardware bundle for most ISV verticals. PayPal’s Open Platform supports POS systems for industries spanning home and field services, fitness and wellness, food and beverage, professional services, and giving and faith — published vertical examples on paypal.com. Stripe’s POS partnerships skew toward marketplace and platform-led merchants where the in-person experience is one channel among many. The card reader is rarely the architectural decision — it’s a tactical entry point ISVs offer multi-segment merchant bases.

International, Currencies, and Cross-Border Economics

The cleanest comparison on the scorecard.

Stripe operates in 47+ countries with 135+ currencies, automatic local payment-method routing (SEPA, iDEAL, Klarna, Afterpay, Alipay, WeChat Pay, and more), and multi-currency settlement. International cards add +1.5%; currency conversion adds +1%. For a US-based SaaS selling globally in USD, the international layer stacks with base processing toward a 5.4% effective rate on FX-converted intl card transactions before any other fee adds.

PayPal operates in 200+ markets with 130+ currencies, deep consumer wallet penetration worldwide, and a mature cross-border payments operation. Cross-border surcharge: +1.50% on every international commercial transaction. Currency conversion: 3-4% spread above the mid-market exchange rate. The conversion spread is the line ISVs miss most often — that’s not a transparent fee, it’s a margin layer in PayPal’s FX path.

For ISVs with international merchant bases, Stripe’s currency conversion at +1% is meaningfully cheaper than PayPal’s 3-4% spread. For ISVs with a US merchant base selling to international consumers, both vendors handle cross-border but the math diverges by transaction mix.

Onboarding, KYC, and Sub-Merchant Activation

Stripe Express onboarding gets merchants accepting payments in minutes through a hosted flow that handles KYC verification, compliance checks, and account provisioning automatically. For platforms where activation speed correlates directly with revenue, this is one of Stripe’s strongest operational advantages — ISVs running freemium-to-paid funnels or service-marketplace flows can move a sub-merchant from signup to first payment in the same session.

PayPal’s onboarding leverage comes from existing accounts. With 36 million merchants already activated on PayPal, ISVs whose merchants overlap with PayPal’s existing base see fast onboarding by association — the merchant logs in with their existing PayPal account rather than going through full KYC again. New PayPal merchant onboarding is measured in business days because PayPal’s underwriting tracks more risk data; PPCP onboarding for sub-merchants under your platform’s umbrella is comparable in duration but typically faster than direct PayPal onboarding because the platform underwrites the merchant relationship.

The risk-model difference matters for ISV revenue forecasting. Stripe is fast to onboard and quiet on risk decisions — Stripe Radar’s account holds surface as cash-flow gaps after the fact. PayPal is slower to onboard and explicit on risk — reserves and hold timelines are negotiated upfront, scoped per-merchant. Both vendors freeze accounts; only one tells you in advance.

Customer Support and Customer Service Reality for ISV Tiers

Neither vendor is celebrated for customer service, and both score equally on the comparison matrix (4/10 each). The operational character is different.

Stripe runs a self-service-first customer support model. The help center documentation is deep enough that most issues resolve without contacting anyone. Live chat and email support exist; live chat is widely available for routine integration and billing questions, and the help center is the canonical first stop. Priority phone support requires Enterprise pricing that adds significant monthly cost. For platforms with senior engineering teams, this is fine — you build runbooks and self-serve. For early-stage ISVs, it’s a real customer support gap.

PayPal runs a relationship-management model at higher tiers. Dedicated partner managers sit at the top of the support tree for PPCP Enterprise tier, plus onboarding and integration specialists, technical training sessions, co-marketing programs, and access to a marketing toolkit library. PayPal’s help center, live chat, and phone support coverage is comparable to Stripe’s at the standard tier, with phone support more readily available for direct merchants but uneven for ISV partners. Customer service reputation is uneven on the consumer-facing side — widely criticized in Trustpilot reviews — but the partner-program experience for ISVs is meaningfully better than direct-merchant support.

