Payrix vs Stax

A feature-by-feature comparison for ISVs integrating payments.

Payrix and Stax both market embedded payments to ISVs but answer fundamentally different questions. Payrix is a PayFac-as-a-Service stack — now part of Worldpay for Platforms inside Global Payments — that lets the ISV operate as a sub-PayFac and capture the full markup spread above interchange. Stax is a subscription-priced merchant platform with an ISV partner program (Stax Connect) and three published tiers from $99 to $199+ per month. The decision turns on whether the ISV wants to become a payment facilitator or partner with one.

Feature Comparison

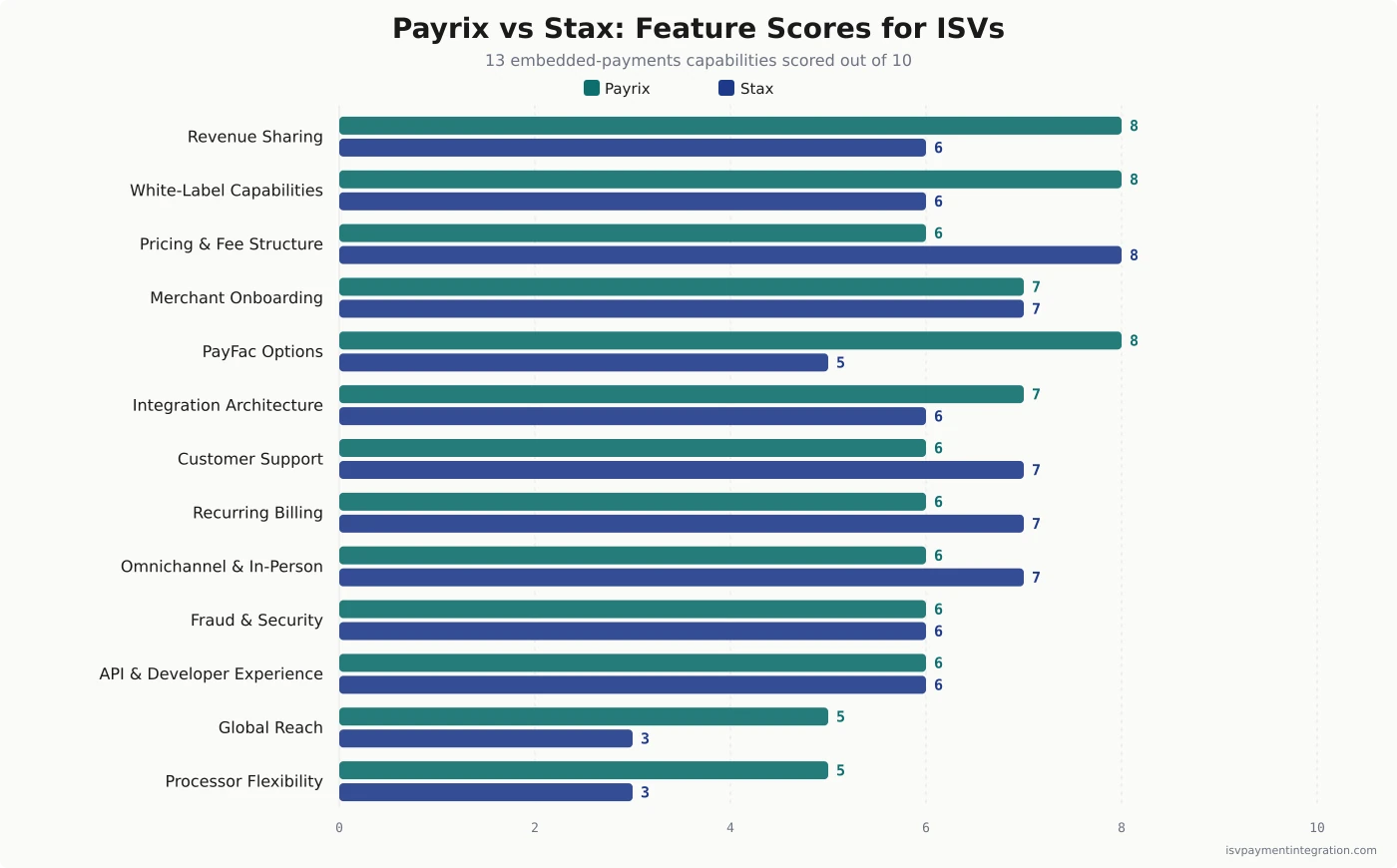

| Feature | Payrix | Stax |

|---|---|---|

| Integration Architecture | 7 | 6 |

| API & Developer Experience | 6 | 6 |

| White-Label Capabilities | 8 | 6 |

| Processor Flexibility | 5 | 3 |

| Pricing & Fee Structure | 6 | 8 |

| Omnichannel & In-Person Payments | 6 | 7 |

| Fraud & Security | 6 | 6 |

| Revenue Sharing | 8 | 6 |

| Merchant Onboarding | 7 | 7 |

| Global Reach | 5 | 3 |

| Recurring Billing | 6 | 7 |

| Customer Support | 6 | 7 |

| PayFac Options | 8 | 5 |

Get this comparison as a shareable PDF

We'll send the Payrix vs Stax breakdown to your inbox — ready to share with your team.

