Adyen vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Every other pairing in this category has one company that publishes a price and one that does not. This is the pair where both put a percentage in public — one on a pricing page, one in a developer agreement. That makes it the right place to ask a question the category usually skips: what is a published number actually worth, and which of these two documents is a promise?

Feature Comparison

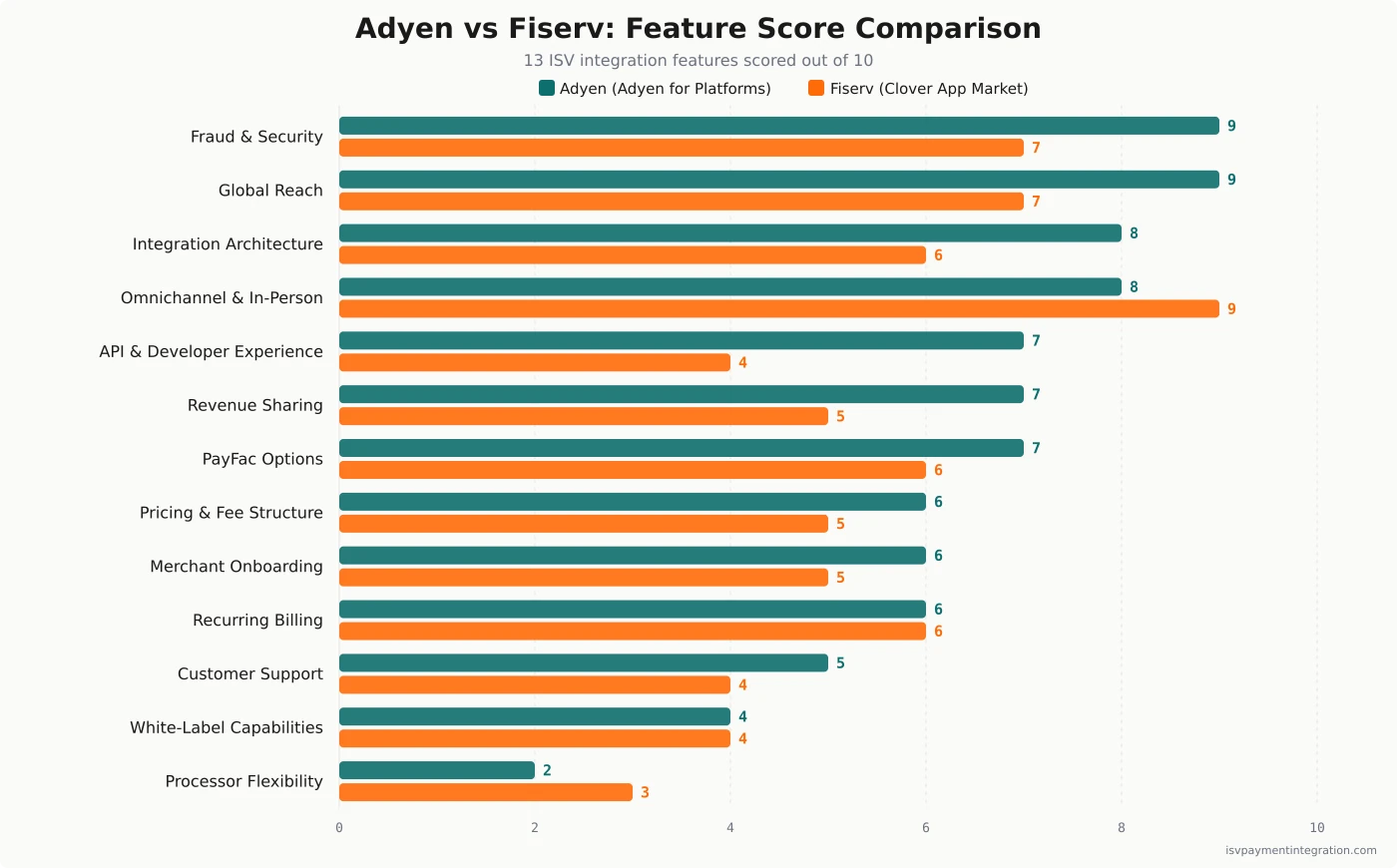

| Feature | Adyen | Fiserv |

|---|---|---|

| Integration Architecture | 8 | 6 |

| API & Developer Experience | 7 | 4 |

| White-Label Capabilities | 4 | 4 |

| Processor Flexibility | 2 | 3 |

| Pricing & Fee Structure | 6 | 5 |

| Omnichannel & In-Person Payments | 8 | 9 |

| Fraud & Security | 9 | 7 |

| Revenue Sharing | 7 | 5 |

| Merchant Onboarding | 6 | 5 |

| Global Reach | 9 | 7 |

| Recurring Billing | 6 | 6 |

| Customer Support | 5 | 4 |

| PayFac Options | 7 | 6 |

Get this comparison as a shareable PDF

We'll send the Adyen vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Adyen

Best for platforms with a sales motion already working, where payments is a second revenue line rather than a distribution channel. Accept the minimum invoice, accept that your rate is negotiated rather than published, and accept that the merchant you introduce signs a User Agreement with Adyen N.V. that Adyen can end on two months' notice.

Best for

Fiserv

Best for software that would rather receive a remittance than run a payments business, and that will trade a marketplace cut for a fee it can read before signing. Accept that Clover contracts with your customer, bills them, deducts before it remits, and may end the arrangement for no stated reason.

Adyen vs Fiserv: Only One of Them Publishes a Commitment

Two percentages travel with these companies. Adyen prints its card fee on a public pricing page. Clover — the Fiserv product a vertical SaaS company is usually evaluating — states its developer take rate in the App Market Developer Terms.

The instinct is to put 0.60% beside 30% and subtract. Resist it, for two reasons. The first is obvious once said: Adyen’s 0.60% prices payments and Clover’s 30% prices software. Adyen does not sell app distribution, and its Platforms terms take no share of an ISV’s software revenue. Clover’s Developer Terms, in turn, give an ISV no share of payment processing. These are not two prices for one thing. They are the prices of two different things.

The second reason is the one this page is about. Read what each number is written on, and the reliable one is not the one you would guess.

