Adyen Review

Enterprise and platform payments with Adyen for Platforms, Capital, Issuing, and Accounts — unified online, in-store, and embedded commerce.

Overview

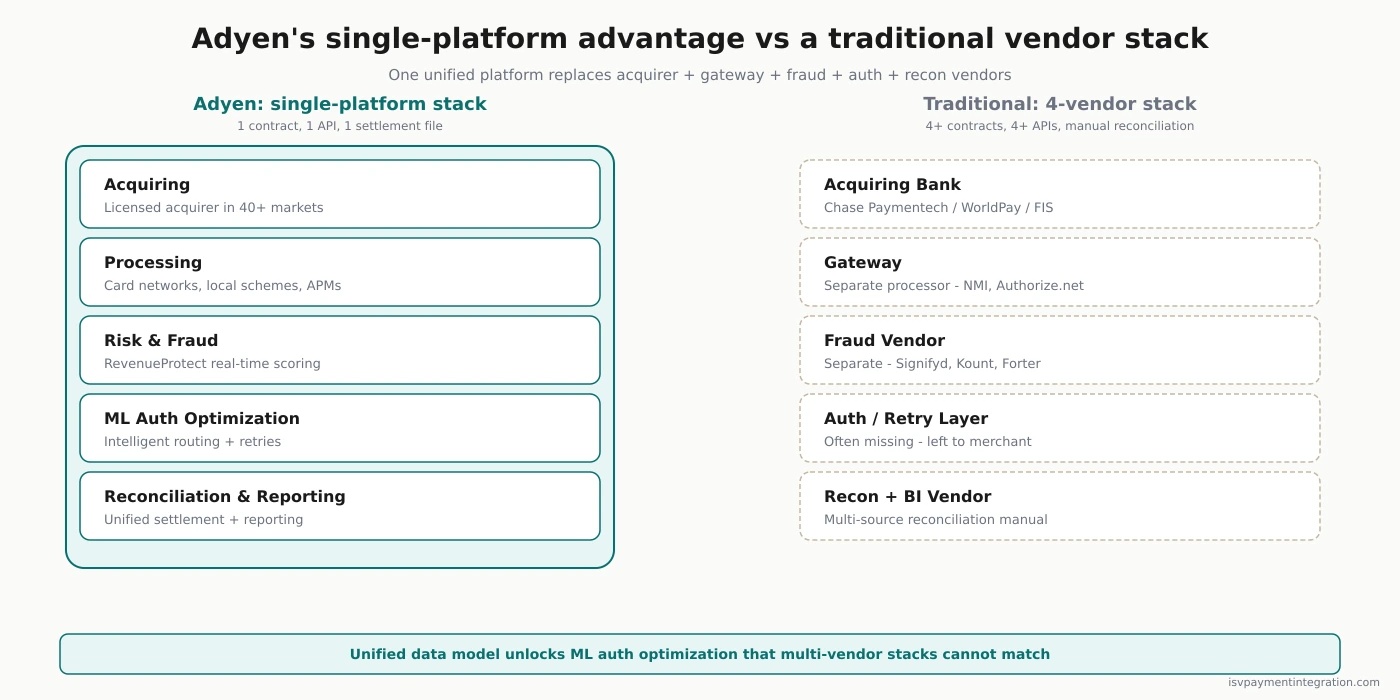

Adyen is a full-stack payments platform (gateway, processor, and acquiring bank in one) serving mid-market, enterprise, and ISV platforms from a single dashboard. The public 1.3 Trustpilot rating sits in stark contrast to the 3.6–4.6 B2B scores on G2, Capterra, and TrustRadius — a consumer-review artifact, not a signal about the product ISVs actually buy. The real story for software companies is Adyen for Platforms and its Capital, Issuing, and Accounts add-ons.

For the latest on Adyen's ISV capabilities, documentation, and partner programs, visit adyen.com.