Best for

Payrix

ISVs ready to operate as a sub-PayFac with full PFaaS infrastructure, vertical-specific underwriting, and access to Worldpay's 146+ country acquiring network — now positioned inside Global Payments after the January 2026 acquisition. Best for mid-market and enterprise software companies in property management, healthcare, fitness, field services, or nonprofit verticals where vertical-specific compliance and high-touch implementation pay back.

Best for

Stax

ISVs whose merchants are US-based, who prefer published subscription pricing ($99/$139/$199+ per month with 0% interchange markup) over negotiated PFaaS economics, and who want a partner platform rather than the operational weight of running as a PayFac. Best for vertical SaaS companies with smaller engineering teams and SMB merchant bases.

Payrix and Stax both pitch ISVs on embedded payments, but they answer different questions. Payrix is a PayFac-as-a-Service stack now sitting inside Worldpay for Platforms, which Global Payments completed acquiring in January 2026. The ISV operates as a sub-payment facilitator on Payrix’s rails and earns the spread between merchant-facing rates and the wholesale cost. Stax is a subscription-priced merchant platform — formerly Fattmerchant — with a separate ISV partner program called Stax Connect, three published price tiers, and a still-private ownership structure under Greater Sum Ventures.

For an ISV, the choice between these two is rarely a feature comparison. It is a business-model comparison. Payrix wants the software company to act as its own PayFac and keep the markup. Stax wants the software company to partner with a flat-priced merchant platform and share in subscription and transaction revenue. The math, the integration surface, and the corporate exposure look very different on either side.

The corporate backstory: how Payrix and Stax got to 2026

The two platforms started in the same era — 2014 and 2015 — but their ownership stories diverged sharply, and that backstory now shapes ISV-side risk calculations.

Payrix: from independent PFaaS pioneer to Global Payments subsidiary

Payrix was founded in 2015 as one of the first PayFac-as-a-Service businesses built specifically for software companies. FIS — the parent of Worldpay at the time — announced the acquisition of Payrix on February 15, 2022. By September 2022, FIS had rebranded the platform-facing offering as Worldpay for Platforms and folded Payrix into a unified ISV stack alongside the broader Worldpay acquiring network.

In January 2026, Global Payments closed its $24.25B acquisition of Worldpay. Payrix is now part of that combined entity. The current platforms.worldpay.com positioning describes three integration modes for ISVs: Referral Payments, PayFac-as-a-Service, and PayFac Developer. The Payrix brand remains visible in technical documentation and partner agreements, but strategic decisions — pricing, roadmap, partner economics — now route up through Worldpay for Platforms and on to Global Payments at the top. ISVs evaluating Payrix in 2026 are signing into a top-tier processor with massive scale and a freshly merged corporate parent. Our Worldpay vs Payrix breakdown covers how the parent positions against its own subsidiary.

Stax: Fattmerchant, the Greater Sum Ventures era, and a 2026 leadership refresh

Stax was founded in 2014 as Fattmerchant. The business pioneered subscription-priced merchant processing — a flat monthly fee replacing percentage-based markup — and rebranded as Stax in 2020. Greater Sum Ventures, a Knoxville-based growth equity firm whose portfolio collectively processes north of $60 billion annually, took control through an acquisition completed December 1, 2020. Stax then closed a unicorn round in March 2022, valued above $1B.

In February 2026, Stax appointed John Cimba as CEO. Cimba came directly from Greater Sum Ventures, where he had been an operating partner, and previously ran PropertyTek — a vertical-SaaS business with integrated payments. That background is a clear signal: the parent fund wants Stax leaning harder into vertical-SaaS embedded payments, not the small-merchant Stax Pay product. The following month, Stax announced new appointments to chief commercial, chief operating, and chief technology roles, with VJ LeBlanc promoted to CTO and prior CTO Mark Sundt moving sideways into a Chief AI Officer role. For ISVs, the signal is mixed: a refreshed leadership team energized to build, paired with the operational uncertainty that comes with a synchronized C-suite reshuffle.

A second corporate development matters here. On October 7, 2025, Stax completed its evolution into a full-stack end-to-end processor with the launch of Stax Processing — built on the APPS (acquired 2023) and BlockChyp (acquired 2024) integrations, with a direct connection to all major US card networks. Stax is no longer a Worldpay reseller; it now operates its own clearing, settlement, and tokenization stack. That’s structurally important for ISV evaluations because reviews and analyses written before Q4 2025 typically describe Stax as routing through external acquirers — and that description is now stale.