Quick Take: Two Doors, and Only One Contract States a Price

Adyen is one legal entity carrying licences in each region it acquires in. adyen.com/licenses/emea records that Adyen N.V. “is authorised as a credit Institution under the supervision of Dutch Central Bank (De Nederlandsche Bank),” which the page notes “is commonly referred to as a ‘banking license’” and which carries “the ability to provide cross-border acquiring, payment and banking services in all EEA countries in accordance with the passporting rules under CRD IV.” In the United States, adyen.com/licenses/united-states describes the San Francisco branch as “a federal Branch of Adyen, N.V., licensed by the Office of the Comptroller of the Currency and the Federal Reserve Board of Governors.” The ISV product is Adyen for Platforms, which Adyen’s own country list puts in 34 markets.

Fiserv answers to the door you knock on. Its ISV Partner Program page sells a gateway called CardPointe and a portfolio console called CoPilot, advertises “Managed PayFac Capabilities” — “Gain control of the payments experience and the benefits of payment facilitation while we handle the heavy lifting” — and, as fetched on 10 July 2026, quotes no rate. Those partner terms are not published on that page and are not read here.

This page reads one Fiserv contract: the Clover App Market Developer Terms. It is the Fiserv-owned ISV document we found that states a figure. CardPointe, Commerce Hub and Managed PayFac carry terms this page has not read, and nothing below describes them. When this page says “thirty percent,” it is describing that one agreement.

Symmetrically, everything below about split instructions and balance accounts describes Adyen for Platforms. The liable balance account and the splits array are features of that product.

What Adyen Publishes: a Number It Calls Indicative

The card rows on adyen.com/pricing render as:

$0.13 + Interchange+ + 0.60%

The tooltip attached to that cell explains the model: “Interchange fees are variable, our Interchange++ pricing passes these fees directly to you, giving you more transparency and lower fees overall.” The page’s own FAQ elaborates: “Interchange++ is a pricing model which accurately tracks Interchange rates and scheme fees right down to a transaction level. This means we can calculate the cost of each payment even before it is completed.”

Then, in the same FAQ, the number softens:

- “The fees outlined above are indicative; please get in touch to discuss pricing options.”

