NMI Review

Processor-agnostic white-label gateway with 200+ acquirer connections, purpose-built for ISVs, ISOs, and PayFacs that want acquirer flexibility instead of single-vendor lock-in.

Overview

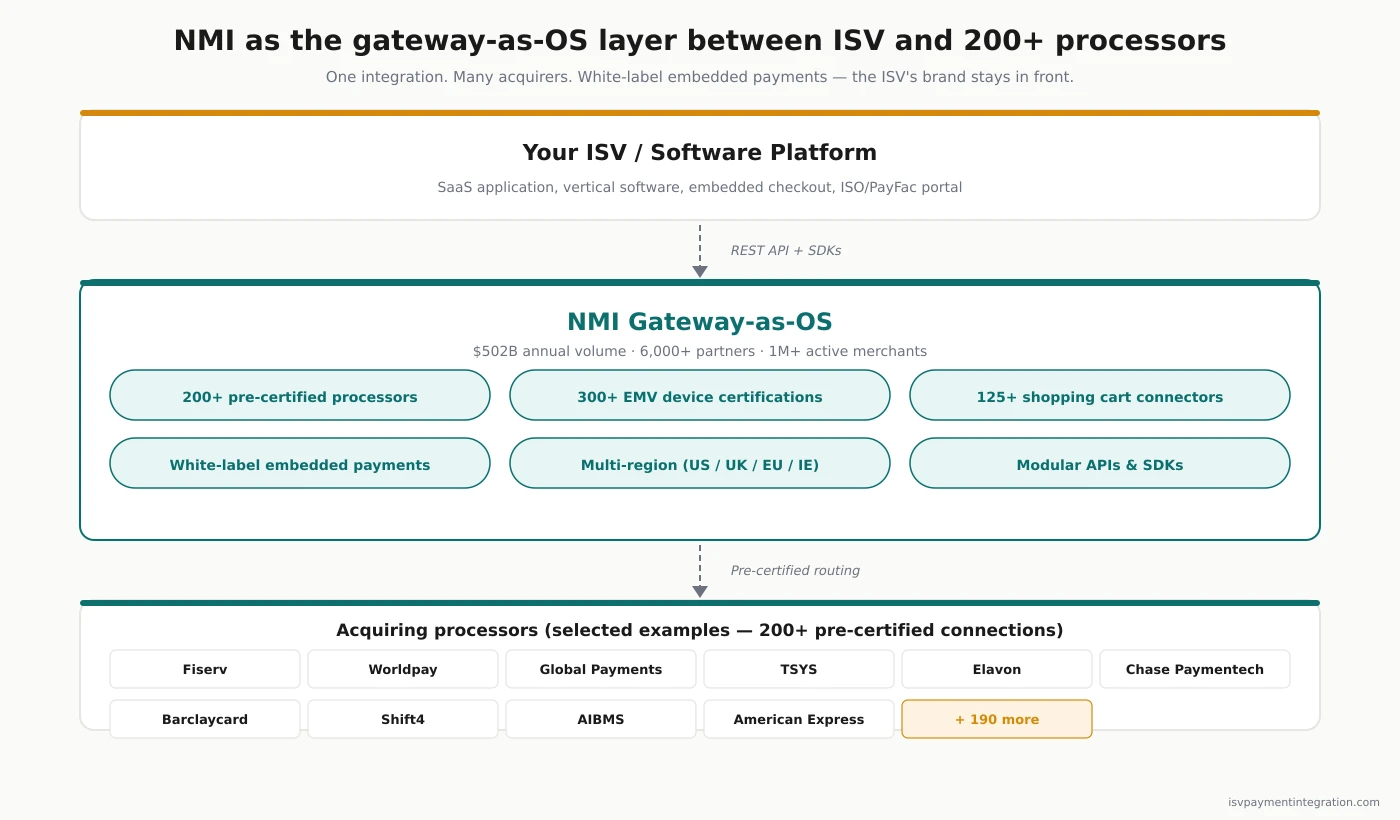

Network Merchants Inc. (NMI) is a Schaumburg, Illinois-based payments technology company founded in 2001 and now backed by Francisco Partners, Great Hill Partners, and Insight Partners. The platform processes $502 billion annually for over 6,000 technology partners and more than one million active merchants worldwide. For ISVs, NMI is the gateway-first alternative to vertically integrated processors like Stripe and Global Payments — the value proposition is processor-agnosticism (200+ pre-certified acquirer connections, 300+ EMV device certifications), white-label embedded payments, and a partner-first commercial model where ISVs control merchant pricing instead of inheriting a fixed Stripe-Connect-style platform fee.

