Global Payments Review

The Worldpay acquisition made Global Payments a pure-play commerce giant with a powerful but complex two-track ISV stack.

Overview

Global Payments became a different company in January 2026, closing its $24.25B Worldpay acquisition and divesting its issuer business to FIS. For ISVs, the upside is a genuinely strong two-track stack — Global Payments Integrated for integrated payments and Worldpay for Platforms (Payrix) for PayFac-as-a-Service — backed by global, full-stack acquiring. The cost is acquisition-built complexity, negotiated pricing with no public rates, and a documented rate-escalation reputation.

For the latest on Global Payments's ISV capabilities, documentation, and partner programs, visit globalpayments.com.

Pricing

Interchange-plus (negotiated; no public rates)

Global Payments publishes no rate card — every ISV and merchant deal is negotiated. Interchange-plus with a negotiated markup; ISV revenue share ranges from roughly 30% (referral) to 90% (full PayFac via ProPay). Authorization fees apply per attempt and chargebacks run $15-25. Watch for documented post-acquisition rate increases and add-on fees.

Full pricing breakdown →Pros

- ✓ Two-track ISV stack: GPI for integrated payments plus Worldpay for Platforms (Payrix) for PayFac-as-a-Service

- ✓ Genuine global reach — $3.7T volume across 175+ countries as a full-stack direct acquirer

- ✓ Owned vertical software (Heartland, AdvancedMD, Genius) opens joint go-to-market angles

- ✓ $1B+ annual product investment; Worldpay integration running ahead of schedule

Cons

- ✗ No published pricing — every deal is negotiated and opaque

- ✗ Documented rate-escalation pattern and add-on fees (2026 MDR increase, infrastructure fee, PCI fees)

- ✗ Contract and cancellation complaints — three-year terms, early-termination fees, equipment leases

- ✗ Post-merger brand complexity — multiple overlapping ISV product lines to navigate

ISV Fit

Best for ISVs that want a global, full-stack acquiring partner with both integrated-payments and PayFac-as-a-Service tracks — especially Worldpay for Platforms/Payrix — plus vertical software depth. Less ideal for ISVs that want transparent published pricing and fast, self-serve onboarding.

Global Payments became a meaningfully different company in January 2026. The close of its $24.25 billion Worldpay acquisition — paired with the sale of its issuer-processing business to FIS — turned Global Payments into a pure-play commerce giant and, more importantly for software companies, handed it one of the strongest ISV payment stacks in the industry. This review evaluates Global Payments strictly from the ISV and SaaS-platform perspective in 2026: not how it serves a coffee shop, but how it serves a software company embedding payments for thousands of merchants.