Pricing models head-to-head

Both platforms charge on interchange-plus economics, but everything that surrounds that number diverges. Payrix prices privately and lets the ISV control the markup. Stax prices publicly and bundles the markup into a fixed subscription fee. The two models behave very differently as merchant volume scales.

Payrix’s negotiated PFaaS economics

Payrix does not publish merchant rates. Pricing is structured per ISV partner, with the markup, monthly minimum, and any platform fee negotiated against expected processing volume, vertical risk profile, and the depth of integration. The ISV sets the merchant-facing rate above Payrix’s wholesale cost and keeps the entire spread as embedded payment revenue. Larger partners in low-risk verticals — B2B SaaS, healthcare billing, property management — historically negotiate the strongest terms.

The structure rewards ISVs willing to commit volume and run a real PFaaS operation. The trade-off is opacity for teams that want to model unit economics from a public pricing page. Our Payrix pricing breakdown walks through the lever set ISVs typically negotiate, including platform fees, residual splits, and chargeback handling.

Stax’s three published subscription tiers

Stax publishes three subscription tiers on its pricing page, set by annual processing volume:

- $99 per month for merchants processing up to $150K per year

- $139 per month for $150K to $250K per year

- $199+ per month for $250K and above (custom quotes for higher volumes)

On top of the subscription, every transaction carries a flat per-transaction fee — $0.08 for card-present (swiped, dipped, tapped) and $0.15 for card-not-present (keyed-in, online). The processing rate is direct-cost interchange with 0% markup. ACH costs 1% per transaction capped at $10. There are no batch fees, no early-termination fees, and a 30-day cancellation policy.

Stax Connect — the ISV partner program — wraps that pricing model in a revenue share for software companies. ISVs typically share in both the subscription revenue and the per-transaction cents that flow through their merchants. The ceiling on ISV economics is therefore tied to Stax’s flat pricing rather than to a markup the ISV controls. Our Stax pricing breakdown covers the merchant side; the partner economics are deal-by-deal and not publicly disclosed.