For the latest on NMI's ISV capabilities, documentation, and partner programs, visit nmi.com.

Pricing

Gateway-as-a-Service + ISV-controlled merchant pricing

NMI's commercial model separates gateway economics from acquiring economics. The ISV pays NMI a per-transaction gateway fee plus monthly platform fees, then layers its own markup on top of whichever acquirer the merchant routes through. Pricing is partner-negotiated and not publicly published. Standard contracts are partner-specific rather than the 3-year auto-renewing structure typical of acquirer-direct relationships.

Full pricing breakdown →Pros

- ✓ 200+ pre-certified processor connections give ISVs and ISOs true acquirer flexibility — switch acquirers per merchant, per geography, or for cost optimization without re-coding

- ✓ White-label embedded payments — the platform stays invisible so the ISV's brand owns the merchant relationship, not NMI

- ✓ 300+ EMV device certifications across Ingenico, ID TECH, Madic, Payter, FEIG, LANDI cover ecommerce, in-person, mobile, and unattended/self-service in a single integration

- ✓ Merchant Central + ScanX/MonitorX automate sub-merchant underwriting (100+ risk checks, minutes-not-days decisioning) without the ISV registering as its own PayFac

- ✓ Named ISO/ISV reference partners (Wind River Financial, ISVPay, Anovia Payments) demonstrate real-world ISV-on-NMI deployments — not anonymous case studies

- ✓ Geographic coverage spans US, UK, EU, and Republic of Ireland with locally certified device estates — broader than US-only ISV-focused processors like Clearent or Payrix

Cons

- ✗ NMI is a gateway, not a processor — ISVs still need an acquirer relationship (direct, or through an NMI-partnered ISO), which adds a vendor and a contract to the stack

- ✗ Pricing is partner-negotiated and not publicly published — no headline rate exists, so ISVs must engage sales to get real economics

- ✗ Trustpilot 2.0/16 rating exposes recurring downstream-merchant complaints (support unresponsiveness, surprise/increased pricing, billing-after-cancellation) that ISVs absorb as brand risk via the ISO/PayFac chain

- ✗ Customer service quality scales with the partnered ISO/PayFac — direct merchants who reach NMI itself often report transferred-and-held-on-hold experiences

- ✗ Developer experience is workmanlike rather than category-leading — APIs and SDKs work but the docs, sandbox polish, and DX velocity lag Stripe and Adyen

- ✗ Brand is wholesale / B2B — recognition among end-merchants and developers is far lower than Stripe, Adyen, or Square, which can become a buying objection in some merchant evaluations

ISV Fit

Strong fit for ISVs and ISOs that want acquirer-independence, omnichannel coverage (especially unattended/self-service and EU/UK device estates), and a white-label experience where the ISV's brand stays in front. Best when the ISV is willing to negotiate commercial terms, manage at least one downstream acquirer relationship, and prioritize processor flexibility over the all-in-one developer ergonomics of Stripe Connect. Weaker fit for early-stage ISVs that need self-serve speed, US-only platforms with no need for multi-acquirer routing, or ISVs whose merchants will read Trustpilot before signing — NMI's wholesale brand carries downstream-merchant complaints that the ISV's brand has to absorb.

NMI Review: An ISV’s Perspective (2026)

Most NMI reviews are written by end-merchants who got NMI through a downstream ISO or PayFac and don’t fully understand the architecture they’re standing on. This review isn’t that. This is NMI evaluated as an ISV infrastructure choice — a payment gateway that sits between a software platform and any of 200+ acquiring processors, designed to let the ISV stay in control of brand, pricing, and acquirer routing.

