Stax vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Line up Stax and Fiserv and the disagreement runs deeper than any feature grid: the two companies price a card payment in opposite ways. Stax sells acceptance like a membership — a flat monthly subscription, a few cents per transaction, and interchange passed straight through at cost with no percentage markup. Fiserv sells it like a percentage — a negotiated residual folded into a blended rate the merchant never sees itemized. A software platform embedding payments is really choosing which of those two pricing philosophies it wants to build its own economics on top of.

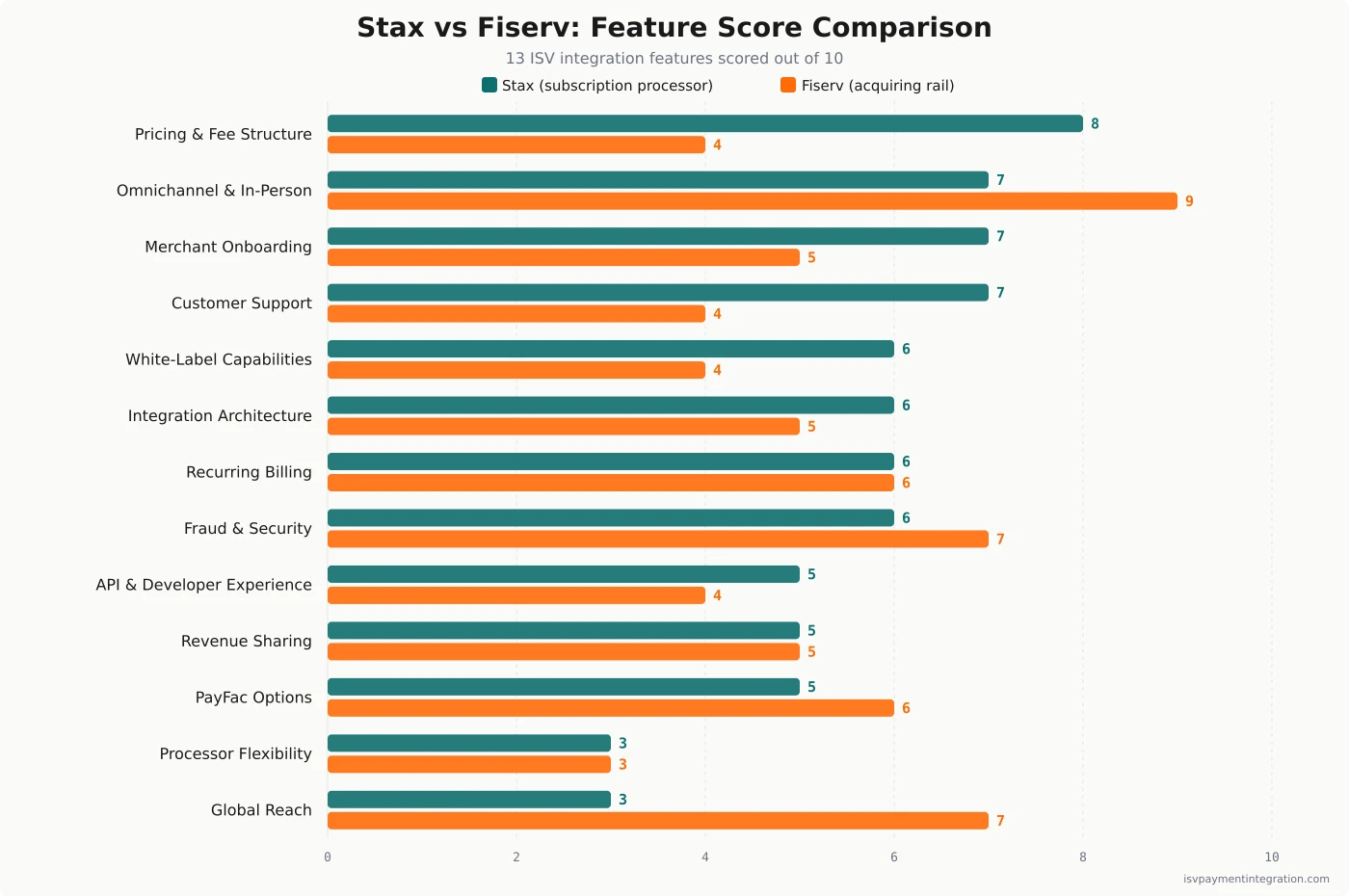

Feature Comparison

| Feature | Stax | Fiserv |

|---|---|---|

| Integration Architecture | 6 | 5 |

| API & Developer Experience | 5 | 4 |

| White-Label Capabilities | 6 | 4 |

| Processor Flexibility | 3 | 3 |

| Pricing & Fee Structure | 8 | 4 |

| Omnichannel & In-Person Payments | 7 | 9 |

| Fraud & Security | 6 | 7 |

| Revenue Sharing | 5 | 5 |

| Merchant Onboarding | 7 | 5 |

| Global Reach | 3 | 7 |

| Recurring Billing | 6 | 6 |

| Customer Support | 7 | 4 |

| PayFac Options | 5 | 6 |

Get this comparison as a shareable PDF

We'll send the Stax vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Stax

Best for ISVs whose merchants clear roughly six figures a year in card volume, where a flat monthly subscription and interchange at cost compound into real savings, and that sell into verticals — field services, professional services, healthcare, education, non-profit — where transparent, itemized pricing is itself a selling point. Accept that below the volume breakeven a percentage model is cheaper, and that Stax is a US-focused, mid-market processor rather than a global one.

Best for

Fiserv

Best for platforms that need the world's largest merchant acquirer, the Clover point-of-sale ecosystem, and the underwriting reach of a seven-bank sponsor roster, and whose merchants are small-ticket, highly varied, or counter-based. Less ideal for platforms whose pitch to merchants is radical pricing transparency, or whose high-volume merchants would plainly benefit from interchange at cost.