Pricing

Interchange-plus

Visa and Mastercard render as $0.13 + Interchange+ + 0.60% (Adyen's own Interchange++ pricing model). Amex North America is 3.3% + $0.10 + $0.13 per transaction (Amex global is 3.95% + $0.13). ACH is $0.13 + $0.27, UnionPay is 3% + $0.13, Affirm/Klarna/Clearpay is 4.19% + $0.30 + $0.13. No setup, monthly, or closure fees, but Adyen labels these published fees 'indicative' and enterprise clients report an industry-dependent minimum invoice that Adyen does not publish.

Full pricing breakdown →Pros

- ✓ Single payments platform covering gateway, processing, and acquiring across online, in-store, and recurring payments

- ✓ Global payment acceptance with local payment methods in 33+ countries for international customers

- ✓ Adyen for Platforms with Capital, Issuing, and Accounts: a complete embedded-finance stack for ISVs

- ✓ Publicly traded, PCI DSS Level 1, with named enterprise clients like eBay, Microsoft, Uber, and Spotify

- ✓ Integrated risk management and fraud prevention analyzing payment data in real time

Cons

- ✗ Minimum invoice by industry and business model, not published publicly: the real SMB barrier

- ✗ Customer support runs through email ticketing with documented responsiveness complaints

- ✗ Onboarding and technical requirements are heavy for small businesses and startups

- ✗ Dashboard is powerful but has a learning curve, less intuitive than Stripe

- ✗ Not a fit for high-risk business types or support-dependent merchants

ISV Fit

Strong for enterprise and mid-market ISVs processing $50M+ annually that need unified omnichannel payments, global reach, and an embedded-finance stack via Adyen for Platforms. Weaker fit for early-stage software companies, SMB-heavy sub-merchant portfolios, or ISVs in high-risk verticals where onboarding friction and minimum-invoice ambiguity kill the commercial fit.

Alternatives

Adyen Review 2026: An ISV’s Perspective

Most Adyen reviews lead with one number: 1.3 stars on Trustpilot, from 423 angry customer reviews. For ISVs evaluating Adyen as a payments partner, that number is misleading, and correcting it is the most important thing this adyen review can do. On every B2B software site, Adyen rates 3.6 to 4.6 stars. G2 gives it 3.6, Capterra hits 4.6 across 30 reviews with 93% positive feedback, TrustRadius scores 8.2/10, and Merchant Maverick lands at 4.1 editorial.