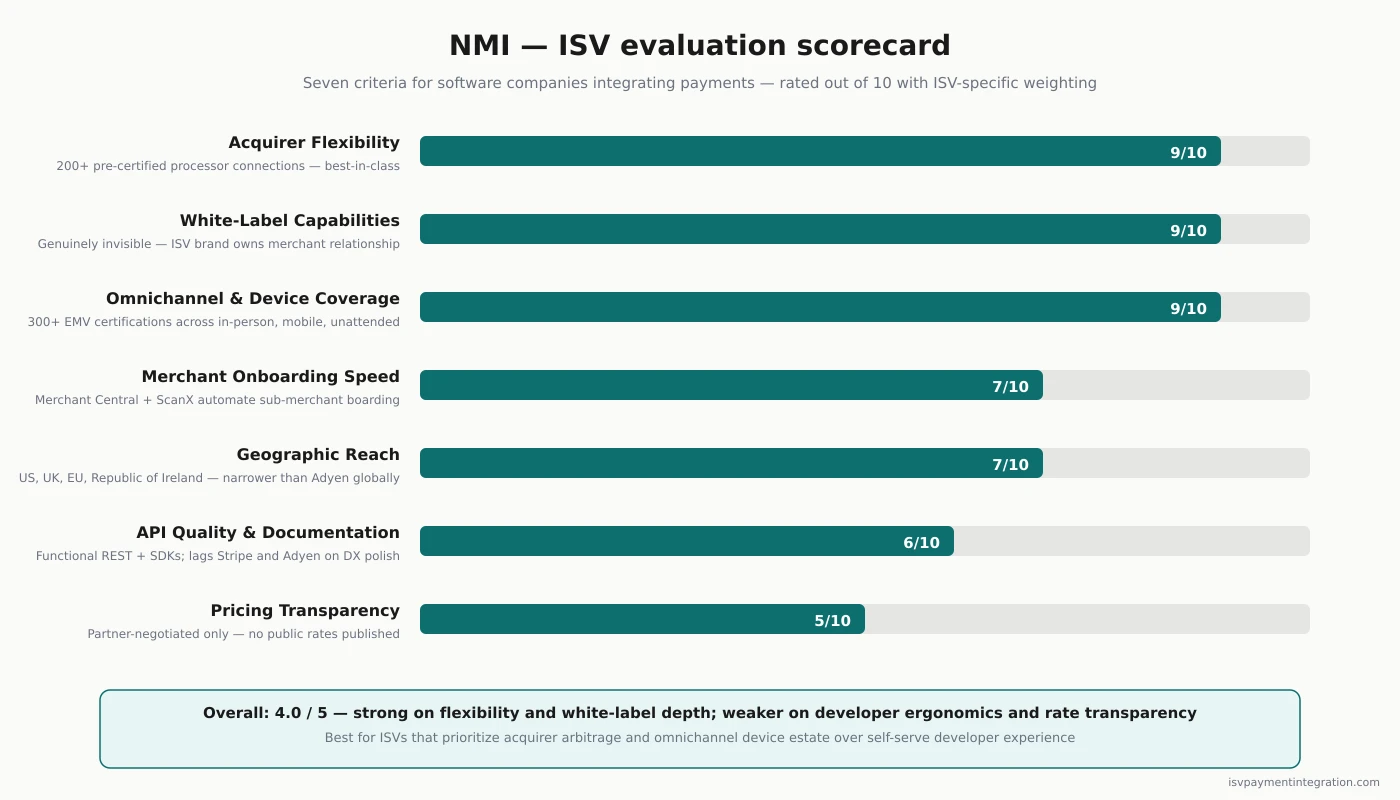

NMI scores 4.0/5 in our ISV-focused evaluation. That rating weighs processor-agnosticism, white-label depth, omnichannel device coverage, and the flexibility to negotiate ISV-favorable economics. It’s a different rating than you’ll find on Trustpilot or Capterra, where the customer base is downstream merchants evaluating a different product entirely.

What NMI Actually Is — A White-Label Gateway, Not a Processor

The single most important fact about NMI for any ISV: NMI is a payment gateway, not a payment processor. That distinction reshapes everything downstream — the integration architecture, the contract structure, the revenue economics, and the kind of merchant problems NMI can and can’t solve.

A processor (Stripe, Adyen, Worldpay, Global Payments, Fiserv, Chase Paymentech) sits on the acquiring rails — they have the BIN sponsorship, the bank relationships, the interchange-plus economics. A gateway (NMI, Authorize.Net, Braintree’s gateway layer) is the technology layer that takes a transaction from a merchant’s point-of-sale or website and routes it to a processor. A gateway-only company doesn’t acquire — it brokers.

NMI’s positioning is built on owning that broker layer at scale. According to NMI’s own about page, the platform now powers $502 billion in transactions every year for over 6,000 technology partners and more than one million merchants globally. That’s a scale where the gateway’s opinions about processor connectivity, device certifications, and embedded-payments tooling start to matter to the entire ISV ecosystem, not just NMI’s direct customers.

What that means for ISVs

If your software platform integrates NMI, you get:

- One integration, many acquirers. The 200+ pre-certified processor connections include First Data/Fiserv, Worldpay/Global Payments, TSYS, Elavon, Chase Paymentech, Barclaycard, and dozens of regional acquirers. Your ISV writes one integration; your merchants can be settled by whichever processor offers them the right economics, geography, or vertical fit.