- “We do not have monthly fees, set-up fees, integration fees or closure fees. We do have a minimum invoice depending on industry or business model.”

And the Platforms documentation confirms that a discount machinery exists behind the list price: “Tiered pricing: Any discounts that are derived from tiered pricing structures cannot be allocated to individual payments.”

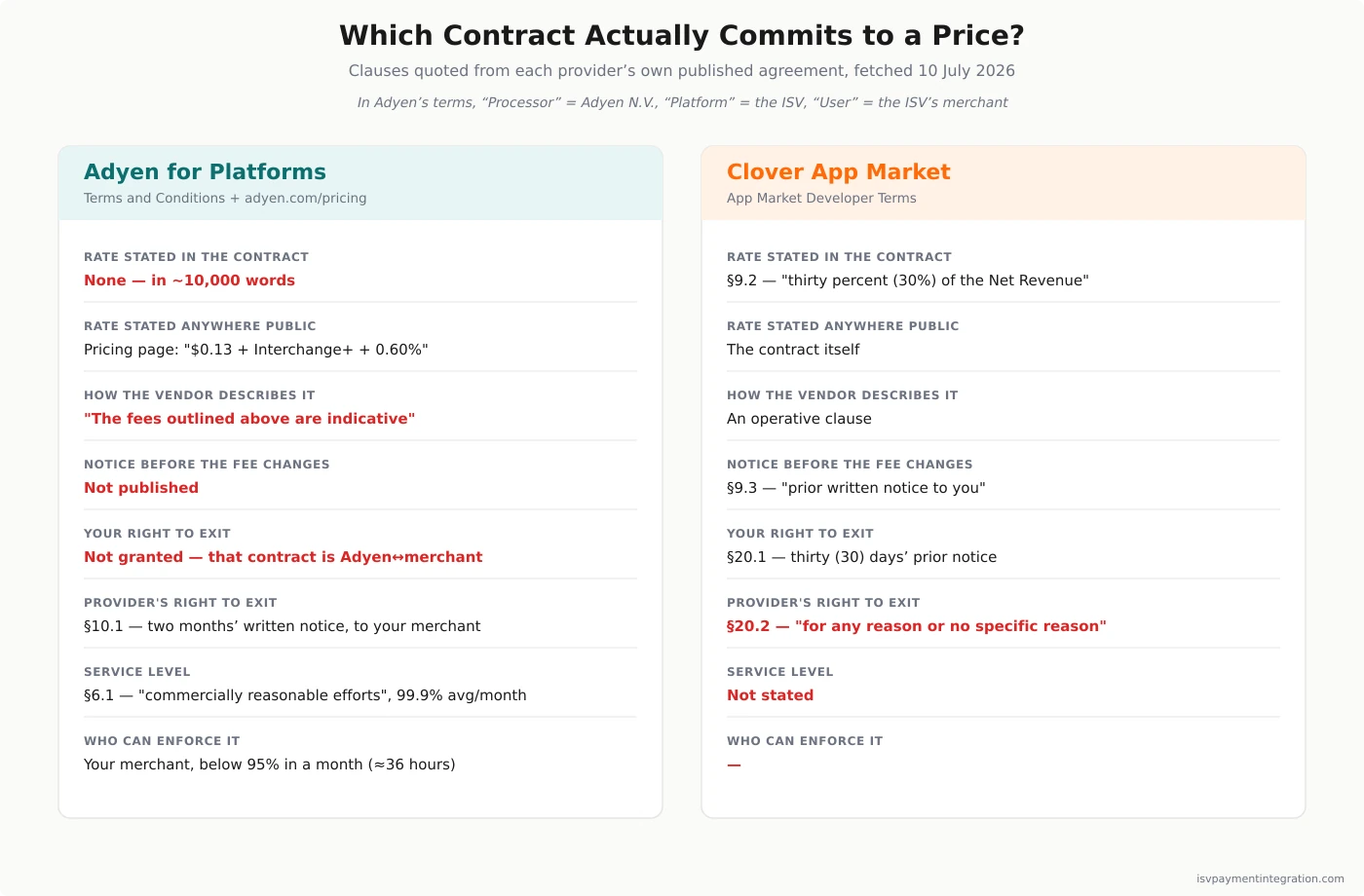

Now open the contract. The Adyen for Platforms Terms and Conditions run to roughly ten thousand words. They contain no rate. The only percentages anywhere in the document are a EURIBOR-plus-2% interest rate on late settlement, a 99.9% uptime target, a 95% termination trigger, and a 50% shareholder test for intra-group transfers. No currency amount appears at all.