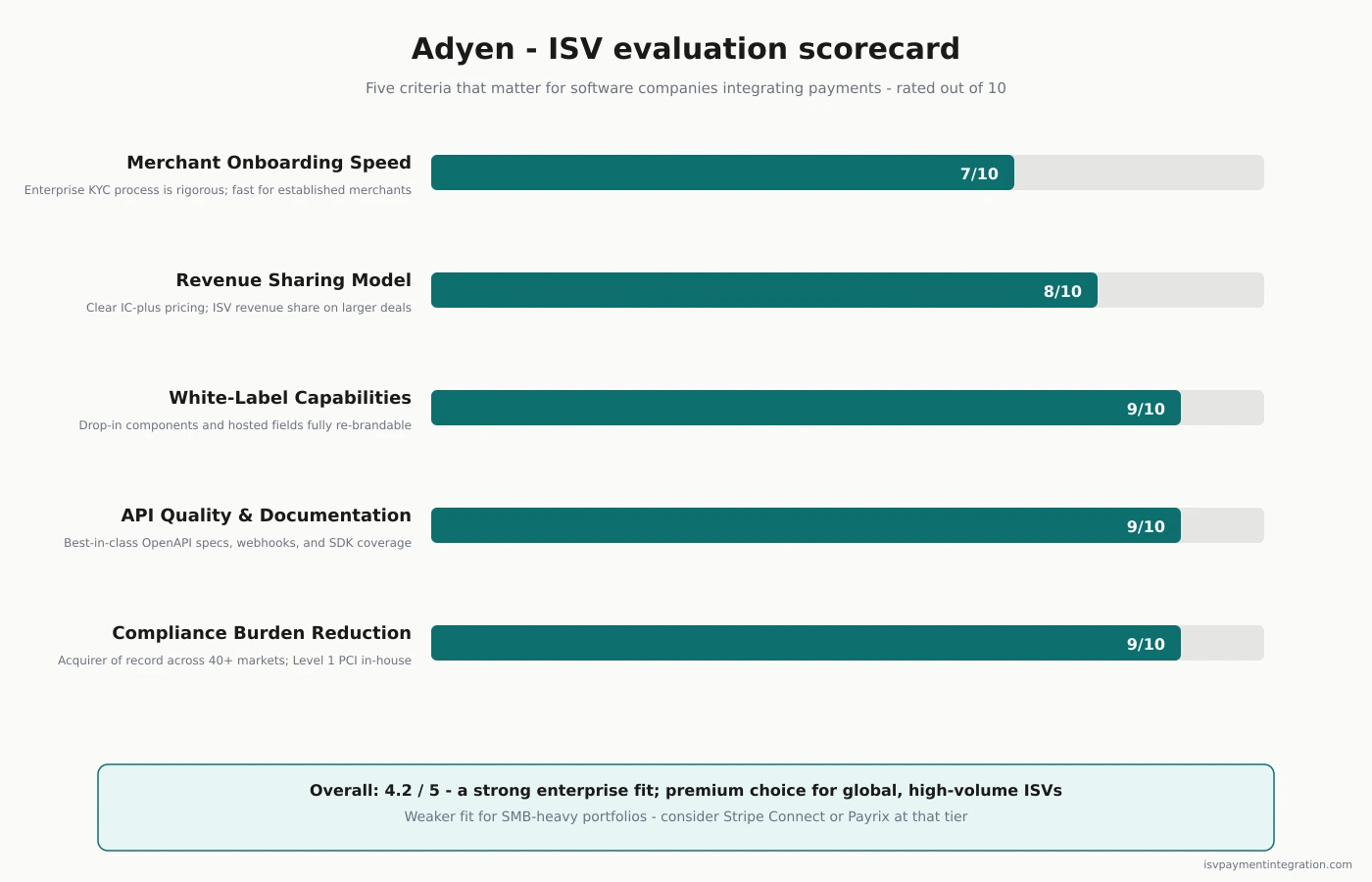

The consumers writing 1-star Trustpilot reviews are almost never Adyen’s customers. They’re shoppers and end customers on Vinted, Depop, and similar marketplaces where Adyen is the invisible payments platform that processes their card payments. These customers are angry at the marketplace fund hold or a refund that hasn’t hit their account, and Adyen catches the blame. This adyen review is written for the audience Adyen actually sells to: mid-market and enterprise businesses, and software platforms embedding payments for their own customers. Adyen scores 4.2/5 in our ISV-focused evaluation, tracking the B2B average across the sites where business buyers leave reviews.

Adyen at a glance

Adyen is a full-stack fintech company combining payment gateway, payments processor, and acquiring bank into one payments platform. Founded in Amsterdam in 2006, the company IPO’d on Euronext Amsterdam in 2018 (ADYEN) and primarily targets mid-market and enterprise businesses. The 4,000+ employees operate from offices across Europe, North America, Asia-Pacific, and Latin America. Named clients include eBay, Microsoft, Uber, Spotify, Lightspeed, and Toast.

For ISVs and platforms, Adyen’s product line extends past basic payment processing. The Adyen for Platforms suite adds Capital (embedded lending), Issuing (card issuing), and Accounts (embedded banking). This is the ISV-relevant stack, and it’s why Adyen keeps appearing alongside Stripe in enterprise RFPs. The platform processes card payments, online payments, bank transfers, e-wallets like Apple Pay, and BNPL payments in multiple currencies across 200+ local payment methods, giving businesses and their customers a wide set of payment options for any purchase anywhere in the world. Adyen’s payment processing stack is designed to accept payments on behalf of businesses of all sizes, with customers paying in their preferred local currencies.