Global Payments Review: An ISV’s Perspective

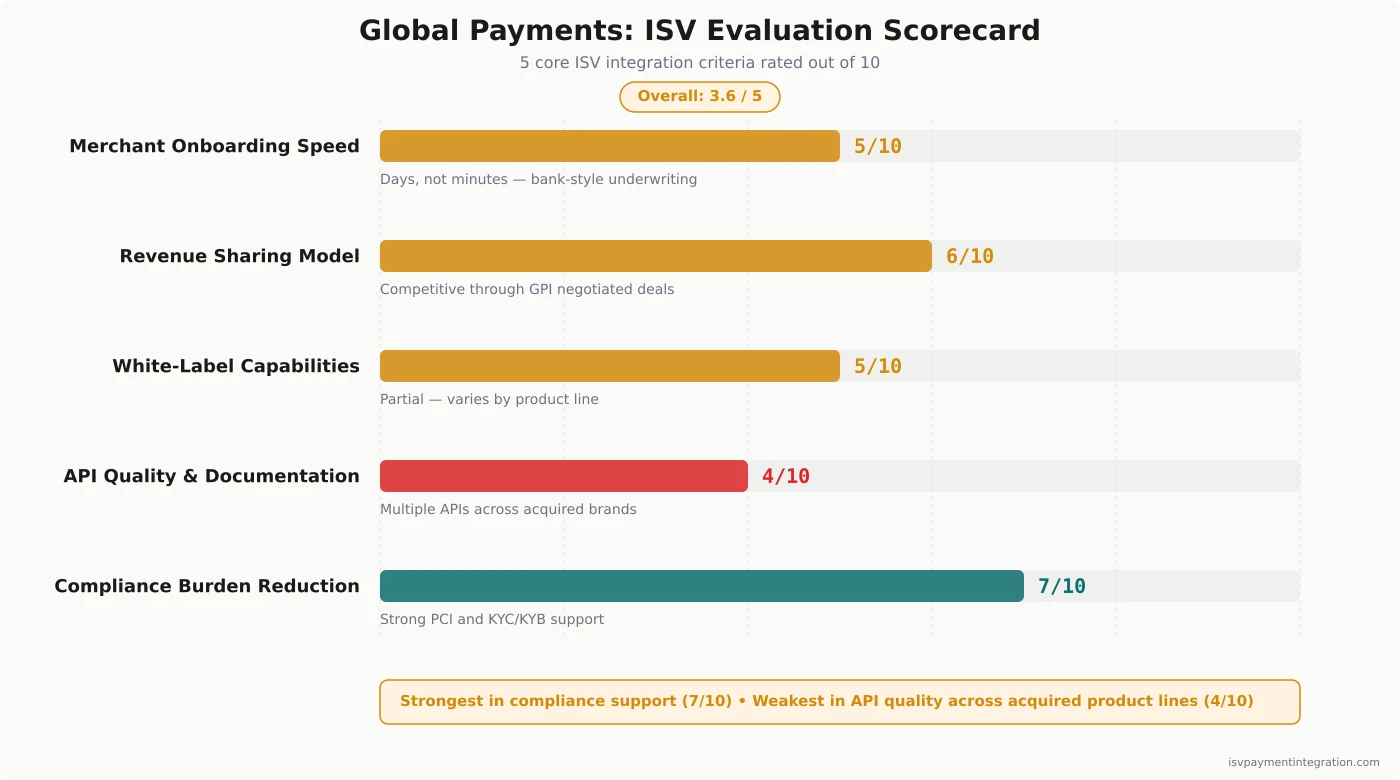

We rate Global Payments 3.7 out of 5 for ISV embedded payments. That rating is a balance of two opposing truths. On one side, Global Payments now operates two complementary ISV tracks — Global Payments Integrated for integrated payments and Worldpay for Platforms (with Payrix) for payment facilitation as a service — backed by genuinely global, full-stack acquiring. On the other, it carries the baggage of a company assembled through decades of acquisitions: opaque negotiated pricing, a documented pattern of rate increases, and a customer-service and contract reputation that gives merchants pause.

A provider can be excellent for direct merchants and mediocre for ISV integration, or the reverse. Our score reflects ISV-specific criteria — merchant onboarding, revenue sharing, white-label control, API quality, and how much compliance the platform carries — not general payment processing. For ISVs, the 2026 version of Global Payments is more capable than the 2025 version, which is why the rating moves up, but the reasons for caution have not gone away.