Adyen publishes a figure it describes as indicative, and signs a contract that does not mention it.

What Clover Publishes: a Number, and a Notice Period

Clover’s App Market Developer Terms reach “any revenue derived from the Installed Apps” — section 9.1 names subscriptions, in-app features, add-ons and extras as examples — and section 9.2 sets the charge at “thirty percent (30%) of the Net Revenue.” The clause attaches it to “each Installed App,” which will matter later.

That is a stated price in an operative clause. Three neighbouring clauses tell you what it is worth:

- 9.3 — Clover may “amend the amount of the Transaction Fee and/or the Distribution Fee from time to time upon prior written notice to you.” The figure can move, but not silently.

- 9.2(2) — Clover reserves a Distribution Fee covering apps “installed by Merchants for free.” The agreement does not state its amount.

- 9.6 — “You authorize the deduction of the Transaction Fee, Distribution Fee and Developer Taxes from the Net Revenue.”

Section 9 has six subsections. None of them prices a card transaction. The thirty percent is a marketplace commission on software, and it is the only Fiserv-owned ISV figure this page found stated anywhere.

The Contract Comparison, With the Counterparties Named

Here is where most comparisons of these two would cheat, so the counterparty for every clause is named. In Adyen’s Platforms terms, Processor is Adyen N.V., Platform is the ISV, and User is the ISV’s merchant. Clover’s Developer Terms run between Clover and the developer.

| Adyen for Platforms | Clover App Market | |

|---|---|---|

| Rate stated in the contract | none, in ~10,000 words | §9.2 — “thirty percent (30%) of the Net Revenue” |

| Rate stated anywhere public | pricing page, described as “indicative” | the contract itself |

| Notice before the fee changes | not published | §9.3 — “prior written notice to you” |

| Your right to exit | not granted by this agreement — it is Adyen↔merchant | §20.1 — “at any time upon providing Clover with thirty (30) days’ prior notice” |

| Provider’s right to exit | §10.1 — “at least two (2) months’ prior written notice”, given to your merchant | §20.2 — “at any time … for any reason or no specific reason” |

| Service level | §6.1 — “commercially reasonable efforts” toward “an average minimum uptime of 99.9% (measured on a monthly basis)“ | not stated |

| Who can enforce that service level | your merchant, by terminating below 95% monthly availability | — |

Read the table rather than the percentages and the received wisdom inverts. The company that put its price on a marketing page does not promise it in the contract that governs the relationship. The company that buried its price in a developer agreement states the figure, owes you written notice before changing it, and lets you leave in thirty days.

Two honest qualifications, because the table is easy to over-read. Clover’s §20.2 is a genuinely one-sided termination right, and §9.2(2) is a fee the agreement never quantifies. And Adyen’s 95% floor is worth arithmetic: five percent of a thirty-day month is thirty-six hours. A processor can be dark for a day and a half and still clear it. The 99.9% figure above it is an efforts obligation, not a warranty.