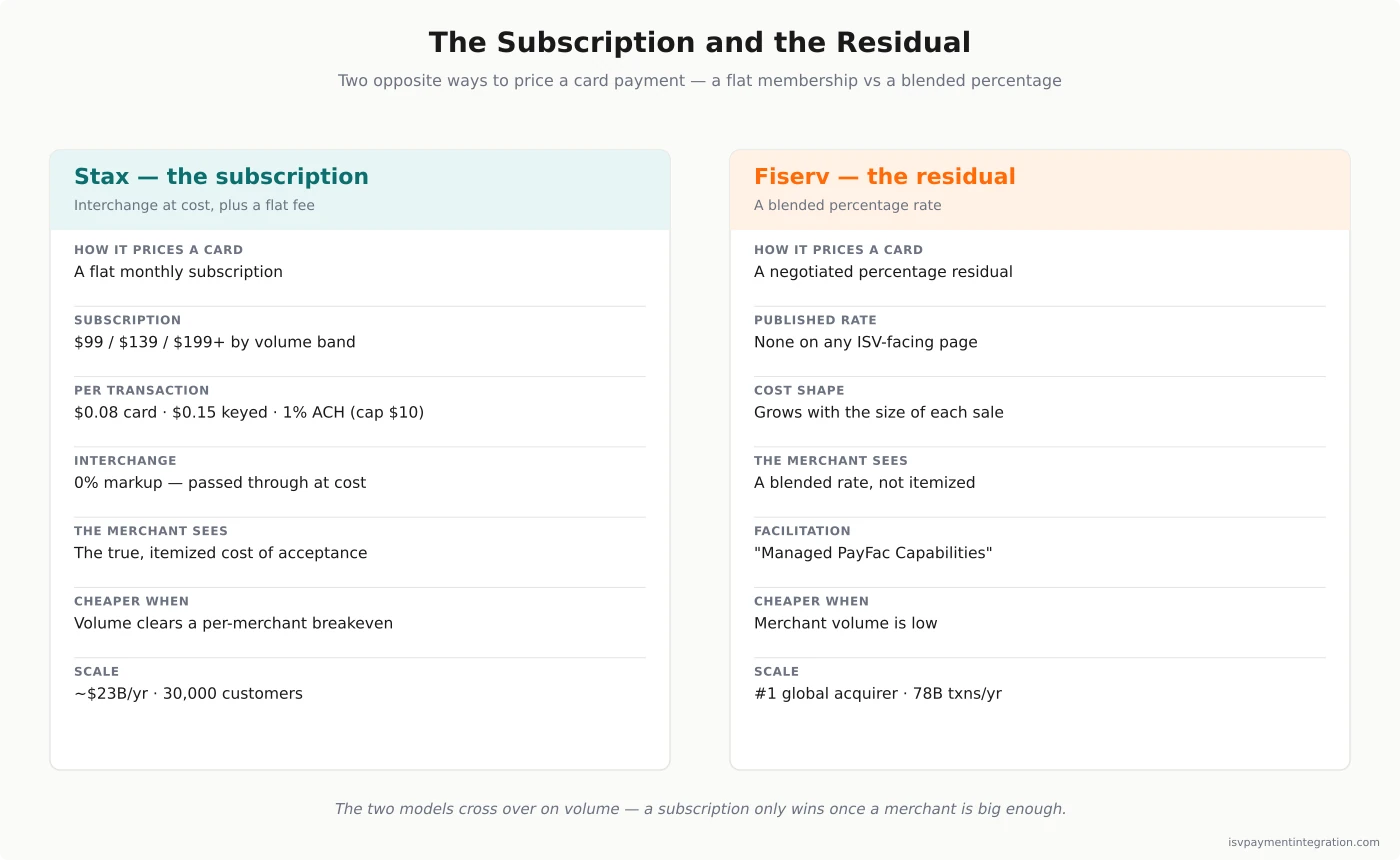

Stax vs Fiserv: The Subscription and the Residual

Most head-to-heads between these two get lost in feature tables, and the tables bury the one difference that actually decides the choice: Stax and Fiserv do not price a card payment the same way, and they do not even agree on whether the merchant should see what a card payment costs. Stax prices acceptance the way a warehouse club prices groceries — you pay a flat membership, and the goods pass through at cost. Its published model is a monthly subscription set by processing volume, a few cents per transaction, and, in its own words, “0% markup on interchange.” Fiserv prices acceptance the way almost everyone else in payments does — as a percentage, a negotiated residual folded into a blended rate, with no processing number published anywhere on its ISV-facing pages.

For a software platform building payments into its product, that is not a detail. The model you adopt from your processor sets the cost base your own payments margin is built on — and, if you pass it through the way many platforms do, the pricing your merchants see too. You can repackage it, of course; a platform is free to wrap either model in its own flat SaaS-plus-payments bundle. But the underlying economics you inherit are near-opposites, and they behave differently as your merchants grow. One puts the cost of a card on a meter; the other keeps it inside a markup.

Quick Take: A Membership Model and a Blended Rate

Stax is a subscription-pricing processor. Its direct product, Stax Pay, publishes the whole schedule: a monthly subscription that steps with annual volume — $99/month up to $150,000 a year, $139/month from $150,000 to $250,000, and $199+/month above $250,000 — plus flat per-transaction fees of $0.08 for card-present, $0.15 for keyed or online, and 1% capped at $10 for ACH. On top of that sits the defining promise: “0% markup on direct-cost interchange … With Stax Pay, you keep more of every transaction.” The ISV arm is Stax Connect, a partner program whose Stax Connect Plus tier will run the payments customer journey — onboarding, support, the operational lift — for the software company. Across the whole business Stax reports it processes about $23 billion a year for more than 30,000 customers with 150+ integrated software partners.

