Adyen vs NMI

A feature-by-feature comparison for ISVs integrating payments.

Both platforms embed payments for ISVs, but they sit at opposite ends of the architecture spectrum — Adyen owns the full stack from gateway to acquiring bank; NMI owns only the gateway layer and lets the ISV pick the acquirer. The right pick is a fit decision against your platform's stage, geography, and how much of the payment stack you want to own — not a feature checklist.

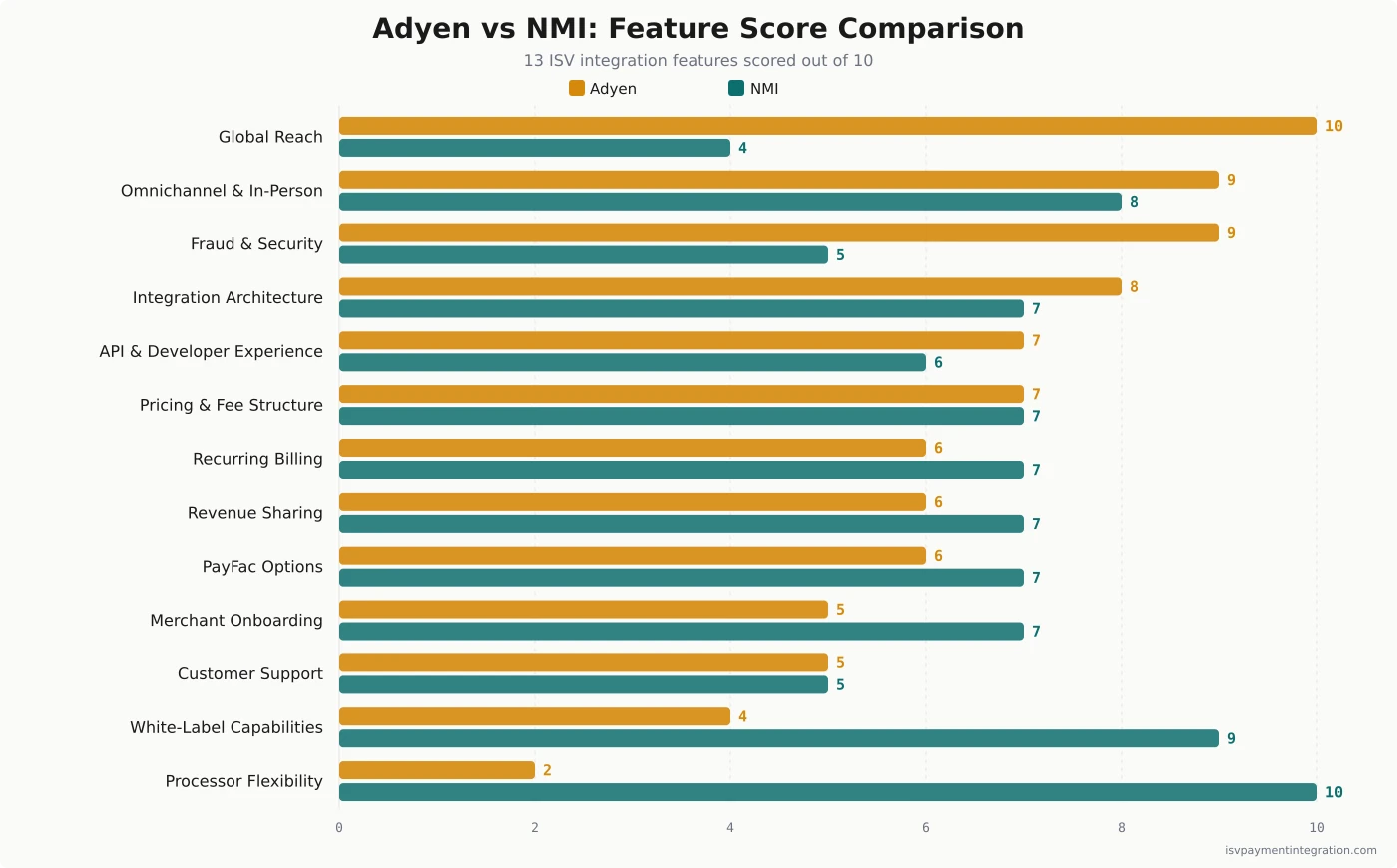

Feature Comparison

| Feature | Adyen | NMI |

|---|---|---|

| Integration Architecture | 8 | 7 |

| API & Developer Experience | 7 | 6 |

| White-Label Capabilities | 4 | 9 |

| Processor Flexibility | 2 | 10 |

| Pricing & Fee Structure | 7 | 7 |

| Omnichannel & In-Person Payments | 9 | 8 |

| Fraud & Security | 9 | 5 |

| Revenue Sharing | 6 | 7 |

| Merchant Onboarding | 5 | 7 |

| Global Reach | 10 | 4 |

| Recurring Billing | 6 | 7 |

| Customer Support | 5 | 5 |

| PayFac Options | 6 | 7 |

Get this comparison as a shareable PDF

We'll send the Adyen vs NMI breakdown to your inbox — ready to share with your team.

Best for

Adyen

Best for enterprise and upper mid-market ISVs processing $50M+ annually with international customers, omnichannel commerce, and a need for embedded finance. Not ideal for early-stage ISVs or SMB-heavy sub-merchant portfolios due to the unpublished minimum invoice.

Best for

NMI

Best for ISVs, ISOs, and PayFacs that want acquirer-independence, white-label embedded payments, and 300+ EMV device coverage across unattended/self-service merchants. Best when the ISV is willing to manage two commercial relationships (gateway + acquirer).

