NMI vs Global Payments

A feature-by-feature comparison for ISVs integrating payments.

NMI is a processor-agnostic payment gateway that connects ISVs to 200+ processors through a single API, offering full white-label branding and transparent per-transaction pricing. Global Payments is a vertically integrated processor with deep expertise in healthcare, education, and restaurants, offering a single-vendor relationship from gateway to acquiring. Choose NMI if your ISV needs processor flexibility and brand control. Choose Global Payments if you operate in a specialized vertical and want one integrated partner.

Feature Comparison

| Feature | NMI | Global Payments |

|---|---|---|

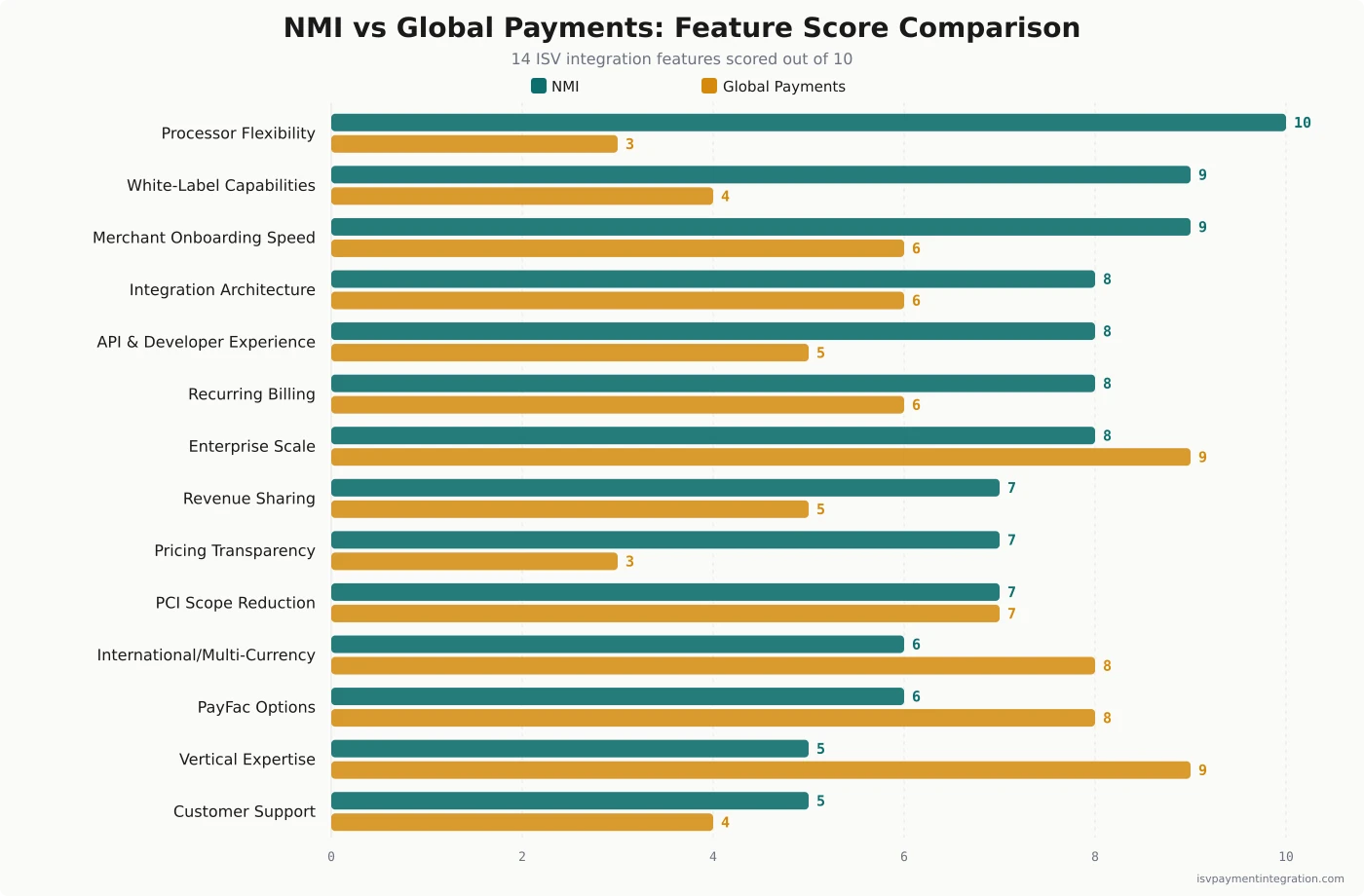

| Integration Architecture | 8 | 6 |

| API & Developer Experience | 8 | 5 |

| White-Label Capabilities | 9 | 4 |

| Processor Flexibility | 10 | 3 |

| Merchant Onboarding Speed | 9 | 6 |

| Revenue Sharing | 7 | 5 |

| Pricing Transparency | 7 | 3 |

| Vertical Expertise | 5 | 9 |

| PayFac Options | 6 | 8 |

| PCI Scope Reduction | 7 | 7 |

| Customer Support | 5 | 4 |

| Recurring Billing | 8 | 6 |

| International / Multi-Currency | 6 | 8 |

| Enterprise Scale | 8 | 9 |

Get this comparison as a shareable PDF

We'll send the NMI vs Global Payments breakdown to your inbox — ready to share with your team.

Best for

NMI

ISVs that need processor flexibility across 200+ processors, full white-label branding, fast automated merchant onboarding (91% same-day), and transparent per-transaction gateway pricing. Best for ISVs serving multiple verticals or wanting maximum control over their payment stack.

Best for

Global Payments

ISVs operating in healthcare, education, or restaurant verticals who want a single vendor relationship covering gateway, processing, and merchant services. Best for larger ISVs that can negotiate custom terms and want hybrid PayFac capabilities without full registration.

NMI and Global Payments take fundamentally different approaches to ISV payment integration. NMI is a processor-agnostic gateway operating system that connects to 200+ processors through a single API — your ISV picks the processor(s) that fit. Global Payments is a full-stack processor with its own acquiring network, offering embedded payments through what was formerly OpenEdge, now Global Payments Integrated. For deeper dives on each platform individually, see our NMI review and Global Payments review.

The right choice depends on how much control your ISV needs over the payment stack, which verticals you serve, and how you want to monetize payments.

The short version: Choose NMI if your ISV needs white-label flexibility and processor choice. Choose Global Payments if you want a single vertically-specialized partner handling everything from gateway to acquiring.