The Worldpay Acquisition: What Changed in 2026

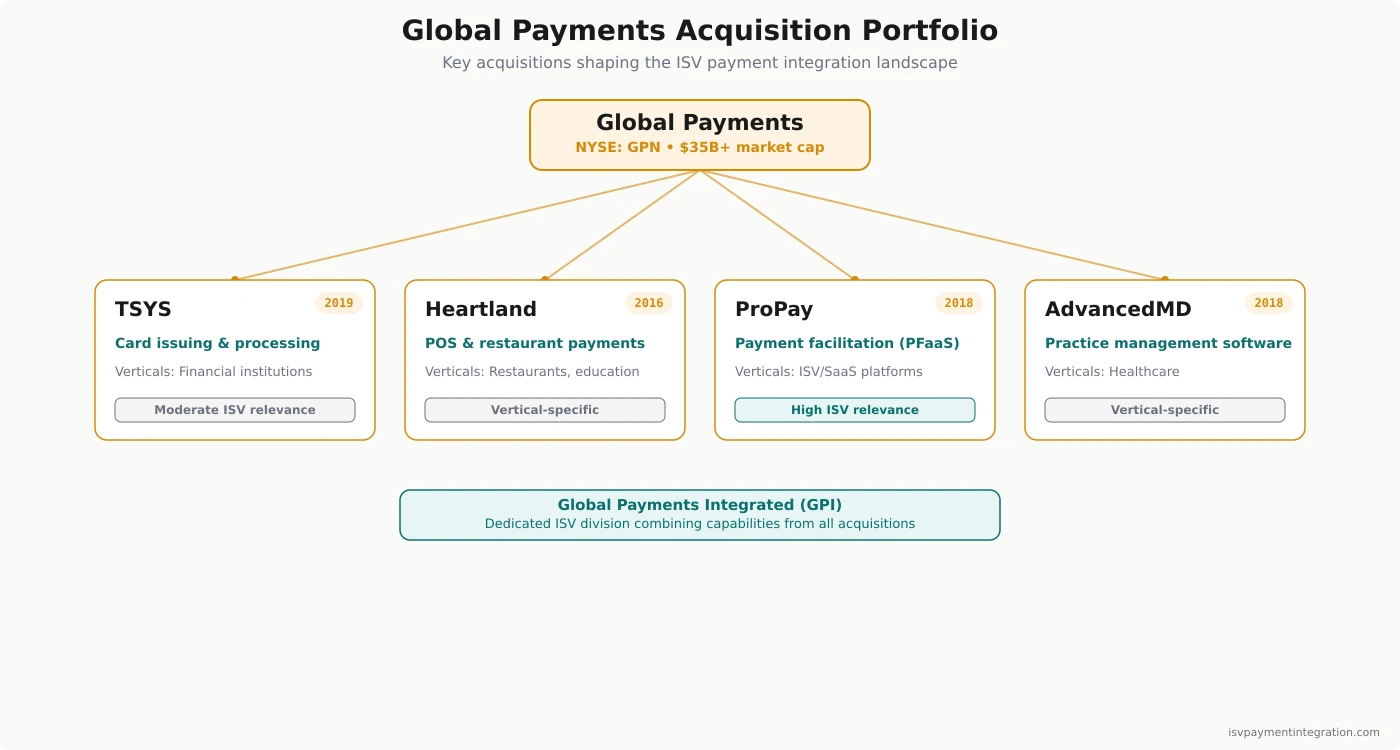

On January 9, 2026, Global Payments completed its acquisition of Worldpay at a $24.25 billion enterprise value, paying roughly $6.2 billion in cash plus 43.27 million newly issued shares, with Worldpay’s former owner GTCR retaining about 15% of the company (American Banker). Simultaneously, Global Payments sold its Issuer Solutions business — the old TSYS card-issuing operation that served banks — to FIS for a $13.5 billion enterprise value (Global Payments IR). The result is a cleaner company: Global Payments is now a pure-play merchant acquirer and commerce-software business with no issuer side.

The scale is real. The combined company processes roughly $3.7 trillion in annual payment volume across about 94 billion transactions, serving more than 6 million merchant locations in 175-plus countries. In Q1 2026 — the first quarter with Worldpay consolidated — adjusted net revenue reached $2.86 billion and adjusted earnings per share came in at $2.96, ahead of consensus, with CEO Cameron Bready reporting that “Day 100” integration milestones were completed ahead of plan (Q1 2026 earnings). Management has committed more than $1 billion a year to product investment and is targeting $600 million in cost synergies by 2028.

For an ISV, the headline is not the size — it is what Worldpay brought with it. Worldpay for Platforms, and the Payrix embedded-payments business inside it, is one of the most capable ISV PayFac offerings in the market, and it now sits under the same roof as Global Payments Integrated. That gives Global Payments two distinct, complementary ways to serve software companies — a combination few competitors can match.

Global Payments’ ISV Stack: GPI and Worldpay for Platforms

Announcing the Worldpay close, Global Payments said it would “go to market through three channels: Enterprise, SMB, and Integrated & Platforms,” each with its own sales strategy and product roadmap. ISVs live in the third. That channel is real and already selling — in May 2026 the company announced that “its Integrated and Platforms business” had renewed and expanded its partnership with Lightspeed DMS, deploying Payrix Pro embedded payments to 4,500-plus dealerships.

What has not happened is a merger of the two ISV brands underneath it. Global Payments told the SEC, in its Form 10-Q for the quarter ended March 31, 2026, that it “was still in the process of modifying the design of our operating structure to combine the operations of the acquired Worldpay business with our existing Merchant Solutions business,” and that it would not report against new segments until that work finished. So the channel exists; the reporting structure behind it does not yet. From an ISV’s point of view, that leaves two tracks that were built separately and are still sold separately.