Adyen vs NMI for ISVs

Most “Adyen vs NMI” comparisons compare them on features. They’re not the same kind of company. Comparing them on features is like comparing a vertically integrated airline to a global distribution system — both move passengers, but the operating models, the contracts, and the unit economics work differently from the first decision onward. This page is the version of that comparison written for ISVs who already know they need embedded payments and now have to choose which architectural path their platform sits on for the next five years.

Both models are legitimate. Both have named ISVs running production volume on them. Both will keep working in 2027 and 2028. The friction you inherit is what differs.

The Quick Take: Who Each Platform Actually Is

Adyen is a full-stack payments platform — gateway, processor, and Dutch-licensed acquiring bank rolled into one product. Founded in Amsterdam in 2006 and public on Euronext since 2018, the company processed €1.29 trillion in 2024 (up 33% YoY) for clients including eBay, Microsoft, Uber, Spotify, Toast, and Lightspeed. The Adyen for Platforms segment — the embedded-finance suite that competes with Stripe Connect — grew 50% YoY in 2024 and reached €27B in platform volume across 255,000 terminals by H1 2025. Pricing renders as $0.13 + Interchange+ + 0.60% on Visa/Mastercard (Adyen’s Interchange++ pricing model), with no setup or monthly fees but an unpublished minimum invoice that sets a meaningful commercial floor.

NMI is a pure payment gateway — it does not acquire transactions, hold a BIN, or settle funds. Founded in 2001 in Schaumburg, Illinois and now backed by Francisco Partners, Great Hill Partners, and Insight Partners, NMI processes $502B+ in annual transaction volume across 6.5B+ transactions, 6,000 channel partners, 1.2M+ active merchants, and 235,000 connected devices (per the company’s January 2026 year-end disclosure). The platform connects to 200+ pre-certified acquiring processors (Fiserv, Worldpay/Global Payments, TSYS, Elavon, Chase Paymentech, Barclaycard) and certifies 300+ EMV payment devices. Pricing is partner-negotiated, splitting a per-transaction gateway fee from the acquirer-side interchange-plus economics that flow through to whichever processor the merchant routes to.

The strategic philosophies underneath the architectures are inverses. Adyen’s published positioning, paraphrased by analyst Jevgenijs Kazanins in Popular Fintech: the company “does not have the organizational capacity to serve small businesses” and explicitly aims to be “the partner of choice for platforms serving SMBs.” That’s a deliberate access gate — Adyen bets that 60% of US merchant-acquiring net revenue comes from sub-$1M merchants (UBS analysis cited in the same piece), and that the only economic way to reach those merchants is through ISV/SaaS distribution rather than direct sales. NMI’s bet is the inverse: be the gateway any ISV can pick up on day one, regardless of size, and let the acquirer-side relationship sort the unit economics. Adyen filters at the door; NMI optimizes the room.

What Adyen and NMI Actually Are

The architectural difference between these two platforms is the most important thing to understand before reading any further. Most reviews skip it; almost every wrong decision starts there.

Adyen: full-stack acquirer with embedded-finance suite

Adyen holds acquiring licenses in the United States (since 2012), Europe, the United Kingdom, Australia, and Singapore. It operates under a Dutch banking license, runs direct relationships with Visa, Mastercard, and local card networks, and skips the intermediate-processor layer that legacy acquirers depend on. For ISVs, that vertical integration produces three things competitors can’t easily replicate: higher authorization rates (no extra hops in the routing chain), cleaner chargeback and dispute handling (Adyen owns the relationship with the network), and a single dashboard that unifies online, in-store, and recurring payments across geographies. The platform’s RevenueProtect risk management engine sits inside the same stack — custom fraud rules, network tokenization, and 3DS2 authentication run against payment data in real time as transactions flow through Adyen’s own infrastructure rather than through a third-party risk service.

The Adyen for Platforms product extends that stack into embedded finance for ISVs. Sub-merchant onboarding spans 33+ countries with 23 languages of KYC/AML/MATCH-list checks, real-time identity verification, and on-demand or scheduled payouts to sub-merchant bank accounts. Three add-on tiers complete the suite — Capital (revenue-share-repaid lending), Issuing (physical or virtual cards for sub-merchants), and Accounts (embedded banking for fund holding and money movement). For an ISV building vertical SaaS in retail, hospitality, restaurant tech, or marketplaces, this is a one-vendor offering that competes directly with Stripe Treasury, Capital, and Issuing.

The trade-off is everything that comes with a full-stack platform: longer onboarding for sub-merchants, a higher minimum-volume bar that is industry-specific and not published publicly, and sales-led commercial engagement on the way in.

NMI: gateway-first platform with multi-acquirer routing

NMI’s positioning starts with a deliberate refusal to acquire. The platform sits between the merchant’s point of sale or website and any of 200+ acquiring processors — the same value proposition Authorize.Net popularized in the early 2000s, scaled to a global ISV/ISO partner network and modernized for embedded-payments use cases.

For ISVs, that gateway-first model produces a different set of strengths. One integration covers many acquirers — your software writes one API integration, and your merchants can be settled by First Data/Fiserv, Worldpay/Global Payments, TSYS, Elavon, Chase Paymentech, Barclaycard, or any of dozens of regional acquirers depending on geography, vertical fit, or commercial terms. The platform stays invisible — NMI’s white-label depth means the ISV’s brand owns the merchant relationship completely, with no NMI logo, document, or reference appearing in the sub-merchant flow. The 300+ EMV device estate spans Ingenico, ID TECH, Madic, Payter, FEIG, and LANDI hardware certified across ecommerce, in-person, mobile, and unattended/self-service environments — a footprint that’s structurally hard to replicate for ISVs serving parking, vending, transit, kiosk, EV-charging, or other self-service verticals.