Fiserv courts software platforms through its ISV Partner Program, whose three verbs its page states plainly — Integrate, Monetize, Grow — and whose proof points are all acquiring scale: the #1 global merchant acquirer, 78 billion merchant transactions a year, nearly 100% of U.S. households reached. The acceptance gateway is CardPointe, CoPilot manages the partner’s portfolio, Clover is the point-of-sale ecosystem, and the program advertises “Managed PayFac Capabilities.” What it does not do, anywhere on those pages, is quote a rate. The number a platform will actually pay — and the residual it will actually earn — arrives through a sales conversation, priced as a percentage, not a subscription.

Interchange at Cost vs the Markup

The cleanest way to see the gap is to trace a single card sale through each model. Under Stax, the interchange set by the card networks passes to the merchant at cost, Stax adds its flat per-transaction fee, and its own compensation lives almost entirely in the monthly subscription — a fixed lump the merchant still has to spread across its own volume to know its true per-transaction cost, but a lump that does not grow with the sale. Because Stax deliberately does not layer a percentage on top of interchange, the network’s cost and Stax’s fee stay separable on the statement.

Under Fiserv, the same sale is priced with a percentage markup, and here it is worth being fair rather than tidy. For a larger platform that markup may be interchange-plus, which itemizes the network’s cost and states the markup on top — as legible, in that form, as Stax’s own statement. For a smaller merchant it is more often a bundled or tiered rate, where the pieces disappear into one blended number; either way, the markup is never published on Fiserv’s ISV pages in advance. So the honest contrast is not simply transparent-versus-opaque, because interchange-plus is itemized too. It is a fixed subscription with zero markup on interchange against a percentage markup — however that markup is disclosed — a cost that climbs with the size of each sale rather than holding flat.