Practical takeaway: budget for support gaps either way. Stripe rewards self-service-capable platforms; PayPal rewards platforms that can land a partner-manager relationship. Neither vendor is going to be the reason you pick them, but both can be the reason you regret the choice.

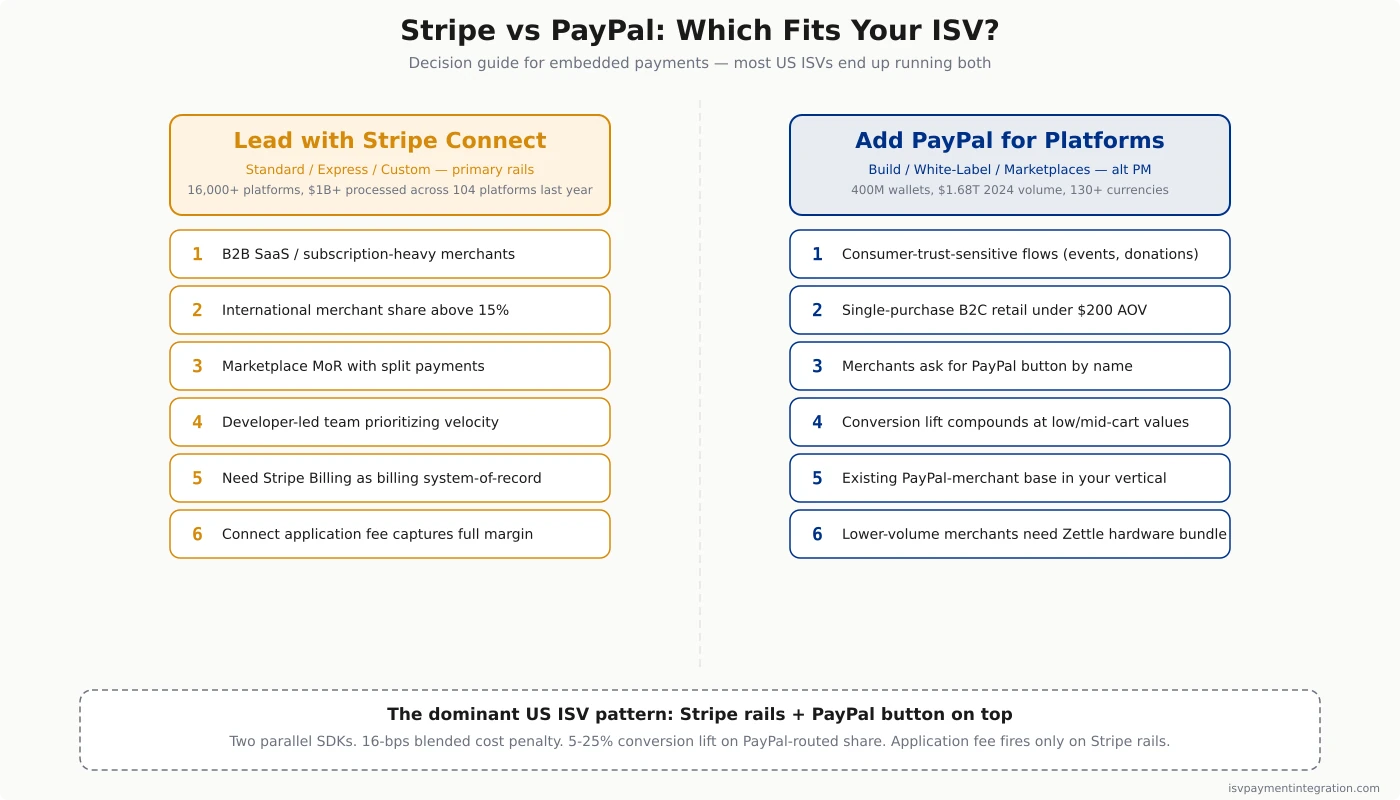

Decision Framework: Pick Stripe, Pick PayPal, or Run Both

Decision tree, not a feature recap. Walk it from the top.