The trade-off is that NMI is a gateway, not a one-stop shop. Your software platform still needs an acquirer relationship — direct or through an NMI-partnered ISO or PayFac — and the ISV ends up managing two commercial relationships (gateway and acquirer) instead of one.

Pricing & ISV Economics

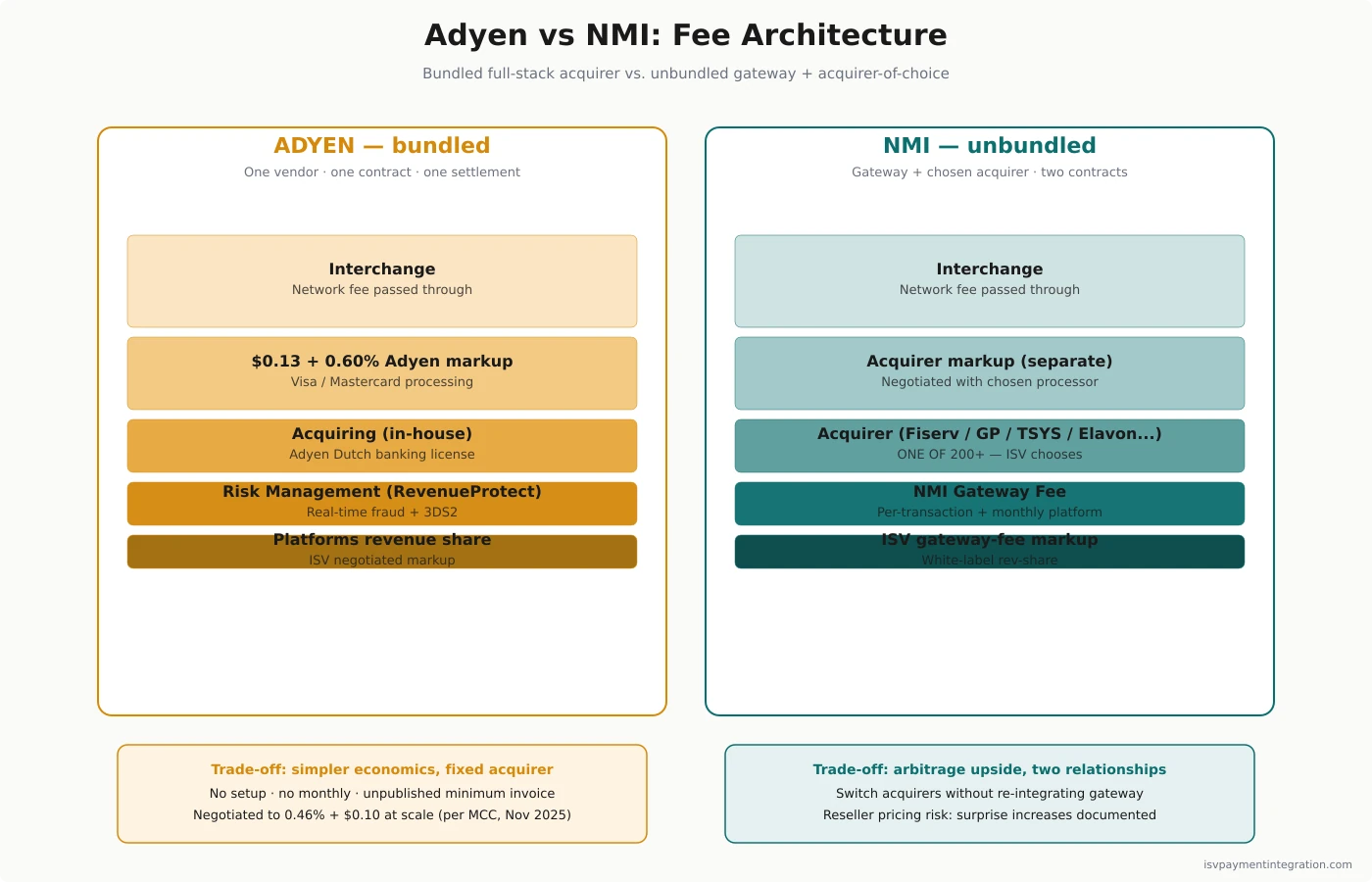

This is where the two platforms diverge most sharply. Adyen publishes a rate. NMI doesn’t. That difference is downstream of the architectural choice each platform made about what to bundle.

Adyen: interchange++ with an unpublished minimum invoice

Adyen’s pricing page is unusually forthcoming for an enterprise processor — though Adyen itself labels the published figures indicative. Visa and Mastercard price at $0.13 + Interchange+ + 0.60% under Adyen’s Interchange++ model, and the FAQ frames that number as a starting point to “discuss pricing options,” not a committed rate. Amex North America runs 3.3% + $0.10 + $0.13 per transaction (not the 3.95% global Amex rate). ACH transfers are $0.13 + $0.27. UnionPay is 3% + $0.13. BNPL via Affirm, Klarna, and Clearpay processes at 4.19% + $0.30 + $0.13. The processing fee is consistent across most payment methods, which makes the rate stack predictable for high-volume merchants.

The 0.60% published markup is also negotiable. Merchant Cost Consulting, a fee-consulting firm with direct Adyen contract access, documented a November 2025 negotiated client proposal at 0.46% + $0.10 per transaction, with tiered drops to 0.25% + $0.10 for merchants processing over $8M/month — roughly 35% lower than the published floor for high-volume platforms. The firm also reports its clients have not experienced post-signature price increases, which is a different pattern than the rate-creep complaints documented at multiple PE-backed gateways.