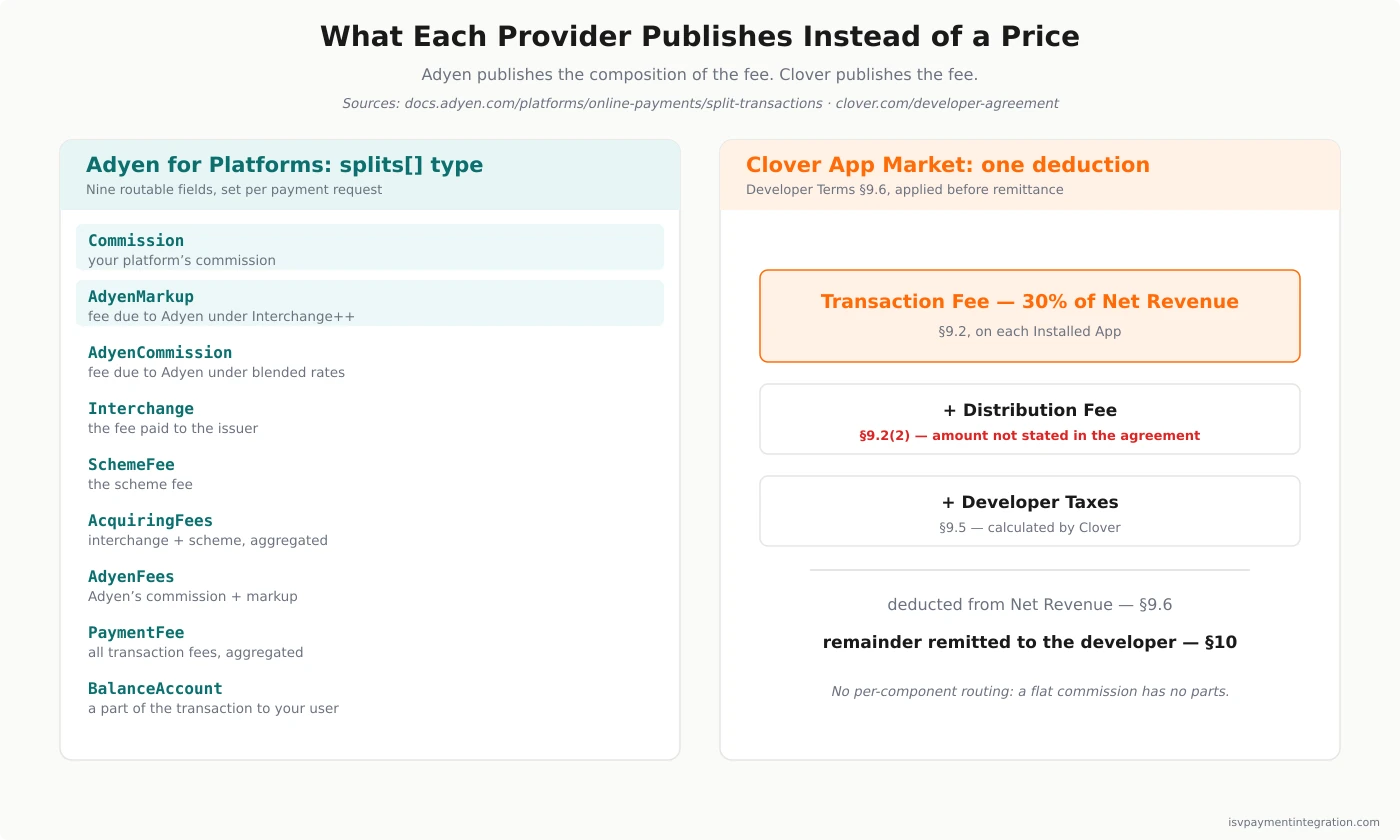

What Adyen Publishes Instead of a Price: a Decomposition

Adyen withholds a committed rate and publishes the composition of the fee instead. The splits array takes a type on every element, and the documented values take a transaction apart.

| Split type | What Adyen’s documentation says it books |

|---|---|

BalanceAccount | a part of the transaction to your user’s balance account |

Commission | ”Books your platform’s commission to your liable balance account.” |

Interchange | ”Books the fee paid to the issuer to the specified account.” |

SchemeFee | ”Books the scheme fee to the specified account.” |

AcquiringFees | the aggregated interchange and scheme fees |

AdyenCommission | ”the transaction fee due to Adyen under blended rates” |

AdyenMarkup | ”the transaction fee due to Adyen under Interchange ++ pricing” |

AdyenFees | Adyen’s commission and markup, aggregated |

PaymentFee | all transaction fees, aggregated |

Because the pricing page’s tooltip identifies the 0.60% row as Interchange++ pricing, AdyenMarkup is the field that carries it — the marketing figure, exposed as a routable line item. And Commission is the ISV’s own margin, named by Adyen, in Adyen’s documentation.

The transaction-fees page makes the routing explicit: “While Adyen deducts all payment-related fees from your platform’s liable balance account by default, you can decide to book them directly to your user.” An ISV can pass interchange to the merchant, keep the scheme fee, absorb Adyen’s markup, or any combination, per payment request.