Why Trustpilot looks catastrophic (and doesn’t matter for ISVs)

Here is the actual rating split for Adyen as of April 2026.

| Platform | Rating | Reviews | Audience |

|---|---|---|---|

| Trustpilot | 1.3 stars | 423 | Consumers on marketplaces |

| G2 | 3.6 stars | 17 | B2B software buyers |

| Capterra | 4.6 stars | 30 | SMB and mid-market |

| TrustRadius | 8.2 / 10 | 7 | Enterprise buyers |

| Merchant Maverick | 4.1 / 5 | Editorial | Processor analyst |

The 1.3 average across 423 Trustpilot reviews is not Adyen’s B2B customer base. Read the reviews: consumers whose Vinted or Depop payouts were held, whose identity verifications failed on a purchase, or whose fundraising account hit open-banking checks. Adyen is the technical rail underneath those marketplaces, and consumers blame the last name on the settlement notice. B2B buyers, the businesses actually running their operations on Adyen’s platform, rate it 3.6 to 4.6, competitive with Stripe and ahead of most legacy processors. If a blog cites only the Trustpilot number, they’ve made a category error.

Is Adyen trustworthy?

Yes, by every verifiable measure. Adyen is publicly traded on Euronext Amsterdam, holds acquiring licenses in the United States, Europe, the UK, Australia, and Singapore, and is certified to PCI DSS Level 1. The company operates under a Dutch banking license as a direct acquirer, which shortens the settlement chain and gives Adyen direct relationships with Visa, Mastercard, and local networks rather than passing through an intermediate processor.

The enterprise client list reinforces the trust case. eBay and Microsoft appear in Merchant Maverick’s analysis. Uber, Spotify, Lightspeed, and Toast have publicly confirmed Adyen as their payments platform. Public company, licensed bank, PCI Level 1, and named enterprise clients — the trust signals are stronger than most competitors can show.

Why is Adyen falling?

The question usually refers to Adyen’s 2023-2024 stock trajectory. The company’s share price declined sharply in mid-2023 after the company reported slower growth and higher hiring costs, and the narrative of Adyen being “in trouble” persisted in financial media. For ISV buyers, stock price is not the right signal. What matters is whether the company is still executing on the product.

On that front, Adyen continues to win enterprise contracts, expanded its Platforms line with Capital, Issuing, and Accounts, and maintains high transaction authorization rates that B2B users consistently praise. Service complaints cluster around small-merchant onboarding friction and email-only service responsiveness, not systemic product or payments failure. The service gaps are real but localized: enterprise customers on a named service manager rarely cite them, while self-serve customers do. Adyen is a mature payments service whose growth rate has normalized, which is different from a failing platform. The distinction matters when you’re underwriting a multi-year commercial relationship with a payments service provider.

Does Adyen work in the USA?

Yes. Adyen has held a US acquiring license since 2012, runs a New York City office, and supports all major US payment options: card networks, ACH Direct Debit, Apple Pay, Google Pay, bank transfers, and BNPL including Affirm, Klarna, and Clearpay. US pricing uses interchange-plus with a $0.13 processing fee and 0.60% on Visa and Mastercard, Amex North America at 3.3% + $0.10 + $0.13 per transaction (not the 3.95% global rate), ACH at $0.13 + $0.27, and UnionPay at 3% + $0.13.

For in-store merchants, Adyen sells its own payment terminals with unified reporting across channels. The same single dashboard covers card payments in a person’s hand and recurring payments in a subscription merchant account, so businesses don’t have to reconcile separate reports to see their real payment data. US enterprise clients like Toast and Lightspeed use this architecture to merge in store and online commerce behind one processor. For ISVs, the direct network relationships mean better authorization rates, cleaner chargeback and refund handling, and fewer fees hidden inside a downstream processor’s margin.

Does Adyen charge a fee?

Yes, and the pricing model is structured rather than flat. Adyen uses interchange++ to process Visa and Mastercard payments: you pay the interchange cost set by the card network, plus Adyen’s $0.13 per transaction processing fee and a 0.60% markup. Adyen’s own pricing page calls these published figures indicative — the FAQ frames them as a starting point “to discuss pricing options,” not a committed rate. Amex North America runs 3.3% + $0.10 + $0.13 per transaction, UnionPay is 3% + $0.13, and Paysafecard varies by industry at 10-12%. ACH transfers process at $0.13 + $0.27, and Adyen processes BNPL payments via Affirm, Klarna, and Clearpay at 4.19% + $0.30 + $0.13. The per-transaction processing fee is the same across most payment methods, which is why Adyen’s total pricing feels predictable for high-volume businesses and their customers.