What Adyen does not charge: no setup fees, no monthly account fees, no closure fees. What Adyen does charge that the pricing page is quiet about: an industry-dependent minimum invoice. Enterprise customers report it lands at a level that effectively rules out small businesses and low-volume merchants. The number is not public, but if your annual processing is under roughly $1M, expect the minimum invoice to come up in sales conversations as the gating commercial term.

For ISVs running Adyen for Platforms, the revenue-share economics are negotiated against expected platform volume — Adyen’s model lets you mark up the per-transaction rate to your sub-merchants and capture the spread, with revenue-sharing structured per platform contract.

NMI: gateway fees plus acquirer-side interchange (separate)

NMI’s commercial model splits the economics across two layers that other platforms bundle. The gateway layer charges the ISV a per-transaction gateway fee plus monthly platform fees, both partner-negotiated and not publicly published. The actual interchange-plus economics live with whichever acquirer the merchant settles through — NMI does not take interchange itself, since it doesn’t acquire.

For ISVs, this produces a meaningful margin difference. The bundled-economics platforms (Adyen’s full-stack model, Stripe Connect’s flat platform fee) give the ISV a single number to negotiate and a single contract to sign. NMI’s split-economics model gives the ISV genuine acquirer arbitrage — different acquirers, different geographies, different vertical specializations, all behind the same NMI integration — but requires managing two separate commercial relationships.

The trade-off shows up most acutely in price-stability risk. Multiple Trustpilot reviewers in NMI’s reseller and ISO tier — including one in January 2026 (“This is the 3rd or 4th time with surprised increased pricing, into the thousands… corporate decisions with people clients can not communicate with”) and another in early 2025 documenting “Mandatory Year End operating fees” that don’t appear on any published rate sheet — describe the same pattern: opaque pricing changes propagating down through partners. ISVs building on NMI need to model that residual risk explicitly in partner SLAs, since the rate-change clauses control whether merchant economics stay stable across renewal cycles.

For ISVs with sophisticated payments teams or multi-vertical merchant bases, the split-economics model is a feature. For ISVs that want one vendor, one contract, and a managed-services experience, it’s friction.

The margin math for ISVs

Take a hypothetical sub-merchant processing $200K/month at an average 2.6% interchange-plus blended rate on card payments. With Adyen for Platforms, the ISV pays Adyen IC + $0.13 + 0.60% — call it ~2.7% all-in including the per-transaction fee on average ticket size — and marks up to the merchant at, say, 2.9% + $0.30. The ISV captures roughly 0.20%–0.30% on volume plus the per-transaction spread, settling through Adyen, on one contract.

With NMI, the same merchant might settle through (for example) Wind River Financial as the partnered acquirer. The ISV pays NMI a gateway fee per transaction plus monthly platform fees, then negotiates the acquirer rev-share with Wind River separately. The math can come out higher or lower than Adyen depending on the negotiated terms — the point is that the ISV controls more variables and has to manage more relationships to capture them.

Both pricing pages cover the model architecture rather than specific basis points: the Adyen pricing breakdown and the NMI pricing model walk the structure for each platform.

Integration Architecture

For ISVs, the integration story isn’t just API quality — it’s the operational model the platform enforces around merchant onboarding, fund settlement, and dispute handling.

Adyen for Platforms: one platform, sub-merchant onboarding built in

Adyen for Platforms exposes APIs for sub-merchant onboarding, KYC verification, payouts, and fund management. The integration model is opinionated: the ISV calls Adyen to create sub-merchants, Adyen runs identity verification and compliance checks against MATCH-list and KYC requirements, Adyen handles funds-on-hold and payout schedules, and the ISV gets a unified view of every sub-merchant across the portfolio in a single Adyen dashboard.

Hosted onboarding flows are available out of the box. Fully customized onboarding can be built against the API for ISVs that want to retain UI control. The payment experience can be white-labeled for the most part, though Adyen’s brand surfaces in some compliance flows and dispute documentation.

The trade-off is that Adyen owns the sub-merchant relationship in the regulatory sense — Adyen is the underwriter, the funds-flow operator, and the compliance owner. ISVs get speed and simplicity in exchange for less control over the underwriting decisions.

NMI Merchant Central: the multi-acquirer ISO/PayFac console

NMI’s integration story for ISVs centers on Merchant Central — the residual management, agent payout, marketing automation, and merchant onboarding hub that lets an ISV (or its partnered ISO) run sub-merchant operations across multiple acquirer relationships from one interface. The case study on ISVPay, an Alpharetta, Georgia ISO focused on unattended-payments ISVs, describes how Merchant Central’s TurboApp portal centralized the entire merchant onboarding workflow through a single console.

Behind Merchant Central, ScanX/MonitorX runs the underwriting automation — 100+ risk checks per merchant application with risk-scored decisioning in minutes rather than days. That’s the engine that makes the NMI embedded-payments pitch operationally credible for ISVs that don’t want to register as their own payment facilitator.

The integration model gives the ISV more control over the underwriting decision (especially when working with a partnered ISO that can adjust risk thresholds per vertical) at the cost of a less opinionated workflow. ISVs that want a self-serve sub-merchant signup flow have to build it on top of NMI’s APIs; Adyen’s hosted onboarding is closer to ready out of the box.

Revenue Sharing & PayFac Models

Both platforms support revenue share for ISVs — it’s the central monetization promise of any embedded-payments integration — but the mechanics are different.