This is what Adyen means on its Platforms page: “Rather than receiving a set kickback fee from a payments provider, you decide how to price per payment and additional features.” Adyen pays the ISV nothing and takes nothing from its software. It sells wholesale, itemised, and lets the ISV retail.

Clover’s Developer Terms provide a single deduction under §9.6 rather than a set of routable components, because a flat marketplace commission has no components to route.

Nobody’s Money Is in Your Account

It is tempting to read the split array as custody, and to conclude that Adyen lets an ISV hold the money while Clover does not. The documents do not support that, and it is worth saying plainly because it is the mistake this page nearly made.

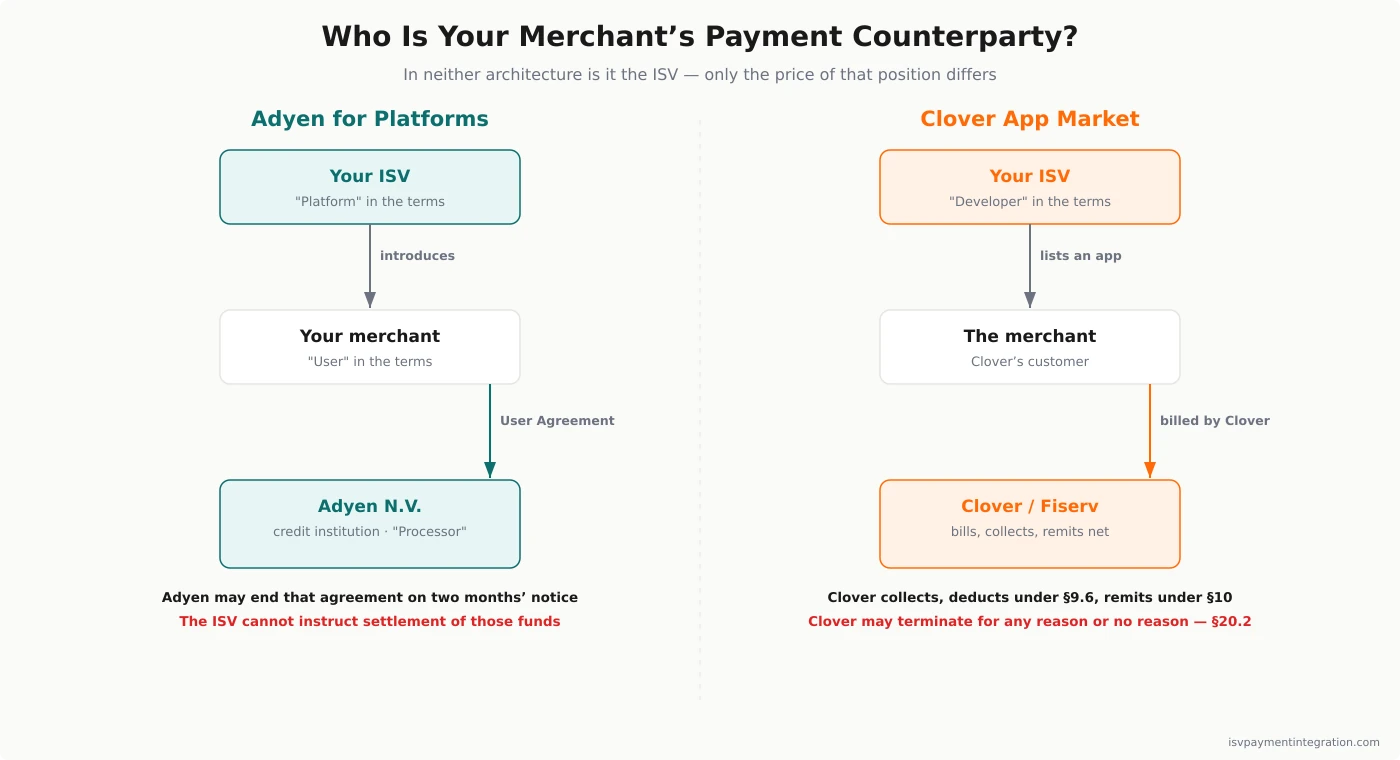

The liable balance account is a ledger position inside Adyen’s own platform. Adyen N.V. is the credit institution. And the Platforms terms are explicit about who may direct the money:

“Platform is under no circumstances entitled to make any individual instructions towards Processor regarding the Settlement of the funds.”