The consequence for the merchant is a crossover. A percentage is cheaper when volume is low, because a fixed subscription has nothing to amortize against; a subscription-plus-cost model is cheaper when volume is high, because the percentage the merchant would otherwise pay keeps climbing while Stax’s monthly fee does not. Which side of that line a merchant sits on is the whole question, and it is why this comparison cannot be settled in the abstract.

The Breakeven That Decides It

Because the models cross over, the honest version of “which is cheaper” is always “it depends” — and any page that tells you Stax is simply cheaper is selling you something. A flat subscription only pays for itself once the percentage it replaces would have cost more than the subscription plus the per-transaction cents — which means the exact crossover depends on the very Fiserv markup that is never published, so no one can name it precisely from the outside. The sensitivity is real: assume a markup around a third of a percent and the entry-tier subscription only breaks even up in the mid-six-figures of annual volume; assume half a percent and it breaks even a good deal sooner. What does not move with the assumption is the direction. Because Stax’s monthly fee is fixed while a percentage keeps climbing with every dollar of volume, the subscription structurally favors larger merchants and the percentage favors smaller ones. Stax is a higher-volume instrument — not because its own price sheet declares it, but because that is simply what a flat fee does when set against a percentage.

One thing can flip even that direction, and it deserves naming because both companies enable it: surcharging and cash-discount programs, where the merchant passes the cost of card acceptance to the cardholder. When a merchant surcharges, the percentage is handed to the customer and largely leaves the merchant’s own books — which quietly removes the “cost that scales with the sale” a subscription is meant to beat. A fixed monthly subscription, by contrast, is not a per-swipe line a merchant can pass through as cleanly, so for a fee-passing merchant the flat fee can be the harder cost to zero out. If your merchants surcharge, run the comparison again with that in mind, because it does not automatically favor the subscription.

That single fact should govern the decision more than any feature score, and for an ISV it is not really a fact about individual merchants — it is a fact about your book. Whichever model you adopt from your processor is the one you hand to every merchant you onboard, so you are betting the shape of your whole portfolio on one side of the crossover. A platform whose merchants skew small — low-ticket, seasonal, just getting started — will make much of its book worse off on Stax’s subscription, and a percentage processor like Fiserv is the kinder default there. A platform whose merchants skew established and volume-heavy leaves money on the table by keeping them on a percentage when interchange-at-cost was on the table. The pricing model is not better or worse in the abstract; it is a bet on the size of the merchants you intend to serve, made once and inherited by all of them.

What This Means for the ISV’s Revenue

Follow the money to the software platform’s own line and the two models shape the ISV’s economics differently. A platform earns on embedded payments from the spread between what its merchants pay and what its processor charges — but the raw material of that spread is different in each case.

With Stax Connect, the platform is layering its economics on a subscription-and-cost base. The revenue share is negotiated — Stax publishes no ISV rate, and its Connect Plus results are quoted as case-study lifts (a Fishbowl program reported a 93% revenue increase from onboarded merchants) rather than a rate card — but the underlying model the ISV inherits is transparent and predictable, and it comes with Stax’s team running onboarding and support. That is a strong fit for a vertical-SaaS company that wants payments revenue without building a payments operation, and whose merchants are the kind of established businesses where interchange-at-cost lands well.

With Fiserv, the platform earns a residual on a percentage, negotiated against the largest acquirer in the world. There is no published tier or figure either — both companies gate the ISV number — but the raw material is a percentage of volume rather than a subscription, and the platform with real scale can negotiate hard against Fiserv’s balance sheet. The trade is opacity and a longer sales cycle in exchange for reach and underwriting muscle Stax cannot match. Neither publishes what you will earn; the difference is the shape of what you are earning on.

Who Each One Is Built For

Strip away the pricing mechanics and the two companies are aimed at different platforms. Stax’s named verticals are telling: its Connect materials point at field services, professional services, healthcare, education and non-profit, and its named case studies — Sera and ClientTether — cluster there. That is deliberate. A subscription model with interchange-at-cost is easiest to sell into verticals where merchants are established, volumes are respectable, and a transparent statement is a competitive weapon against incumbent processors. Stax is a focused, US, mid-market platform, and it is good at being one.