Adyen for Platforms lets ISVs earn revenue share on every sub-merchant transaction, with revenue mechanics negotiated against expected platform volume. The model rewards platforms with predictable, high-volume sub-merchant bases — Adyen’s economics reward scale, and the minimum-invoice term prices SMB-heavy platforms out of the most favorable terms. The Capital, Issuing, and Accounts add-ons compound the revenue opportunity by giving the ISV additional spreads on lending, card spend, and embedded banking. For platforms that are already mid-market or enterprise-volume, this is a complete embedded-finance monetization stack from one vendor.

NMI’s partner model is more traditional ISO economics, dressed for the ISV era. The ISV (or its partnered ISO) earns a markup on the gateway fee plus a negotiated rev-share on the acquirer-side interchange. The economics are highly negotiable because they’re stitched together across two relationships, and ISVs with leverage on either side (high volume, vertical specialization, growth trajectory) can usually do better than the published partner-tier rates of bundled platforms.

The architectural difference is whether the PayFac-as-a-Service economics live with one vendor (Adyen) or are assembled across two (NMI + acquirer). ISVs that want the simpler revenue accounting often pick Adyen. ISVs that want maximum negotiating leverage often pick NMI.

White-Label Control

This is where NMI most clearly outperforms Adyen for ISVs that need brand invisibility.

Adyen offers white-label capability but ships with co-branded defaults. Adyen’s brand surfaces in dispute documentation, KYC compliance flows, some sub-merchant communications, and the underlying payments dashboard if sub-merchants are given direct access. The platform can be heavily customized to minimize Adyen visibility, but the practical reality of running Adyen for Platforms is that the Adyen name appears in enough places that it’s effectively a co-branded experience for the sub-merchant.

NMI ships with full white-label as the default. Partners can run an end-to-end embedded payments experience with NMI nowhere on the merchant-facing surface — no brand on checkout, no logo on settlement reports, no name on dispute notifications. The ISV’s brand owns the merchant relationship completely.

For ISVs whose competitive positioning depends on owning the merchant brand experience (vertical SaaS where the merchant has chosen the ISV as their primary platform; embedded payments where the payments experience must feel native), NMI’s white-label depth is a meaningful differentiator. For ISVs where the payments brand is less load-bearing (marketplaces where the brand is the marketplace, not the underlying infrastructure), Adyen’s co-branded defaults are not a buying objection.

Geographic Reach

Adyen wins this category decisively, but the magnitude of the win depends on whether the ISV’s merchants are actually international.

Adyen holds direct local acquiring licenses in 33+ markets, supports 200+ payment methods including local options like iDEAL (Netherlands), SEPA (Europe), Konbini (Japan), and Pix (Brazil), and operates from offices across Europe, North America, Asia-Pacific, and Latin America. For ISVs with international sub-merchants, one Adyen integration covers what would otherwise require multiple processor relationships, multiple currency-conversion partners, and multiple compliance frameworks. The direct acquiring footprint also produces meaningfully higher authorization rates in the markets where Adyen acquires natively versus pass-through processors.

NMI operates as a US-anchored gateway with explicit UK, EU, and Republic of Ireland coverage through its UK entity (Network Merchants Limited). The 300+ EMV device certifications cover all four geographies with locally certified hardware. Beyond US/UK/EU/ROI, NMI depends on its partnered acquirers for additional geographic reach — the gateway model means international expansion is an acquirer-relationship decision, not an NMI-platform decision.

The practical translation for ISVs: if your sub-merchants are heavily international with material volume in non-Anglo markets, Adyen is structurally easier. If your sub-merchants are concentrated in the US, UK, EU, and Ireland, NMI’s coverage is sufficient and the multi-acquirer routing inside those geographies often wins on commercial terms.

Onboarding Friction & Sub-Merchant Approval

Both platforms run real KYC, AML, and MATCH-list checks — that’s not negotiable in regulated payments. The difference is in approval velocity and the ISV’s role in the underwriting decision.

Adyen runs a thorough underwriting process that can take days to weeks for sub-merchants in higher-risk verticals or with incomplete documentation. The underwriting is centralized — Adyen makes the decision, the ISV provides the application data, and the timeline depends on Adyen’s internal queue. Smaller sub-merchants and SMB-heavy ISV portfolios feel this most acutely; the most common B2B-review complaint about Adyen is exactly this onboarding pace.

NMI’s TurboApp through Merchant Central is engineered for fast decisioning. The published ISVPay case study reports a best-month performance of 98.2% approval rate, 91% same-day approval, 92.8% activation within 15 days, and 97.7% retention for sub-merchants flowing through TurboApp. ISVPay’s VP of Customer Experience Lacey Frenzl described the workflow shift directly: “We’re no longer sending PDFs back and forth or chasing down wet signatures — there are no delays. When the merchant submits their application through the ISV, it reaches us instantly. We review and audit the forms, then submit everything through TurboApp, with approvals often coming back within hours.” That data is filtered through an ISO intermediary rather than a direct ISV-to-NMI integration, but it’s the most concrete published evidence on either platform’s onboarding throughput.

The Adyen side of this comparison is roughly the inverse. Embed.co’s November 2025 mid-market SaaS analysis put Adyen for Platforms integration at 120–160 developer hours, 5–6 month implementation timelines, and tens of thousands of euros in sunk cost before first transaction. That’s a 2-quarter commitment, not a sprint, and it’s the single largest reason ISVs evaluating Adyen end up either negotiating deeper with Stripe (Connect Custom, interchange-plus) or picking NMI as the faster path to live revenue.

For ISVs serving SMB-heavy sub-merchant bases or that need to hit a near-term go-live date, NMI’s onboarding model is structurally faster. For ISVs serving mid-market and enterprise sub-merchants where activation speed matters less than regulatory rigor and the long-term embedded-finance roadmap, Adyen’s approach is closer to the right shape.