Global Payments Integrated (GPI), formerly OpenEdge, is the legacy ISV division. It serves more than 4,000 technology partners across roughly 70 industries and processes over a billion transactions a year for partner merchant bases. GPI is the traditional integrated payments route: a software company embeds Global Payments’ acquiring rails and earns a share of processing revenue, with the depth of involvement scaling by partnership tier.

Worldpay for Platforms, with Payrix as its flagship, is the embedded-payments-native track Global Payments gained in the acquisition. Payrix Pro lets a software company hold a PayFac-style position in the merchant experience — owning onboarding and the customer relationship — while Worldpay handles the underwriting, compliance, and sponsor-bank layer underneath (Worldpay for Platforms). This is true PayFac-as-a-Service, and it is the more modern of the two tracks. Rounding out the portfolio, Genius is Global Payments’ owned POS platform (now being cross-sold into Worldpay’s enterprise accounts), and Heartland brings vertical software for restaurants, schools, and nonprofits.

The practical implication: an ISV evaluating Global Payments is really choosing a track, not just a vendor. A software company that wants a straightforward integrated-payments referral relationship will land in GPI; one that wants to own a branded, white-label embedded payments experience will want Worldpay for Platforms and Payrix.

How ISVs Embed Payments with Global Payments

Both tracks offer a ladder of partnership models that map to how much of the payments business an ISV wants to run. Worldpay for Platforms names its three rungs explicitly — Referral payments, PayFac-as-a-Service, and PayFac® developer. The GPI track offers an analogous progression, and advertises a “revenue sharing program” of its own, with ProPay® as its named payment-facilitation product:

- Referral / agent model — the ISV refers merchants; Global Payments owns the merchant relationship, onboarding, and risk. The lightest lift and the smallest economics.

- PayFac-as-a-Service / hybrid PayFac — the ISV controls onboarding and the merchant experience while the provider handles compliance, underwriting, and sponsor-bank access. A middle path for software companies that want the economics without the regulatory apparatus.

- Full payment facilitation — via ProPay on the GPI side, or PayFac® developer on the Worldpay side. The ISV owns the merchant experience end to end and keeps the largest share of the economics, along with the heaviest operational and regulatory burden.

Neither Global Payments nor Worldpay publishes revenue-share percentages for any of these tiers. GPI’s site confirms a revenue sharing program exists and that ProPay “allows flexibility in setting fees, easily splitting funds and more.” Worldpay’s platforms site advertises “configurable fees” — the ability for a platform to set its own merchant pricing. Neither attaches a number to any of it, and no rate card exists. The percentage bands widely quoted elsewhere on the web appear in no Global Payments filing, no earnings material, and on neither company’s product pages. Anyone quoting you a precise band without a source is guessing; get yours in writing.

Technical onboarding runs through the Global Payments partner developer portal, and the Worldpay for Platforms track has its own developer documentation and Payrix implementation path. Both tracks reduce the ISV’s PCI and underwriting burden relative to becoming a registered payment facilitator independently — which is the entire point of building on a provider like this rather than going direct to the card networks. The trade, as always, is that the more compliance Global Payments carries, the more of the economics and control it keeps.

Pricing and Fees for ISVs

This is where ISV diligence matters most. Global Payments publishes no pricing — not for merchants, and not for ISV partnerships. Every deal is negotiated, and the terms vary widely by processing volume, vertical, and partnership tier. A platform processing $50 million a year will negotiate materially different economics than one at $2 million. The base structure is interchange-plus with a negotiated markup; authorization fees are charged per attempt regardless of outcome, and chargebacks run roughly $15-25 each. For the partnership-tier revenue-share ranges, see our Global Payments pricing breakdown.

The bigger pricing story is escalation, and it is the single most important thing for an ISV to understand. Global Payments has a well-documented pattern of raising rates and adding fees after a relationship is established. In January 2026 it increased the merchant discount rate by 0.20% across accounts not already hit by an earlier 2025 increase, and a new “Infrastructure Upgrade Fee” of roughly $450 appeared on merchant statements in late 2025 (Merchant Cost Consulting). Merchants on legacy Heartland and TSYS-lineage accounts have reported effective rates climbing dramatically over time — in one documented case from 2.25% in 2013 to over 15% by early 2026 through incremental unilateral adjustments.

