Stripe vs WePay

A feature-by-feature comparison for ISVs integrating payments.

Stripe is the developer-first payments platform that operates in 47 countries with the deepest API ecosystem in fintech. WePay is now part of J.P. Morgan Payments — Chase folded the WePay platform into its modern commerce stack in 2024-2025, and the WePay brand survives mainly as a marketing wrapper for three ISV tiers (Link, Clear, Core) that ride on JPMorgan Chase acquiring. Choose Stripe for global reach, developer experience, and the broadest single-vendor ecosystem. Choose WePay (now J.P. Morgan Payments) for US ISVs that want bank-grade processing tied to Chase commercial banking.

Feature Comparison

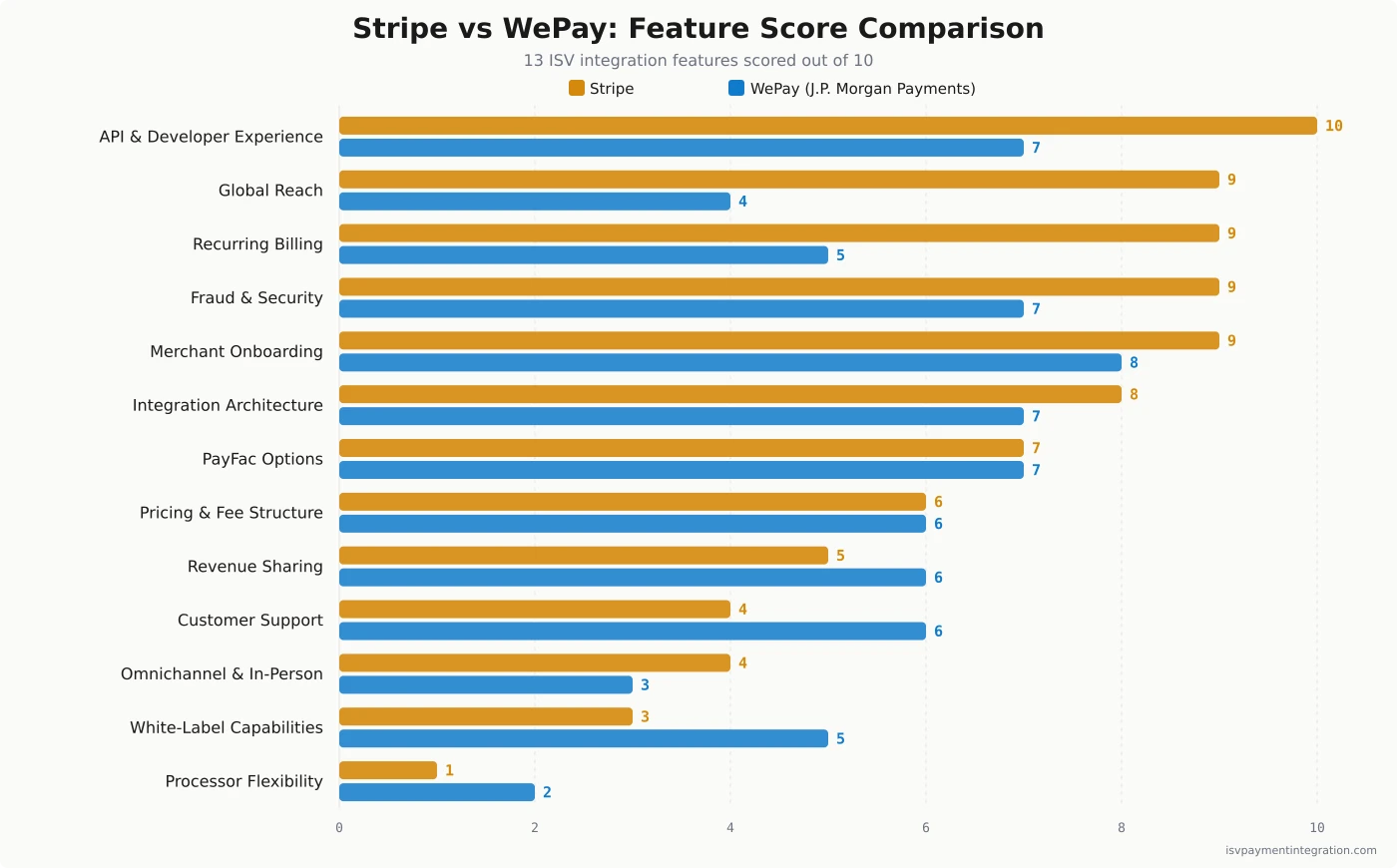

| Feature | Stripe | WePay |

|---|---|---|

| Integration Architecture | 8 | 7 |

| API & Developer Experience | 10 | 7 |

| White-Label Capabilities | 3 | 5 |

| Processor Flexibility | 1 | 2 |

| Pricing & Fee Structure | 6 | 6 |

| Omnichannel & In-Person Payments | 4 | 3 |

| Fraud & Security | 9 | 7 |

| Revenue Sharing | 5 | 6 |

| Merchant Onboarding | 9 | 8 |

| Global Reach | 9 | 4 |

| Recurring Billing | 9 | 5 |

| Customer Support | 4 | 6 |

| PayFac Options | 7 | 7 |

Get this comparison as a shareable PDF

We'll send the Stripe vs WePay breakdown to your inbox — ready to share with your team.

Best for

Stripe

ISVs at any stage that want fast time-to-market, the deepest API and SDK ecosystem in fintech, multi-currency support across 47+ countries, and a single vendor for payments, billing, fraud, and identity. Developer-led teams and SaaS platforms with international ambitions get the most value.

Best for

WePay

US-focused ISVs and platforms that want bank-backed payment processing tied to JPMorgan Chase and value same-day payouts to Chase business accounts, white-label embedded checkout, and a managed PayFac model where Chase handles the compliance and underwriting layer.