Customer Support Reality

Both platforms carry support reputation issues that ISVs need to underwrite honestly.

Adyen’s customer support runs primarily through email ticketing for non-enterprise accounts. Enterprise clients with named account managers report responsive service; platform-tier and smaller clients report meaningful delays in support response and a lack of phone-support escalation paths. The most vocal complaint across G2, Capterra, and Trustpilot is exactly this — when a fund hold or account verification needs fast human attention, the email-only model becomes a real constraint.

NMI’s support quality varies significantly with the partnered ISO/PayFac. Direct merchants who reach NMI itself often report transferred-and-held experiences; merchants supported by their partnered ISO get a more personal touch but quality depends entirely on the partner. The unclaimed Trustpilot profile (2.0/16) shows recurring patterns around customer support unresponsiveness, surprise pricing changes, and billing-after-cancellation that ISVs need to plan support content for.

For ISVs running either platform, the same mitigation applies: position your own support team in front of every sub-merchant flow so merchants reach the ISV’s escalation path before they reach the gateway’s.

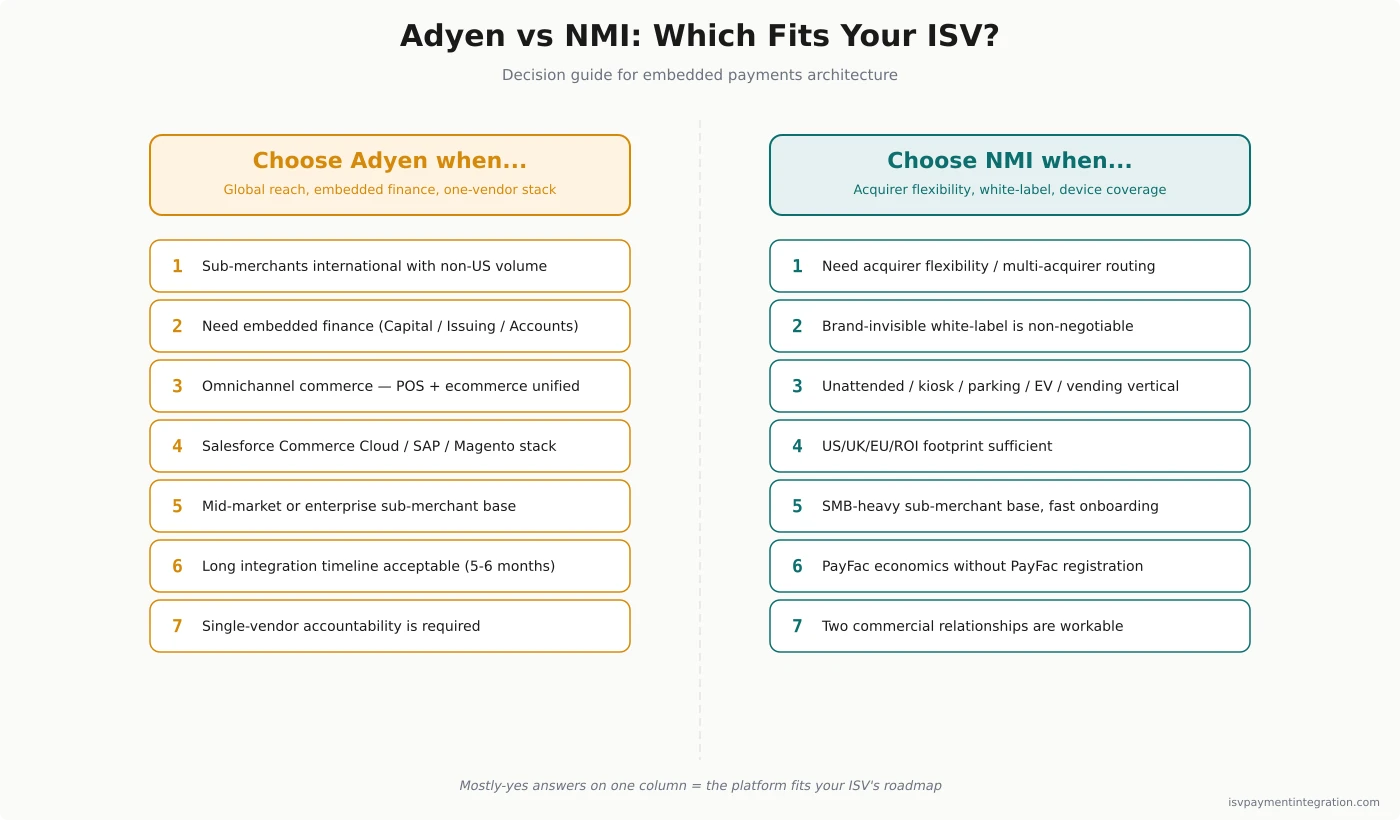

When Adyen Wins for ISVs

Adyen is the right pick when the ISV’s profile matches what the platform is built for:

- Enterprise and upper mid-market ISVs processing $50M+ annually across the platform

- International sub-merchant bases that need local payment methods (iDEAL, SEPA, Pix, Konbini) and direct acquiring in non-US markets

- Omnichannel commerce — POS software, retail-plus-ecommerce, restaurant tech — where unified online and in-store data on one dashboard removes meaningful operational friction

- Embedded-finance roadmaps that monetize beyond payments through Capital (lending), Issuing (cards), or Accounts (embedded banking)

- Salesforce Commerce Cloud or enterprise commerce stacks where Adyen is a certified payment provider with native integration

- Platforms with named enterprise reference clients in their merchant base — Adyen’s roster of Toast, Lightspeed, Uber, Spotify, eBay, and Microsoft is genuinely useful for sales. The Adyen for Platforms named client list is broader than most ISVs realize: Olo, Mews, Roller, Epos Now, Wix, Bill, Moneybird, Etsy, and Vinted all run on the program