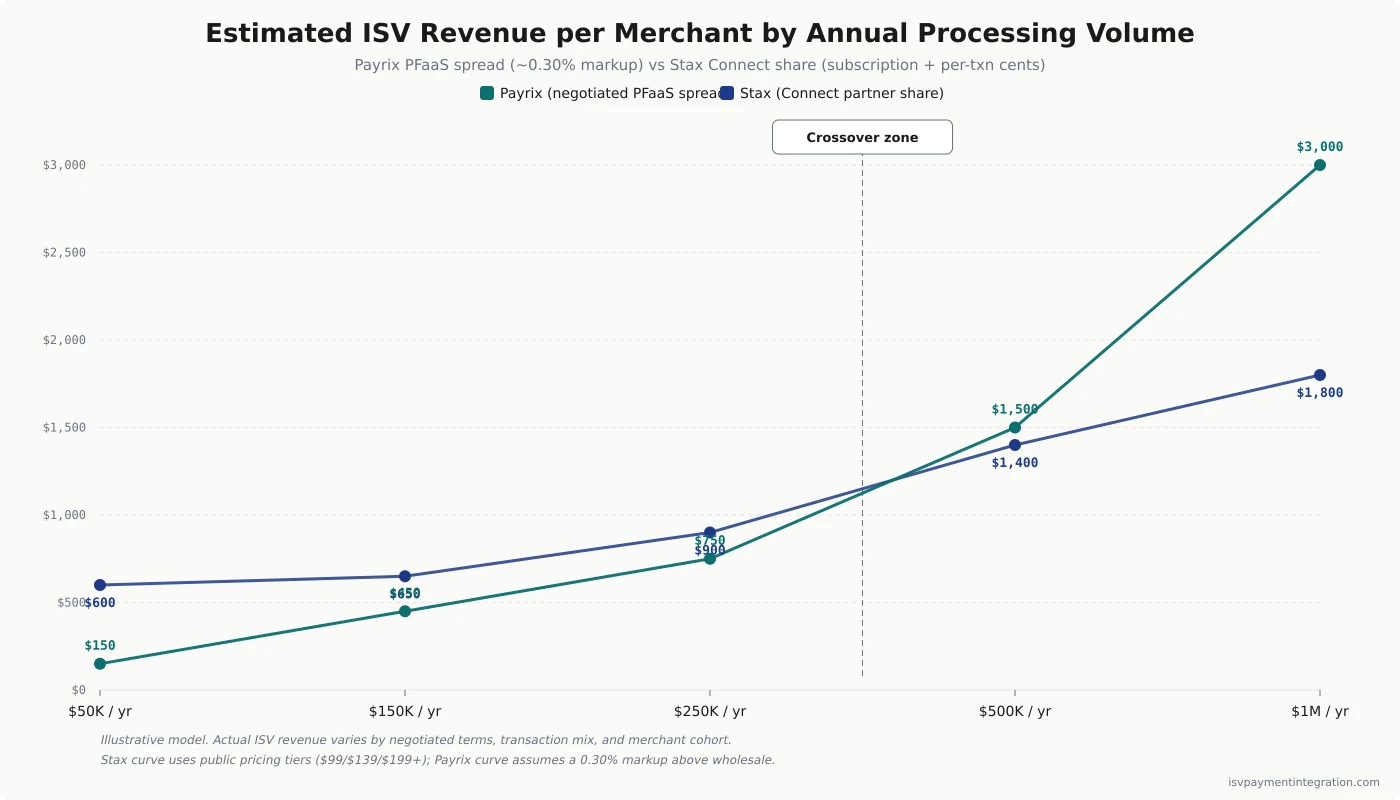

Volume economics: where the crossover happens

The cleanest way to evaluate Payrix vs Stax for an ISV is to model effective revenue per merchant across realistic volume tiers. Payrix’s economics scale with interchange-plus markup spread on merchant gross processing volume. Stax’s economics for the ISV partner scale with a slice of a fixed subscription plus per-transaction cents — a model that flattens at higher volumes.

For low-volume merchants — under roughly $150K per year per merchant — Stax’s $99-tier subscription delivers economics competitive with Payrix’s spread model, particularly because the merchant pays no percentage markup and the ISV captures a slice of the fixed subscription. As volume climbs into the $250K-plus range, Payrix’s percentage markup compounds in a way the Stax subscription cannot, since Stax’s pricing flattens into the third tier and beyond.

The inflection point depends on three variables: the markup the ISV negotiates with Payrix, the revenue-share percentage the ISV agrees with Stax Connect, and the merchant ARPU on processing. ISVs with high-volume, low-risk merchant cohorts — vertical SaaS in B2B, healthcare, or property management — generally find Payrix’s economics more attractive at scale. ISVs with broad SMB cohorts where merchants process under $150K annually often see Stax’s flat-subscription model produce a smoother per-merchant return.

Integration architecture: PFaaS infrastructure vs partner platform

The two platforms ask the ISV to take on very different operational roles, and that shapes the integration scope.