- 300+ EMV-certified payment devices. Ingenico, ID TECH, Madic, Payter, FEIG, and LANDI hardware all work out of the box across US, UK, EU, and Republic of Ireland geographies. For ISVs with parking, vending, transit, kiosk, EV charging, or other unattended/self-service merchants, that device estate is genuinely hard to replicate.

- 125+ shopping cart connectors for ecommerce-flavored ISV deployments, plus low-code and no-code components for partners that don’t want to build the full payment UI from scratch.

- No acquirer relationship of NMI’s own. Your platform still needs an acquirer somewhere in the stack. NMI partners with hundreds of ISOs and PayFacs that supply the BIN side, or your ISV brings its own.

The model is deliberately not Stripe Connect. Stripe Connect bundles gateway, acquirer, risk, compliance, and PayFac-as-a-Service into one vertically integrated product with a fixed platform-fee economic model. NMI unbundles those layers and lets the ISV assemble its preferred stack — gateway always NMI, acquirer/PayFac negotiable, value-added services modular.

Ownership, Scale, and Leadership Transition

NMI was founded in 2001 in Schaumburg, Illinois, where its headquarters still sit at 1450 American Lane. The company spent its first decade building one of the early independent gateways for online payments and eventually pivoted toward the embedded-payments and ISV/ISO partner model that defines it today.

The PE chain

NMI’s ownership has moved through three private-equity hands across roughly a dozen years:

- 2013 — Bregal Sagemount made the initial significant investment.

- 2014 — Great Hill Partners came in with a growth investment, joining Bregal.

- September 2017 — Francisco Partners acquired NMI from Bregal Sagemount, with Great Hill Partners retaining a stake. Bregal exited.

- September 2021 — Insight Partners made a strategic growth investment, joining Francisco Partners and Great Hill Partners. CEO Vijay Sondhi and the management team co-invested.