For an ISV, these increases are not abstract — they land on the merchants on your platform, and they can trigger attrition and chargeback disputes that become your support problem and your reputation risk. The defensive move is contractual: negotiate rate-lock provisions, cap pass-through fee increases, and get the escalation terms in writing before you sign. The strength of Global Payments’ platform is real, but so is the need to negotiate hard against its pricing playbook.

The Fees ISVs and Their Merchants Should Watch For

Because Global Payments bundles many fees and discloses none publicly, it helps to know the line items that appear on merchant statements — the ones your platform’s merchants will ask you about. The recurring fees documented across Global Payments, Heartland, and TSYS-lineage accounts include:

- PCI non-compliance fees — merchants who do not complete PCI self-assessment have reported monthly charges around $125, on top of an annual PCI fee.

- Annual fees — a roughly $499 annual fee appeared on some merchant statements at the end of 2025 without prior contractual notice.

- Infrastructure and upgrade fees — a new fee of about $450 surfaced on statements in late 2025.

- Early-termination fees — standard three-year contracts carry early-termination fees, and some include liquidated-damages clauses that raise the cost of leaving further.

- Equipment leases — multi-year equipment leases, sometimes 48 months, are a recurring complaint when merchants say the terms were not clearly disclosed at signup.

- Authorization and batch fees — authorization fees are charged per attempt regardless of approval, with batch and statement fees layered on top.

- Rate increases — periodic merchant-discount-rate increases, including a 0.20% bump in early 2026, applied without direct written notice in many documented cases.

The takeaway for an ISV is not that every merchant pays all of these — it is that the fees exist, are not published, and tend to grow over time. Build fee transparency into your merchant communications and negotiate caps where you can, so that a Global Payments fee increase does not become a surprise your support team has to absorb or, worse, a reason a merchant blames your software.

Strengths for ISVs

Genuine global reach

At $3.7 trillion in volume across 175-plus countries, few acquirers match Global Payments’ cross-border coverage. An ISV expanding internationally can consolidate most markets under one acquiring partner rather than stitching together regional processors.

Full-stack direct acquiring

Global Payments is a direct acquirer, not a reseller, which means tighter economics, faster issue escalation, and no middleman margin between your platform and the card networks. Combined with its own sponsor-bank relationships, that gives ISV partners a more controllable stack.

Two complementary ISV tracks

The combination of GPI and Worldpay for Platforms/Payrix is the differentiator. Most competitors offer one model; Global Payments lets an ISV choose integrated payments or full PayFac-as-a-service depending on scale and compliance appetite — and grow from one to the other inside one company.

Owned vertical software

Global Payments owns software businesses in restaurants, education, healthcare, and hospitality. If your vertical overlaps, there are joint go-to-market and distribution angles beyond raw payment rails — something a pure payments provider cannot offer.

Committed product investment

With over $1 billion in annual product investment and Worldpay integration milestones reported ahead of schedule, the platform is being actively developed rather than left to stagnate post-merger.

Weaknesses and Risks for ISVs

Opaque pricing and rate escalation

The lack of published rates plus the documented increase pattern is the dominant risk. ISVs that do not negotiate protective contract terms can watch their merchants’ costs creep upward, with the fallout landing on the platform.

Contract and cancellation reputation

Across Heartland, TSYS, and Global Payments-branded accounts, complaints recur around three-year contracts with early-termination fees, equipment leases with terms merchants say were misrepresented, billing that continued after confirmed cancellation, and slow refunds — including one acknowledged overcharge of more than $6,000 that remained unresolved for months. Global Payments is not BBB-accredited and carries a meaningful volume of such complaints. Most come from direct SMB merchants rather than ISV partners, but the pattern still touches the merchants on an ISV’s platform.

Post-merger complexity

With GPI, Worldpay for Platforms, Payrix, Genius, and Heartland all under one roof, an ISV has to navigate which product line is the right fit — and the merged company’s internal channel strategy is still settling. Expect to spend real time understanding the org before you understand the integration.

Customer service

Reviews consistently describe support as slow and disjointed, with merchants chasing representatives across multiple follow-ups. For an ISV whose product depends on its payment partner resolving merchant issues quickly, this is a material operational consideration.