The maturity model is real. Lightspeed’s documented payments journey walks the path most ISVs follow: Phase 1 referral-only, Phase 2 revenue-share ISO model (2018), Phase 3 fully integrated payments via Adyen. Lightspeed GM of Payments Jona Georgiou described the destination: “Pairing a card reader with an iPad or another device, or pay at your screen, pay at your table — it all runs through a single engine, and that’s our edge.” For ISVs at Phase 1 or 2 today, Lightspeed’s arc is the playbook for what Phase 3 looks like once merchant volume justifies the integration investment. For an ISV that fits this profile, Adyen for Platforms is one of the two or three best embedded-finance stacks on the market and is the natural Stripe Connect alternative at the enterprise tier.

When NMI Wins for ISVs

NMI is the right pick when the ISV values acquirer flexibility, brand control, or device coverage above one-vendor convenience:

- ISOs and ISVs with multi-acquirer requirements — the ability to swap or layer acquirers behind a single gateway integration is operationally meaningful, especially for ISVs with merchants that have been impacted by acquirer M&A (Worldpay → Global Payments, First Data → Fiserv)

- Unattended, self-service, kiosk, transit, parking, EV-charging, vending verticals where NMI’s 300+ EMV device estate (Ingenico, ID TECH, Madic, Payter, FEIG, LANDI) is structurally hard to replicate

- Brand-critical embedded payments — vertical SaaS, white-label PFaaS, embedded-payments-as-a-feature where the ISV’s brand has to own the merchant relationship completely

- Multi-region without re-architecture — US/UK/EU/Republic of Ireland coverage from one gateway integration with locally certified device estates

- Partner-enabled PFaaS economics — NMI’s white-label embedded payments model lets ISVs earn rev-share without registering as their own PayFac, with named ISO references like Wind River Financial, ISVPay, and Anovia Payments

For an ISV that fits this profile, NMI is the gateway most likely to match the next five years of platform evolution — the multi-acquirer optionality compounds in value as the ISV’s merchant base diversifies. Steven Pinado’s appointment as CEO in September 2025 reinforces the direction: his background includes board seats at Helcim (a direct-to-merchant acquirer with strong SMB ISV tooling) and Browzwear (3D fashion software), plus prior roles at Billtrust (B2B AR automation) and Constellation Payments (embedded payments for software platforms). The Helcim seat in particular signals NMI’s intent to compete more aggressively for ISV software partners under the new regime, not just ISO resellers — a meaningful strategic tilt for ISVs evaluating long-term partner alignment.

NMI’s January 2026 year-end disclosure also previewed the next product surface: Tap to Pay (NFC mobile acceptance), AI-powered fraud and risk tools, and Embedded Lending — the company’s direct response to Adyen Capital. The lending product lets ISVs offer merchant capital inside their own software, repaid against future payment volume. For ISVs picking a payments infrastructure partner today, that 2026 lending parity matters: both Adyen and NMI are now racing to be the embedded credit provider as well as the embedded payments provider, and the platform decision is increasingly a 2027–2028 capital-product decision too.

How They Compare to Stripe Connect & Other Alternatives

Both Adyen and NMI exist in a competitive set that ISVs should benchmark against at least one or two other platforms before committing.

vs Stripe Connect — Stripe Connect is the default for SaaS platforms that want bundled gateway/acquirer/risk and best-in-class developer ergonomics across the broadest geography. Adyen wins when acquiring economics at scale, omnichannel commerce, or embedded finance matter more than developer self-serve speed. NMI wins when acquirer flexibility, multi-acquirer routing, or unattended-payments device coverage matter more than developer-tooling polish. See Stripe vs Adyen and NMI vs Stripe for the head-to-heads.

vs Checkout.com — Checkout.com is Adyen’s closest enterprise peer with global acquiring and a platform product, often more responsive on commercial terms but with a smaller geographic footprint. See Adyen vs Checkout.com.

vs Finix — Finix is a platform-first processor positioned explicitly against Adyen’s enterprise-first stance, with no minimum-invoice friction. The right pick for ISVs that want full PayFac economics without a sales-led commercial engagement. See Adyen vs Finix.

vs Authorize.Net — The other major US gateway brand, owned by Visa via the 2010 CyberSource acquisition. Authorize.Net’s product velocity has been described as steady-state under Visa stewardship, while NMI’s PE-backed acquisitive growth produces faster product churn. ISVs valuing stability often pick Authorize.Net; ISVs valuing modular growth pick NMI.

vs Global Payments — A full-stack acquirer with its own embedded-payments product (Genius) and direct ISV partnerships. The choice between Global Payments and NMI depends on whether the ISV wants single-vendor accountability (Global Payments) or unbundled flexibility with an independent gateway (NMI). NMI also supports merchants settled by Global Payments — the question is one of commercial structure, not technical compatibility. See NMI vs Global Payments.

Final Verdict by ISV Use Case

For most ISVs, the decision between Adyen and NMI comes down to four binary questions. Each one points decisively to one platform or the other.

| Question | If yes → | If no → |

|---|---|---|

| Are sub-merchants international with material non-US volume? | Adyen (33-country direct acquiring) | NMI (US/UK/EU footprint sufficient) |

| Does the ISV need embedded finance beyond payments (lending, cards, banking)? | Adyen (Capital + Issuing + Accounts) | NMI (payments-only is fine) |

| Is the ISV’s brand expected to be invisible behind the merchant experience? | NMI (full white-label default) | Adyen (co-branded acceptable) |

| Does the ISV need acquirer flexibility (multi-acquirer routing, vertical-specialist routing)? | NMI (200+ acquirer connections) | Adyen (single-vendor simpler) |

For ISVs that answer yes to the first two questions, Adyen is structurally the right platform — the embedded-finance suite plus international acquiring is hard to assemble any other way. For ISVs that answer yes to the second two questions, NMI’s gateway-first model is the right fit — the multi-acquirer flexibility and white-label depth are hard to replicate with a bundled platform.

