Braintree Review

PayPal's developer-facing payment gateway — strong Venmo and wallet coverage for US-first businesses, but the Marketplace product is narrow and the independent roadmap faded after the 2013 acquisition.

Overview

Braintree (the payment gateway) is PayPal's developer-facing processing arm. PayPal acquired the company in 2013 for $800 million, and the product now sits inside the paypal.com domain rather than on its old independent website. For businesses that need native PayPal, Venmo, Apple Pay, and Google Pay acceptance in a single integration, this service remains one of the cleanest options. For platforms that need a true multi-party marketplace layer — the ISV case Stripe Connect owns — the fit is thinner than the marketing implies.

For the latest on Braintree's ISV capabilities, documentation, and partner programs, visit braintreepayments.com.

Pricing

Flat-rate with interchange-plus option for higher volume

Braintree Direct US eCommerce rate is 2.89% + $0.29 per transaction — confirmed by Merchant Maverick's 2025-07-08 pricing review. Venmo sits at 3.49% + $0.49. ACH Direct Debit runs 0.75% capped at $5. Non-US cards and non-USD currency add 1% each. Chargebacks cost $15. No monthly, setup, or early-termination fees on the standard plan. High-volume accounts (above roughly $80,000/month) can negotiate a flat custom rate or interchange-plus. The 2.59% + $0.49 figure floating around the web refers to PayPal Commerce Platform — a sibling product, not Braintree Direct.

Full pricing breakdown →Pros

- ✓ Native PayPal and Venmo acceptance built into one SDK — no second integration, no second contract

- ✓ Mature developer platform: JavaScript v3, Android v5, iOS v7 SDKs, Drop-in UI, Hosted Fields for PCI scope reduction

- ✓ Predictable US flat-rate pricing at 2.89% + $0.29, no monthly fee, no early termination fee

- ✓ Dedicated business accounts rather than aggregated — lower freeze risk than a classic aggregator

- ✓ 130+ settlement currencies and 45+ merchant countries for global-leaning businesses

Cons

- ✗ Braintree Marketplace is US-only, does not support PayPal, and does not support recurring billing — a hard disqualifier for most platform use cases

- ✗ Trustpilot rating sits at 1.5 out of 5 across 281 reviews, with recurring complaints about fund holds and unresponsive customer service

- ✗ Post-acquisition, braintreepayments.com redirects to paypal.com/us/braintree — brand signal and roadmap independence have faded

- ✗ 3-D Secure support is not extended to every account; lower-volume businesses report being gated out of it

- ✗ Standalone gateway pricing ($49/month plus $0.10 per transaction) is uncompetitive against Authorize.Net and NMI

ISV Fit

Good fit for US-first software companies where PayPal and Venmo acceptance drives checkout conversion — B2C eCommerce businesses, subscription SaaS companies, and creator platforms whose customers live inside the parent company ecosystem. Weak fit for global marketplaces, gig platforms that need multi-party payouts, or any ISV whose sub-merchants need recurring billing inside a marketplace structure — Adyen or Finix are the honest answers there.

Braintree Review 2026: An ISV’s Perspective

Most Braintree review articles evaluate the payment processor for a single business accepting payments on one website. This one does not. It evaluates Braintree Payments through the lens that matters for software companies: embedding payment services into an application, onboarding sub-merchant business accounts, and deciding whether the Venmo and PayPal lock-in offsets a thinner multi-party product than the competition. Getting this call right saves an ISV real time and money over a multi-year integration process.