- Are you primarily B2B SaaS / subscription / marketplace? → Stripe Connect Express + Stripe Billing as primary. PayPal button optional and rarely material.

- Is your international merchant share above 15%? → Stripe primary. PayPal’s FX spread eats more than your application fee at the international layer.

- Are your merchants selling consumer-trust-sensitive products under $200 AOV (event tickets, donations, single-purchase B2C retail)? → Both. Run Stripe rails plus the PayPal button on top to capture the Nielsen-measured lift on the PayPal-routed share.

- Are you a marketplace where the platform itself is the merchant of record? → Stripe Connect Custom or PayPal for Marketplaces. The decision is your developer ecosystem fit and how you negotiate the revenue share.

- Is your platform European-based with sub-merchants in supported markets? → Stripe-orchestrated PayPal becomes available — single Payment Element with PayPal as a payment method. This is the cleanest integration available, but only in EU/UK/CH locations.

- Are you US-based with sub-merchants on Stripe Connect? → Hybrid stack runs as two parallel SDKs. Accept the dual-dashboard reality and budget engineering time for separate reconciliation.

- Do your merchants ask for the PayPal button by name? → Run both. Consumer recognition compounds on conversion in ways the rate comparison can’t capture.

In the long term, the better choice for an ISV’s business needs is rarely one payment gateway in isolation — it’s the integration pattern that maps to your merchant base. Online businesses serving consumer-facing verticals see the strongest case for adding the PayPal button on top of a Stripe payment gateway primary, because online payment conversion rates respond to brand-recognition signals at the checkout page in ways the headline transaction fees comparison can’t capture. PayPal fees on the branded checkout page run higher than Stripe’s standard processing fees, with PayPal charges layered across both online and point-of-sale flows; long-term modeling of PayPal fees against blended business needs typically nets out around 16 basis points above Stripe-only when PayPal-button uptake stays below 20%, but the conversion lift on a properly instrumented checkout page typically offsets the rate gap for online payment volumes under $200 average order value. Online businesses with international transactions skewed above 15% see the opposite — Stripe’s payment methods coverage and payment processing economics on international payments win, because PayPal charges add 1.50% on top of the headline rate plus a 3-4% currency conversion spread, which compounds when major credit card transactions cross borders. Major credit card networks (Visa, Mastercard, Amex, Discover) carry the same per-transaction ease of use through both vendors at the standard tier — the major credit card brand recognition isn’t where the differentiation sits. PayPal Zettle’s hardware footprint is the point-of-sale anchor for in-person and online payment hybrid stacks bundled into ISV starter tiers, while Stripe Terminal owns the higher-volume payment gateway and POS software path. Whichever payment gateway you primary, model the ease of use of integrating both payment methods so the dual-rail option stays open as merchant conversion data accumulates.

The platform-margin question is the load-bearing one. Every PayPal-button-routed dollar bypasses Stripe Connect’s 0.25% application fee. At low PayPal uptake and high platform fee, the leakage is meaningful. The three operator strategies for handling this — let it leak (Shopify model, optimize for merchant conversion), gate PayPal behind a higher tier (Finix / PayFac-as-a-Service model, optimize for platform take rate), or charge a per-PayPal-transaction surcharge to recover platform margin without blocking merchants (the Memberful / Outseta hybrid model) — each fit different ISV verticals.

For deeper provider context, see our Stripe review and PayPal pricing analysis. For PayPal-owned alternatives without the consumer-wallet UX, Stripe vs Braintree is the comparison most ISVs should run alongside this one. ISVs that want true white-label control over the gateway often look at NMI vs Stripe; for global acquiring at enterprise scale, Stripe vs Adyen and Stripe vs Worldpay are the natural next reads. For the broader economics of where ISV payment revenue actually comes from, our guide on white-label payment processing for ISVs walks through the referral, revenue-share, and full payment facilitator models.

