NMI vs Stripe

A feature-by-feature comparison for ISVs integrating payments.

NMI is a processor-agnostic white-label gateway that connects ISVs to 200+ processors through a single API, with interchange-plus pricing and full branding control. Stripe is a developer-first all-in-one platform with the industry's best API documentation, global coverage across 46+ countries, and an integrated ecosystem spanning billing, fraud detection, and identity. Choose NMI if your ISV needs white-label control, processor flexibility, and better economics at scale. Choose Stripe if speed to market, developer experience, and a single-vendor ecosystem matter most.

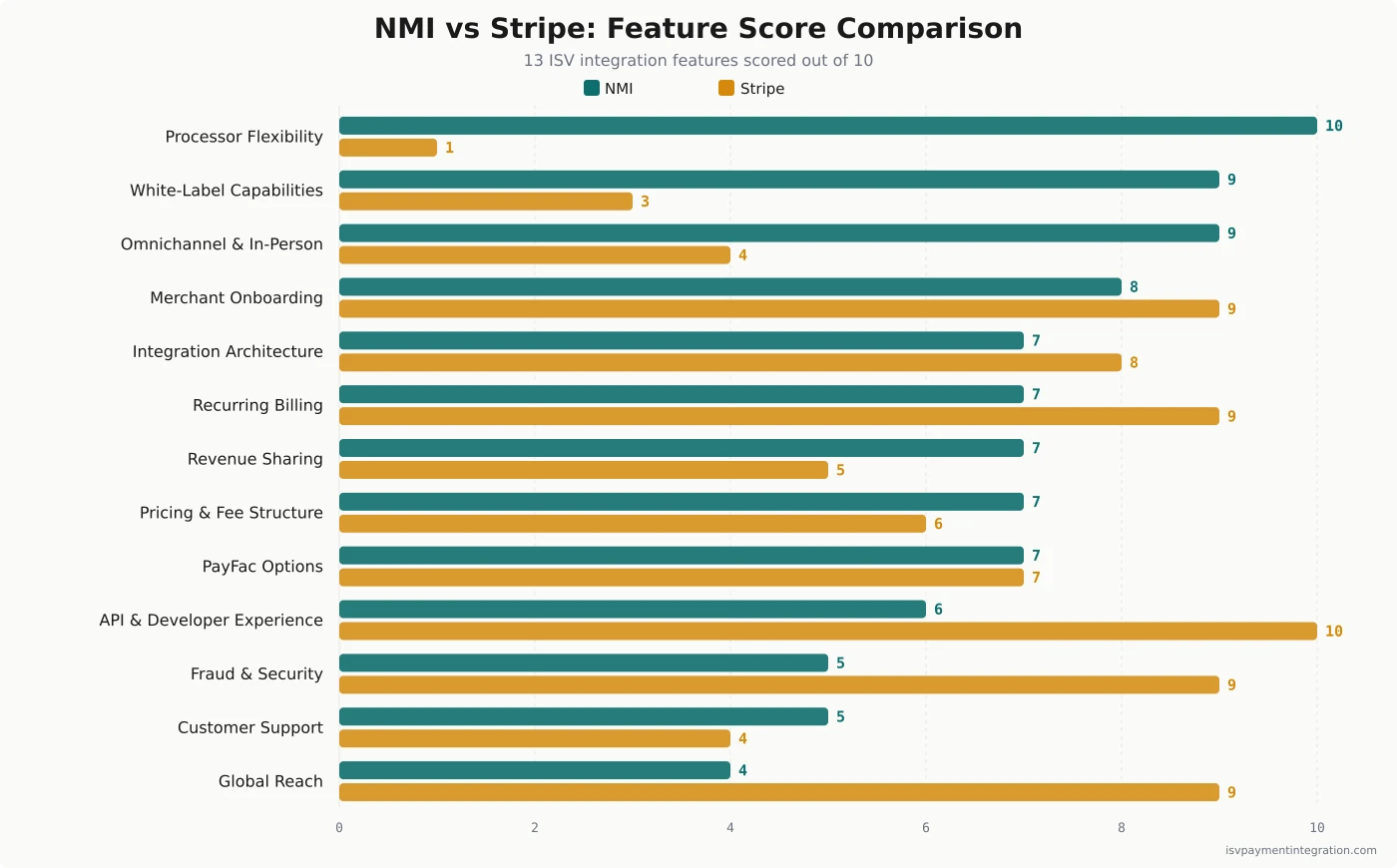

Feature Comparison

| Feature | NMI | Stripe |

|---|---|---|

| Integration Architecture | 7 | 8 |

| API & Developer Experience | 6 | 10 |

| White-Label Capabilities | 9 | 3 |

| Processor Flexibility | 10 | 1 |

| Pricing & Fee Structure | 7 | 6 |

| Omnichannel & In-Person Payments | 9 | 4 |

| Fraud & Security | 5 | 9 |

| Revenue Sharing | 7 | 5 |

| Merchant Onboarding | 8 | 9 |

| Global Reach | 4 | 9 |

| Recurring Billing | 7 | 9 |

| Customer Support | 5 | 4 |

| PayFac Options | 7 | 7 |

Get this comparison as a shareable PDF

We'll send the NMI vs Stripe breakdown to your inbox — ready to share with your team.

