Authorize.net vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Authorize.net is Visa's stable but aging US gateway — published rates, 430,000+ merchants, an XML-first API surface that Visa is modernizing carefully rather than rebuilding. Fiserv is the post-First Data merchant acquirer in turbulence: a $21B revenue base, six million merchant locations, and an active securities fraud class action over forced Clover migrations. Choose Authorize.net when pricing transparency and Visa-network stability matter more than ISV economics. Choose Fiserv (CardConnect for ISVs, Clover for POS) when scale, bank distribution, and interchange-plus negotiation outweigh Fiserv's product fragmentation and 2025 credibility hit.

Feature Comparison

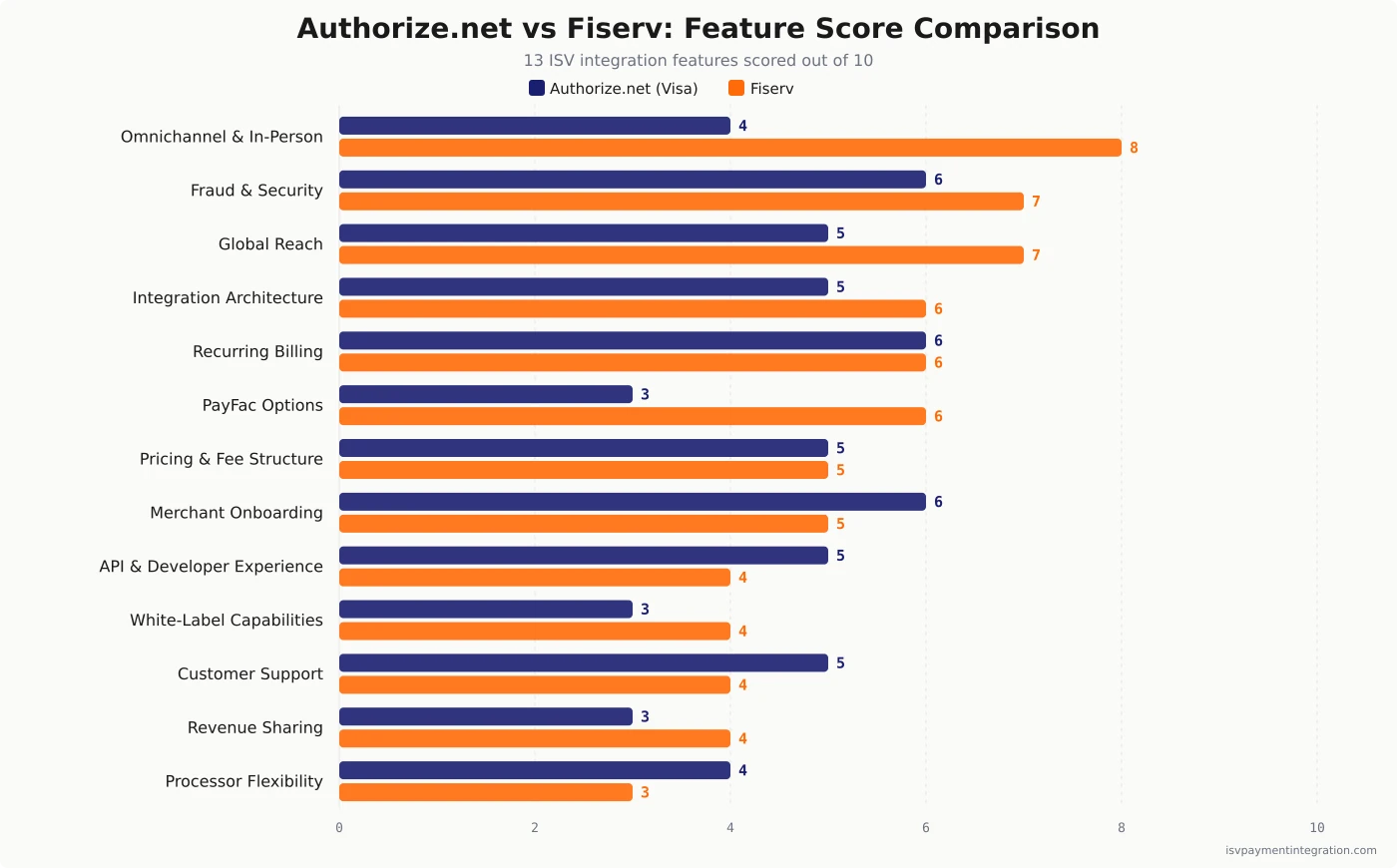

| Feature | Authorize.net | Fiserv |

|---|---|---|

| Integration Architecture | 5 | 6 |

| API & Developer Experience | 5 | 4 |

| White-Label Capabilities | 3 | 4 |

| Processor Flexibility | 4 | 3 |

| Pricing & Fee Structure | 5 | 5 |

| Omnichannel & In-Person Payments | 4 | 8 |

| Fraud & Security | 6 | 7 |

| Revenue Sharing | 3 | 4 |

| Merchant Onboarding | 6 | 5 |

| Global Reach | 5 | 7 |

| Recurring Billing | 6 | 6 |

| Customer Support | 5 | 4 |

| PayFac Options | 3 | 6 |

Get this comparison as a shareable PDF

We'll send the Authorize.net vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Authorize.net

ISVs that need predictable, published gateway pricing ($25/mo + $0.10/txn gateway-only or 2.9% + $0.30 all-in-one), strong Visa-network stability, and integration with merchants already on Authorize.net's 430,000-merchant footprint. Best for SaaS platforms that prefer a single, stable gateway over an integrated commerce stack.