Get a free integration assessment for your ISV →

Frequently Asked Questions

The five questions ISVs ask most often. Inline answers; structured-data versions are in the page schema.

How much is the Stripe fee for $100?

On a $100 US online card transaction, Stripe charges 2.9% + $0.30 = $3.20. For an ISV running Stripe Connect on platform-set pricing, the platform also earns a 0.25% application fee on top — so the merchant pays $3.20 and the ISV captures $0.25 of that as platform revenue. Stripe Express and Custom Connect accounts add $2 per monthly active account plus $0.25 per payout. International cards add +1.5%, currency conversion adds +1%, and refunds keep the original 2.9% + $0.30 (post-2020 policy).

What are the disadvantages of Stripe for ISVs?

Five real ones. Flat-rate pricing barely flexes below $1M annual processing — meaningful concessions only start above $5-10M, and Stripe’s revenue share is reportedly capped for many platforms around $50M annual volume. The Connect fee stack is loud at scale: PromptBase’s founder posted on Hacker News that at peak the marketplace was “burning $9,400/month in opaque Stripe Connect fees” — the $2-per-monthly-active-account plus 0.25% + $0.25 domestic payout fee plus 0.25-1.25% cross-border fee plus 0.50-1% FX fee combination, in his words, “costs more than $2 to move $1.” Refunds keep the original processing fee — a permanent margin leak invisible in any rate comparison. The dual-fee dispute model (effective June 2025) charges $15 to receive any dispute and another $15 if you contest. Stripe Radar can quietly account-hold merchants on risk signals, surfacing later as cash-flow gaps the platform inherits. Stripe is closed ecosystem — no external acquirer routing — so platforms whose merchants want interchange-plus eventually graduate to a direct deal with Adyen, Worldpay-for-Platforms, or a custom acquirer. The gold-standard graduation example is eBay’s 2018 announcement of intermediating payments on its marketplace via Adyen — PayPal lost its anchor marketplace, and the migration completed with full PayPal sunset in July 2023.

Is Stripe or PayPal safer?

Both are PCI DSS Level 1 compliant — the highest tier. Stripe Radar is ML-driven with customizable rules; included tier is meaningful out-of-the-box protection. PayPal’s fraud network is informed by 434 million wallet relationships and tends toward more conservative reserve-and-hold patterns — sub-merchants in higher-risk verticals routinely see rolling reserves of 5-15% held for 60-180 days. Both are safe. Their reserve and hold patterns are not interchangeable.

Why is Stripe valued more than PayPal?

Different businesses, different valuation drivers. Stripe is privately valued around $70B (2024 tender) on platform optionality — Connect’s 16,000+ platforms, Stripe Billing as a system of record, plus Issuing, Capital, Tax, Identity, and the embedded-finance build-out. PayPal is publicly traded with a market cap reflecting its consumer-wallet network: 434M active accounts, $1.68T 2024 payment volume, 26B 2024 transactions. PayPal generates more revenue today; Stripe is priced on what its platform stack could earn.

Should ISVs use Stripe Connect or PayPal for Platforms for marketplaces?

For most US-based ISVs, the answer is Stripe Connect as primary with the PayPal button as an alternate payment method on top. Stripe Connect’s three account types (Standard, Express, Custom) cover the full spectrum of platform-merchant ownership, and the application-fee mechanism is the cleanest path for capturing platform revenue. PayPal for Platforms is competitive for ISVs serving consumer-facing merchants — BigCommerce is PayPal’s marquee partner — but native Stripe-orchestrated PayPal is restricted to European merchant locations and explicitly excludes platforms onboarding other businesses. In the US, the hybrid stack runs as two parallel SDKs: Stripe for cards, PayPal for the wallet button.