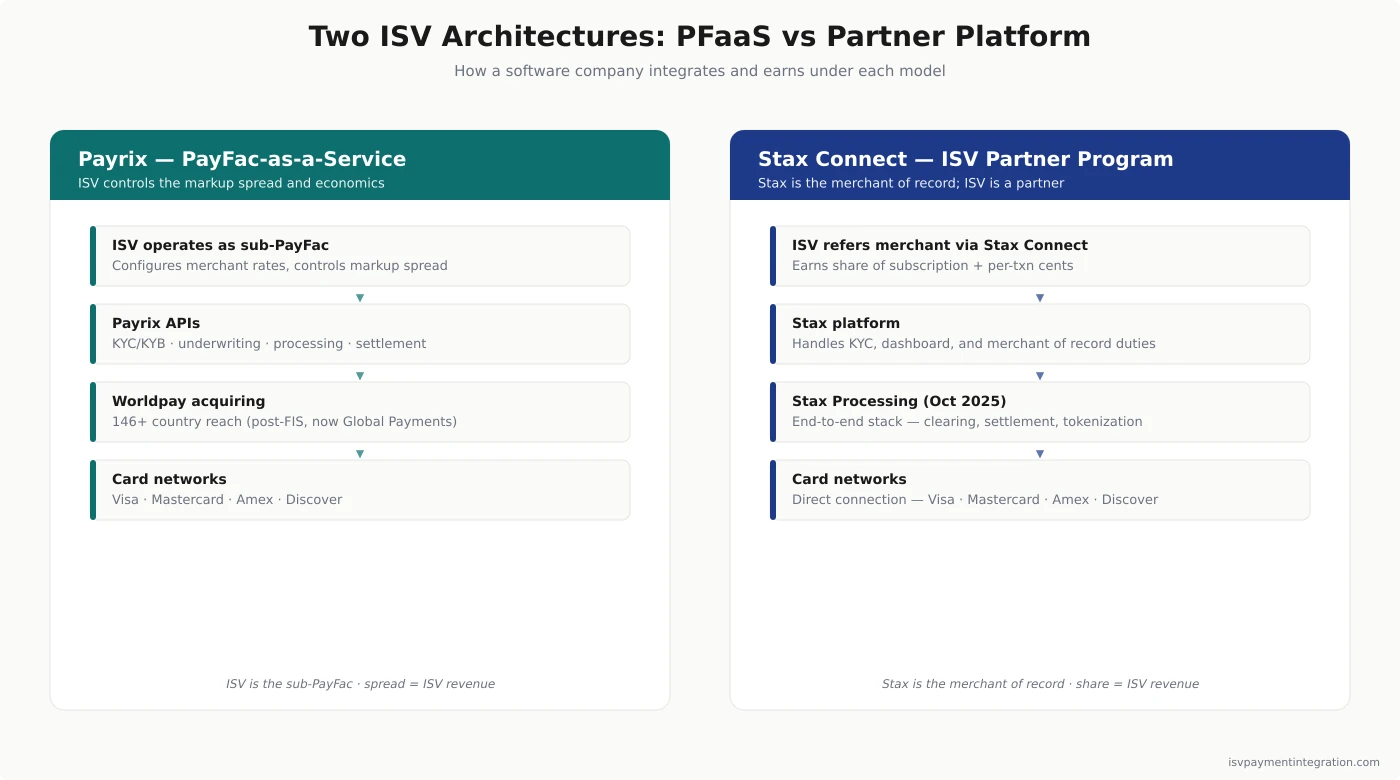

Payrix: the ISV becomes a PayFac

In the Payrix model, the ISV runs an operating model close to a registered payment facilitator. Payrix’s APIs cover sub-merchant onboarding, KYC and KYB checks, underwriting decisions, transaction processing, settlement, reporting, and dispute handling. The ISV configures merchant-facing rates, receives funds into platform accounts, and disburses to sub-merchants on a schedule the ISV controls. Worldpay for Platforms surfaces three engagement modes for ISVs: Integrated Referral Partnership (light-touch, low effort, capped revenue), Payrix Pro (PayFac-as-a-Service — the managed model, fastest time-to-market), and Payrix Premium (full PayFac® infrastructure for ISVs that hold or plan to hold their own PayFac license). The integration surface is large because the ISV is taking on a real PayFac’s operational scope. Storable, the multi-vertical SaaS platform, publicly reported moving from a 31-day average merchant onboarding window with their previous vendor to under 3 days on Payrix after consolidating 15-plus integrations into one stack.

Stax: the ISV partners with a merchant platform

Stax Connect is structured differently. The ISV refers merchants into Stax, embeds Stax’s checkout and dashboard surfaces under partial co-branding, and earns a slice of subscription and transaction revenue. Stax handles merchant of record duties — onboarding, KYC, settlement, and disputes — directly, with adoption experts handling implementation alongside the ISV’s team. Since the October 2025 Stax Processing launch, that lifecycle runs end-to-end on Stax’s own infrastructure rather than through a third-party acquirer. The integration surface is smaller because the ISV is not running a PayFac operation; the ISV is a referral and embedding partner with deeper-than-affiliate hooks.

Stax also offers Stax Connect Plus — a managed-sales overlay where Stax’s own sales team sells, activates, and onboards merchants on the ISV’s behalf. The pitch addresses a chronic problem in vertical SaaS: ISV-resold payments routinely sit at 10–30% adoption while pure referral partnerships hit 50–90%. Fishbowl Inventory, an early Stax Connect Plus customer, publicly reported a 36% increase in onboarded merchant IDs, a 25% increase in active processing IDs, a 93% lift in revenue from onboarded merchants, and a 112% lift in total processing volume after rolling onto the program.

For a deeper architectural view of the PayFac side, our embedded payments for ISVs and white-label payment processing for ISVs breakdowns walk through the building blocks each model exposes.

Developer experience: APIs, sandbox, docs

Payrix’s REST API has been around since the original 2015 platform launch and shows its age in places. Documentation covers the full PFaaS lifecycle — sub-merchant onboarding through underwriting through settlement — but the API design predates more recent entrants like Tilled and Finix. Engineering teams accustomed to Stripe-quality DX often note that Payrix’s sandbox flow and developer onboarding feel more procedural than self-serve. The trade-off is breadth: Payrix’s APIs cover a true PFaaS scope that newer providers don’t expose.

Stax Connect has a leaner integration surface because the ISV is not operating as a PayFac. The Stax API covers payment processing, recurring billing through Stax Bill, customer and invoice management, and tokenized card handling. The smaller scope tends to mean shorter integration windows for ISVs with lean engineering teams. Stax’s API documentation is publicly accessible and covers the Stax Pay and Stax Connect surfaces.

A practical heuristic: a two-engineer team that wants to ship in weeks rather than months will move faster on Stax Connect. A larger team that needs to control merchant-level economics, operate a real PFaaS, and run vertical-specific compliance flows will use Payrix’s full surface and build on it.

White-label and merchant-facing brand control

Payrix’s white-label scope is among the strongest in the PFaaS market. Sub-merchant onboarding, transaction dashboards, dispute management, and reporting can run entirely under the ISV’s brand. Merchants experience the ISV as their payment provider; Payrix and Worldpay sit invisibly in the technical and regulatory layers underneath. That control is a meaningful asset for ISVs whose merchant-facing brand carries equity.