Fiserv is built for breadth. Its whole pitch is that it is the largest acquiring rail on earth, that it reaches nearly every U.S. household, and that through Clover it can put a hardware operating system on any counter. A platform serving a huge, heterogeneous, small-ticket or counter-attached merchant base — restaurants, retail, the long tail — is exactly what Fiserv’s scale, underwriting reach and hardware ecosystem are designed to absorb. Where Stax says “we make acceptance transparent for serious merchants in a few verticals,” Fiserv says “we can process almost anything, almost anywhere.” Both are honest claims. They just describe different platforms.

Where Fiserv Outweighs Stax

It would misfit a reader to leave the impression that transparency settles everything, because on raw capability Fiserv is the heavier platform by a wide margin. It is the world’s number-one merchant acquirer, clearing 78 billion transactions a year; Stax reports roughly $23 billion in annual card volume. The figures are in different units, but the weight classes are not close. Fiserv’s international acquiring reaches markets a US-domestic processor simply does not serve. At the counter, Clover’s hardware ecosystem operates at a scale Stax’s terminal lineup does not approach. And the sponsor-bank distribution behind First Data Merchant Services is the kind of banking reach that took decades to assemble.

There is one more concession an ISV should weigh, and it is the one most comparisons skip: counterparty durability. Fiserv is a public company and one of the oldest, largest acquirers in the world; Stax is a far smaller, privately held processor that has been through rebranding and ownership changes. When you are, in this page’s own words, betting the shape of your whole portfolio on a processor, the odds that it will still be there — with the same roadmap, the same pricing, the same team — in five years is a real input, and it favors the incumbent. Stax’s model can be the better economic fit and Fiserv can still be the safer institutional bet; a serious platform weighs both.

For a platform whose merchants are global, or overwhelmingly counter-based, or so varied that no single vertical playbook fits, that scale is the deciding factor and Stax’s elegant pricing is beside the point. Transparency is worth a great deal when a merchant is big enough to benefit from it; it is worth less than raw acceptance reach when the merchant base is small, scattered, or international. Match the platform to the merchants, not to the prettier pricing page.

The Rail Underneath Both

One symmetry is worth stating plainly, because it punctures a tempting overclaim. Stax’s transparency does not mean Stax owns the rail. Its own footer discloses that Stax Payments is a registered ISO/MSP in association with Fifth Third Bank and Pinnacle Bank dba Synovus Bank, and a registered partner/ISO of Elavon — so, like almost every non-bank processor, Stax runs on sponsor banks it does not own. Fiserv sits on its own, larger roster: First Data Merchant Services is disclosed as a registered ISO of seven banks, while the CardConnect door names five. The difference is the breadth of the banking distribution, not that one company has escaped bank sponsorship and the other has not.

One more clarification keeps the transparency claim precise, because it is easy to overstate. Stax’s openness is about the merchant’s price, not the ISV’s. Its subscription tiers and 0% interchange markup are posted for any merchant to read, and that merchant-facing legibility is exactly what this whole comparison turns on — it is the thing a software platform can point a prospect at. The Stax Connect revenue share a platform negotiates for itself is a separate matter, and it is no more public than Fiserv’s residual; a platform should not expect a posted partner rate from either. But that shared silence at the partner layer is not the interesting axis here. The interesting axis is upstream of it: Stax’s subscription puts no markup on interchange at all, while Fiserv’s margin is a percentage — itemized as interchange-plus for the largest platforms, blended out of sight for everyone else. Read the Stax pricing breakdown and the Fiserv pricing breakdown together to see exactly where each one opens its books.

Choosing by Merchant Economics, Not Brand

The reframe that makes this decision clean is to stop asking which processor is better and start asking which pricing model fits the merchants you actually serve. Because the two models cross over on volume, the answer is not a matter of taste — it is a matter of your merchants’ size and your own positioning.

If your merchants are established, volume-heavy businesses in a focused vertical, and part of your pitch is that you make payments honest and legible, Stax is the model that fits. You inherit a subscription-and-interchange-at-cost base, lean on Stax Connect Plus to run the payments operation, and sell transparency as a feature. If your merchants are small, seasonal, wildly varied, or standing at a physical counter that needs a hardware operating system, Fiserv is the model that fits. You accept a percentage residual and an opaque, negotiated rate in exchange for the largest acquiring rail, Clover, and sponsor-bank reach. The mistake is to choose on brand or on a single feature and then discover the pricing model was wrong for your merchants all along — a subscription forced on tiny merchants, or a percentage forced on merchants who should have had interchange at cost. Decide the economics first. For nearby comparisons, Stripe vs Fiserv looks at an API-first acquirer that does put its platform economics in public, and Stax vs NMI sets this same subscription processor against a processor-agnostic gateway. Model your own merchants’ numbers with the revenue calculator, and read the full Stax review and Fiserv review for the ground-level detail.