Stripe and WePay are the two most-cited names when ISV teams scope embedded payment processing — but they no longer compete the way they did three years ago. Stripe is the developer-first payments platform in 47+ countries with the deepest API and SDK ecosystem in fintech. WePay is now part of J.P. Morgan Payments — JPMorgan Chase folded the WePay platform into its modern commerce stack between 2024 and 2025, ended a slate of legacy ISV agreements during that integration, and now markets WePay as three tiers (Link, Clear, Core) that ride on Chase acquiring. For deeper coverage of each, see our Stripe review and WePay review.

The right choice in 2026 turns on three questions: how much of the world your merchants live in, how much white-label control your ISV needs, and whether the JPMorgan Chase relationship is an asset or a constraint.

The short version: Choose Stripe for global reach, developer experience, and a single-vendor ecosystem. Choose WePay (J.P. Morgan Payments) for US ISVs that want bank-grade processing tied to Chase.

Editor’s note on WePay’s status (2026). WePay was acquired by JPMorgan Chase in December 2017 and operated semi-independently for several years. In late 2023, JPM abruptly ended a number of long-standing WePay ISV and business customer agreements. In May 2024, J.P. Morgan formally announced that WePay’s capabilities would be “fully integrated into our modern commerce platform” over the following 12 months — a transition that completed in mid-2025. The WePay brand and

go.wepay.comsite still exist, but the underlying payment processing product is now J.P. Morgan Payments, and new ISV onboarding goes through Chase’s combined offering rather than WePay’s old standalone platform. We treat this comparison as Stripe vs J.P. Morgan Payments for any decision a new ISV is making today.

Stripe vs WePay: ISV Comparison at a Glance

Stripe is a full-stack payment processor: gateway, payment processing, acquiring, billing, fraud, and identity behind one API. Stripe charges 2.9% + $0.30 per successful credit card transaction, 2.7% + 5¢ for in-person credit card processing, and 4.4% + $0.30 for international cards. The platform supports Apple Pay, Google Pay, Link, ACH, EMV terminals via Stripe Terminal, and 135+ currencies with multi-currency settlement.