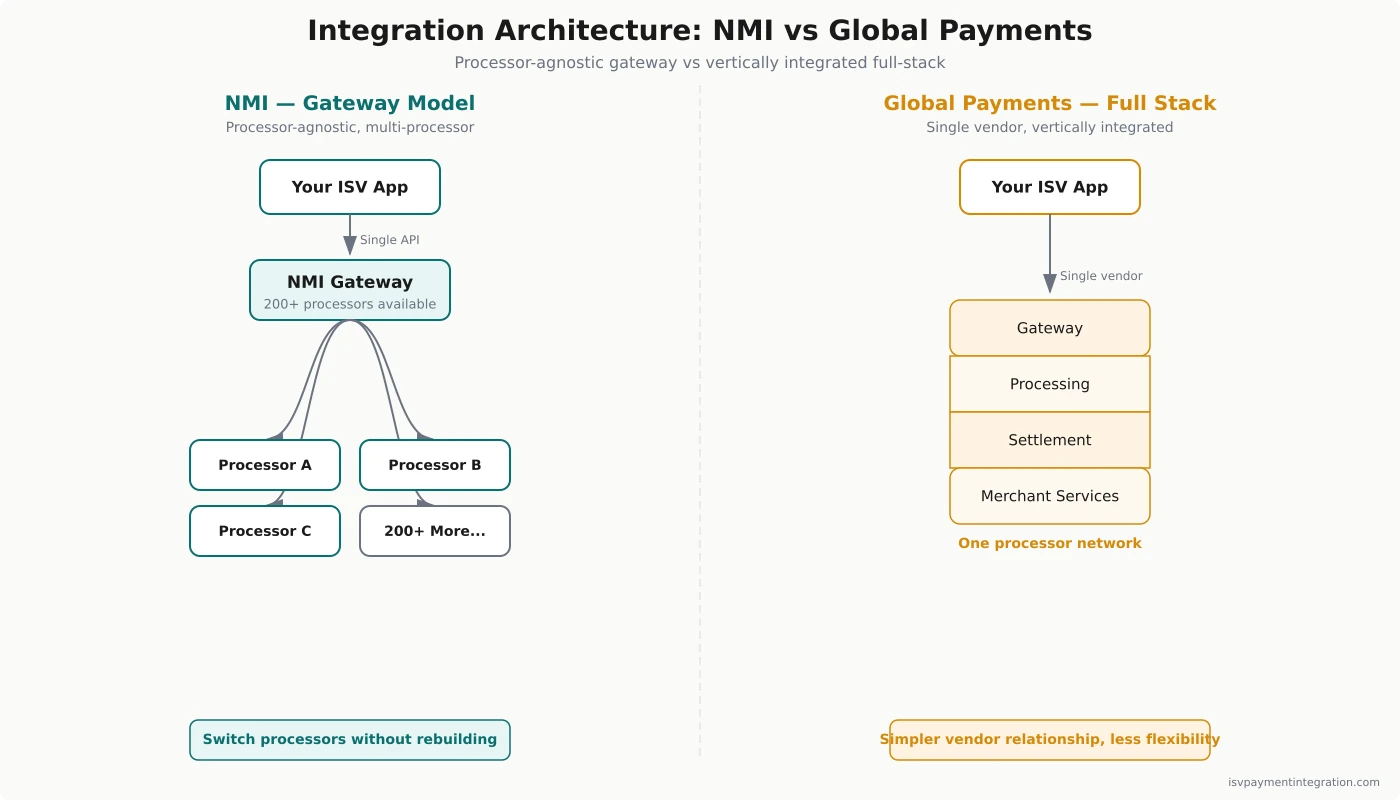

Integration Architecture: Two Fundamentally Different Models

This is the most important distinction for ISVs, and it affects every downstream decision.

NMI operates as a gateway operating system. It sits between your software and the processor, giving your ISV a single integration point that connects to 200+ payment processors. Your ISV — or your merchants — can choose which processor handles their transactions. If a processor raises rates or underperforms, you can switch without rebuilding your integration. NMI supports 125+ shopping cart integrations and 235,000+ payment devices through this single gateway layer.

Global Payments is a vertically integrated processor. When you integrate with Global Payments Integrated (formerly OpenEdge), you’re connecting to their proprietary acquiring network. They handle everything: gateway, processing, settlement, and merchant services. This simplifies the vendor relationship — one contract, one integration, one support line — but it means your ISV and all your merchants are locked to Global Payments’ network.

What this means for ISV decision-makers: If your software serves merchants across different industries or regions with varying processing needs, NMI’s multi-processor flexibility is a significant architectural advantage. If your ISV operates in a single vertical where Global Payments has deep expertise (healthcare, education, restaurants), the integrated stack may outweigh the flexibility trade-off.

Developer Experience & API Quality

ISV engineering teams will spend weeks or months on payment integration. The quality of documentation, SDKs, and sandbox environments directly impacts your integration timeline and ongoing maintenance burden.

NMI provides SDKs in PHP, C#, Java, and VB.NET, with a quick-start guide that promises “first integration in minutes.” Their documentation includes example requests and responses for every endpoint, webhooks for real-time transaction data, and a Query API for reporting. G2 reviewers rated NMI easier to use, set up, and administer than both Stripe Connect and Square Payments. The trade-off: compared to Stripe or Adyen, NMI offers “greater control but requires more involvement from the developer side.”