Best for

NMI

ISVs wanting white-label gateway capabilities with multi-processor flexibility, omnichannel payments, and interchange-plus pricing at scale. Ideal when the ISV needs to own the merchant relationship, control pricing to merchants, and serve diverse verticals including those Stripe won't onboard.

Best for

Stripe

ISVs at any stage wanting the fastest path to embedded payments with the broadest feature set, developer ecosystem, and global coverage across 46+ countries. Ideal for developer-led teams, marketplace platforms using Connect, and ISVs prioritizing speed over payment margin optimization.

NMI and Stripe take fundamentally different approaches to ISV payment integration. NMI is a processor-agnostic gateway that connects to 200+ processors through a single API — your ISV picks the processor(s) that fit each merchant segment. Stripe is a full-stack platform where gateway, processing, and acquiring are one integrated service — fastest path from code to production. For deeper dives on each platform individually, see our NMI review and Stripe review.

The right choice depends on how much control your ISV needs over the payment stack, how fast you need to launch, and whether payment margin optimization or speed to market matters more.

The short version: Choose NMI if your ISV needs white-label control and processor flexibility. Choose Stripe if developer experience and a single-vendor ecosystem are the priority.

Integration Architecture: Gateway Layer vs Full Stack

This is the most important distinction for ISVs, and it shapes every downstream decision.

NMI operates as a gateway layer. It sits between your software and the processor, giving your ISV a single integration point that connects to 200+ payment processors. If a processor raises rates or underperforms on approvals for a merchant segment, you can switch without rebuilding your integration. NMI supports 125+ shopping cart integrations and 235,000+ payment devices through this single gateway. The trade-off: NMI is not a processor itself, so your ISV needs a separate acquiring relationship.

Stripe is a full-stack platform. When you integrate with Stripe Connect, you get gateway, processing, acquiring, and a growing ecosystem of products (Billing, Radar, Terminal, Identity) in one service. One contract, one API, one dashboard. The trade-off: you and all your merchants are on Stripe’s processing network with no option to route transactions elsewhere.

What this means for ISV decision-makers: If your software serves merchants across different industries or regions with varying processing needs, NMI’s multi-processor flexibility is a structural advantage. If your team wants the fastest possible path to accepting payments with minimal infrastructure decisions, Stripe’s integrated stack removes complexity.

API and Developer Experience

ISV engineering teams will spend weeks or months on payment integration. The quality of documentation, SDKs, and sandbox environments directly impacts your integration timeline.

Stripe’s developer experience is the industry benchmark. The API documentation covers every major language with copy-paste examples, the sandbox mirrors production behavior, and most developers can process their first test transaction in under an hour. Stripe.js and Elements handle client-side tokenization with minimal PCI scope. G2 reviewers consistently rate Stripe highest for developer experience among payment platforms.

NMI’s developer tools are closer to Stripe’s than most ISVs realize. Collect.js, NMI’s client-side library, follows the same patterns as Stripe Elements: hosted payment fields, client-side tokenization, Apple Pay, Google Pay, and 3D Secure support. Developers who have built with Stripe.js can pick up Collect.js quickly because the integration architecture is nearly identical. NMI provides SDKs in PHP, Python, Ruby, Java, Node.js, C#, ColdFusion, and ASP.

Where NMI pulls ahead for B2B ISVs: full API control over Level II and Level III data processing. Passing enhanced transaction data (tax amounts, line items, customer codes) qualifies B2B transactions for lower interchange rates. Stripe does not support Level II/III processing, which means B2B-focused ISVs leave money on the table with every transaction.

NMI’s documentation draws mixed reviews. G2 reviewers rated NMI easier to use and set up than Global Payments and Square. But some ISVs describe integration as difficult, with onboarding support quality varying by partner channel.

Bottom line: Stripe is the faster, smoother integration. NMI offers more control once integrated, especially for B2B ISVs needing Level II/III processing.

Revenue Economics for ISVs

This is where the comparison matters most for ISV business models. For a deeper breakdown of fee structures, see our NMI pricing analysis and Stripe pricing analysis.