Best for

Fiserv

ISVs that need Fiserv's bank-distribution scale, interchange-plus negotiation at high volume, and either CardConnect's PayFac-style boarding for embedded payments or Clover's POS ecosystem for vertical software (restaurant, retail, salon). Best for ISVs whose merchants benefit from a banking-grade processor relationship over Stripe-style developer ergonomics.

Authorize.net and Fiserv occupy two of the oldest seats in US payments — and the comparison most ISV teams need isn’t the comparison the SERP currently runs. Authorize.net is the Visa-owned legacy gateway with 430,000+ merchants, 3,000+ resellers, and an XML-first API surface that Visa is modernizing carefully rather than rebuilding from scratch. Fiserv is the post-First Data merchant acquirer — $21.19B in 2025 revenue, six million merchant locations, the parent of Clover, CardConnect, and Carat — and the defendant in an active securities fraud class action over forced Clover migrations. For deeper coverage of each, see our Authorize.net review and Fiserv review.

If you’re an ISV evaluating these two for embedded payments, the relevant comparison isn’t “which has better card processing” — both can process a card. The relevant comparison is which Fiserv product you’d actually integrate, how each handles sub-merchant economics, and whether Authorize.net’s stable-but-aging surface is a virtue or a constraint for your roadmap.

The short version: Choose Authorize.net for pricing transparency and Visa-network durability. Choose Fiserv (CardConnect for ISVs, Clover for vertical POS software) for scale, interchange-plus negotiation, and bank-distribution leverage — knowing the Clover product line is in a turbulent stretch.