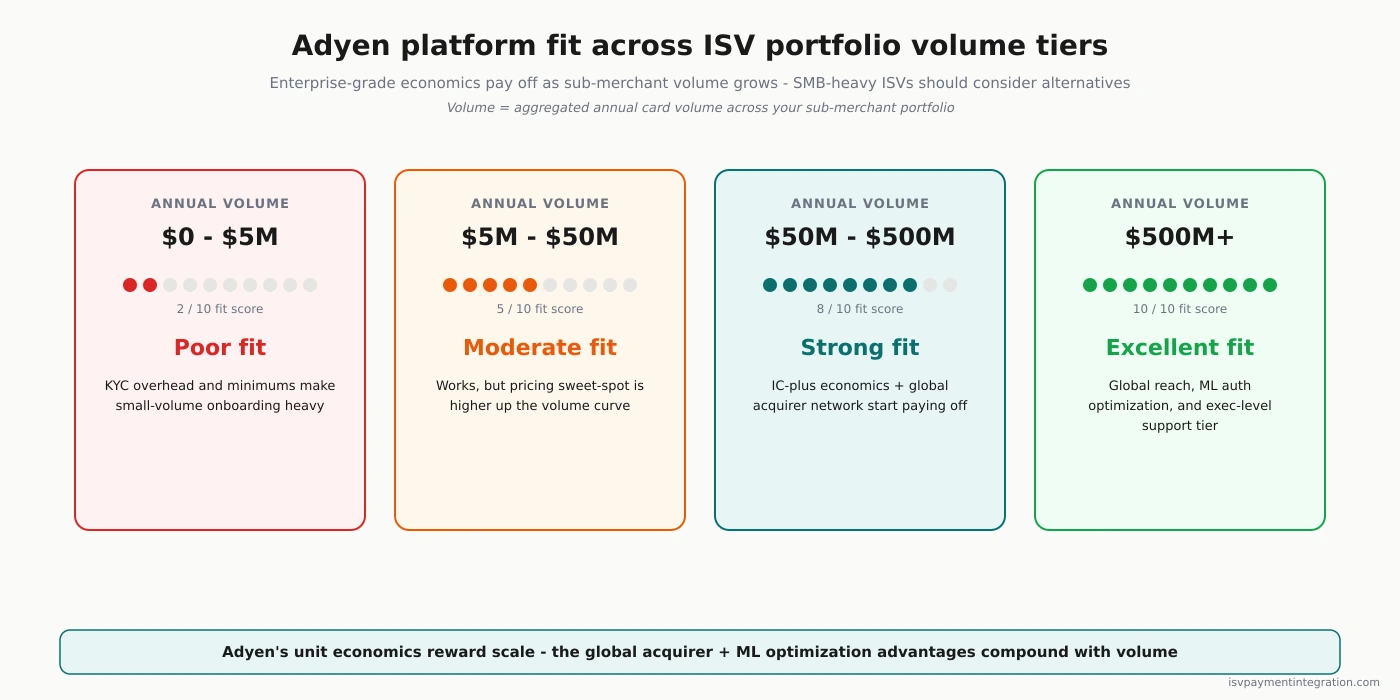

What Adyen does not charge: no setup fees, no monthly account fees, and no account closure fees. That’s explicit on Adyen’s pricing page and unusually clean for an enterprise processor. What Adyen does charge that is less visible: a minimum invoice based on industry and business model. The number is not published, and enterprise customers report it lands at a level that rules out small businesses and low-volume merchants. This is the real SMB barrier, not the per-transaction rate or the card network fees. If your annual processing is under roughly $1 million, expect the minimum invoice to come up in sales conversations as the gating commercial term. Larger businesses with predictable processing volumes absorb these fees comfortably; smaller businesses rarely do. For a full fee breakdown, see the Adyen pricing page.