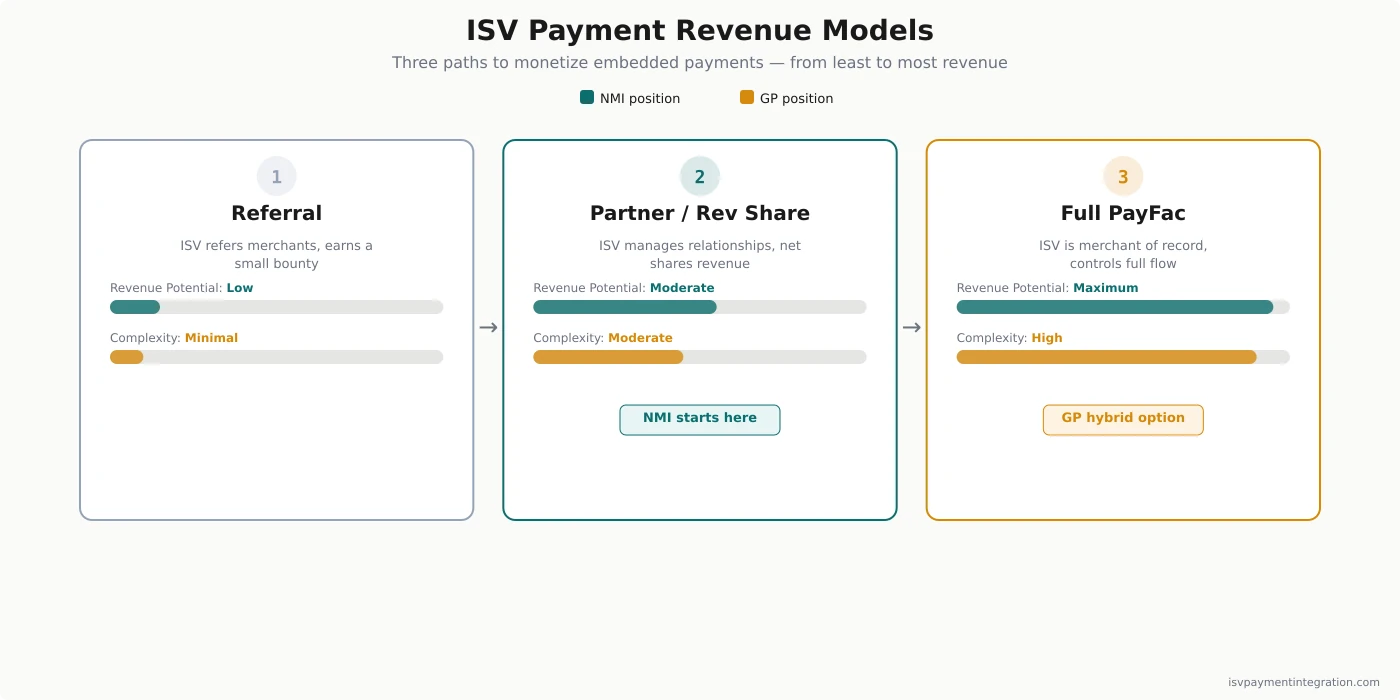

How ISVs Make Money from Embedded Payments

ISVs earn payment revenue through the spread between what merchants pay and what the processor charges. The embedded payments market is growing fast — McKinsey data shows US payment-processing revenue through ISVs grew 20% annually for five years, projected to hit $16 billion in 2025. The three models, from least to most revenue:

- Referral — ISV refers merchants, earns a small bounty. Minimal revenue.

- Partner-enabled / Revenue share — ISV manages merchant relationships, shares net payment revenue. Moderate revenue.

- Payment Facilitator (PayFac) — ISV becomes the merchant of record, controls the full payment flow. Maximum revenue, maximum complexity. See our guide on PayFac-as-a-Service for a middle path.

NMI Pricing and Revenue Sharing

NMI uses interchange-plus pricing through its partner network. Effective rates typically run 1.5% to 2.2%, which is 30% to 40% lower than Stripe’s flat rate according to AGMS pricing data. On $20,000 in monthly online sales, the difference works out to roughly $210 per month, or about $2,500 per year.

NMI’s partner-enabled model starts revenue sharing from the first transaction. ISVs can earn additional revenue through value-added extensions: fraud protection, secure card storage, Level III processing, and automatic card updating.

Important caveat: NMI’s pricing comes through resellers and ISOs, and transparency varies. Trustpilot reviewers report cases of hidden fees, surprise rate increases, and inactivity charges. Get your pricing agreement in writing and ask specifically about monthly minimums, PCI compliance fees, and early termination terms.