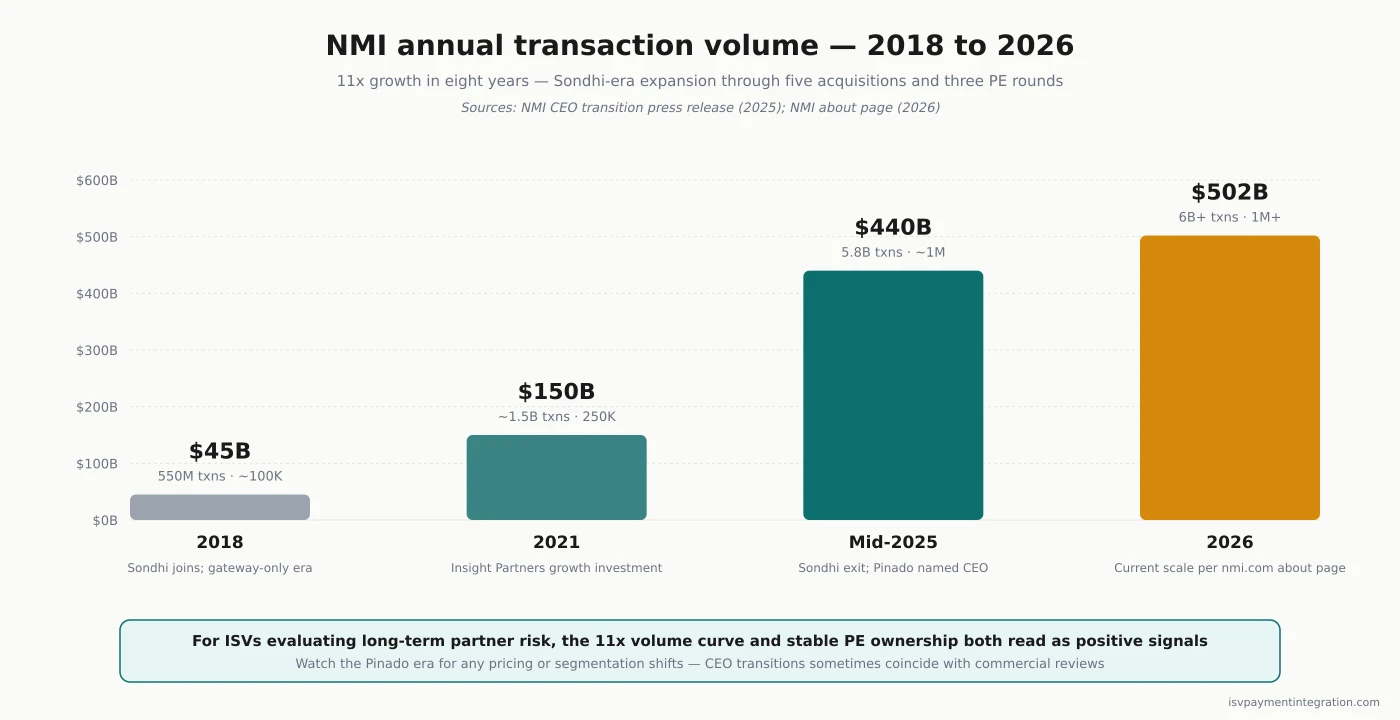

The current ownership trio — Francisco Partners ($24B+ raised across 200+ companies), Great Hill Partners, and Insight Partners ($30B+ raised across 400+ companies) — gives NMI deep capital, strategic patience, and three different sets of fintech investment theses pulling in roughly the same direction. For ISVs evaluating long-term partner risk, that stable PE backing reads as positive — gateway companies that flip between owners every two years tend to ship product roadmaps that flip with them.

The growth story under Sondhi

NMI’s CEO transition press release puts the Sondhi-era growth in concrete terms: from 550 million transactions and $45 billion in annual volume in 2018 to 5.8 billion transactions and $440 billion annually by mid-2025, with merchants growing nearly tenfold to over a million. That’s the kind of scale curve that justifies the gateway-as-platform positioning rather than the traditional gateway-as-utility framing.

The September 2025 leadership change

On September 2, 2025, Steven Pinado succeeded Vijay Sondhi as CEO. Pinado came in with thirty years of fintech experience, most recently as a Partner at Radian Capital and previously President of Billtrust (which he led through both an IPO and a subsequent sale). Sondhi remained as a strategic advisor through the end of 2025 to ensure continuity.

For ISVs evaluating NMI in 2026, the practical implication is that the company’s product strategy has continuity through the transition — Pinado’s mandate is explicitly to extend the embedded-payments roadmap, not to redirect it. But it’s worth tracking whether the Pinado era introduces any commercial-terms shifts; CEO transitions at PE-backed companies sometimes coincide with pricing reviews and segmentation changes, the same pattern that surfaced post-rebrand at Clearent.

NMI as an ISV/SaaS Partner: The Real Product

Beyond the gateway plumbing, NMI’s actual product surface for ISVs spans onboarding, lifecycle management, risk, and embedded financing. The components that matter most for ISV evaluation:

NMI Payments (the all-in-one platform)

The flagship product wraps the gateway, embedded payments tooling, and acceptance platform into a single offering. ISVs get a feature-rich PCI-compliant gateway, modular APIs and SDKs, low-code and no-code components, and “20+ years of experience leading innovation in payments” (NMI’s framing). The product targets ISVs that want most of what a PayFac-as-a-Service delivers — fast merchant decisioning, monetized payments, flexible options — without the operational overhead of registering as a payment facilitator themselves.

Merchant Central (CRM and underwriting)

Merchant Central is the residual management, agent payout, marketing automation, and merchant onboarding hub. The case study on ISVPay — an Alpharetta, Georgia ISO focused on unattended-payments ISVs — describes how Merchant Central’s TurboApp portal centralized and automated the entire merchant onboarding workflow through a single interface. For ISVs running an ISO-owned downstream channel, that consolidation is real operational leverage.

ScanX / MonitorX (risk)

The risk product runs 100+ checks per merchant application and produces a risk-scored report in minutes rather than days. That’s the underwriting-automation engine that makes the embedded-payments pitch credible — without it, sub-merchant onboarding becomes a bottleneck that defeats the activation-rate value of integrating payments in the first place.

Business Capital (embedded merchant financing)

Newer to the lineup, Business Capital lets ISVs offer merchant financing inside their own product. It’s a value-added revenue line that competes with Stripe Capital and Square Capital in the lending-on-payment-history product category.

Named partners that prove the model

Public NMI case studies surface real partners using these components:

- Wind River Financial — an ISO and payment processing company that supplies payment technology to a “large base” of ISV integrations. Wind River reports a 25% transaction increase and 10% customer satisfaction lift after integrating with NMI.

- ISVPay — the unattended-payments-focused ISO mentioned above.

- Anovia Payments LLC — a registered ISO/MSP of Merrick Bank, Wells Fargo Bank, and Elavon DAC, named in NMI’s product page footer.

That’s a partner roster narrower than what processors like Adyen or Stripe publish, but the named ISO partners genuinely operate the ISV-services-on-NMI model the platform is selling. For ISVs evaluating NMI, the most valuable reference call is one with Wind River or ISVPay, not with NMI sales directly.

Revenue Economics for ISVs

NMI’s commercial model is unusual in the ISV-payments landscape because it splits the economics across two layers — gateway and acquirer — that other platforms bundle. That’s a feature for ISVs who know what they want, and a liability for ISVs that just want one number.