Adyen for Platforms: the real ISV product line

Adyen for Platforms is the suite built for marketplaces, SaaS, and vertical software companies that embed payments into their own product. The core offering handles sub-merchant onboarding across 33+ countries and 23 languages, built-in KYC/AML and MATCH list checks, real-time identity verification, and flexible on-demand or scheduled payouts to sub-merchant bank accounts. Adyen frames this as “make money on every transaction” — revenue share for the ISV is a first-class feature, and sub-merchants can start to process customer payments quickly once the account is approved.

Three add-on tiers complete the embedded-finance stack. Capital is embedded lending for sub-merchants, with repayment pulled from future transaction volume. Issuing provides card issuing for sub-merchants, physical or virtual, table stakes for expense and spend SaaS. Accounts is embedded banking: sub-merchants can hold funds, receive payouts, and move money without needing an external merchant account. These financial products compete directly with Stripe Treasury, Capital, and Issuing.

Integration can be hosted or fully customized via the API, and the payment experience can be white-labeled so the processor brand never appears to the end user. For ISVs building vertical SaaS in retail, hospitality, or marketplaces, the Platforms stack is a complete offering from one vendor, not three. The trade-off: a higher onboarding bar than Stripe Connect, a sales engagement, and a minimum-volume conversation on the way in.

Strengths for ISVs

Global payment acceptance. Adyen supports 200+ payment methods including local payment methods specific to each region: iDEAL in the Netherlands, SEPA across Europe, Konbini in Japan, Pix in Brazil, alongside Apple Pay, Google Pay, and multi-currency card payments across multiple currencies. For ISVs with international customers, one integration covers regions that would otherwise need multiple gateway relationships and multiple merchant account setups. This is what global payment acceptance and genuine global reach look like in practice, with customers paying in their own currencies rather than being forced to convert.

Risk management and fraud prevention. Adyen integrates risk management features into its payments platform. The fraud prevention tools analyze payment data to detect potentially fraudulent transactions and distinguish fraud from legitimate customer activity without adding friction. G2 and Capterra reviewers cite the fraud detection and high authorization rates as reasons to choose Adyen over alternatives, and the positive feedback on fraud scoring is one of the clearest signals of product maturity across the review corpus.

Single dashboard, commerce integrations, and revenue share. One dashboard unifies online, in-store, and recurring payments. For ISVs building omnichannel platforms (POS software, retail-plus-ecommerce, subscription commerce), the single dashboard eliminates the pain of merging reports from separate processors. Adyen is also a certified Salesforce Commerce Cloud payment provider and integrates natively with SAP Commerce, Magento, BigCommerce, and Shopify Plus. Revenue share mechanics on Adyen for Platforms let ISVs earn transaction revenue on every payment flowing through their sub-merchants, turning payments from a cost line into a margin line for the software business.

Weaknesses for ISVs

Onboarding friction for small businesses. Adyen’s onboarding and technical requirements can be a barrier for smaller businesses and startups. This is the most common criticism across B2B review platforms, and it’s real. If your platform’s sub-merchants skew SMB or your ISV is early stage, the onboarding process will feel heavy, and the required document set and compliance process runs longer than self-serve competitors ask for. Smaller businesses that need to process customer payments within days, not weeks, will find the onboarding pace frustrating. Adyen’s underwriting team will still process the application, but expect more back-and-forth than with a self-serve gateway.

Customer support and service. Adyen’s customer support primarily operates through an email ticketing system. Users report a lack of responsiveness from the support team, and some say support issues weren’t addressed in a timely manner. Enterprise accounts get a dedicated account manager and named service contacts; platform-tier and smaller clients feel the email-only support access as a real constraint on service quality, especially when a fund hold or account verification needs fast human attention from the support team. Service and support response times are the most vocal complaints in negative customer reviews.

Dashboard learning curve and fit limits. G2 reviewers note the dashboard is powerful but not always intuitive. Expect a learning curve compared to Stripe. Merchant Maverick’s review also explicitly calls out that Adyen is not built for high-risk business types. CBD, firearms, adult, and other high-risk verticals will likely see the relationship declined at underwriting.

Enterprise vs SMB: where Adyen fits

The clearest mental model for Adyen is processing volume and complexity, not vertical. High-volume merchants with global footprints and multi-channel commerce win with Adyen. Low-volume SMBs with simple card-present payments or single-channel online payments are better served by Stripe, Square, or a regional payments service provider with lighter onboarding.