Stax Connect is co-brandable rather than fully white-label. ISVs can customize merchant-facing surfaces — checkout, dashboards, communications — but the Stax identity remains visible in the platform’s contracts, statements, and certain user flows. For ISVs where merchant relationships need to feel like a single-vendor experience, the trade-off is real. For ISVs comfortable presenting Stax as a named processing partner, the simpler integration is often a better fit.

Verticals where each platform wins

Payrix has historically concentrated on verticals where integrated payments for SaaS generate strong unit economics: property management (Storable, ResMan), nonprofit (Neon One), lawn care and field services (Real Green), healthcare (patient payments, copays, billing integration), and fitness and wellness (membership billing, class bookings, retail POS). The product carries pre-built compliance workflows, vertical-specific underwriting rules, and risk models tuned to those industries.

Stax markets dedicated Stax Connect verticals across field service software (Sera publicly reported a 52% revenue lift among its merchants within six months on Stax), SaaS accounting, healthcare, legal and professional services, retail, and surcharging-driven merchants through CardX. The flat-subscription economics make Stax a natural fit for businesses with high-frequency, low-ticket transactions where percentage markup pricing penalizes volume. As a scale benchmark, Stax processes roughly $23 billion annually across more than 39,000 businesses and software platforms — meaningfully smaller than Worldpay’s footprint but firmly past the early-stage tier.

Healthcare and field services are the meaningful crossover verticals. Both platforms have credible offerings; the choice often comes down to merchant size, geographic exposure, and whether the ISV needs a true PFaaS operation or a referral-and-revenue-share partner.

Geographic reach and cross-border processing

Payrix processes through Worldpay’s acquiring network, which extends across 174 countries with Worldpay handling more than 50 billion transactions per year. The platform-specific Worldpay for Platforms product expanded into Canada, the United Kingdom, and Australia in July 2025, with CampLife (an accommodation and camping vertical SaaS) named as the first Canadian customer. Post-January-2026, Global Payments’ international footprint layers on top of that.

Stax is effectively US-focused. The company describes itself as serving merchants “across the U.S. and Canada,” and recent press materials point to limited Canadian coverage, but the operational stack (bank partners, certifications, ISV partner deals) is overwhelmingly US-centric. There has been no European, UK, or APAC expansion through 2025–2026. Any ISV with a meaningful share of merchants outside North America will run into structural constraints with Stax Connect that Payrix does not have. ISVs evaluating both should be honest about their five-year merchant geography roadmap before signing.

Compliance burden: what each platform lifts off the ISV

Payrix is a true PFaaS, which means the platform absorbs PCI Level 1 acquiring, card brand registration, sponsor bank relationships, KYC and KYB compliance, AML monitoring, and risk model operations. The ISV operates as a sub-PayFac under Payrix’s umbrella — meaningful compliance work still exists at the ISV layer (sub-merchant due diligence, dispute management at the platform level, monitoring partner-level fraud), but the foundational regulatory work is Payrix’s. This is the core value of payment facilitation for software companies.

Stax handles PCI compliance at the platform level and sits as the merchant of record for every transaction processed through the platform. The ISV inherits a lighter compliance burden because the ISV is not a PayFac in any form — Stax is. The trade-off is operational distance: Stax owns the merchant relationship in regulatory terms, and decisions about merchant offboarding, risk holds, or fund holds sit with Stax rather than the ISV.

Support models and partnership economics

Payrix runs a relationship-driven support model for ISV partners. Solution engineering teams are assigned to integrations, and partner success managers handle the ongoing relationship. The model works well for mid-market ISVs with complex requirements; it can feel slower for early-stage software companies that prefer a self-serve developer experience.

Stax’s adoption-experts model layers in-house specialists onto every Stax Connect partnership, handling implementation, go-to-market positioning, and ongoing optimization. The structure has been a Stax differentiator since the Stax Connect launch and is one of the reasons Stax often wins against more developer-centric rivals on services-heavy ISV deals.

For a small ISV with a lean engineering team, Stax’s hands-on adoption flow tends to produce faster time-to-revenue. For a mid-market or enterprise ISV with the in-house technical scale to run a PFaaS, Payrix’s solution engineering depth compounds across the partnership lifecycle.

The “acquirer-owned vs PE-independent” question

This is the corporate-risk question that often dominates the final decision, and it has changed shape in 2026.