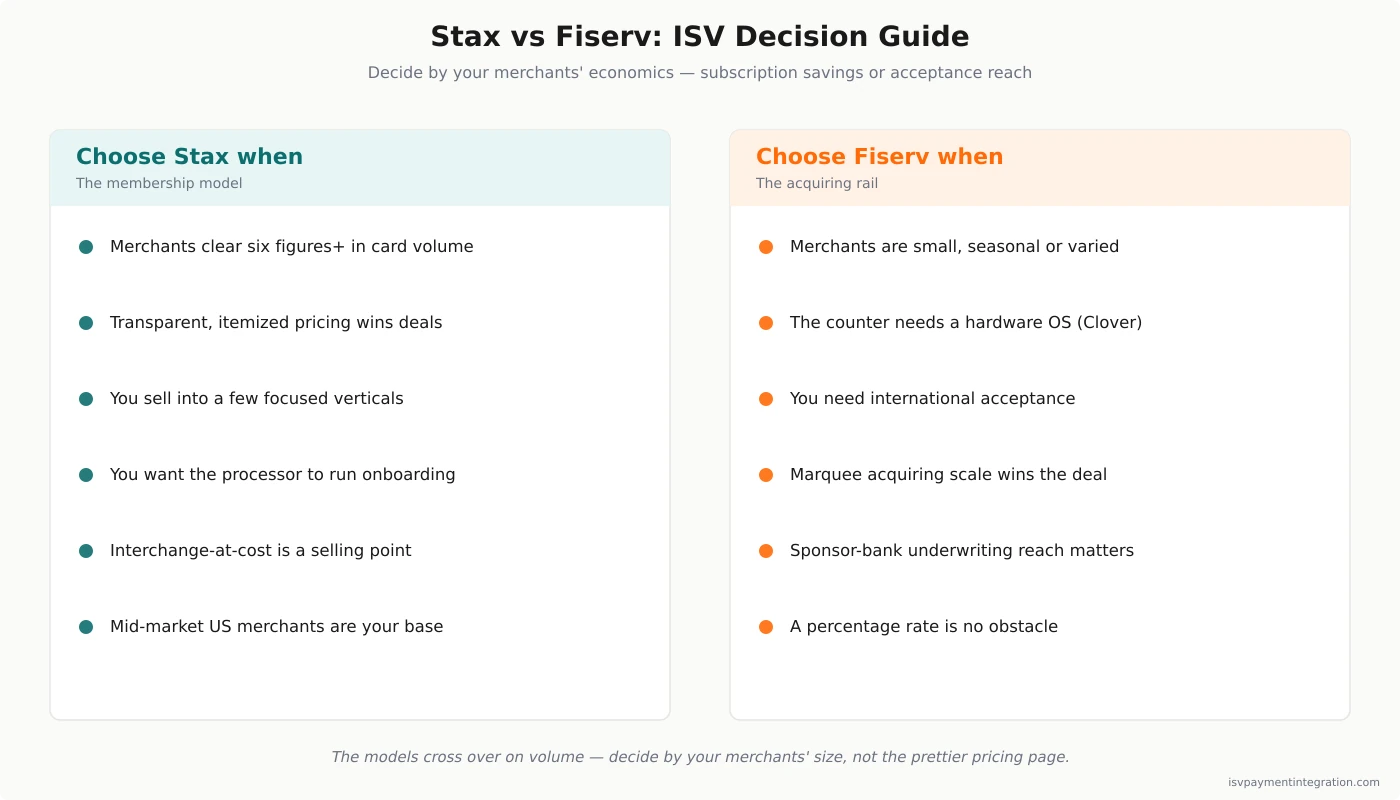

Stax vs Fiserv: ISV Decision Guide

- How much card volume do your typical merchants process? Well into six figures and up favors Stax’s subscription and interchange-at-cost; tens of thousands favors a percentage model like Fiserv’s, where there is no fixed fee to amortize.