WePay charges 2.9% + $0.25 for card-not-present credit card processing — $0.05 per transaction lower than Stripe — plus 1% + $0.30 for ACH bank account transfers. Same-day payouts are available, but only to merchants holding a bank account at JPMorgan Chase. WePay supports virtual cards, contactless payments, mobile checkout, and Apple Pay/Google Pay through its embedded UI. Small businesses get the same published fee schedule as larger ISVs; WePay’s pricing differentiation happens at the partnership level.

For deeper fee analysis, see our Stripe pricing analysis and WePay pricing analysis.

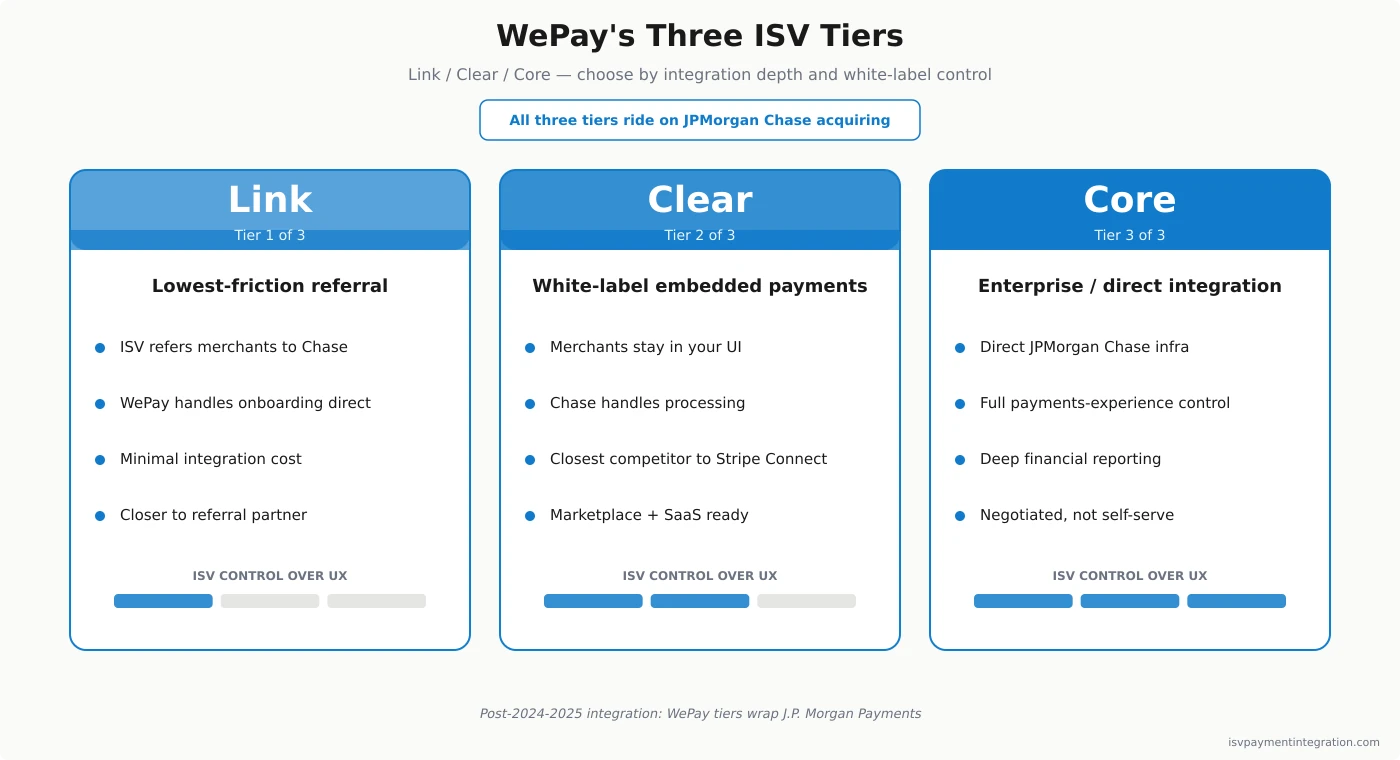

WePay’s Three ISV Tiers: Link, Clear, and Core

WePay, inside J.P. Morgan Payments, comes in three tiers — and which tier you pick determines most of the other answers below.