The gateway layer

NMI charges the ISV a per-transaction gateway fee plus monthly platform fees. The exact numbers are partner-negotiated and not publicly published; volume, vertical, geography, and the breadth of NMI products consumed (Merchant Central, ScanX, Business Capital) all factor in. For ISVs, the gateway layer is a relatively predictable cost line that scales with transaction count, not transaction value.

The acquirer layer

The actual interchange-plus economics live with whichever acquirer the merchant is settled by. NMI doesn’t take interchange itself — that flows through to the partnered ISO, PayFac, or direct acquirer. The ISV’s revenue share is typically negotiated with the acquirer side of the stack, not with NMI, although NMI’s tooling makes it easier to manage residuals across multiple acquirer relationships.

What this means for margin

The bundled-economics platforms (Stripe Connect’s flat platform-fee model, Adyen’s MarketPay) give the ISV a single number to negotiate and a single contract to sign — at the cost of acquirer flexibility. NMI’s split-economics model gives the ISV genuine acquirer arbitrage — different acquirers, different geographies, different vertical specializations, all behind the same NMI integration — but requires the ISV to manage two commercial relationships.

For ISVs with sophisticated payments teams or multi-vertical merchant bases, the split-economics model is a feature. For ISVs that want one vendor, one contract, and a managed-services experience, it’s friction.

Why this is hard to compare on a public-rates page

Most payment-processor pricing pages publish a headline rate (“2.9% + $0.30”) because they bundle gateway, acquirer, and risk into one product. NMI can’t publish a comparable rate because the rate depends on which acquirer the merchant ends up on. That’s why our pricing page for NMI covers the model architecture rather than specific basis points — the specifics live in the partner contract, not the website.

Merchant Pain Points ISVs Must Understand

When an ISV integrates NMI as its payments platform, the ISV’s brand sits in front of every merchant interaction. Some of those merchants will eventually search for NMI directly, find Trustpilot, Reddit, or industry forums, and read complaints written by other downstream merchants on entirely different acquirer chains. Those complaints become, indirectly, complaints about the ISV’s payment experience. The honest version of an ISV evaluation has to underwrite that risk rather than wave it away.

What the public review record shows

NMI’s Trustpilot profile is unclaimed and carries a 2.0/5 rating across 16 total reviews. That’s a small sample by consumer-services standards — Stripe has 17,000+ Trustpilot reviews — and the small N is itself a signal: NMI sells primarily to ISVs, ISOs, and PayFacs, not to end-merchants directly, so the people who do show up on Trustpilot are usually downstream merchants who’ve had a problem and are looking for an escalation channel.

The patterns in those reviews recur across multiple sources:

- Customer support unresponsiveness. Multiple reviews cite long hold times, transferred-and-held experiences, and meeting no-shows. One reviewer describes booking three meetings and getting stood up three times.

- Surprise pricing changes and rate creep. A January 2026 reviewer wrote: “This is the 3rd or 4th time with surprise increased pricing, into the thousands. Don’t see how any sales office can run their business with surprise billing.” That’s the same rate-creep pattern documented at other PE-backed processors and gateways — ISVs should ask explicitly about pricing-change notification clauses.

- Billing-after-cancellation. A June 2025 UK reviewer reported that Network Merchants Limited (NMI’s UK entity) continued billing for two months after a Worldpay account cancellation. That’s the same anti-pattern documented at Clearent, Stax, and several other processors with multi-tier downstream channels — the cancellation request gets caught between the partner ISO and the underlying gateway.

- Fraud handling. One review describes NMI suggesting a victim of card fraud “reach out to the fraudulent merchant directly to resolve the issue.” That’s a documentation problem if accurate — NMI’s fraud workflow as advertised doesn’t read that way — but the ISV-implication is that downstream-merchant fraud experiences become brand events the ISV’s support team has to absorb.

Why this matters for ISV decision-making

An ISV’s brand is the abstraction layer that hides NMI from end-merchants. When that abstraction holds, NMI’s wholesale-tier complaints stay invisible. When it leaks — when a merchant searches for “NMI” because the platform name appears on a billing descriptor or a reconciliation report — the ISV inherits the brand exposure.

The mitigation isn’t to avoid NMI; it’s to (a) confirm the descriptor / brand surfacing in the merchant flow stays under the ISV’s brand, (b) read the partner SLAs around support escalation and cancellation processing, and (c) pre-position support content so merchants reach the ISV’s support before they reach Trustpilot.

What NMI Does Better Than Most

The complaint surface is real, but the platform also has genuine strengths that don’t surface in a Trustpilot-only read.