Stripe Pricing and Revenue Sharing

Stripe charges 2.9% + 30c per online transaction, 2.7% + 5c for in-person, and 4.4% + 30c for international cards. The pricing is simple and predictable — no monthly fees, no setup costs. For ISVs processing over $100K monthly, Stripe offers custom interchange-plus pricing through its sales team.

Stripe Connect’s revenue share model requires high processing volumes before ISVs see meaningful economics. Swipesum’s analysis notes that revenue share is “only available to platforms with very high processing volumes — often in the tens of millions annually.”

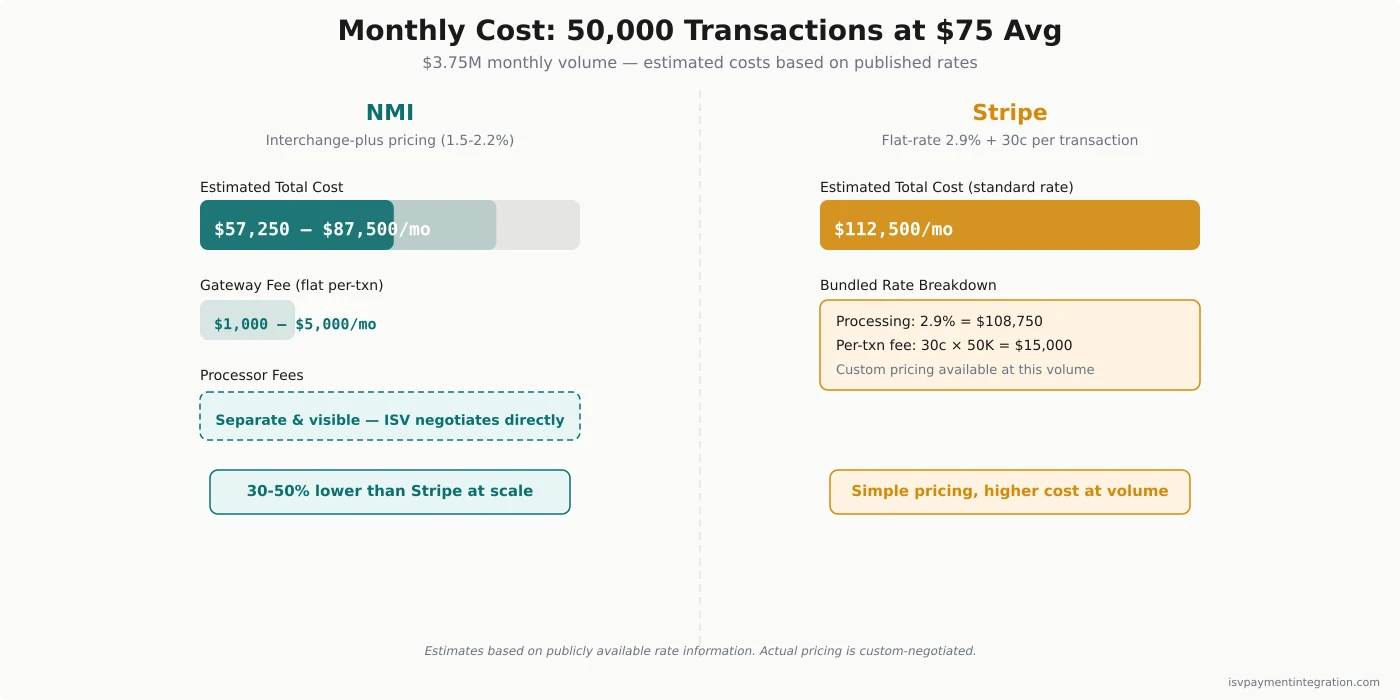

Revenue Example: 50,000 Transactions/Month

For an ISV processing 50,000 monthly transactions at $75 average ticket ($3.75M monthly volume):

- Stripe estimated cost: ~$112,500/month at standard rates (2.9% + 30c). Custom pricing available at this volume.

- NMI estimated cost: ~$56,250-$82,500/month (1.5-2.2% effective) plus flat gateway fees ($1,000-$5,000/month)

- Key difference: NMI separates gateway and processing costs so ISVs see exactly where money goes. Stripe bundles everything into one rate.

Note: Actual pricing is custom-negotiated. These estimates use publicly available rate information from Stripe’s pricing page and AGMS. Request ISV-specific pricing from both platforms.

Not sure which pricing model works better for your ISV? Get a free assessment →

Merchant Onboarding Speed

How quickly your merchants can start processing payments directly affects your ISV’s activation rates and customer satisfaction.