- Is transparent, itemized pricing part of your pitch? If showing a merchant the true cost of acceptance wins deals for you, Stax’s 0% interchange markup is a feature; if your merchants don’t care how the sausage is priced, Fiserv’s blended rate is no obstacle.

- How focused is your vertical? Stax is strongest in field services, healthcare, professional services, education and non-profit; a wildly heterogeneous merchant base is more at home on Fiserv’s breadth.

- Do your merchants live behind a counter? When the hardware runs the day, Clover’s ecosystem tilts the decision to Fiserv regardless of pricing elegance.

- Do you need international acceptance? Stax is US-focused; cross-border acquiring is Fiserv’s ground, not Stax’s.

- Do you want the processor to run onboarding and support for you? Stax Connect Plus is built to manage that payments operation; Fiserv’s program leans on partner and bank channels.

- Which matters more, the best price for big merchants or acceptance reach for any merchant? Interchange-at-cost rewards volume in a few verticals; the largest acquiring rail absorbs almost any merchant, anywhere.

Frequently Asked Questions

How is Stax’s pricing actually different from Fiserv’s for an ISV’s merchants?

Stax prices acceptance as a subscription: a flat monthly fee that steps with annual volume ($99, $139, $199+), small per-transaction fees ($0.08 card-present, $0.15 keyed, 1% ACH capped at $10), and 0% markup on interchange, so the network’s cost passes to the merchant at cost. Fiserv prices it as a percentage — a negotiated residual blended into a rate that is not published on its ISV pages. The practical difference is where the processor’s margin lives: in a fixed subscription that stays flat as volume grows, or in a percentage that grows with every sale. For an ISV, that determines whether your merchants get cheaper or more expensive as they scale, and whether you can show them an itemized statement.

Is Stax always cheaper than Fiserv?

No, and it is important not to believe that. A subscription only beats a percentage above a breakeven volume — the point where the percentage a merchant would otherwise pay exceeds Stax’s monthly subscription plus its per-transaction cents. Below that volume, a percentage model like Fiserv’s is genuinely cheaper because there is no fixed fee to cover; above it, Stax’s interchange-at-cost compounds into savings. The crossover shifts with average ticket size and card mix, so the right answer depends on your specific merchants’ volume. A platform serving small or seasonal merchants can make them worse off by putting them on Stax; a platform serving established, high-volume merchants can overpay by keeping them on a percentage.

Does Stax own its own processing and bank, or does it rely on sponsors like Fiserv?

Stax runs on its own Stax Pay platform but it is not its own bank. Its footer discloses that Stax Payments is a registered ISO/MSP in association with Fifth Third Bank and Pinnacle Bank dba Synovus Bank, and a registered partner/ISO of Elavon — meaning it depends on sponsor banks for card-network access, exactly as most non-bank processors do. Fiserv is larger and sits on its own seven-bank roster through First Data Merchant Services (with the CardConnect door naming five), but the structural picture is the same: neither is an acquiring bank in its own right. The real difference is the breadth of banking distribution behind each, where Fiserv is far larger, not that one has escaped bank sponsorship.

Which is better for in-person and counter-based merchants?

Fiserv, when the counter is central. Clover is a countertop operating system — it rings up orders, runs the register and prints receipts — with an installed base and years of lead that Stax’s terminals do not match, and Fiserv settles the card behind it. Stax supports in-person acceptance and terminals through Stax Pay, and does it well for its mid-market base, but it is not a hardware ecosystem on Clover’s scale. If your software serves restaurants, retail or other counter-heavy businesses where the terminal is part of the product itself, Clover’s ecosystem is what tips the decision; if your merchants are service businesses that take payment by invoice, card-on-file or a single terminal, Stax’s model is a comfortable fit.

How does an ISV earn revenue on each platform?

On both, through a negotiated revenue share with no published rate — so the number requires a sales conversation either way. What differs is the base you are earning on. With Stax Connect, a software platform shares in economics built on a subscription-and-interchange-at-cost model, and Stax Connect Plus can run onboarding and support so the ISV doesn’t build a payments team; its case studies quote merchant-level lifts rather than a rate card. With Fiserv, the platform earns a residual on a percentage of volume through the ISV Partner Program’s “Monetize” track, negotiated against the largest acquirer in the world. Stax offers a transparent underlying model and a managed operation for a focused set of verticals; Fiserv offers scale and reach at the cost of an opaque, percentage-based rate.