Authorize.net vs Fiserv: ISV Comparison at a Glance

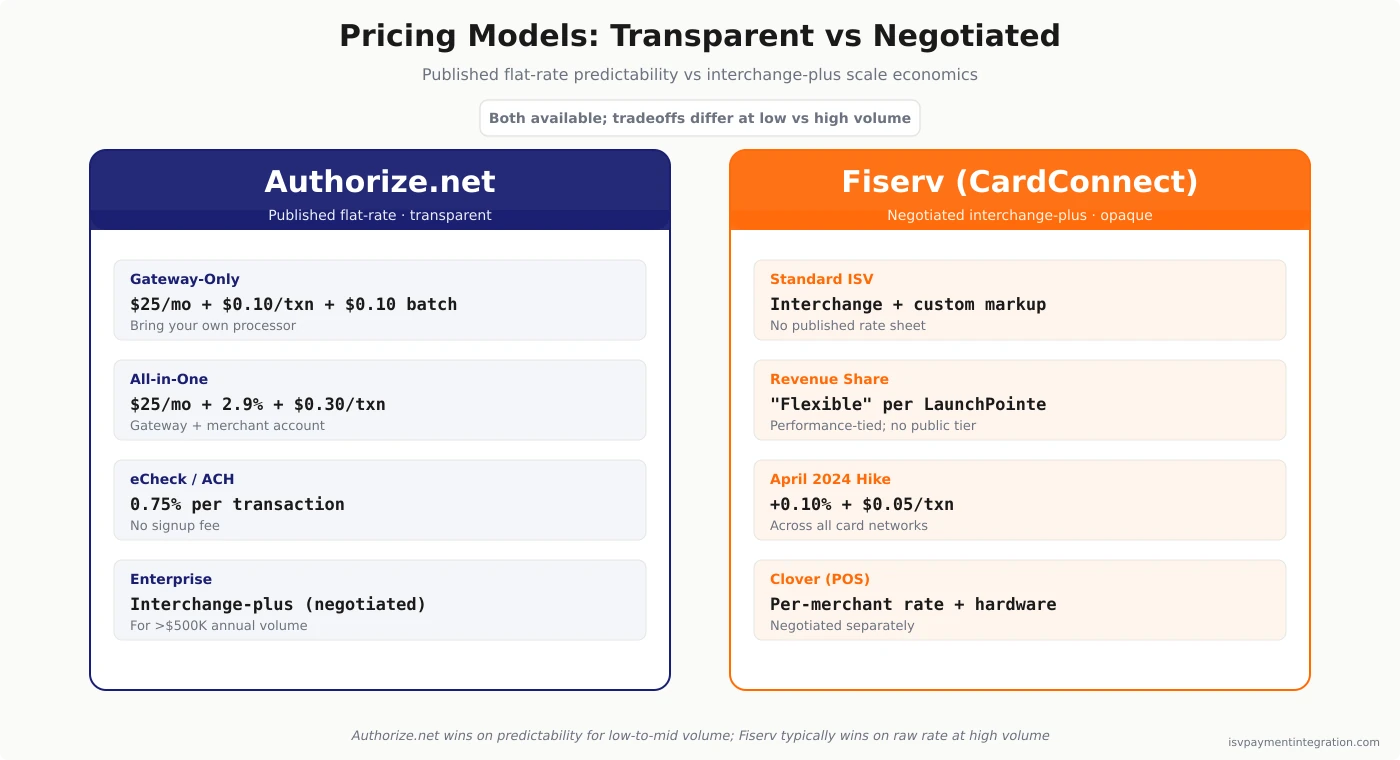

Authorize.net is a payment gateway, not an acquirer. Visa Inc. owns it through CyberSource (CyberSource bought Authorize.net for $565 million in 2007; Visa bought CyberSource for $2 billion in 2010). The published pricing is among the most transparent in US payments: $25/month + $0.10 per transaction + $0.10 daily batch fee for the gateway-only plan, or 2.9% + $0.30 + $25/month for the all-in-one plan that bundles merchant account services. eCheck/ACH runs at 0.75% with no signup fee. Custom interchange-plus pricing kicks in for merchants over $500K in annual volume. The gateway supports 430,000+ merchants and partners with 3,000+ resellers, including the kind of CRM, e-commerce, and SaaS platforms that ISVs typically build alongside.

Fiserv is the merchant-side counterpart to that picture, but the integration target depends on which Fiserv product an ISV actually wants. CardConnect (acquired through First Data in 2017 for $750M, retained post-Fiserv merger) is the gateway product for embedded payments and SaaS platforms. Clover is the POS hardware + commerce OS for SMB verticals — restaurants, retail, salons, service businesses. Carat is the enterprise omnichannel commerce platform for Fortune 500 merchants. AccessOne is consumer/patient financing for healthcare. There is no unified Fiserv developer portal across all four; ISVs must self-route to the right product before integration begins, and the most common ISV path is Fiserv’s ISV Partner Program partner program.

For pricing, see our Authorize.net pricing analysis and Fiserv pricing analysis.

What Each Brand Actually Sells

The single biggest source of confusion in this comparison is that “Fiserv” is four products, not one — and most listicle comparisons treat it as one. Getting this right shapes every other decision.