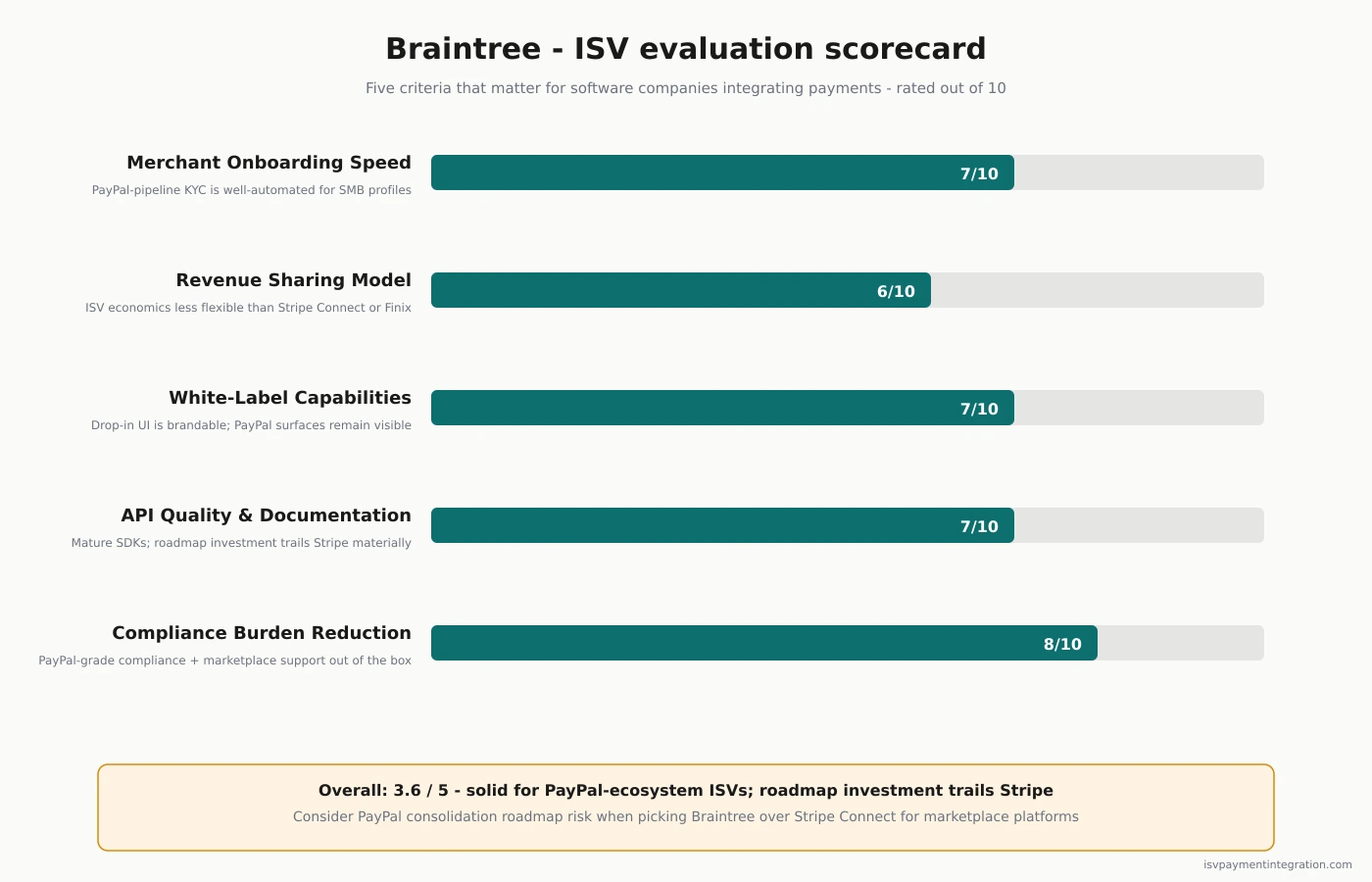

Braintree scores 3.6 out of 5 in our ISV-focused evaluation. That number blends three signals: the MM review’s 4.4 score, Capterra’s 3.8 ease-of-use rating, and Trustpilot’s 1.5 average across 281 customer reviews. The gap between those numbers is the story of this review.

Quick verdict

Braintree Payments is a solid option for US-first businesses whose customers want to pay with PayPal or Venmo at checkout, and whose accounts only need a standalone Direct product rather than Marketplace. It is a weak choice for global marketplaces, gig platforms, or any ISV whose economics depend on the Marketplace module to accept multi-party payments. The technology holds up; the post-acquisition roadmap and customer service reputation do not.

Is Braintree trustworthy?

Braintree Payments is a PCI DSS Level 1 certified payment processor owned by a publicly traded parent company. The platform processes over 6 billion online transactions and more than $50 billion in customer money each year. At the infrastructure layer it is trustworthy for any business: security protocols are current, certifications are real, and the tokenization vault has held up for more than a decade. The service holds certifications from all major card networks and has passed independent penetration testing, a baseline every business should find when evaluating a payment processor.