Integration risk

Merging two large legacy technology stacks is a multi-year effort, and any delay in platform migration could introduce instability for ISV partners. Markets remain cautious — the stock traded well below analyst targets through early 2026 — which is a signal the integration thesis is not yet proven.

Global Payments vs the Alternatives

For ISVs that prize transparency and developer experience, the most common alternative is Stripe, whose published pricing and Connect platform offer self-serve onboarding and revenue share without negotiation — at the cost of Global Payments’ global acquiring depth and vertical software. ISVs that want to own the full payments stack and capture the maximum margin spread often look at Finix, which is built for software companies graduating into their own PayFac, or compare Global Payments against Adyen for enterprise, multi-national scale.

There is also irony worth noting for diligence: Payrix, now Global Payments’ modern PFaaS engine via Worldpay for Platforms, is the same product an ISV would have evaluated as an independent option a few years ago. If you want a sense of how that PFaaS model competes head to head, our Payrix vs Stax comparison and the Finix and Stax reviews are useful companions. The takeaway: Global Payments now contains a top-tier PFaaS, but you access it inside a much larger and more complex organization.

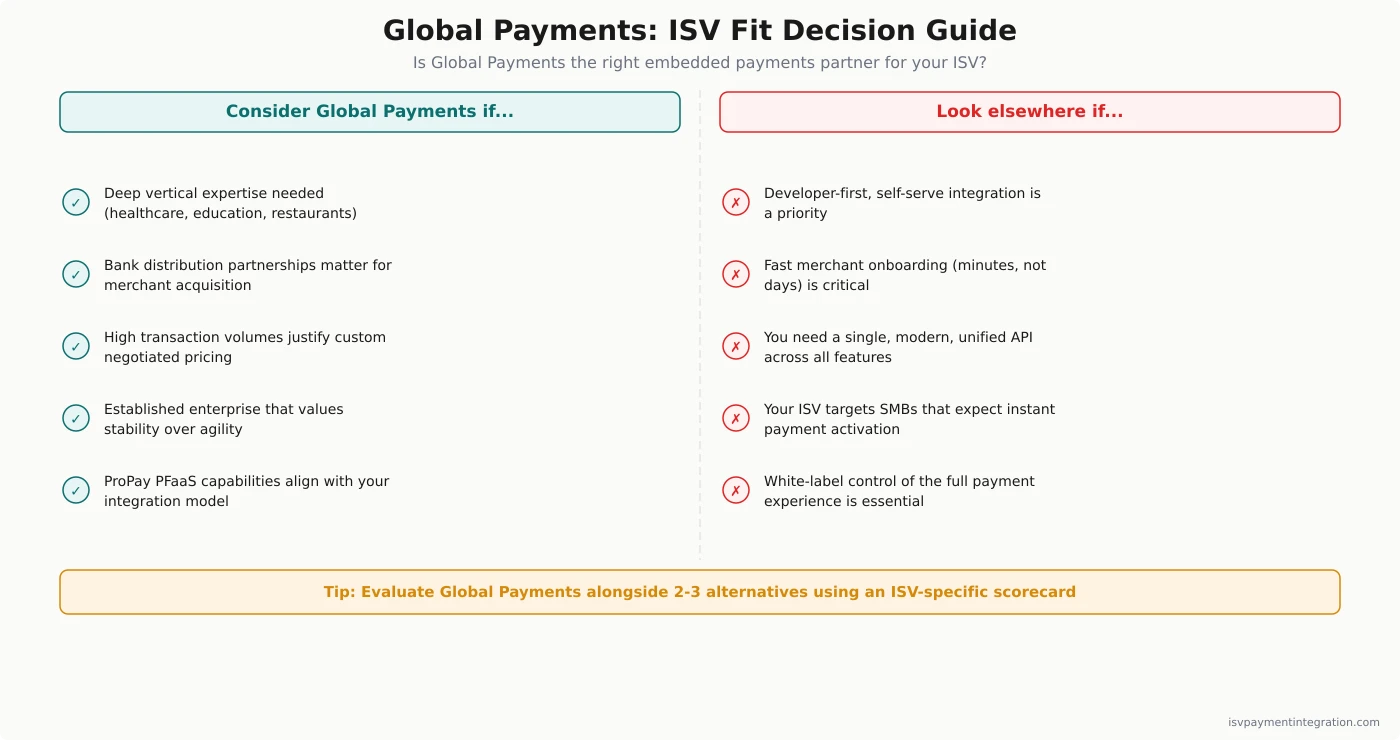

Who Should Choose Global Payments

Global Payments fits ISVs that need global, full-stack acquiring and want the option of both integrated payments and PayFac-as-a-Service under one partner. If your platform serves merchants across many countries, or your vertical overlaps with Global Payments’ owned software (restaurants, healthcare, education, hospitality), the distribution and reach are hard to replicate elsewhere. Larger and mid-market ISVs with the volume to negotiate strong terms — and the legal resources to lock them — get the most value, particularly through Worldpay for Platforms and Payrix.

It is a weaker fit for early-stage or small ISVs that want transparent, published pricing and fast self-serve onboarding. Those teams will generally find Stripe or a focused PayFac-as-a-Service provider faster to adopt and easier to reason about. And any ISV that cannot or will not negotiate hard on pricing and contract terms should think twice — Global Payments’ platform rewards sophisticated partners and penalizes passive ones.

The Bottom Line

Global Payments in 2026 is genuinely more compelling for ISVs than it was a year ago. The Worldpay acquisition gave it a two-track ISV stack — integrated payments through GPI and PayFac-as-a-Service through Worldpay for Platforms and Payrix — on top of global, full-stack acquiring and a portfolio of vertical software. That is a real, differentiated capability, and it earns the 3.7 rating.