- Link is the lowest-friction option. Your ISV refers merchants to Chase Integrated Payments; WePay handles onboarding and compliance directly with the merchant. Integration cost is minimal, but your platform sits closer to a referral partner than an embedded payments owner.

- Clear is the white-label embedded payment solution. Merchants stay inside your software’s UI for signup, checkout, and account management, while Chase handles processing. This is the tier ISVs evaluate against Stripe Connect for marketplace and SaaS use cases.

- Core is the enterprise integration that connects directly to JPMorgan Chase infrastructure. Built for high-volume platforms that need full control over the payments experience, deep financial reporting, and custom revenue sharing.

Stripe doesn’t slice its ISV offering the same way. Stripe Connect covers the equivalent ground — Standard, Express, and Custom account types map roughly to referral, white-label-lite, and full-control models — but the framing is API-first rather than membership-based.

API and Developer Experience

For most engineering teams, this is where the comparison is decided.

Stripe’s developer experience is the industry benchmark. Stripe’s API documentation is the example everyone else copies — SDKs in every major language, copy-paste sample code, a sandbox that mirrors production, and the most active developer community in fintech. Most engineers process a test transaction in under an hour. Stripe.js and Elements handle client-side tokenization with minimal PCI scope, and the same primitives extend to mobile via Stripe’s iOS and Android SDKs.

WePay’s APIs are functional and modern but less expansive. WePay offers the building blocks an ISV needs for payment processing — hosted payment fields, tokenization, recurring billing, KYC, and Apple Pay/Google Pay — and developer documentation lives at dev.wepay.com. Compared vs Stripe, what it doesn’t offer is the surface area: no native equivalent to Stripe Billing or Stripe Identity, and a smaller third-party tool ecosystem. Where WePay holds up well is platform-style flows for marketplaces and crowdfunding — the legacy use case it was built for as the payment processor behind GoFundMe.

A B2B note: neither vendor is best-in-class for Level II/III interchange data. ISVs serving B2B merchants that want to pass purchase order numbers and line-item data to qualify for lower interchange rates should look at gateways like NMI.

Revenue Economics for ISVs

ISVs earn payment revenue from the spread between what merchants pay and what the processor charges — and the math diverges fast at scale.

WePay’s $0.05-per-transaction discount versus Stripe is small in absolute terms but accumulates. At 200 card-not-present transactions per merchant per month, that’s $10/merchant/month or $120/year — multiplied across a few thousand merchants, the delta becomes meaningful, but only if your platform passes the saving through or captures it.

The bigger lever is ACH. WePay’s 1% + $0.30 ACH rate is significantly cheaper than Stripe’s 0.8% (capped at $5) for higher-ticket bank account transfers, and meaningfully cheaper than card processing for ISVs whose merchants run heavy on subscription plans, B2B invoicing, or rent payments.

Stripe Connect’s revenue share ramps slowly. According to Swipesum’s analysis of Stripe alternatives, revenue share is “only available to platforms with very high processing volumes — often in the tens of millions annually,” and many SaaS platforms find margin capped around $50M in annual processed payments before they look elsewhere.

WePay’s revenue sharing model runs on Chase commercial relationships. Custom interchange-plus pricing, ISV-controlled markup, and per-transaction fee management are available — typically at Clear or Core, rather than out of the box at Link.

For where ISV payment revenue actually comes from, our guide on PayFac-as-a-Service walks through referral, revenue-share, and full payment facilitator models.

Same-Day Payouts and the Chase Lock-In

WePay’s most-cited advantage is one business day turnaround on payouts — and same-day payouts when the merchant holds a Chase bank account. For ISVs whose merchant base is heavily Chase-banked (event organizers, fundraising platforms, marketplace sellers on Chase business banking), this materially improves cash flow.

The catch: it’s a Chase-account benefit, not a WePay benefit. Merchants on any other bank get standard banking timelines. Stripe charges 1% (minimum $0.50) for instant payouts to eligible debit cards and accounts, plus 2-day standard payouts with no acquiring-bank requirement.