Authorize.net is one product. A gateway. Hosted payment pages (Accept Hosted), an embeddable form, AIM/SIM/DPM legacy integrations (officially obsolete and being phased out per the developer KB), and the current XML/JSON API. Tap to Pay was added in 2025 via TSYS for the Authorize.net 2.0 mPOS app on iOS and Android. ARB (Automated Recurring Billing) handles basic subscription scenarios. Sub-merchant onboarding is manual; there’s no native PayFac capability.

Fiserv is a stack you have to navigate. The path for most embedded-payments ISVs is CardConnect, which markets the ISV Partner Program to software companies and offers interchange-plus pricing, white-label options, and a residual revenue share that the company explicitly describes as “flexible” and “never set in stone.” For POS-attached vertical SaaS (restaurant, retail, salon, service), the path is Clover — either semi-integration (your software talks to Clover hardware) or full integration (your app runs natively on Clover Android devices via Clover App Market). Enterprise omnichannel work goes through Carat. Healthcare patient financing routes through AccessOne.

The practical implication: if an article compares “Authorize.net vs Fiserv” without specifying which Fiserv product, it’s comparing a gateway to an entire stack — apples to a fruit basket. For most SaaS platforms reading this comparison, the ISV path on Fiserv is CardConnect.

Pricing and Revenue Economics for ISVs

This is where the two diverge most sharply, because Authorize.net publishes its rates and Fiserv does not.

Authorize.net’s pricing is set by Visa, transparent, and aimed at predictability. Gateway-only at $25/month + $0.10/transaction + $0.10/batch fee. All-in-one at 2.9% + $0.30 + $25/month. eCheck at 0.75%. Volume above $500K/year qualifies for custom interchange-plus rates. The reseller economics are real but narrow: ISV partners earn residuals on the spread between a “buy rate” Authorize.net delivers and the markup the ISV sets — paid monthly, with no cost to enroll, but with a 12-month restriction on subsidizing merchant fees for new resellers. Per-transaction fees can be negotiated below $0.10 at meaningful volume, but Authorize.net does not publish tier breaks; that’s a sales conversation.

Fiserv’s pricing through CardConnect is interchange-plus, negotiated, and opaque. CardConnect publishes no consumer-facing rate sheet. The Fiserv ISV Partner Program offers performance-tied revenue share, white-label processor branding, and structures that merchant-cost analysts say typically beat Authorize.net’s flat-rate at high volume — but ISVs report meaningful negotiation friction at lower scale. CardConnect raised processing rates by 0.10% + $0.05 per transaction across all major card networks effective April 1, 2024, and that increase passes through to ISV revenue share margins. Clover’s POS economics are separate again — hardware fees, software subscription tiers, and processing rates negotiated per-merchant.

The honest take for ISVs:

- At low or mid volume (under ~$1M/yr platform-aggregated processing), Authorize.net’s published gateway-only structure is cheaper to model, easier to pass through, and produces predictable cost-per-merchant. ISV revenue share is small but visible.

- At high volume (multi-million-dollar platform processing), Fiserv/CardConnect’s interchange-plus typically wins on raw cost — but the negotiation cycle is longer, the residual structure is “we’ll figure it out,” and the dependency on Fiserv’s bank-distribution partners (Wells Fargo, Deutsche, PNC, MVB, Pathward, Citizens, KeyBank) means underwriting decisions sit further from your platform.

For the deeper economics of ISV revenue capture — referral, revenue-share, and full payment facilitator models — see our guide on PayFac-as-a-Service and our white-label payment processing breakdown.

API and Developer Experience: A Tale of Two Legacies

Both providers are old. The interesting question is how each wears its age.

Authorize.net’s API surface is candid about its legacy. The official developer support knowledge base states that “legacy API integration including AIM, SIM, DPM, Relay Response and Silent Post are now obsolete and in the process of being phased out.” The current standard is the unified XML/JSON API, with Accept Hosted (an embeddable hosted form that reduces PCI scope to SAQ-A) as the recommended embedded-ISV pattern. REST endpoints exist but the API’s heritage is XML-first, and the documentation reflects that. Visa launched Partner Portal 2.0 for new partners in June 2025, deprecated the legacy mobile apps in August 2025, and shipped the Authorize.net 2.0 mPOS app in mid-2025. Tap to Pay routes through TSYS as the underlying processor. There is no Stripe-style ground-up rebuild on the roadmap; the product is being modernized layer by layer rather than replaced.