Acquirer-agnostic switching. Few gateways match NMI’s processor connectivity at this scale. ISVs that have either changed acquirers or had their acquirer go through M&A (Worldpay → Global Payments, First Data → Fiserv, etc.) report being able to keep their NMI integration intact while migrating the underlying acquiring relationship. That’s a switching-cost eraser that pure Stripe Connect or Adyen-bundled platforms don’t offer.

Unattended and self-service device coverage. The 300+ EMV device certifications include parking, vending, transit, kiosk, EV-charging, and outdoor-environment readers from Ingenico, FEIG, Payter, Madic, and LANDI. ISVs serving those verticals — Wind River and ISVPay both cite this segment — have effectively two viable gateway choices: NMI or a vertical-specialist processor. NMI’s geographic reach and device breadth make it the structurally easier option for multi-region deployments.

EU/UK depth without re-architecting. NMI’s UK entity (Network Merchants Limited) and EU device certifications mean ISVs expanding from US-only to multi-region don’t need to swap gateways at the border. That’s a meaningful difference from Clearent or Payrix, both of which have narrower geographic footprints.

Modular, white-label embedded payments. The platform really is invisible — partners can run a full embedded-payments experience with NMI nowhere on the merchant-facing surface. Stripe Connect technically supports white-label, but the practical reality of Stripe-branded onboarding documents and Stripe-tagged compliance flows leaks the brand. NMI’s white-label is closer to genuinely transparent.

Behind-the-scenes acquisitions. NMI acquired Agreement Express’s payments solutions (date undisclosed in press) and made five total acquisitions during the Sondhi era, expanding capabilities across in-person, online, unattended, and mobile commerce. The acquisitive growth strategy means the platform expands faster than a pure organic build can deliver.

How NMI Compares to Other ISV-Focused Platforms

Every ISV evaluating payments infrastructure should benchmark at least three platforms. Where NMI lands depends on which axes the ISV weights highest.

vs Stripe Connect — gateway-first vs SaaS platform generalist

Stripe Connect is the default for SaaS platforms that want bundled gateway/acquirer/risk and best-in-class developer ergonomics across the broadest geography. NMI is the choice when acquirer flexibility, multi-acquirer routing, and unattended-payments device coverage matter more than developer-tooling polish. Most ISVs that “outgrow” Stripe end up either negotiating deeper with Stripe (Connect Custom, interchange-plus) or migrating to a gateway-first model — NMI is the most common destination for the second path.

vs Global Payments — gateway alone vs gateway plus acquiring at scale

Global Payments is a full-stack acquirer with its own embedded-payments product (Genius) and direct ISV partnerships. The choice between the two depends on whether the ISV wants single-vendor accountability (Global Payments) or unbundled flexibility with an independent gateway (NMI). NMI also supports merchants settled by Global Payments — they appear in NMI’s certified processor list — so the question is one of commercial structure, not technical compatibility.

vs Stax (formerly Fattmerchant) — gateway approach vs subscription-pricing acquirer

Stax sits in a different commercial frame — flat-monthly subscription pricing on top of interchange instead of gateway-fee plus acquirer-bundled economics. Stax fits ISVs whose merchants are predictable, mid-volume, and price-sensitive on rate transparency. NMI fits ISVs whose merchants vary in volume, geography, and channel mix and benefit from acquirer optionality.

vs Clearent / Xplor Pay — gateway-first vs vertical SaaS PFaaS

Clearent, now operating as Xplor Pay, is the relationship-managed vertical-SaaS-focused alternative. Clearent has pre-tuned underwriting for dental, medical aesthetics, fitness, home services, and field services — verticals where NMI is competent but not specialized. The pick depends on whether the ISV’s vertical is one Clearent has explicitly tuned for. If yes, Clearent is often the cleaner choice. If no, NMI’s acquirer flexibility usually wins.

vs Authorize.Net — both are gateways, different parent dynamics

Authorize.Net is the other major US gateway brand — owned by Visa via the 2010 CyberSource acquisition. The functional overlap with NMI is large; the differentiation is corporate. Authorize.Net’s product velocity has been described as steady-state under Visa stewardship, while NMI’s PE-backed acquisitive growth produces faster product churn. ISVs valuing stability often pick Authorize.Net; ISVs valuing modular growth pick NMI.