The same acquisition-built scale is the source of the caveats: opaque negotiated pricing, a documented rate-escalation pattern, contract and service complaints, and the integration risk that comes with merging two giants. None of those are dealbreakers for a prepared ISV, but they are reasons to go in with eyes open and a hard-negotiated contract. If you are weighing Global Payments for your platform, get an ISV payments assessment and we will map your merchant base, volume, and vertical to the right track — and the right protections.

Frequently Asked Questions

Did Global Payments buy Worldpay?

Yes. Global Payments completed its acquisition of Worldpay on January 9, 2026, at a $24.25 billion enterprise value, while simultaneously selling its Issuer Solutions (TSYS card-issuing) business to FIS. The result is a pure-play commerce company processing about $3.7 trillion in annual volume across 175-plus countries. For ISVs, the key gain is Worldpay for Platforms and its Payrix embedded-payments product, now part of Global Payments.

Is Global Payments a legit and safe company to use?

Yes, Global Payments is a legitimate, publicly traded company (NYSE: GPN) and one of the largest merchant acquirers in the world, serving over 6 million merchant locations. “Safe” in the security sense is not the concern — it is PCI compliant and bank-backed. The recurring criticisms are commercial: opaque pricing, rate increases over time, and contract and cancellation friction. It is a credible partner that requires careful contract diligence.

How much does Global Payments charge per transaction?

Global Payments publishes no rates — all pricing is negotiated. The structure is interchange-plus with a negotiated markup, plus per-attempt authorization fees and chargeback fees of roughly $15-25. ISV revenue share ranges from about 30% on a referral model to 90% on a full PayFac arrangement via ProPay. Because there is no public rate card, an ISV must negotiate terms directly — and lock them, given the documented pattern of post-signup increases.

What is the Global Payments controversy?

The main controversy is pricing conduct. Merchants and review bodies have documented Global Payments (and its Heartland and TSYS-lineage brands) raising rates without clear notice, adding fees such as a 2026 merchant-discount-rate increase and an infrastructure fee, and enforcing long contracts with early-termination penalties. Some merchants report effective rates climbing far above their original quotes over time. It is not a fraud question — it is a transparency and contract-conduct question that ISVs should address in negotiation.

What is Worldpay for Platforms and Payrix?

Worldpay for Platforms is Global Payments’ ISV-native embedded-payments brand, and Payrix is its flagship PayFac-as-a-Service product. Together they let a software company embed payments and hold a payment-facilitator-style position — owning onboarding and the branded merchant experience — while Worldpay handles underwriting, compliance, and the sponsor-bank relationship. It is the more modern of Global Payments’ two ISV tracks and the main reason the company’s 2026 ISV offering is stronger than before.