Global Payments Integrated offers an API library, a developer portal, and dedicated integration specialists who walk ISVs through setup. They also run an integration certification process — Global Payments certifies your ISV’s workflows and features for bug-free merchant onboarding. A 2025 third-party assessment noted that “Global Payments has the infrastructure, but not the nimble developer experience most ISVs want. Support is strong for enterprise customers, but embedded tools are lacking.”

Bottom line: NMI gives your developers more flexibility and self-service capabilities. Global Payments provides more hand-holding during setup but has a steeper ongoing developer experience curve.

Revenue Economics for ISVs

This is where the comparison matters most for ISV business models — and where most comparisons fall short.

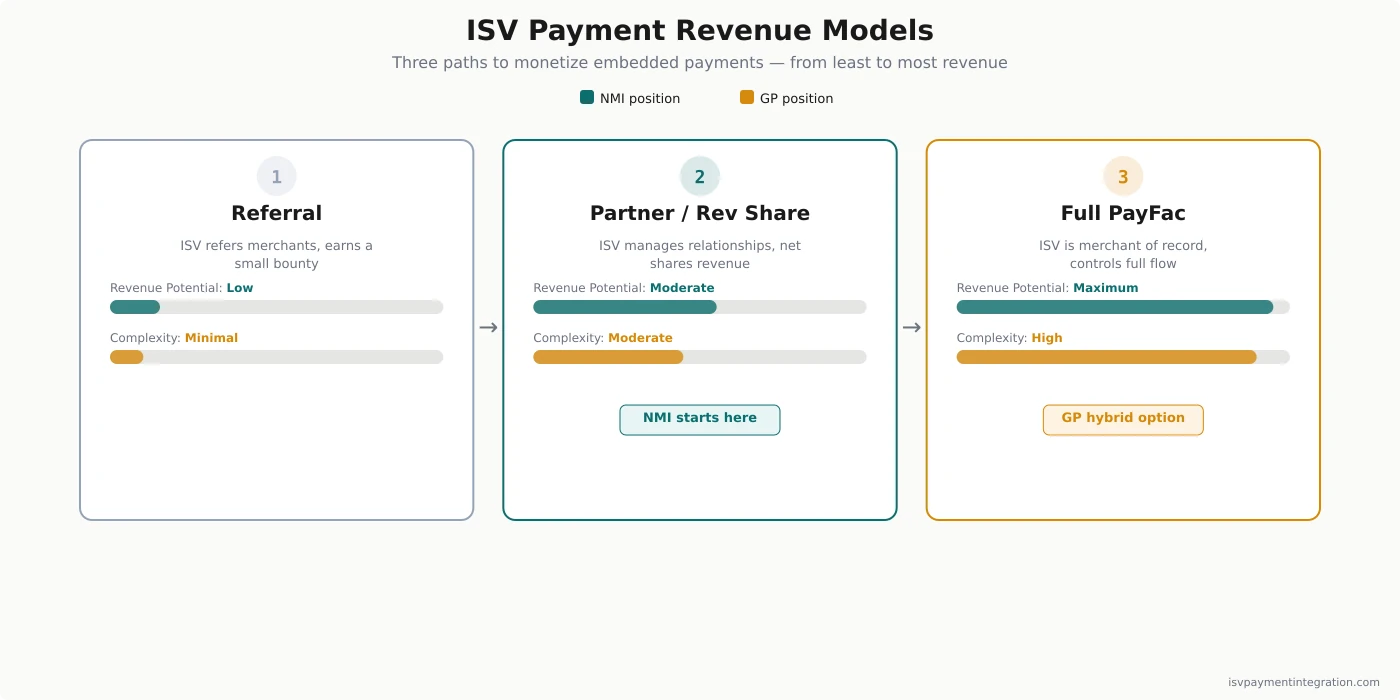

How ISVs Make Money from Embedded Payments

ISVs earn payment revenue through the spread between what merchants pay and what the processor charges. For a deeper breakdown of fee structures, see our NMI pricing analysis and Global Payments pricing analysis. The three models, from least to most revenue:

- Referral — ISV refers merchants, earns a small one-time or recurring bounty. Minimal revenue.