For ISVs, the translation is straightforward. If your sub-merchant base is mid-market to enterprise, with annual processing above $1M and real international exposure, Adyen for Platforms is competitive with Stripe Connect and often wins on acquiring economics, local payment methods, and predictable processing fees. If your sub-merchants are SMB, early-stage, or domestic-only, the onboarding friction and minimum invoice outweigh the platform benefits, and a lighter-weight processor becomes the right fit.

Adyen alternatives for ISVs

Stripe Connect is the default for platforms wanting the broadest geography, best developer tooling, and fastest self-serve onboarding. It wins when developer experience and time-to-live matter more than acquiring economics at scale. See Stripe vs Adyen.

Checkout.com is a direct enterprise competitor with global acquiring and a platform product. Smaller footprint, often more responsive on commercial terms. See Adyen vs Checkout.com.

Finix is a platform-first processor positioned explicitly against Adyen’s enterprise-first stance. Better for ISVs that want the full PayFac economics without a minimum invoice. See Adyen vs Finix.

Braintree is PayPal-owned with strong developer tooling and a mature platform product for payments. Fits platforms that want PayPal as a native payment option alongside card payments.

Final verdict: who should use Adyen

Best fit

- Enterprise and upper mid-market ISVs processing $50M+ annually

- Businesses with international customers needing local payment methods

- Omnichannel merchants unifying online payments, in store, and recurring payments on one platform

- Marketplaces and SaaS platforms that need Capital, Issuing, and Accounts

- Clients on Salesforce Commerce Cloud or an enterprise commerce stack

Not a fit

- Early-stage ISVs or SMB-heavy sub-merchant portfolios

- Support-dependent merchants who need phone support on their account issues

- High-risk business types

- Developers prioritizing self-serve speed over commercial economics

For ISV fit against comparable processors, the Payrix review covers the PFaaS-pioneer alternative.

Frequently asked questions

Is Adyen trustworthy? Yes. Adyen is publicly traded on Euronext Amsterdam, holds a Dutch banking license, is certified to PCI DSS Level 1, and counts eBay, Microsoft, Uber, Spotify, Lightspeed, and Toast among its clients. The low Trustpilot rating is consumer-review spillover from marketplaces that use Adyen as an invisible processor, not a signal about the B2B product.

Why is Adyen falling? Adyen’s share price dropped in mid-2023 after the company reported slower growth and higher hiring costs, and the narrative persisted in financial media. Stock price is not a useful signal for ISVs evaluating the platform. The product continues to win enterprise contracts and expand the Platforms suite, and B2B review sites rate Adyen between 3.6 and 4.6 stars.

Does Adyen work in the USA? Yes. Adyen has held a US acquiring license since 2012, runs a New York office, and supports all major US payment methods including card payments, ACH, Apple Pay, Google Pay, bank transfers, and BNPL. US pricing uses interchange-plus with a $0.13 processing fee, Amex North America at 3.3% + $0.10 + $0.13, and ACH at $0.13 + $0.27.

Does Adyen charge a fee? Yes, on an interchange++ model. Visa and Mastercard are interchange + $0.13 + 0.60%, Amex North America is 3.3% + $0.10 + $0.13, ACH is $0.13 + $0.27. Adyen does not charge setup, monthly, or closure fees, but enterprise clients report an industry-dependent minimum invoice that Adyen does not publish publicly.

The bottom line for ISVs

Adyen is a legitimate enterprise payments platform with a genuine ISV product line. The 1.3-star Trustpilot rating should not enter your evaluation. The real decision is whether your sub-merchant volume, international footprint, and omnichannel needs justify the commercial engagement and onboarding friction. For mid-market to enterprise ISVs processing $50M+ with global customers, Adyen for Platforms plus Capital, Issuing, and Accounts is one of the two or three best embedded-finance stacks on the market. If you’re earlier stage or SMB-heavy, Stripe Connect or Finix will serve you better. For fee depth, see the Adyen pricing breakdown; for head-to-head, Stripe vs Adyen is the right next read.