The customer experience layer is where reviews change sharply. Trustpilot shows Braintree at 1.5 out of 5 across 281 customer reviews as of April 2026. The pattern: funds on hold with slow resolution time, accounts closed without clear explanation, fraudulent transactions approved by the system that the business is later asked to absorb (rather than refund), and support cases where the response was generic or redirected to the parent company. One customer share summed it up: “Tech remains good, customer service is abysmal.”

For an ISV, Braintree is trustworthy at the infrastructure layer but operationally uneven at the support layer. Your sub-merchants will receive both halves, the strong security features and the weaker post-sale experience. Budget support time accordingly.

Is Braintree owned by Venmo?

No. Braintree (the payment gateway) is owned by PayPal, which acquired the business in September 2013 for $800 million. Venmo is a separate parent-owned service. When the acquisition closed, Venmo came along in the same deal as a Braintree subsidiary at the time. Today the two services are siblings, not parent and child. Both sit under the same parent company.

People ask this question because Venmo acceptance on most US websites is implemented through the Braintree SDK. If you have ever seen a “Pay with Venmo” button at checkout, that payment flow almost certainly runs on a Braintree Payments integration under the hood. The two services share engineering and the same processing stack, which is why the ownership question keeps surfacing in online reviews.

What does Braintree charge per transaction?

The US eCommerce rate is 2.89% + $0.29 per card transaction for Braintree Direct, confirmed by the MM July 2025 update. Every business on the standard plan pays the same rate with no monthly fee.

Rates worth knowing before you integrate:

- Venmo: 3.49% + $0.49 per transaction

- ACH Direct Debit: 0.75%, capped at $5 per transaction

- Non-US cards or non-USD settlement: +1% on each dimension

- Chargebacks: $15 per dispute

- American Express (bring-your-own): $0.15 on top of the Amex rate

- Standalone gateway: $49 per month plus $0.10 per transaction

- High-volume accounts (above roughly $80,000/month): negotiated flat rate or interchange-plus

- Monthly, setup, and early termination fees: $0 on the standard plan

A rate of 2.59% + $0.49 floats around SEO blog posts as if it were the standard. It is not. That figure is for Commerce Platform, a sibling product that shares infrastructure but has different pricing and onboarding. Braintree Direct is 2.89% + $0.29. Our Braintree pricing page has the full schedule. The foreign transaction fee compounds quickly on international business, and ACH services are notably less competitive than dedicated ACH providers.

Is Braintree good?

“Good for whom?” is the honest version of the question. The MM review rates Braintree Payments 4.4 out of 5, with affordability, product depth, and contract terms all scoring high. Capterra rates ease-of-use at 3.8. Trustpilot rates customer service at 1.5 across 281 reviews. Averaging those numbers is meaningless. What matters is which dimension your business cares about most.

Braintree is a great fit for:

- US-first businesses whose checkout conversion depends on PayPal and Venmo payments

- B2C eCommerce companies that want one SDK covering card payments, digital wallets, and Apple Pay options

- Subscription SaaS companies that use the native recurring billing features to accept customer payments on schedule

- Development teams that value SDK maturity and the time saved on integration

Braintree is weaker for:

- Marketplaces or platforms that need a true multi-party payout product to accept and split payments

- Businesses needing global payment acceptance in jurisdictions the service does not offer

- Companies that expect enterprise customer support on a standard pricing plan

- High-risk verticals, where the underwriting process generally declines the business account