- Partner-enabled / Revenue share — ISV manages merchant relationships, shares net payment revenue with the processor. Moderate revenue.

- Payment Facilitator (PayFac) — ISV becomes the merchant of record, controls the full payment flow. Maximum revenue, maximum complexity and compliance burden. See our guide on PayFac-as-a-Service for a middle path.

NMI Revenue Sharing

NMI’s partner-enabled model sits between referral and full PayFac. Revenue sharing starts from the first transaction and grows with volume. ISVs can earn additional revenue through value-added extensions: fraud protection, secure card storage, Level 3 processing, and automatic card updating.

NMI’s gateway fee is a flat $0.02–$0.10 per transaction (varies by reseller), with acquirer fees separate and transparent. However, because NMI goes to market exclusively through reseller partners, your actual economics depend heavily on which NMI reseller you work with — some mark up significantly.

Important caveat: A 2025 independent comparison noted that NMI’s revenue share “is not structured for SaaS partners and is often not offered” — which contradicts NMI’s own marketing. ISVs should get revenue share terms in writing before committing.

Global Payments Revenue Sharing

Global Payments offers revenue sharing through their ISV partner program, and a McKinsey report confirmed they use revenue shares as “a key lever to scale distribution.” However, third-party assessments consistently note that revenue share is “not commonly offered to smaller software vendors.”

Pricing transparency is a documented concern. Multiple independent sources report that Global Payments’ initial rates — often quoted around interchange + 0.55% + $0.25 per transaction — can increase dramatically after the first year. One merchant documented their rates jumping to 1.5% + $1.00 per transaction plus additional network compliance fees ($139/month), CE Suite fees ($45/month), and analytics fees ($45/month). As of January 2026, Global Payments announced a 0.20% per-transaction increase across the board.