Fiserv’s developer experience is criticized for fragmentation, not age. Industry trade analysis (Retail Systems’ “Payments — What Happened to Fiserv?” commentary) describes Fiserv as “disconnected from the actual problems ISVs face” and notes platform-operator frustration with portability and residual transparency. Each Fiserv product has its own developer surface (developer.fiserv.com, cardconnect.com, clover.com developer portal), and no unified federation spans them. Notably, Fiserv ships an AIM emulator through BluePay/CardConnect specifically to capture existing Authorize.net integrations — recognition that Authorize.net’s XML heritage is so entrenched that the migration tool is a competitive necessity.

For developer-led teams that need REST-native, version-controlled, copy-paste-good APIs, neither vendor is the default choice — that’s Stripe territory. Both Authorize.net and Fiserv are choices made for reasons other than the API surface itself: Visa-network durability, bank distribution, vertical POS attachment, or the simple inertia of an existing merchant base.

Onboarding and Underwriting Speed

For ISVs whose activation rate correlates with merchant time-to-live, this matters more than headline pricing.

Authorize.net’s gateway provisioning is straightforward — most merchants are processing within a business day of approval. Sub-merchant boarding for ISVs is manual rather than API-driven, which is fine for low-volume platforms but a friction tax at scale. Authorize.net does not operate a managed PayFac model; ISVs that want sub-merchant flows either build their own facilitation layer or partner with a separate PayFac provider.

Fiserv’s underwriting runs through bank sponsorships — Wells Fargo, Deutsche Bank, PNC, MVB Bank, Pathward, Citizens Bank, and KeyBank all sponsor Fiserv merchant services activity per the company’s standard footer disclosure. This is bank-grade underwriting (slower, more conservative, more documentation) versus Authorize.net’s gateway-style provisioning. CardConnect offers PayFac-adjacent boarding APIs through ISV Partner Program for ISVs that meet program criteria. For embedded payments flows where the ISV wants merchants live in minutes, neither vendor is best-in-class — that’s Stripe Connect Express or a dedicated PayFac-as-a-Service partner.

Risk, Compliance, and the Fiserv Litigation

Both vendors handle the table-stakes compliance work — PCI tokenization, 3DS2 authentication, KYC, KYB, dispute management. The interesting differences are upstream.

Authorize.net’s risk infrastructure runs through Visa. The Advanced Fraud Detection Suite (AFDS) offers configurable transaction filters at the gateway layer — velocity checks, IP geolocation, AVS mismatches, and shipping-address rules. Fraud detection is included in the standard pricing and integrates with the gateway’s reporting tools. Visa-network rules apply to chargebacks and dispute handling. Customer-trust signals are mixed — Capterra puts Authorize.net at 4.5/5 across 217 reviews and TrustRadius scores it 8.0/10, while Trustpilot consumer reviews skew sharply lower at 1.5/5. The split is a familiar pattern: B2B buyers (the SaaS audience) rate the gateway favorably; consumer merchants who hit chargeback or compliance friction rate it poorly. For an ISV evaluating the gateway, the B2B reviews are the relevant signal.

Fiserv’s risk infrastructure runs through bank-grade compliance — and two active securities class actions. Per Fiserv’s own Form 10-Q for the quarter ended March 31, 2026, the first was filed July 24, 2025 in the Southern District of New York against Fiserv, former Chairman and CEO Frank J. Bisignano (now head of the U.S. Social Security Administration), Michael P. Lyons, former CFO Robert W. Hau, and Kenneth F. Best, covering purchasers of Fiserv securities from July 22, 2024 to July 24, 2025. It alleges that Fiserv’s statements about the growth of the Clover platform were false or misleading. Lead plaintiffs were appointed November 17, 2025; the case is captioned In re Fiserv, Inc. Securities Litigation, No. 1:25-cv-06094. A second action, filed in November 2025 in the Eastern District of Wisconsin over statements made in connection with Fiserv’s second-quarter 2025 earnings, was consolidated as No. 25-cv-1716 and transferred to the Southern District of New York on April 28, 2026. At least six shareholder derivative complaints are also pending. Fiserv has accrued $26 million against its legal proceedings and estimates possible exposure above that accrual at $0 to roughly $160 million. Reporting on the underlying allegations is available from Bloomberg Law.