For ISVs in the middle — domestic US, payments-focused, brand-flexible, single-acquirer comfortable — the decision usually comes down to volume profile. Mid-market and enterprise volumes favor Adyen’s acquiring economics; SMB-heavy portfolios favor NMI’s faster onboarding and no-minimum-invoice commercial model.

Frequently Asked Questions

Who is Adyen’s biggest competitor?

Stripe is Adyen’s most direct competitor in the enterprise and platform tier — both offer full-stack payments with embedded-finance suites (Stripe Connect + Treasury + Capital + Issuing vs Adyen for Platforms + Capital + Issuing + Accounts). Other meaningful competitors include Checkout.com (closest peer on global acquiring), PayPal/Braintree (developer-friendly with PayPal as a native payment option), Worldpay (now part of Global Payments after the January 2026 acquisition), and Fiserv (legacy acquirer with the broader US merchant footprint). For ISVs specifically, the Adyen vs Stripe Connect decision is the most common live evaluation.

Who are NMI’s competitors?

NMI’s direct competitors are other gateway-first platforms: Authorize.Net (Visa-owned, longest-tenured US gateway), Braintree’s gateway layer (PayPal-owned), and to a lesser extent Spreedly (which positions more as a payment orchestration layer than a gateway proper). On the bundled-platform side — vendors that compete with NMI by offering a different model rather than a comparable gateway — the competitive set includes Stripe Connect, Adyen, Global Payments’ embedded-payments products, and vertical-SaaS-focused PFaaS providers like Payrix (now Worldpay for Platforms inside Global Payments) and Tilled.

Does Adyen work in the USA?

Yes. Adyen has held a US acquiring license since 2012, runs a New York City office, and supports all major US payment methods including card networks, ACH Direct Debit, Apple Pay, Google Pay, bank transfers, and BNPL via Affirm, Klarna, and Clearpay. US pricing uses interchange-plus with $0.13 + 0.60% on Visa/Mastercard, Amex North America at 3.3% + $0.10 + $0.13 per transaction, and ACH at $0.13 + $0.27. For in-store merchants, Adyen sells its own payment terminals with unified reporting across online and in-person channels.

Is NMI a good company?

NMI is a legitimate enterprise payments platform with strong PE backing (Francisco Partners, Great Hill Partners, Insight Partners), real scale ($502 billion annual transaction volume across 6,000+ partners and 1M+ merchants), and named ISO/ISV reference partners (Wind River Financial, ISVPay, Anovia Payments). The 2.0/16 Trustpilot rating reflects downstream-merchant complaints — surprise pricing changes, support unresponsiveness, billing after cancellation — that ISVs absorb as brand risk via the ISO/PayFac chain rather than through the NMI brand directly. For ISVs, the right read is to evaluate NMI on the gateway product (which is genuinely strong) while planning for the support and billing friction that downstream merchants sometimes experience.

Can an ISV use both Adyen and NMI?

Yes — and some ISVs do exactly this. The split usually maps to merchant geography or merchant tier: Adyen handles international and enterprise sub-merchants where direct acquiring and embedded finance pay back the higher onboarding friction; NMI handles US-domestic and SMB sub-merchants where faster activation and partner-tier economics matter more. The trade-off is operational complexity — running two payments stacks doubles the integration surface, the reconciliation work, and the support training. For most ISVs, the right answer is to pick one and grow on it; the dual-platform approach makes sense only when the merchant base is large enough and bifurcated enough to justify the overhead.

What to Do Next

The verdict is already at the top of this page. The four-question table in the section above narrows the answer to one platform for most ISVs. What remains is execution. A short checklist for whichever direction the decision pointed.

If Adyen is the answer, request a quote through the Adyen for Platforms contact form rather than the generic enterprise sales path — the platforms team handles ISV evaluations differently and will ask for sub-merchant volume projections, vertical mix, and target geographies in the first call. Bring three numbers to the meeting: expected platform GMV in year one, the SMB-vs-mid-market split of your sub-merchant base, and your roadmap for embedded finance (lending, cards, banking). The minimum-invoice conversation will surface in call two; the rate negotiation room sits roughly 30–35% below the published 0.60% Visa/Mastercard markup based on Merchant Cost Consulting’s documented client outcomes.

If NMI is the answer, the path is rarely direct. Most ISVs sign NMI through a partnered ISO or PFaaS provider — names worth contacting include Wind River Financial, Anovia Payments, or any of NMI’s named tier-1 ISO partners listed under Merchant Central case studies. Bring two questions to that conversation: what acquirer the ISO routes through for your sub-merchant profile, and what the rate-change notification clause looks like in the partner SLA. The reseller-tier surprise-pricing pattern documented in this comparison is real; the mitigation is contractual, not editorial.

If both should compete head-to-head, run the same 90-day evaluation against each: the same target sub-merchant cohort, the same volume assumptions, the same embedded-payments user story. Score against the feature comparison matrix at the top of this page and the decision guide above. The exercise usually surfaces a clear winner inside three sales conversations.

For deeper fee mechanics, see the Adyen pricing breakdown and NMI pricing model. For the third option in this market, NMI vs Stripe and Stripe vs Adyen cover the Stripe Connect comparison from each side.