Adyen also deducts from that account without asking: “Adyen deducts all payment-related fees from your platform’s liable balance account by default.” Set that beside Clover’s §9.6 — “You authorize the deduction of the Transaction Fee, Distribution Fee and Developer Taxes” — and the difference is bookkeeping order, not control. Adyen books the transaction to you and then deducts. Clover deducts and then remits. In both cases a larger regulated counterparty holds the funds and helps itself first.

The word “liable” is the one worth keeping. It describes the ISV’s exposure, not its asset.

Neither Architecture Makes You Your Merchant’s Counterparty

This is the asymmetry that actually decides things, and it is visible only once the parties are named.

Under Adyen for Platforms, the merchant an ISV introduces accepts a User Agreement with Adyen N.V. The ISV is Platform — a third party to that agreement. Adyen may terminate that merchant on two months’ notice. The merchant, not the ISV, holds the right to walk if availability falls below 95% in a month. And the ISV may not instruct settlement of its own merchant’s funds.

Under the Clover App Market, the merchant is Clover’s customer. Clover bills them for the ISV’s software, and section 10 — “COLLECTION AND REMITTANCE OF APP FEES TO YOU” — governs what comes back.

So in neither architecture does the ISV own the payment relationship with its own merchant. What an ISV is really choosing is which regulated company will stand between it and its customer, and what that company charges for standing there. Adyen charges a markup on payments and lets the ISV price the merchant. Clover charges thirty percent of the software and lets the ISV skip the payments business entirely.

Both prices buy the same structural position. That is the finding, and it survives every percentage on this page.

Even the Decomposition Doesn’t Give You Your All-In Cost

Adyen’s Interchange++ claim — “we can calculate the cost of each payment even before it is completed” — is a claim about interchange and scheme fees, and it is true of them. It is not a claim about the ISV’s all-in cost, and Adyen’s own documentation says why.

The same transaction-fees page that publishes the split types also lists what cannot be attributed to a single payment. Processing costs are aggregated and apply to refused and cancelled payments too, so they cannot be allocated per transaction. And “any discounts that are derived from tiered pricing structures cannot be allocated to individual payments.”

An ISV on a tiered Adyen contract therefore does not know its true per-transaction cost at authorization. It knows its interchange and its scheme fees at authorization, which is a real and unusual thing to know, and it learns the rest on the invoice. Any model built from the published 0.60% should carry the word indicative through to its output — and should include the minimum invoice, which is a floor an ISV pays regardless of volume and which can consume a small platform’s entire spread.

What the Thirty Percent Actually Buys

Read against the counterparty map, the fee resolves into something more specific than “distribution.”

The thirty percent is the price of the position. Clover contracts with the merchant, invoices the merchant, collects, deducts under §9.6 and remits the remainder under §10. The ISV is never in the flow of funds, never underwrites a sub-merchant, never carries a balance account, and never appears in the merchant’s payment contract. Adyen’s 0.60% buys the mirror position: the ISV prices the merchant, keeps the spread, and takes the obligations that come with standing next to the money.

Neither is the better deal in the abstract. They are prices for opposite jobs, quoted in different units.

One scoping point before either. Section 9.2 attaches its fee to “each Installed App.” Clover’s docs distinguish a native integration — “the POS is an Android app installed on a Clover device” — from a semi-integration, in which an SDK lets existing ISV software drive the device. On the face of the clause, revenue from software that produces no installed app falls outside it. “Installed App” is a defined term, so get the scoping confirmed in writing rather than inferred; Square vs Fiserv works through that hardware-side choice in detail.

Custody Comes With Liability — On Both Sides

Whichever door an ISV takes, it is worth pricing the obligations before the fee.

Under Adyen for Platforms, the ISV stands close enough to the flow of funds to inherit its problems: Article 7 governs Chargebacks and Refunds, Article 11 governs Liability, and Adyen’s general Terms and Conditions provide that “upon termination of the Merchant Agreement for any reason, Adyen shall remain entitled to recover Chargebacks and Chargeback Fees and related Fines.” Exposure outlives the relationship. Sub-merchant onboarding, KYC, AML and MATCH-list screening come with the balance account.