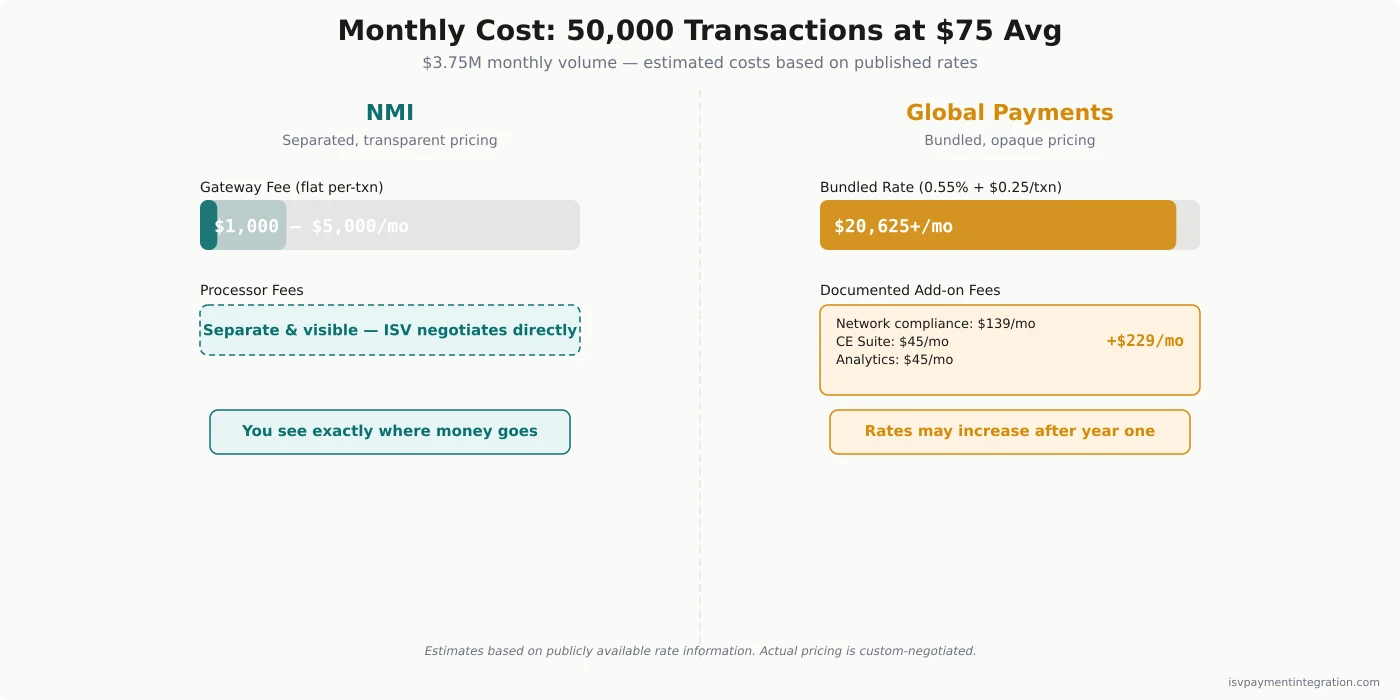

Revenue Example: 50,000 Transactions/Month

For an ISV processing 50,000 monthly transactions at $75 average ticket ($3.75M monthly volume):

- NMI estimated gateway cost: $1,000–$5,000/month (flat per-transaction) plus separate processor fees (transparent, ISV-negotiated)

- Global Payments estimated cost: ~$20,625+/month (bundled at initial rates of 0.55% + $0.25) plus documented add-on fees ($200+/month)

- Key difference: NMI separates gateway and processing costs so ISVs see exactly where money goes. Global Payments bundles everything, making it harder to identify margin opportunities.

Note: Actual pricing is custom-negotiated. These estimates are based on publicly available rate information and independent reviews. Request ISV-specific pricing from both platforms.