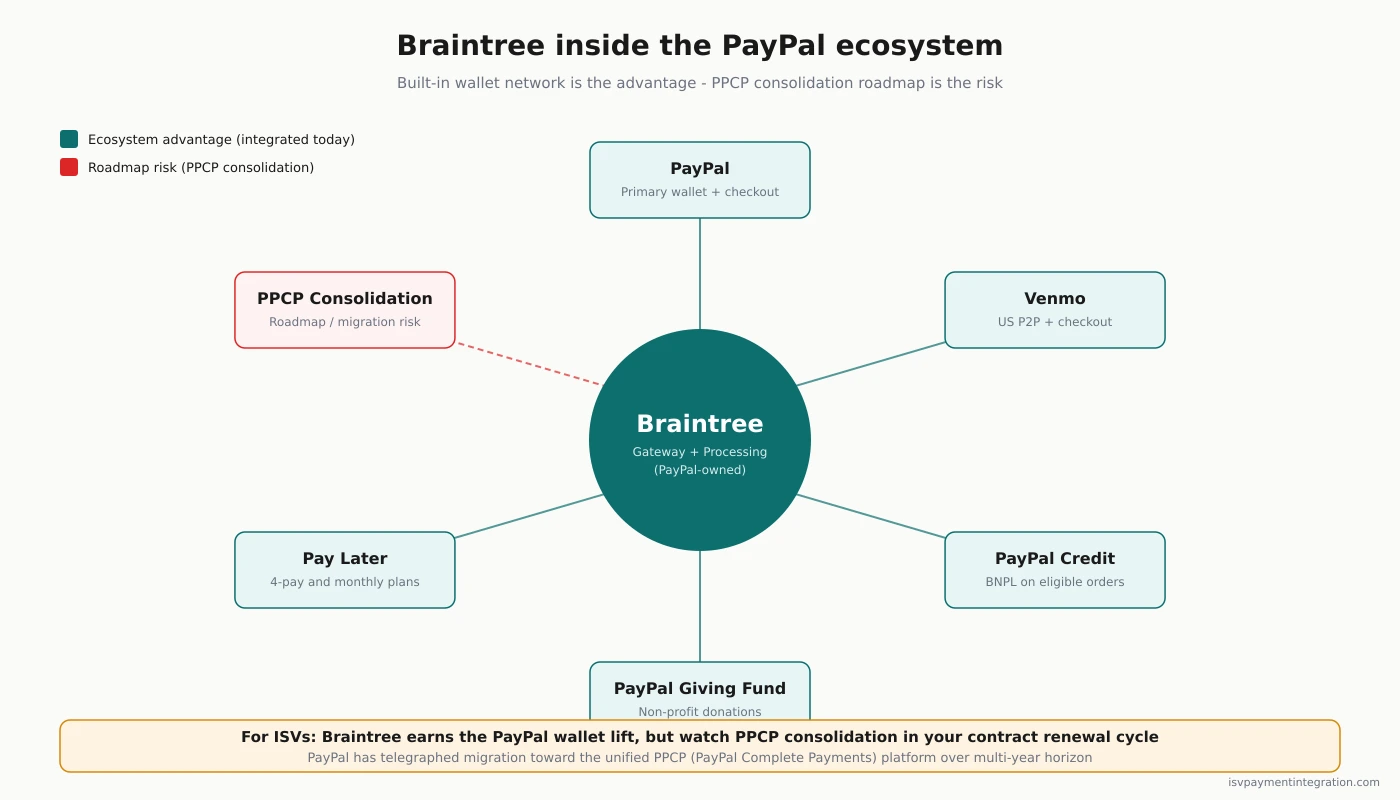

The PayPal ecosystem advantage

The strongest reason to pick this payment processor over a competing gateway is the PayPal wallet. Hundreds of millions of active accounts and a growing Venmo user base mean that offering both payment options at checkout measurably lifts conversion on US consumer websites. Hundreds of thousands of businesses process payments here for exactly this reason.

Both wallets come through the same integration. One SDK, one business account, one reconciliation file. Software companies integrating with this payment processor receive access to card payments, PayPal, Venmo, Apple Pay, Google Pay, ACH, and SEPA Direct Debit services from a single contract. If you have ever wired up a wallet checkout separately from your card processor, the time savings are real. Integration with Shopify and WooCommerce means a business can send customers through an existing checkout and receive payouts on a predictable schedule. Money moves on a consistent funding cycle, the reconciliation process is automatic, and funding arrives in the business account at the same time each week. Receiving payments from customers and sending money to sellers runs through one account.

The flip side is roadmap concentration. The braintreepayments.com website now 301-redirects to paypal.com/us/braintree. Independent marketing and the developer blog have quieted since the acquisition, and pricing increases that started on the parent side have bled into existing accounts. If your roadmap assumes this service remains a distinct product with its own team, that assumption is weaker in 2026 than in 2018. Build your integration to be portable.

The Marketplace gap: the real ISV dealbreaker

Braintree Marketplace is the answer to the multi-party payout category: a way for a platform to accept payments on behalf of many sub-merchant business accounts, split money between sellers, and send payouts to each seller’s account. On paper it looks competitive. In practice, the fine print removes most of the cases a modern platform needs.