If “same day deposits to Chase” is a feature you can sell to merchants, WePay wins. If your merchants bank everywhere, Stripe’s payout flexibility is more useful.

Geographic Reach and Currency Support

This is the cleanest comparison on the scorecard. Stripe operates in 47+ countries with 135+ currencies and automatic local payment method routing — SEPA, iDEAL, Klarna, Afterpay, Alipay, WeChat Pay, and so on. ISVs serving international merchants get multi-currency settlement and a single integration that works globally.

WePay is effectively US-only. J.P. Morgan Payments supports cross-border acceptance for US merchants selling to international customers, but onboarding non-US merchants is not a path WePay markets. ISVs with international ambitions either route those merchants to Stripe, run a multi-vendor strategy with Adyen or Braintree, or wait for JPMorgan Chase to extend WePay outside the US.

If even 10-15% of your merchants are non-US, Stripe is the structural choice.

Fraud, Compliance, and the JPMorgan Backing

Both vendors handle the basics — PCI tokenization, 3DS2, dispute management, KYC, KYB, anti-money-laundering checks. The differences are upstream.

Stripe Radar is a competitive advantage. Stripe charges an extra $0.07 per screened transaction for advanced rules, but the baseline ML protection — trained on billions of transactions across Stripe’s network — is included in standard pricing. For ISVs that don’t want to build or tune fraud rules themselves, this is meaningful out-of-the-box protection.

WePay’s risk and compliance infrastructure runs on JPMorgan Chase’s institutional risk operation. The bank’s anti-money-laundering, fraud monitoring, and own-due-diligence processes are unambiguously thorough — but they also tend to be more conservative than Stripe’s ML-driven risk model. The abrupt offboarding of WePay business customers in late 2023 is the case study for how that conservatism affects ISV partners.

Customer Support: The Reality

Neither vendor is celebrated for support, and the operational character is different.

Stripe runs a self-service-first model. Documentation is deep enough that most issues resolve without contacting anyone. Live chat and email support exist; priority phone support requires an Enterprise plan that costs extra. Capterra’s user reviews put Stripe at 4.6/5 overall (3,327+ users) with customer service at 4.2/5.

WePay does not offer phone support at all. The vendor relies on a ticket system with a published one business day turnaround. Capterra’s user data shows WePay at 3.2/5 overall (73 users), value for money at 2.8/5, and customer service at 2.6/5. Post-integration with JPMorgan Chase, the support pathway is different anyway — Chase relationship managers sit at the top of the tree for higher-tier ISVs.

Practical takeaway: budget for support gaps either way. Stripe rewards self-service-capable teams; WePay rewards ISVs that already have a JPMorgan Chase banking relationship.

Onboarding and Activation Speed

Stripe’s Connect Express onboarding gets merchants accepting payments in minutes. The hosted flow handles KYC verification, compliance checks, and account provisioning automatically — easily Stripe’s strongest operational advantage, especially for small businesses that need to be live in the same session they sign up.

WePay’s onboarding leverages JPMorgan Chase’s underwriting and KYB. Approval is fast for merchants that fit Chase’s risk profile, but it’s measured in business days rather than minutes. The trade-off is that WePay’s managed PayFac model handles compliance for you — at Clear and Core tiers, your ISV doesn’t carry the registration burden of becoming a full payment facilitator.

For platforms where activation speed correlates directly with revenue, Stripe wins. For ISVs where merchants are recruited and underwritten through a longer sales process, WePay’s pace is a non-issue.