Payrix is now part of Global Payments’ Worldpay for Platforms unit following the January 2026 close. Global Payments brings massive scale, a public balance sheet, and a roadmap shaped by the realities of integrating two of the largest acquirers in the industry. The advantages: stability, infrastructure depth, international reach, and a parent company that needs the ISV channel to perform. The risk: Global Payments has telegraphed roughly $600M in cost synergies from the Worldpay acquisition, with about a third coming from rationalizing the combined tech stack and “duplicative vendor and software expenses.” For ISVs signing multi-year embedded-payments contracts in 2026, that is the signal to negotiate platform-stability and roadmap-commitment language directly into the master agreement. The first 18 to 24 months after a deal of this size historically include product reorgs, partner-economics reviews, and roadmap pauses while the combined entity rationalizes its product portfolio.

Stax is privately held by Greater Sum Ventures, with a freshly appointed CEO who came directly from the parent fund. The advantages: focused product leadership, faster decision cycles, and an ownership structure that has visibly invested in payments adjacencies. The risk: PE-backed companies with new C-suites operate under acquisition pressure on a 3-to-5-year horizon. ISVs signing long-term deals with Stax should ask the same portability and termination questions any prudent partnership demands. A useful operator data point: in early 2026, the r/ChargeForward community surfaced research from the Rainforest Vertex 2026 conference indicating that 92% of ISV operators reported at least one significant challenge with their payments provider, and 55% cited “limited product roadmap” as the top complaint — a reminder that platform-roadmap risk applies to both an acquirer-owned PayFac and a PE-owned independent. For comparison, our Stax vs Tilled and Stax vs Fiserv breakdowns show how Stax’s positioning shifts against different ownership structures.

How to choose: a decision guide for ISVs

The decision is rarely close once an ISV is honest about its merchant cohort, engineering scale, and five-year geography roadmap.