Two things about posture. Nothing has been adjudicated — as of that filing, “the defendants have not yet answered or otherwise responded to any of the complaints,” and Fiserv says it intends to defend vigorously. And the leadership that will do the defending is new: Michael Lyons resigned as CEO and director on June 12, 2026, effective immediately and with no severance or accelerated vesting; Takis Georgakopoulos was appointed CEO on June 14, 2026; and president Dhivya Suryadevara resigned “for good reason” on July 7, 2026.

For an ISV evaluating Clover specifically, this matters in two ways. First, Clover’s reported growth narrative is being publicly contested — reputational and partner-confidence risk that was not priced in two years ago. Second, the migrations at the center of the allegations stranded software built against the legacy Payeezy stack and forced rework on ISV partners. CardConnect is not directly implicated. But the broader operating posture is the context any Fiserv partnership decision lands in: revenue down 2.0% year over year in the first quarter of 2026, operating income down 34.2%, and a chief executive and a president who both left within four weeks.

This is not a reason to disqualify Fiserv. It is a reason to enter the relationship with eyes open about which product line is stable (CardConnect’s ISV channel has its own ISV Partner Program Circle of Excellence Award program) and which is in active turbulence (Clover’s growth narrative).

Customer Support, Ratings, and Reputation

Neither vendor is celebrated for support, and the operational character is different.

Authorize.net offers phone and email support with reasonable response times under Visa stewardship. The SaaS-buyer review sites tell a consistent story: Capterra ranks Authorize.net at 4.5/5 across 217 reviews, TrustRadius at 8.0/10 (90% would buy again), and Software Advice users rank Invoice Processing 4.86, Credit Card Processing 4.82, and Payment Fraud Prevention 4.82 as standout features. Trustpilot’s consumer reviews skew sharply lower (1.5/5), but the consumer/B2B split is the familiar pattern — small-business merchants who hit chargeback friction rate gateways harshly, while the SaaS audience evaluating the gateway as a development target rates it favorably.

Fiserv’s support experience depends on which product line and channel you came in through. Capterra puts Fiserv at 3.6/5 across 33 reviews; TrustRadius scores it lower (2.1/10 on a smaller sample driven by the Fiserv-ICICI legacy product). Fiserv’s customer-support footprint is large but distributed across the merchant-services, financial-institutions, and Clover product organizations. ISV partners under Fiserv’s ISV Partner Program report different (better) experiences than direct merchants under Clover — an artifact of Fiserv’s bank-distribution model where banks themselves are the front-line support channel for many merchants.

For ISVs evaluating either vendor, the relevant question isn’t the consumer rating — it’s whether the partner-channel team can answer your boarding, fraud detection, and reporting questions on your timeline. That’s a sales-conversation answer, not a Capterra-rating answer.

Geographic Reach and Currency Support

Authorize.net operates in the US, Canada, the UK, Europe, and Australia, with limited emerging-market coverage. ISVs serving international merchants typically pair Authorize.net with a regional acquirer or move to a globally-licensed platform like Adyen or Stripe.

Fiserv operates at global scale through its bank partnerships and the legacy First Data acquiring footprint — six million merchant locations, 10,000+ financial institutions clients, and an active expansion of the Clover suite into Japan via a Sumitomo Mitsui partnership scheduled for late 2026. The financial institutions network drives Fiserv’s distribution moat; banks sell merchant services to their own business-banking customers, and Fiserv’s processing rails sit underneath. Even so, Fiserv’s strongest ISV-program presence remains North America and Europe, and the legacy product fragmentation means international integration paths vary by region and product line.

For ISVs with material international merchant exposure (more than 15% of platform volume), neither vendor is structurally optimized for global. That’s a different conversation — see Adyen vs Fiserv for the enterprise-global alternative.