Not sure which pricing model works better for your ISV? Get a free assessment →

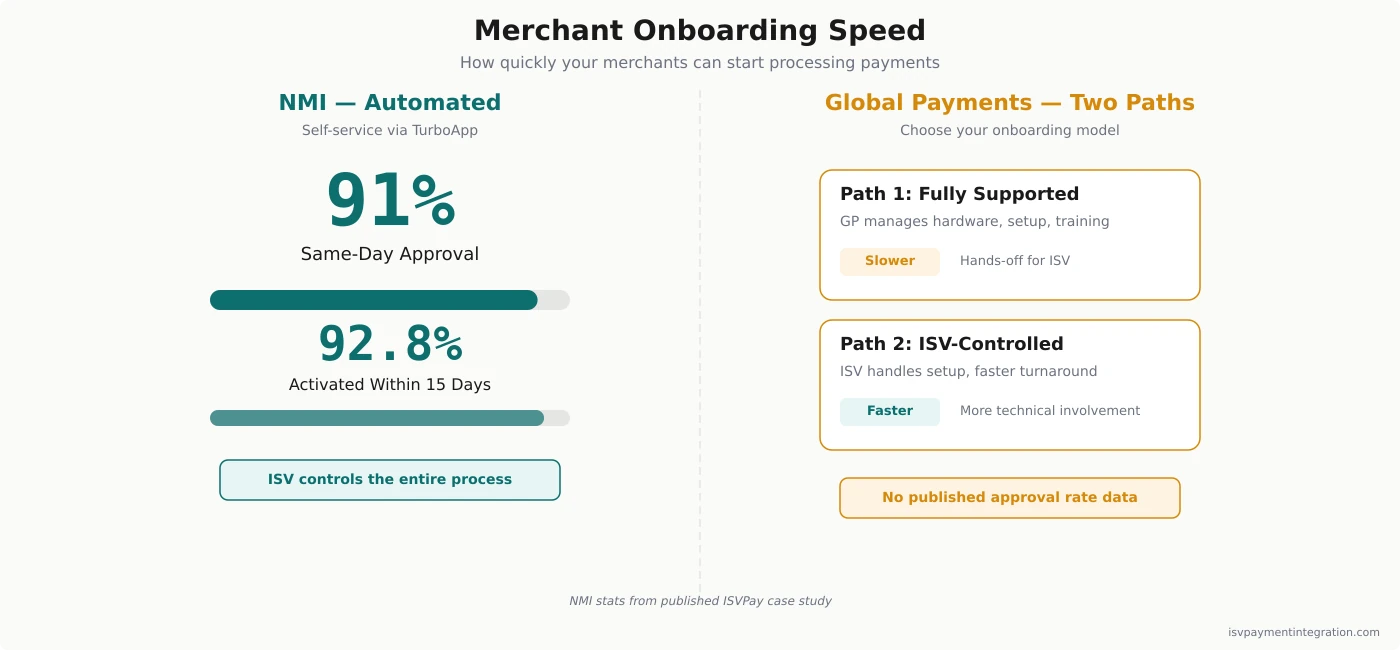

Merchant Onboarding & Sub-Merchant Management

How quickly your merchants can start processing payments directly affects your ISV’s growth rate and customer satisfaction.

NMI offers automated onboarding through its Merchant Relationship Management platform and TurboApp for underwriting. In a published case study, NMI partner ISVPay achieved a 91% same-day merchant approval rate in their highest-volume month, with 92.8% of merchants activated within 15 days. ISVs manage their merchant portfolio through NMI’s white-labeled portal.

Global Payments offers two distinct onboarding paths: (1) Fully Supported — Global Payments manages everything including hardware installation, merchant setup, and training (hands-off for the ISV but slower); (2) ISV-Controlled — faster turnarounds with less dependency on GP’s team, but requires more technical involvement from your side. Both paths include a dedicated integration specialist.

For ISVs prioritizing speed: NMI’s automated, self-service onboarding appears faster based on published data. For ISVs whose merchants need in-person hardware setup and training (retail, restaurants), Global Payments’ fully-supported path handles logistics your team may not want to manage.

White-Label & Brand Control

For ISVs building payment experiences inside their software, brand consistency matters. Your merchants should see your brand, not your processor’s.

NMI is built for white-label payment processing. Partners get branded domains, merchant-facing portals, and customized onboarding flows — all under the ISV’s brand. This is core to NMI’s go-to-market: because they sell exclusively through partners, white-labeling is a first-class feature, not an afterthought.

Global Payments offers a co-branded experience but with less depth. The merchant experience often includes Global Payments branding alongside the ISV’s, particularly in statements, reporting portals, and merchant-facing communications. For ISVs where brand control is a competitive differentiator, this can be a limitation.

Vertical Expertise & Market Fit

Global Payments has the edge here. Their Integrated division has deep, purpose-built solutions for healthcare, education, restaurants, and retail — including industry-specific compliance features, reporting, and terminal configurations. If your ISV serves one of these verticals, Global Payments’ specialization translates to faster integration and fewer edge cases.

NMI is deliberately horizontal. The platform serves any vertical equally through its processor-agnostic architecture. This is an advantage for ISVs whose merchants span multiple industries, or for ISVs in verticals where Global Payments doesn’t have specialized solutions.