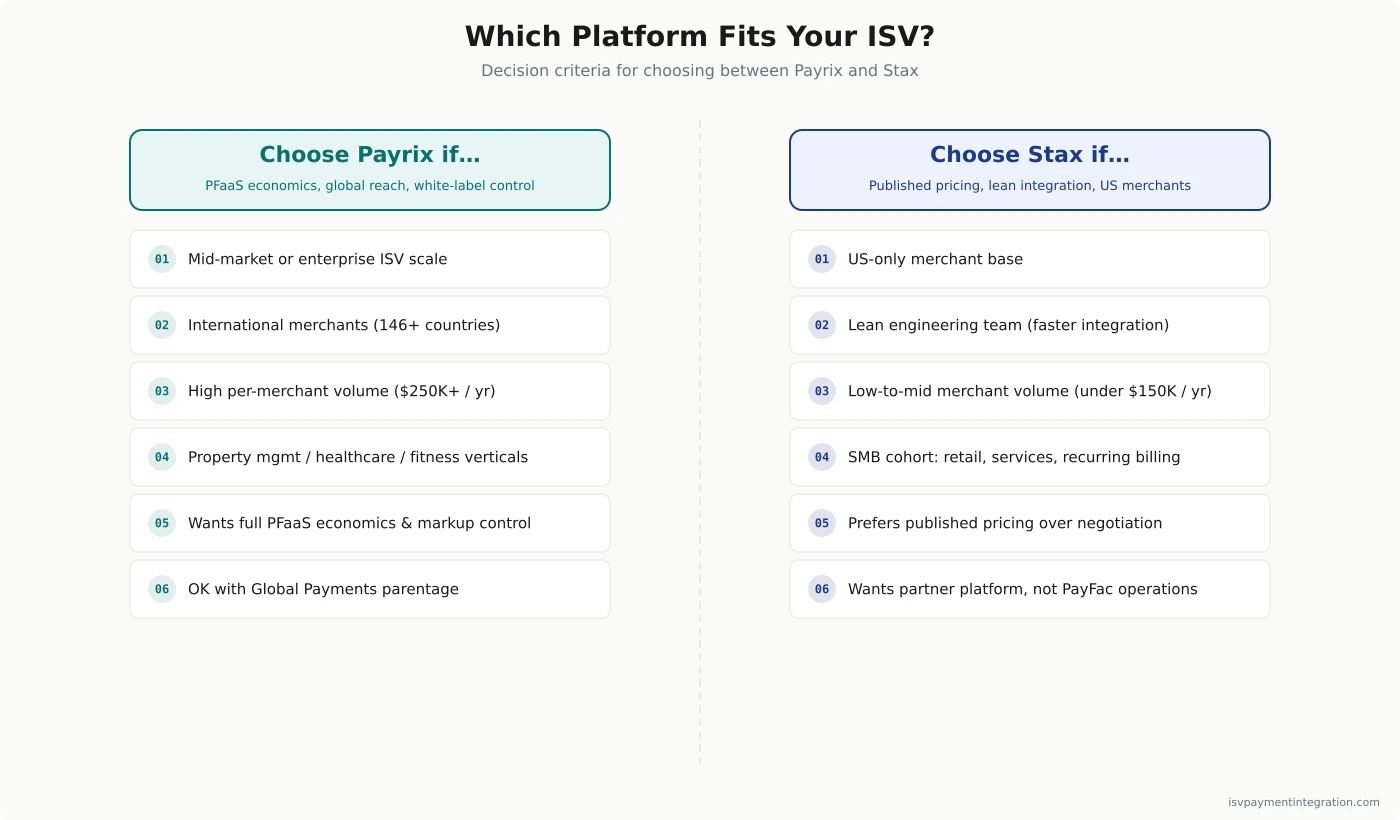

Choose Payrix if: the ISV operates in property management, healthcare, fitness, field services, nonprofit, or any vertical with meaningful card-present or recurring volume; merchant volume justifies PFaaS economics ($250K+ per merchant per year on average); the engineering team can carry a real PFaaS integration; international merchants are part of the roadmap; full white-label brand control matters; the ISV is comfortable with Global Payments parentage.

Choose Stax if: the ISV’s merchants are US-based; merchant volume per merchant sits under $150K per year for a meaningful share of the cohort; the engineering team prefers a leaner integration surface; subscription billing through Stax Bill maps to the merchant base; published pricing matters more than negotiated economics; partnering with a platform feels operationally cleaner than running as a PayFac.

For ISVs caught between the two profiles, the right move is usually to model the unit economics on actual merchant data — average GPV, transaction mix, vertical risk — and compare effective revenue per merchant across both platforms over a three-year horizon. Both Payrix and Stax sales teams will provide realistic terms once an ISV brings concrete volume forecasts and a credible go-to-market plan. One operator-side note worth internalizing: in the same Rainforest Vertex 2026 research cited earlier, ISVs with a dedicated C-suite payments leader reported median take rates roughly twice those without one. The choice of platform matters less than whether the ISV staffs a payments leader to negotiate, monitor, and renegotiate the relationship. Adjacent comparisons worth running before finalizing: Payrix vs Tilled, Square vs Payrix, and Stax vs Fiserv. Talk to a payments specialist for a second opinion on volume and merchant fit.

Frequently Asked Questions

Is Payrix still independent in 2026?

No. FIS — Worldpay’s parent — acquired Payrix in February 2022 and folded the platform into Worldpay for Platforms by September of that year. In January 2026, Global Payments closed its $24.25B acquisition of Worldpay, moving Payrix into the combined Global Payments and Worldpay entity. Existing Payrix integrations continue to operate, but pricing, roadmap, and partner-economics decisions now route through Worldpay for Platforms and on to Global Payments. ISVs evaluating Payrix today are signing into a top-tier processor with a recently merged corporate parent.

Who owns Stax in 2026?

Stax is owned by Greater Sum Ventures, a Knoxville-based growth equity firm that completed its acquisition of Stax on December 1, 2020. Greater Sum Ventures’ portfolio companies collectively process more than $60 billion in payments annually. In February 2026, Stax appointed John Cimba as CEO; Cimba came directly from Greater Sum Ventures, where he had been an operating partner. The company also announced a refreshed C-suite in March 2026, with new chief commercial, chief operating, and chief technology officers. Stax remains privately held.

Can either platform process internationally for an ISV’s merchants?

Payrix processes through Worldpay’s acquiring network, which spans 146+ countries — and Global Payments’ parentage extends international rails further. ISVs with Canadian, UK, EU, or APAC merchants have a structural advantage with Payrix. Stax is US-only with no announced international expansion through 2025–2026; Stax’s bank partners are all domestic. Any ISV whose merchant base includes meaningful share outside the US should treat geographic reach as a deal-breaker variable in the comparison.

What does Stax actually cost per merchant in 2026?

Stax publishes three subscription tiers on its pricing page: $99 per month for merchants processing up to $150K per year, $139 per month for $150K to $250K per year, and $199+ per month for $250K and above (with custom quotes at higher volumes). On top of the subscription, every transaction carries $0.08 for card-present and $0.15 for card-not-present. Processing happens at 0% markup on direct-cost interchange. ACH costs 1% per transaction capped at $10. Optional add-ons include chargeback protection at $25 per dispute. There are no batch fees, no early-termination fees, and a 30-day cancellation policy.

Which platform offers a better revenue share for ISVs?

The honest answer is that it depends on volume and business model. Payrix gives ISVs the full markup spread above interchange-plus, which compounds as merchant volume scales — at $250K-plus per merchant per year, the spread economics typically beat Stax Connect’s flat-subscription revenue share. Stax Connect partners earn a slice of subscription revenue plus per-transaction cents; the ceiling is shaped by Stax’s flat pricing rather than a markup the ISV controls. For low-volume cohorts where merchants process under $150K per year, Stax’s economics often hold up well; for higher-volume cohorts in low-risk verticals, Payrix’s PFaaS spread typically wins.