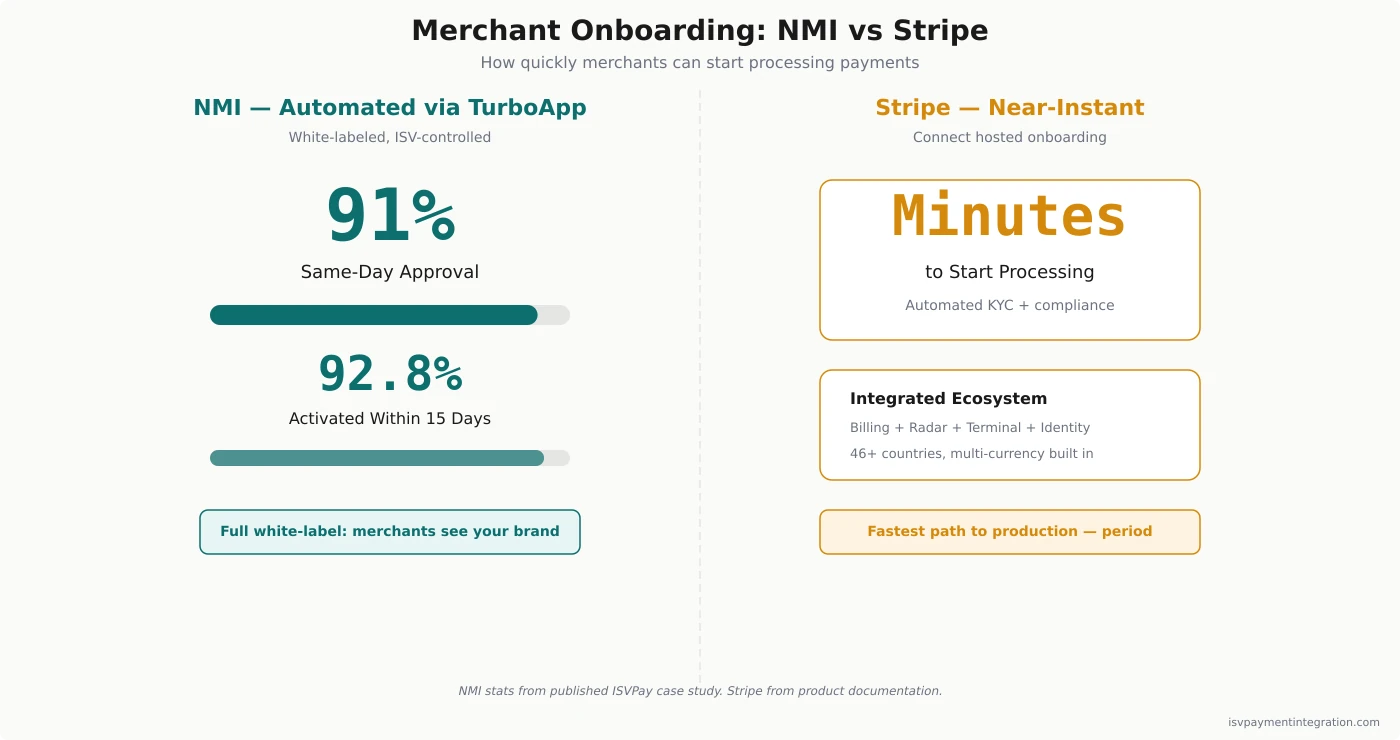

Stripe’s onboarding is near-instant. Connect’s hosted onboarding flow gets merchants accepting payments in minutes. Stripe handles KYC verification, compliance checks, and account provisioning automatically. For ISVs prioritizing merchant activation speed, this is Stripe’s strongest operational advantage.

NMI offers automated onboarding through TurboApp. In a published case study, NMI partner ISVPay achieved a 91% same-day merchant approval rate in their highest-volume month, with 92.8% of merchants activated within 15 days. Fast, but not instant — the separate acquiring relationship adds a step that Stripe’s integrated model eliminates.

For ISVs prioritizing speed: Stripe wins. For ISVs that need the onboarding flow white-labeled under their brand, NMI’s approach gives you that control at the cost of slightly slower activation.

White-Label and Branding Control

For ISVs building payment experiences inside their software, brand consistency drives merchant trust and retention.

NMI is built for white-label payment processing. The entire gateway is white-label: your merchants see your brand on the checkout, the payment portal, and the transaction receipts. NMI stays invisible. ISVs also control pricing to their merchants — you set the markup, the fee structure, and the billing terms.

Stripe takes the opposite approach. Stripe Connect handles multi-party payment flows well, but the merchant still has a Stripe account, sees Stripe branding in parts of the experience, and the underlying merchant relationship sits with Stripe. With Stripe, the pricing model is Stripe’s. You earn a share, but you don’t control the rate card.