When to Choose NMI

NMI is the stronger choice for ISVs that:

- Need processor flexibility — you want to choose (or let merchants choose) from multiple processors

- Prioritize white-label branding — your merchants should never see NMI’s name

- Want fast, automated merchant onboarding — 91% same-day approval through self-service tools

- Serve multiple verticals — horizontal flexibility beats vertical specialization for your business

- Have development resources — your team can handle more integration depth in exchange for more control

- Value transparent pricing — flat gateway fee with visible, separate processing costs

When to Choose Global Payments

Global Payments is the stronger choice for ISVs that:

- Operate in healthcare, education, or restaurants — GP’s vertical depth provides real value

- Want a single vendor relationship — one contract covering gateway, processing, and merchant services

- Need in-person merchant setup — GP’s fully-supported onboarding handles hardware and training

- Prefer a hybrid PayFac model — GP’s 2023 hybrid offering lets ISVs act as sub-merchant facilitators without full PayFac registration

- Are large enough to negotiate custom terms — revenue sharing and favorable pricing require volume leverage

- Want NYSE-listed enterprise stability — Global Payments (GPN) is a publicly traded company with global reach

Consider a Third Option

Both NMI and Global Payments serve ISVs well, but they represent two ends of a spectrum: maximum flexibility (NMI) versus maximum integration (Global Payments). Some ISVs find that neither extreme is the right fit.

ISV-first embedded payment platforms like Xplor Pay bridge this gap — offering the white-label capabilities and ISV-focused onboarding that NMI provides, with the integrated acquiring and vertical expertise that Global Payments brings. See how they compare in our Xplor Pay vs NMI and Xplor Pay vs Global Payments analyses. If your ISV needs embedded payments without choosing between flexibility and simplicity, it’s worth evaluating platforms specifically built for the ISV use case.

Get a personalized comparison for your ISV →

Frequently Asked Questions

Is NMI a payment processor or a gateway?

NMI is a payment gateway — specifically, a “gateway operating system” that connects to 200+ payment processors. It does not process transactions itself. Your ISV chooses which processor handles the actual transaction processing, and NMI routes the transaction through its gateway layer.

Can I switch from Global Payments to NMI (or vice versa)?

Switching from Global Payments to NMI means re-integrating your payment flow through NMI’s gateway API. Because NMI is processor-agnostic, you’ll also need to select a new processor. Switching from NMI to Global Payments means consolidating onto GP’s proprietary stack. In both cases, expect 4-8 weeks of development work and a merchant migration plan.

What’s the typical ISV integration timeline?

NMI’s quick-start guide promises “first integration in minutes” for basic payment acceptance, though a production-ready ISV integration typically takes 2-6 weeks. Global Payments’ integration process includes a certification step where GP validates your workflows, which adds time but reduces post-launch issues. Plan for 4-8 weeks for either platform.

How do ISVs earn revenue from embedded payments?

ISVs monetize embedded payments through the spread between merchant fees and processor costs. Both NMI and Global Payments offer revenue sharing models, though terms vary significantly based on volume, vertical, and negotiation. NMI’s partner-enabled model starts sharing revenue from the first transaction. Global Payments’ revenue share is more commonly available to larger ISV partners.

What happened to OpenEdge?

OpenEdge was Global Payments’ ISV-focused division, rebranded to Global Payments Integrated. The technology platform is the same, but the branding change has caused documented confusion — some merchants report difficulty distinguishing between OpenEdge and Global Payments parent company support channels.

The Bottom Line

NMI and Global Payments serve different ISV profiles. NMI wins on flexibility, white-labeling, and pricing transparency — it’s the platform for ISVs that want control over their payment stack and serve merchants across multiple verticals. Global Payments wins on vertical depth, enterprise stability, and hybrid PayFac options — it’s the platform for ISVs in specialized industries who want a single integrated partner.

Neither platform is universally “better.” The right choice depends on your ISV’s specific vertical, transaction volume, technical resources, and how much of the payment experience you want to own. For more context, see how NMI stacks up against other gateways in our Adyen vs NMI and Braintree vs NMI comparisons, or explore Worldpay vs Global Payments and Global Payments vs Fiserv for full-stack processor alternatives.

Need help evaluating which platform fits your ISV? Get a free integration assessment →