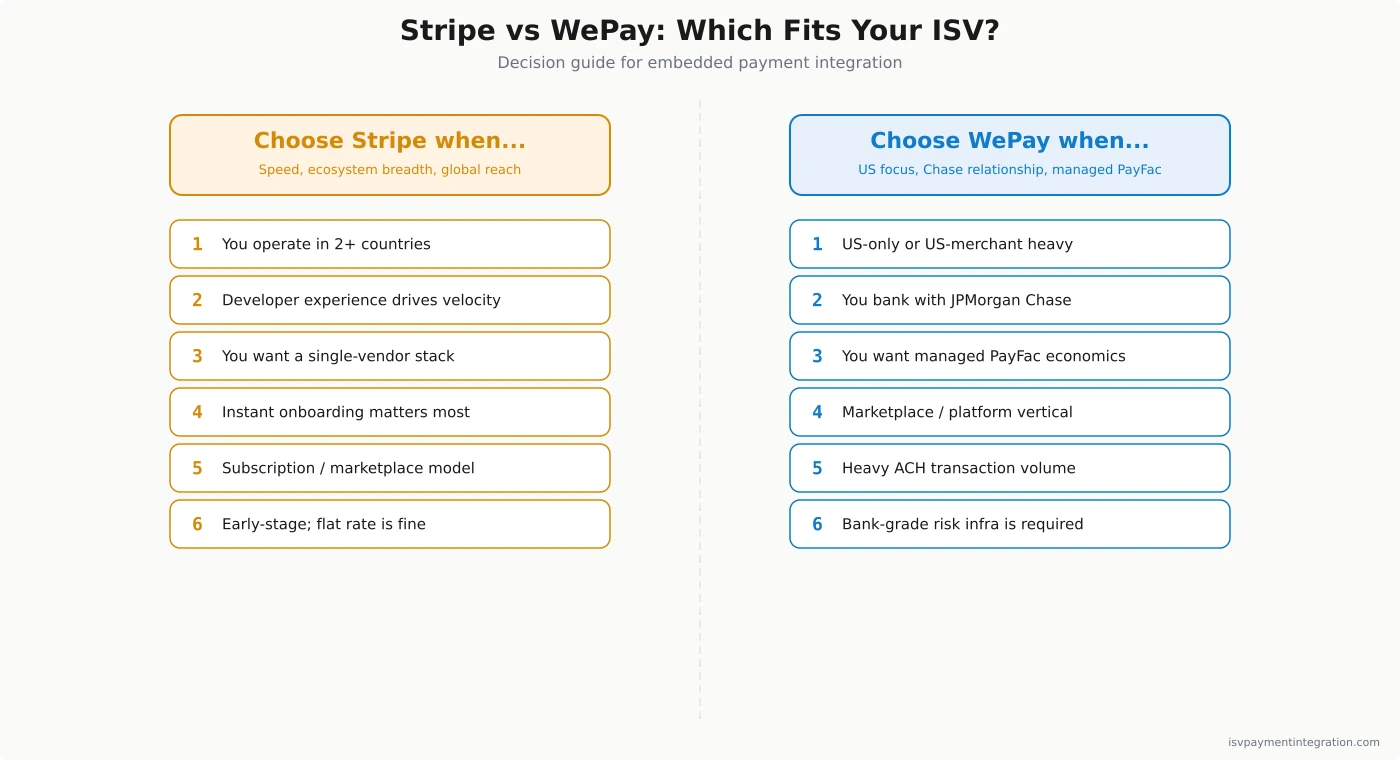

When to Choose Stripe

Stripe is the better fit for ISVs and platforms that:

- Operate internationally — 47+ countries, 135+ currencies, local payment methods

- Prioritize developer experience — best-in-class APIs, SDKs, sandbox, and community

- Want a single vendor — payments, billing, fraud, terminal, and identity in one platform

- Need instant merchant onboarding — Connect Express activates merchants in minutes

- Run subscription or marketplace models — Stripe Billing and Connect handle complex flows

- Are early-stage — flat-rate pricing simplicity outweighs cost optimization at low volume

For developer-led teams especially, the speed advantage is hard to overstate. Stripe is the default for a reason.

When to Choose WePay (J.P. Morgan Payments)

WePay is the better fit for ISVs and platforms that:

- Are US-focused and US-merchant heavy — international support is not on the roadmap

- Have a JPMorgan Chase banking relationship — same-day payouts and rate negotiation work in your favor

- Need a managed PayFac model — Chase handles compliance, underwriting, and risk

- Sell into platforms or marketplaces — Clear and Core tiers were built for this

- Process heavy ACH volume — 1% + $0.30 ACH pricing is competitive

- Want bank-grade risk infrastructure — institutional anti-money-laundering and own-due-diligence processes

The J.P. Morgan WePay integration page is the canonical statement on how the product is positioned post-2024.