For ISVs where branding trust drives retention — especially in B2B verticals — NMI’s white-label model is a significant differentiator.

Processor Flexibility and Gateway Independence

NMI connects to 200+ payment processors and supports 125+ shopping cart integrations. This gateway independence means your ISV can route transactions to the processor with the best rates or approval ratios for each merchant type. If a processor’s performance degrades or rates increase, you switch processors without touching your integration code.

Stripe is the processor. There is no option to route transactions elsewhere, switch acquirers for better pricing, or add a backup processor for redundancy. If Stripe’s rates, approval ratios, or risk policies don’t work for a merchant segment, you either accept it or move your entire integration.

For ISVs with diverse merchant bases — including high-risk verticals that Stripe declines — NMI’s processor-agnostic model is a structural advantage. You can onboard merchant types that Stripe would reject and route them to acquirers that specialize in those verticals.

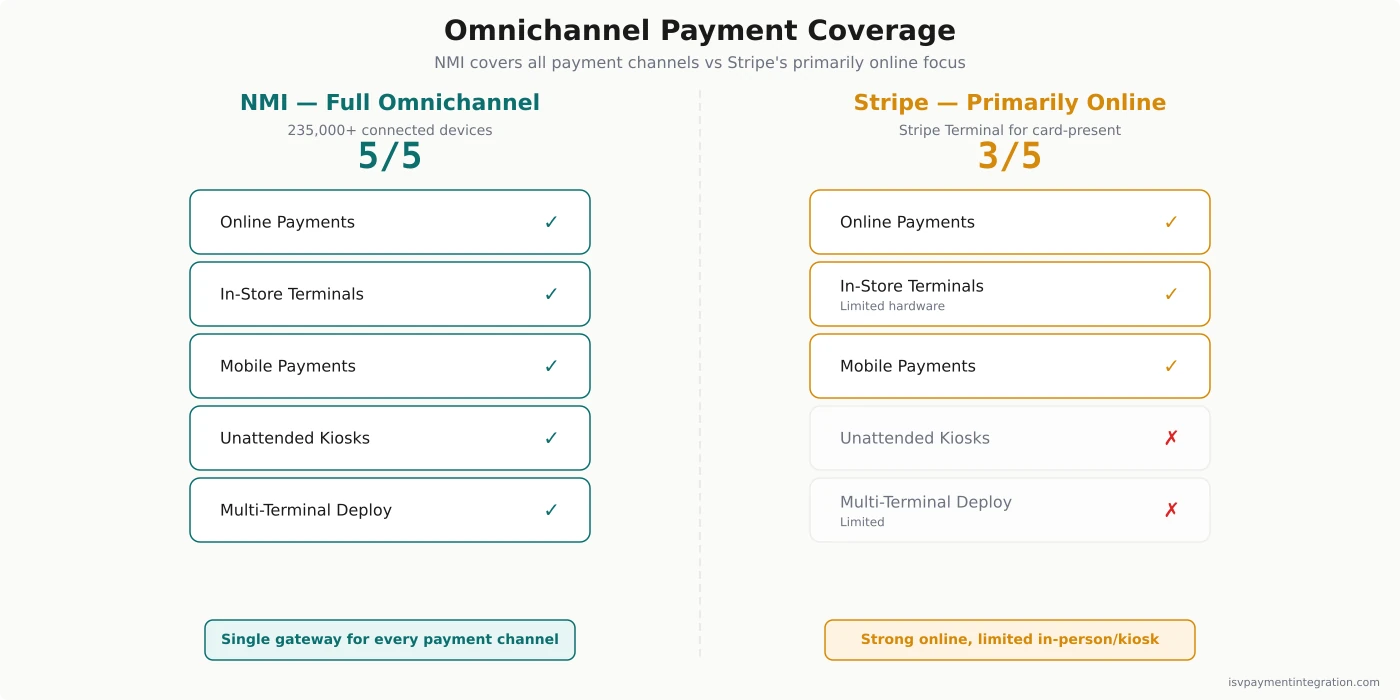

Omnichannel and In-Person Payments

NMI supports in-store terminals, online payments, mobile payments, and unattended kiosks through a single gateway. NMI connects to 235,000+ payment devices across these channels — relevant for ISVs in retail, food service, field services, and any vertical where merchants accept payments both online and at a physical location.

Stripe Terminal handles card-present payments, but the hardware selection is limited and the in-person experience is not Stripe’s strength. Unattended kiosk payments, multi-terminal deployments, and complex POS integrations are better served by NMI’s device ecosystem. If your ISV’s merchants only sell online, this distinction is irrelevant. If even 20% of them need card-present capability, NMI has a meaningful edge.