When to Choose Authorize.net

Authorize.net is the better fit for ISVs and platforms that:

- Need pricing transparency — published $25/month + $0.10/transaction (gateway-only) or 2.9% + $0.30 (all-in-one) makes cost modeling and merchant pass-through straightforward

- Integrate with merchants already on Authorize.net — 430,000+ merchants and 3,000+ resellers means a meaningful portion of the SMB e-commerce base is already reachable

- Want Visa-network durability — under Visa Acceptance Solutions ownership, the gateway is not going anywhere, and chargeback/dispute mechanics inherit Visa-network rules

- Operate at low-to-mid volume — under roughly $1M/year platform-aggregated processing, the published-rate predictability outweighs interchange-plus negotiation

- Need Authorize.net’s reseller program — the ISV/Reseller path is real, with monthly residuals on buy/sell rate spread, no enrollment cost, and access to Visa partner resources

- Don’t need PayFac-grade boarding — sub-merchant onboarding is manual; if your activation flow tolerates business-day provisioning, this is a non-issue

For a closer alternative on the white-label gateway side, see our NMI vs Stripe breakdown — NMI sits in the same gateway lane but with stronger ISV-specific tooling.

When to Choose Fiserv (CardConnect or Clover)

Fiserv is the better fit for ISVs and platforms that:

- Operate at high volume — multi-million-dollar platform processing makes interchange-plus through CardConnect economically meaningful versus flat-rate

- Want bank-distribution scale — Fiserv’s Wells Fargo, PNC, Citizens, KeyBank, MVB, and Deutsche Bank sponsorships unlock relationships an independent gateway can’t

- Build vertical POS-attached SaaS — restaurant, retail, salon, and service software with hardware integration belongs on Clover, not Authorize.net

- Need PayFac-adjacent boarding — Fiserv’s ISV Partner Program offers boarding APIs and managed-PayFac-style flows that Authorize.net does not

- Sell into enterprise — Carat handles Fortune 500 omnichannel work that neither Authorize.net nor most ISV-grade gateways are scoped for

- Are comfortable with negotiation friction — the residual structure, the interchange-plus rates, and the bank-underwriting cycle all require sales-cycle patience

For developer-first ISVs that find both vendors too legacy, the modern alternatives sit elsewhere — see Stripe vs Adyen for the platform-payments comparison and Xplor Pay for the ISV-specialized PayFac play.

Consider a Third Option

Authorize.net and Fiserv represent two specific seats in US payments — Visa’s gateway and the post-First Data merchant acquirer. The ISV market has moved past both for purpose-built embedded payments.

Stripe is the developer-first default for early-stage ISVs that want fast time-to-market and a single-vendor stack. Adyen for Platforms is the enterprise-global alternative for ISVs with international merchants. NMI is the white-label gateway specialist that sits closer to Authorize.net’s lane but with stronger ISV tooling. Xplor Pay is the ISV-specialized PayFac play that bridges the gap. WePay (now part of J.P. Morgan Payments) is the bank-grade ISV alternative for US-only platforms. Authorize.net vs Global Payments is the comparison if you’re looking at Worldpay’s new parent post-January 2026.

Get a free integration assessment for your ISV →

Frequently Asked Questions

Who is Fiserv’s biggest competitor?

It depends on the cut. By overall revenue scale, FIS (Fidelity National Information Services) is the closest direct competitor, with overlapping financial-institution technology and merchant services. By merchant acquiring volume in 2026, Global Payments — newly enlarged after closing its $24.25 billion acquisition of Worldpay on January 12, 2026 — is the most direct rival in omnichannel acquiring. By embedded payments and enterprise-platform work, Adyen is Fiserv’s primary threat, growing 23% YoY versus Fiserv’s 4%. By US bank-distribution scale, JPMorgan Payments ($19.4B 2025 revenue, ~$2.6T merchant processing volume) is the institutional rival — and increasingly competitive in ISV-focused embedded payments since the WePay/JPM integration completed in mid-2025. For developer-first ISV platforms specifically, Stripe is the dominant alternative.

What is the Fiserv controversy?