Per the developer documentation, Marketplace has these constraints on the sub-merchant account setup process:

- US only. Sub-merchant accounts outside the United States cannot sign up. The competing Connect product offers coverage in 46+ countries.

- No PayPal or Venmo inside Marketplace. The wallet advantage that makes Direct attractive disappears. Sub-merchants can only accept card payments from customers.

- No recurring billing inside Marketplace. Subscription businesses hit a hard wall; recurring features only exist in Direct.

- Limited third-party shopping cart compatibility. Most eCommerce shopping cart options do not integrate out of the box.

- Sales-gated. Onboarding requires special approval; it is not self-serve. Expect a week or more of back-and-forth before sub-merchants go live.

Each constraint on its own is workable. Stacked together, they disqualify Marketplace for most platform use cases ISVs build: global marketplaces, creator platforms, subscription aggregators, vertical SaaS with in-app receiving payments flows. This is why our rating sits at 3.6 rather than higher.

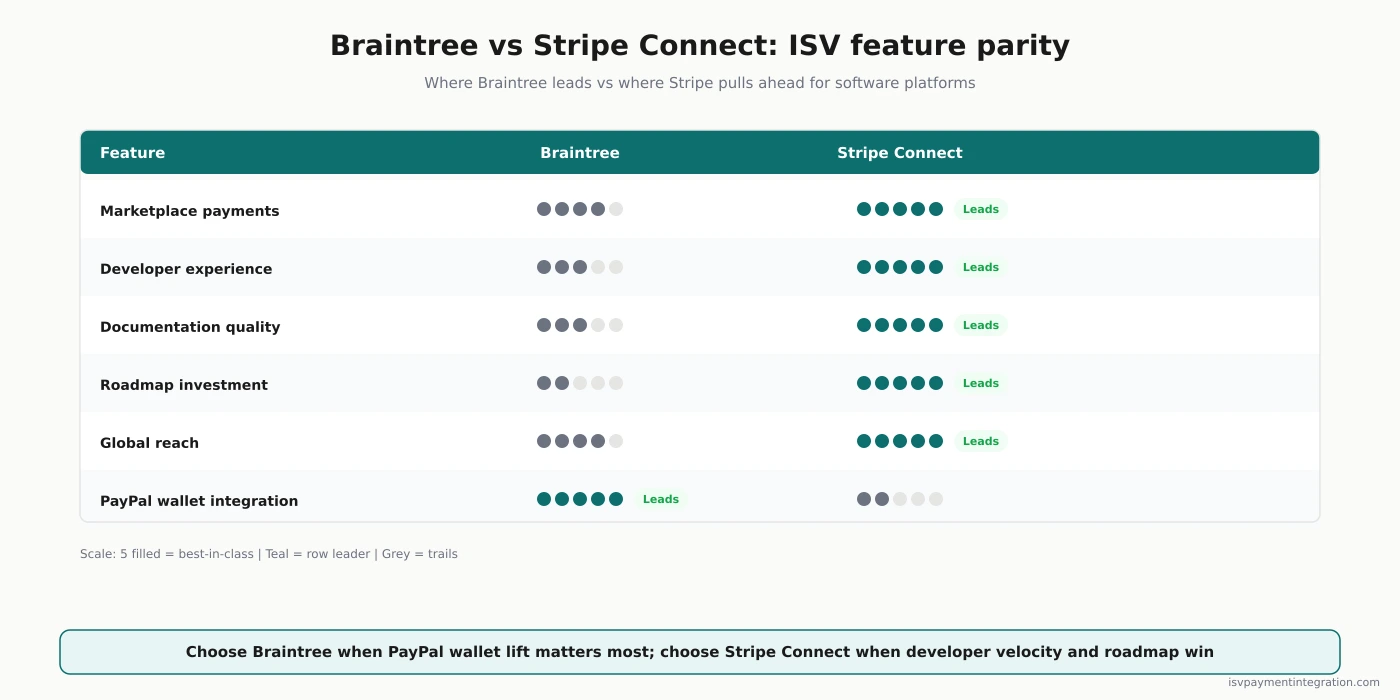

How Braintree compares to the competition for ISV platforms

On developer experience, the competing platform is widely considered the category benchmark in API design. Braintree’s SDKs are mature and stable, but developer features have not kept pace since 2020. On marketplace capability, the competing product wins decisively on more countries served, recurring billing inside the platform, and self-serve onboarding tiers for sub-merchant accounts. On wallet acceptance, Braintree wins on PayPal and Venmo payments from a single business account. Both companies offer similar flat-rate structures at the top tier and negotiate interchange-plus at higher volumes. On roadmap, the competitor ships new features monthly; Braintree has shipped less since 2013.