Fraud and Security

Stripe Radar is a specific competitive advantage. It uses machine learning trained on billions of transactions across Stripe’s network to adapt fraud detection rules automatically. For ISVs that don’t want to build or tune fraud rules manually, Radar provides strong out-of-the-box protection.

NMI’s fraud prevention relies on configurable rules and Kount integration for AI-powered fraud scoring. The tools are capable but require more manual configuration. Trustpilot reviewers have documented cases of fraud exposure, and NMI’s rules-based system catches fewer novel fraud patterns than Stripe’s ML approach.

Both platforms provide PCI-compliant tokenization that reduces ISV PCI scope. NMI uses gateway-level tokenization; Stripe tokenizes at the platform level.

Customer Support

Neither platform excels here, and you should plan accordingly.

NMI routes support through its partner network, which means your experience depends on which ISO or reseller you work with. Some ISV partners report dedicated account managers and fast resolutions. Others report 20-minute hold times, missed callbacks, and email responses that take over a week. NMI’s Trustpilot rating sits at 2.0 out of 5, mostly driven by support complaints.

Stripe’s support is ticket-based and self-service first. The documentation is strong enough that many issues resolve without contacting anyone. But when you need a human — especially for urgent payment issues — reaching someone quickly requires a priority support plan that costs extra. G2 and Swipesum both flag support responsiveness as a common reason ISVs start looking for alternatives.

Practical takeaway: budget for support gaps with either platform. If dedicated human support is a requirement, NMI through a strong partner channel is the better bet. If your team can self-serve from documentation, Stripe’s resources are deeper.

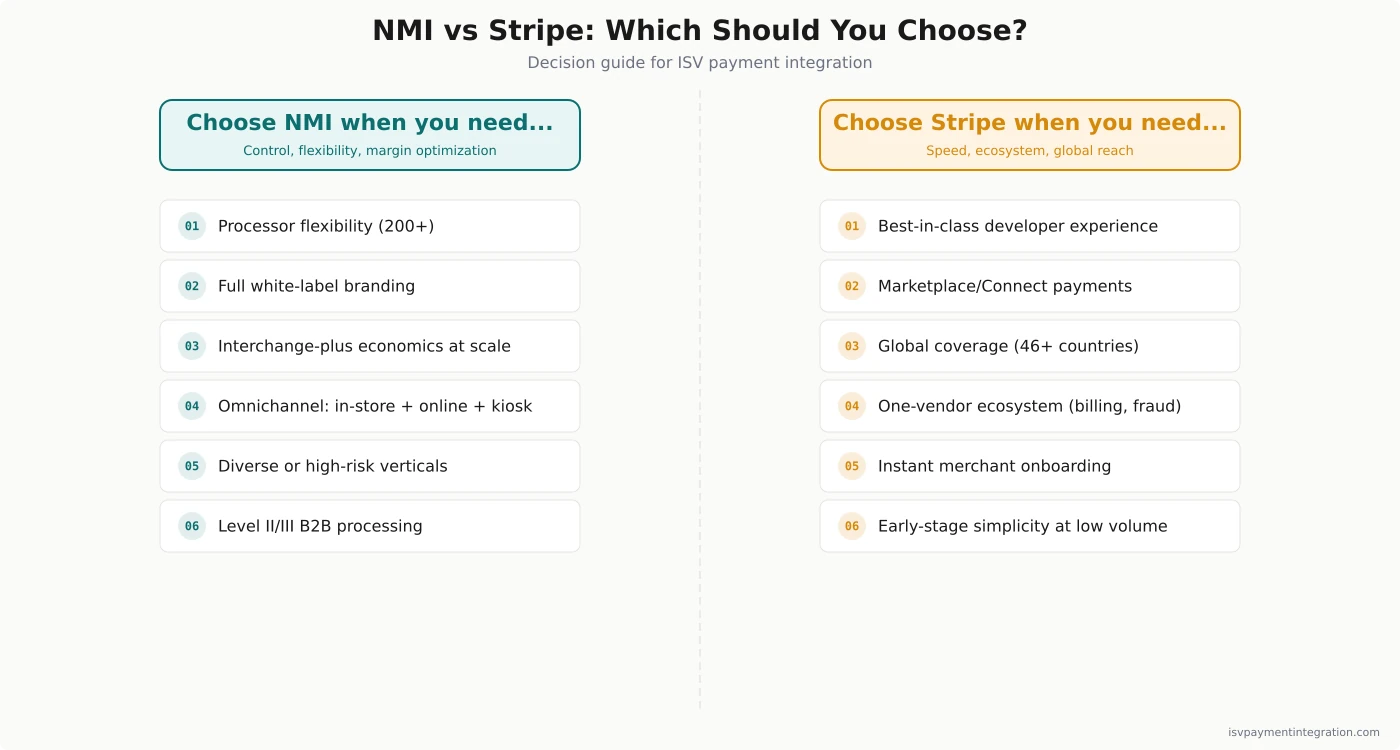

When to Choose NMI

NMI is the stronger choice for ISVs that:

- Need processor flexibility — you want to choose (or let merchants choose) from multiple processors

- Prioritize white-label branding — your merchants should never see NMI’s name

- Want interchange-plus economics — better margins at $50K+ monthly volume vs Stripe’s flat rate

- Serve omnichannel merchants — in-store + online + kiosk through one gateway

- Serve diverse or high-risk verticals — onboard merchant types Stripe won’t accept

- Need Level II/III processing — B2B ISVs saving on interchange through enhanced data

NMI also fits ISVs pursuing a PayFac-alternative model through NMI’s FACe program, which enables PayFac-like sub-merchant onboarding without the cost and compliance burden of becoming a registered payment facilitator.

When to Choose Stripe

Stripe is the stronger choice for ISVs that:

- Prioritize developer experience — fastest integration with the best documentation in the industry

- Need marketplace payments — Stripe Connect handles complex multi-party flows

- Operate globally — Stripe covers 46+ countries with built-in multi-currency support

- Want one vendor — payments, billing, invoicing, fraud (Radar), and identity in a single platform

- Need instant merchant onboarding — Connect’s hosted flow activates merchants in minutes

- Are early-stage — flat-rate pricing simplicity outweighs cost optimization at low volume

Stripe’s fraud tooling is a specific advantage. Stripe Radar uses machine learning trained on billions of transactions. NMI’s fraud prevention relies on configurable rules that require more manual tuning.

Consider a Third Option

NMI and Stripe represent two ends of a spectrum: maximum gateway flexibility (NMI) versus maximum platform integration (Stripe). Some ISVs find that neither extreme fits.

ISV-first embedded payment platforms like Xplor Pay bridge this gap — offering white-label capabilities and ISV-focused onboarding with integrated acquiring and dedicated support. See how they compare in our Xplor Pay vs NMI and Xplor Pay vs Stripe analyses. If your ISV needs embedded payments without choosing between flexibility and simplicity, it’s worth a conversation.

Get a personalized comparison for your ISV →

Frequently Asked Questions

Is NMI better than Stripe for ISVs?

It depends on your ISV’s priorities. NMI is better for white-label control, processor flexibility, and interchange-plus economics at scale. Stripe is better for developer experience, global reach, and integrated fraud tooling. The right choice maps to your merchant base, technical resources, and revenue model.

Can I switch from Stripe to NMI?

Yes, but expect the migration to take longer than quoted. Token migration, webhook rewiring, reporting changes, and fee reconciliation all need attention. Plan for weeks, not days — one HighLevel community user reported a migration promised in “1-2 days” that took a full month. Some ISVs run both platforms in parallel during the transition.

What is NMI’s pricing model?

NMI uses interchange-plus pricing distributed through its partner network (ISOs and resellers). Rates are custom and depend on your ISV’s volume, integration depth, and the partner you work with. Always get pricing in writing and ask about monthly fees, PCI compliance charges, and early termination terms.

Does NMI support recurring billing?

Yes. NMI’s Customer Vault stores payment credentials securely, and its API supports subscription creation, management, and automated retry logic for failed payments. Recurring billing works for both card-not-present and ACH transactions. For more advanced subscription needs (metered billing, revenue recovery, proration), Stripe Billing has deeper capabilities.

How does Stripe Connect compare to NMI for marketplace ISVs?

Stripe Connect is purpose-built for marketplace and multi-sided platform payments — it handles split payments, connected accounts, and payouts natively. NMI can support marketplace flows but requires more custom development. If your ISV operates a marketplace model, Stripe Connect is the stronger fit.

The Bottom Line

NMI and Stripe serve different ISV profiles. NMI wins on white-label control, processor flexibility, and interchange-plus economics — it’s the platform for ISVs that want to own every aspect of the payment experience and serve merchants across diverse verticals. Stripe wins on developer experience, global reach, and platform breadth — it’s the platform for ISVs that want the fastest path to production with the strongest ecosystem of integrated tools.

Neither platform is universally “better.” The right choice depends on your ISV’s specific vertical, transaction volume, technical resources, and how much of the payment experience you want to own. For more context, see how NMI stacks up against other gateways in our Adyen vs NMI and Braintree vs NMI comparisons, or explore Stripe vs Adyen and Stripe vs Braintree for alternative full-stack options.

Need help evaluating which platform fits your ISV? Get a free integration assessment →