Two things, and they compound. The first is litigation: two securities class actions, both now in the Southern District of New York. The lead case, In re Fiserv, Inc. Securities Litigation, No. 1:25-cv-06094, was filed July 24, 2025 and covers purchasers of Fiserv securities from July 22, 2024 to July 24, 2025; it alleges Fiserv’s statements about Clover’s growth were false or misleading. A second action over Fiserv’s second-quarter 2025 earnings statements was consolidated in Wisconsin as No. 25-cv-1716 and transferred to New York on April 28, 2026. At least six shareholder derivative complaints are pending alongside them. Fiserv has accrued $26 million and estimates additional possible exposure of up to roughly $160 million. Nothing has been adjudicated.

The second is leadership. CEO Michael Lyons resigned on June 12, 2026, effective immediately, taking no severance and no accelerated equity. Takis Georgakopoulos — previously Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank — was appointed chief executive two days later. On July 7, 2026, president Dhivya Suryadevara resigned “for good reason.” Meanwhile first-quarter 2026 revenue fell 2.0% year over year and operating income fell 34.2%. For an ISV, the controversy is not any single lawsuit; it is that the counterparty is defending securities litigation, replacing its senior team, and watching margin compress at the same time.

Does Fiserv have a future?

Yes. Fiserv reported $21.19 billion in 2025 revenue (up 4% YoY), serves six million merchant locations and 10,000+ financial institutions, and has a multi-year IBM AI partnership and a 2026 ISV Playbook published on fiserv.com targeting omnichannel acceptance, embedded finance, and fraud defense. International expansion into Japan via Sumitomo Mitsui is scheduled for late 2026. The Clover credibility hit is real and ongoing, but Fiserv’s bank-distribution moat, scale, and post-First Data operating integration mean the company is structurally durable. The medium-term question is whether Clover’s growth narrative recovers and whether Fiserv closes the developer-experience gap with Stripe and Adyen.

Who did Fiserv merge with?

Fiserv acquired First Data Corporation in 2019. Announced January 16, 2019; closed July 29, 2019. The deal was an all-stock transaction valued at approximately $22 billion, with First Data shareholders receiving 0.303 Fiserv shares per First Data share at a 29.6% premium. Post-close ownership split was 57.5% legacy Fiserv, 42.5% legacy First Data. Fiserv brought 12,000+ FI clients and bank-tech infrastructure; First Data brought the largest US merchant acquiring footprint, the Clover POS platform (already inside First Data since 2012), the STAR debit network, and international merchant services. The “bank-to-merchant flywheel” is the strategic logic that still drives Fiserv’s product portfolio today.

Is Authorize.net still being modernized under Visa?

Yes — incrementally rather than through a ground-up rebuild. Visa shipped Partner Portal 2.0 to new partners in June 2025, deprecated the legacy mobile apps in August 2025, released the Authorize.net 2.0 mPOS app in mid-2025, and added Tap to Pay (Android and iOS) via TSYS as the underlying processor. The unified XML/JSON API replaces the obsolete AIM, SIM, DPM, Relay Response, and Silent Post integrations. Accept Hosted is the recommended embedded-ISV pattern for SAQ-A PCI scope reduction. There is no Stripe-style REST-native rebuild on the public roadmap; under Visa Acceptance Solutions ownership, the product is being layered forward from its 1996 foundation rather than replaced.

The Bottom Line

Authorize.net and Fiserv are both legacy choices, but they’re legacy in different ways. Authorize.net is Visa’s stable, transparent, slowly-modernizing gateway — the right pick for ISVs that want predictable pricing, durable network ties, and a single-product gateway whose 430,000-merchant base is a real distribution channel. Fiserv (specifically CardConnect for ISVs, Clover for vertical POS software) is the post-First Data merchant acquirer — bigger, more fragmented, with bank-distribution scale that no independent gateway can match, and a Clover product line working through a credibility hit that has not yet resolved.

Neither is the developer-first default an early-stage SaaS would pick today. The question is which legacy fits your ISV’s profile: Visa-network gateway with transparent economics (Authorize.net), or bank-grade merchant acquirer with negotiated interchange-plus and vertical POS attach (Fiserv). For a platform that’s growing past either, the Stripe vs Adyen, NMI vs Stripe, and Xplor Pay vs Stripe comparisons are where the next decision lives.

Need help evaluating which platform fits your ISV? Get a free integration assessment →