For a deeper side-by-side read our head-to-head comparison. Short version: if PayPal and Venmo payments move the conversion needle, Braintree earns a serious look. For a marketplace, the competing platform is safer. Many businesses offer both payment services during evaluation to see which converts better.

Customer service reality check

Customer service response time shows up in every negative review. The pattern: long wait times on tickets, generic replies, support redirecting the business to the parent company’s help center (which does not handle product-specific issues). Customers report tickets on hold more than a week before receiving a reply; many share screenshots of canned responses that never resolve the issue.

Enterprise support exists but is a separate commercial agreement with dedicated account management. If your platform volume is not yet at that level, your account sits in the standard queue alongside small businesses. Plan for it: keep a runbook, resolve what you can internally, share knowledge across the team, and send only what genuinely needs the vendor up the escalation path. The rest of the time your team resolves issues faster than the vendor process would.

Who Braintree fits

Braintree is a great fit for:

- US-first B2C eCommerce companies. PayPal and Venmo payments lift checkout conversion; the integration is the cleanest way to offer both options from one business account.

- Subscription SaaS companies with US customers. Native recurring billing inside Direct is solid, and the dedicated-account model reduces the sudden-freeze risk aggregator services carry.

- Mid-market digital businesses. The 2.89% + $0.29 rate is competitive, the no-ETF contract is clean, and the SDKs are battle-tested.

- Companies already integrated with the parent wallet. Migration is low-friction.

Who should look elsewhere

Braintree is the wrong choice for:

- Global marketplaces and gig platforms. The Marketplace gap (US-only, no PayPal, no recurring billing) is too wide. Adyen or Finix will serve your business better.

- High-risk verticals. Underwriting declines CBD, adult, firearms, and similar businesses. A high-risk specialist is the honest answer.

- Low-volume businesses that need 3-D Secure. Braintree holds back 3DS features on smaller accounts. If fraud tooling is critical at low volume, verify 3DS availability before committing.

- Teams that need white-glove customer service on standard pricing. Enterprise support is a separate agreement.

- Companies that cannot absorb post-acquisition drift. If your roadmap needs a partner with an independent team and an independent website, the braintreepayments.com-to-paypal.com redirect is a signal worth taking seriously.

The bottom line for ISVs

Braintree is a legitimate choice for a specific ISV profile: US-first, wallet-driven, standalone Direct product rather than Marketplace, comfortable with PayPal as the long-term brand holder. For that profile the technology is strong, the pricing is predictable, and the Venmo lock-in is a real conversion lever. Businesses that fit the profile find the combination of flat-rate pricing, dedicated accounts, and deep wallet features to be great value for the money, and time-to-integrate is among the lowest in the category.

For any other profile (global platform, multi-party marketplace, high-risk vertical, white-glove support), the honest move is to look at Adyen or Finix first. Payment processing services are built for specific shapes of business, and Braintree’s shape narrowed after 2013.

If you are comparing head-to-head against the competition, start with our Braintree comparison page and the Braintree pricing breakdown to find the numbers that matter.

Frequently asked questions

Is Braintree the same as PayPal? No. Braintree is a PayPal subsidiary. Direct is developer-focused card processing; Commerce Platform and Checkout are separate services with different pricing (2.59% + $0.49 for Commerce Platform vs 2.89% + $0.29 for Direct).

Does Braintree charge a monthly fee? Not on the standard plan. No monthly fee, no setup fee, no early termination fee. The gateway-only option costs $49 per month plus $0.10 per transaction, a separate product type.

Can I use Braintree outside the US? Yes, for accounts in Canada, Australia, the UK, most of Europe, Singapore, Hong Kong, Malaysia, and New Zealand, with settlement in 130+ currencies. Marketplace only supports US-based sub-merchant accounts.

Does Braintree support recurring billing? Yes in Direct. Native subscription features include trial periods, proration, and a configurable dunning process for failed payments. No inside Marketplace.