Consider a Third Option

Stripe and WePay represent two ends of a spectrum: maximum global reach and developer ecosystem (Stripe) versus US-focused bank-grade processing tied to one acquiring relationship (WePay/Chase). Some ISVs find neither extreme fits.

ISV-first embedded payments platforms like Xplor Pay, Finix, and Adyen for Platforms bridge the gap — white-label control and ISV-focused onboarding with integrated acquiring and dedicated support. See how each compares in our Xplor Pay vs Stripe, Stripe vs Finix, and Stripe vs Adyen analyses, or Stripe vs Braintree for a PayPal-owned alternative. ISVs that want true white-label control over the gateway often look at NMI vs Stripe — see our guide on white-label payment processing for ISVs for the economics.

Get a free integration assessment for your ISV →

Frequently Asked Questions

Is WePay still accepting new ISV signups in 2026?

Yes — but through J.P. Morgan Payments, not the legacy WePay platform. New ISV agreements are evaluated against Chase’s risk and underwriting criteria, and the Link, Clear, and Core tiers are the current routes in. JPMorgan ended a number of legacy WePay ISV agreements during the 2024-2025 integration, so your platform’s risk profile and merchant base matter to the application.

What happened to WePay?

WePay was acquired by JPMorgan Chase in December 2017 and operated as a Chase company for several years. In May 2024, J.P. Morgan announced that WePay’s capabilities would be fully integrated into the J.P. Morgan Payments platform over the following 12 months. That integration completed in mid-2025. The WePay brand and go.wepay.com site still exist as a marketing wrapper for the three ISV tiers, but the underlying product is now part of J.P. Morgan Payments.

What is the difference between Stripe Connect and WePay Clear?

Stripe Connect is a developer-first platform payments product available globally, with three account models (Standard, Express, Custom) covering referral-style to fully-controlled merchant relationships. WePay Clear is the white-label embedded payments tier inside J.P. Morgan Payments — built for US ISVs that want their merchants to never see Chase branding, with compliance and underwriting handled by JPMorgan Chase. Connect is broader and faster to integrate; Clear is deeper on bank-grade compliance for US merchants.

What is the disadvantage of Stripe?

Stripe’s main disadvantages for ISVs at scale are flat-rate pricing that becomes expensive without a custom deal, a Connect revenue share model that requires very high processing volumes before margins improve, partial white-label (Stripe branding remains visible in parts of the merchant experience), and self-service-first support that requires a paid plan for priority phone access. Higher-risk verticals also report account stability issues.

Who is Stripe’s biggest competitor?

It depends on the cut. Globally, Adyen is Stripe’s most direct enterprise competitor on payment processing scale and global acquiring. For developer-first APIs in the US, Braintree (PayPal) and Finix are common alternatives. For ISV-focused white-label embedded payments specifically, NMI and Xplor Pay are the names that come up most often in vendor evaluations.

The Bottom Line

Stripe and WePay no longer occupy the same competitive lane. Stripe wins on global reach, developer experience, and ecosystem breadth — the platform for ISVs that want speed, scope, and a single-vendor stack. WePay (now J.P. Morgan Payments) wins for US-focused ISVs that want bank-grade processing tied to JPMorgan Chase — same-day payouts to Chase accounts, a managed PayFac model, and competitive ACH pricing for transaction-heavy verticals.

The post-integration shift inside J.P. Morgan Payments means today’s WePay decision is really a J.P. Morgan Payments decision. The trade-off between bank-channel safety and Stripe’s reach-and-velocity model is the one your ISV actually has to make. For more context, see Stripe vs Adyen, Stripe vs Braintree, and Stripe vs Finix.

Need help evaluating which platform fits your ISV? Get a free integration assessment →