Who NMI Fits — and Who It Doesn’t

Strong fit

- ISVs and ISOs that want acquirer-independence — the ability to swap or layer multiple acquirers behind a single gateway integration

- Platforms serving unattended, self-service, kiosk, transit, parking, EV-charging, or vending merchants — NMI’s device estate is hard to replicate

- ISVs expanding from US-only to UK, EU, or Republic of Ireland that want one gateway integration across geographies

- ISOs and PayFacs that need residual management, automated underwriting, and onboarding workflows in a single CRM (Merchant Central)

- ISVs that want a white-label embedded payments experience with the platform brand fully invisible to merchants

Weaker fit

- Early-stage ISVs prioritizing self-serve speed and developer ergonomics over acquirer flexibility — Stripe Connect or Finix are usually faster

- US-only platforms with no need for multi-acquirer routing — a single bundled processor (Stripe, Adyen, Global Payments) is operationally simpler

- ISVs whose merchants are likely to read Trustpilot before signing — NMI’s wholesale-tier complaint surface can become a buying objection that the ISV has to defuse mid-sale

- Platforms in verticals with named-specialist alternatives (dental, medical aesthetics, fitness) where Clearent / Xplor Pay or vertical-tuned competitors offer better pre-built underwriting

- ISVs without the bandwidth to manage two commercial relationships (gateway and acquirer) and a partner-negotiated pricing process

Frequently Asked Questions

Is NMI a payment processor? No. NMI is a payment gateway, not a processor. It connects merchants and software platforms to 200+ acquiring processors (Fiserv, Worldpay/Global Payments, TSYS, Elavon, Chase Paymentech, Barclaycard, and more) but does not hold a BIN sponsorship or acquire transactions itself. ISVs integrating NMI still need an acquirer relationship somewhere in the stack.

Who owns NMI? NMI is privately held and backed by three private equity firms: Francisco Partners (lead investor since September 2017), Great Hill Partners (since 2014), and Insight Partners (since September 2021). Founder and earliest backer Bregal Sagemount exited in the 2017 transaction.

Where is NMI headquartered? NMI is headquartered at 1450 American Lane, Schaumburg, Illinois. The company also operates a UK entity (Network Merchants Limited) supporting its EU and UK certified-device estate.

How many merchants and partners does NMI serve? According to NMI’s own about page, the platform processes $502 billion in transactions annually for over 6,000 technology partners (ISOs, PayFacs, and SaaS providers) and more than one million active merchants worldwide.

Does NMI publish pricing? No. NMI’s commercial terms are partner-negotiated and not publicly listed. The model separates a per-transaction gateway fee plus monthly platform fees from the acquirer-side interchange-plus economics, which live with the partnered ISO, PayFac, or direct acquirer. ISVs evaluating NMI need to engage sales for specific numbers.

Is NMI good for software companies and SaaS platforms? Yes, when the ISV’s priorities match what NMI does well: acquirer flexibility, white-label embedded payments, omnichannel device coverage (especially unattended), and multi-region deployment. ISVs prioritizing self-serve speed, single-vendor simplicity, or vertical-specialist underwriting often pick a different platform — Stripe Connect for self-serve, Global Payments for single-vendor, Clearent for vertical SaaS specialization.

What is the difference between NMI and Authorize.Net? Both are major US payment gateways with broadly overlapping technical capabilities. The principal differences are corporate: Authorize.Net is owned by Visa (via the 2010 CyberSource acquisition) and operates with the cadence of a strategic Visa asset; NMI is privately held by three PE firms and operates with a more acquisitive, faster-iteration roadmap. NMI also has a broader device estate for unattended/self-service and EU/UK geographies; Authorize.Net has a longer-tenured developer ecosystem in the US.

The Bottom Line for ISVs

NMI is the gateway-first answer for ISVs that want acquirer flexibility, white-label embedded payments, and omnichannel device coverage that scales beyond the bundled-platform offerings. The product is real, the partner roster is named and verifiable, the PE backing is stable, and the leadership transition into Steven Pinado looks continuous rather than disruptive.

The trade-offs are real too. NMI is not the right pick for ISVs that want one vendor, one contract, public rates, and self-serve onboarding — Stripe Connect, Adyen, or Square’s developer tier handle that better. NMI also carries downstream-merchant complaint surface that ISVs absorb through their brand; ISVs whose merchants will research the gateway directly need to plan for that brand exposure.

For ISVs whose roadmap genuinely benefits from acquirer arbitrage — multi-region, multi-acquirer, or unattended/self-service-heavy — NMI is the gateway most likely to match the next five years of platform evolution. For everyone else, the simpler bundled platforms usually win on operational overhead even when they cost more on the margin.

For the full pricing model, see the NMI pricing breakdown. For head-to-head decisions, the NMI vs Stripe and NMI vs Global Payments comparisons map the platform-vs-bundle decision in detail.