Under the Clover App Market the ISV is further from the money and correspondingly closer to a set-off: the Developer Terms let Clover reimburse a merchant for losses attributed to the ISV’s app and recover them without notice to you, from funds it is already holding. The FAQ below quotes that clause in full, because it is the one an ISV is least likely to have read.

Neither is a hidden trap. Both are the stated price of the position, and both are cheaper to read now than to discover.

Six Clauses to Read Before You Sign Either One

- Clover §9.2(2) — the Distribution Fee covering apps “installed by Merchants for free.” Reserved; the agreement does not state its amount.

- Clover §9.3 — amendment of the Transaction Fee on prior written notice. Thirty percent is the current figure, and the notice obligation is the protection.

- Clover §20.1 and §20.2 — read them together. Thirty days out for you; “for any reason or no specific reason” for Clover.

- Clover §20.3 — on termination other than for your breach, App Agreements for installed apps “continue with full force and effect.” Your obligations to merchants survive the contract that created them.

- Adyen for Platforms §6.1 and §10.2 — the uptime obligation is “commercially reasonable efforts,” and the 95% termination right belongs to your merchant, not to you.

- Adyen for Platforms Articles 7 and 11 — Chargebacks and Refunds, and Liability. Price these before pricing the 0.60%.

For the neighbouring comparisons: Square vs Fiserv reads Clover’s contract against Square’s developer agreement from the hardware side, Stripe vs Fiserv covers a competitor that publishes a platform fee on a marketing page, and Adyen vs NMI sets Adyen’s single-stack model against a gateway built to route across many acquirers. Provider-level detail lives in the Adyen review and the Fiserv review.

Frequently Asked Questions

Which contract actually commits to a price, Adyen’s or Clover’s?

Clover’s. The App Market Developer Terms state the fee in section 9.2 and oblige Clover to give prior written notice before amending it under section 9.3. The Adyen for Platforms Terms and Conditions state no rate anywhere in roughly ten thousand words — the only percentages in the document govern late-settlement interest, uptime, a termination trigger and an intra-group shareholder test. Adyen’s 0.60% lives on a pricing page whose own FAQ calls the published figures “indicative.” A published number and a contractual commitment are different objects, and in this pairing they belong to different companies.

If both providers deduct their fees automatically, what does “liable balance account” actually give me?

Visibility, not control. Adyen’s documentation is explicit that it “deducts all payment-related fees from your platform’s liable balance account by default,” and the Platforms terms bar the platform from making “any individual instructions towards Processor regarding the Settlement of the funds.” What the account does give an ISV is a per-transaction view of the components — interchange, scheme fee, Adyen’s markup, its own commission — and the ability to route each one to a different balance account in the payment request. That is a reporting and pricing capability, not custody. Adyen N.V. is the credit institution, and the funds are inside it.

If Clover holds the money, what happens when a merchant disputes my app’s charges?

Clover’s Developer Terms answer this directly, and it is the clause an ISV is least likely to have read. Where a merchant suffers losses the contract attributes to the developer’s app, then without notice to you, Clover may “reimburse such Merchant for such losses” and recover them either by invoicing the developer — “payable by you on receipt” — or by “withholding any Transaction Fee otherwise due to you.” Because §10 puts Clover in the collection seat and §9.6 authorises deduction before remittance, the money it would withhold is money it is already holding. An ISV cannot dispute a set-off against funds it never touched. Adyen’s arrangement moves the same exposure earlier rather than removing it: chargebacks land against the platform’s liable balance account, and Adyen’s Terms and Conditions let it recover chargebacks and related fines even after the agreement ends.

Can I compare Adyen’s 0.60% to Clover’s 30% to see which is cheaper?

No, and not because one is larger. The 0.60% is a markup on card volume the ISV processes; the thirty percent is a commission on subscription revenue the ISV earns from its own software. Adyen’s Platforms terms take no share of an ISV’s software revenue, so an ISV on Adyen keeps it whole; Clover’s Developer Terms give an ISV no share of payment processing, so an App Market listing yields no processing spread. The comparison that would be meaningful — Adyen’s markup against Fiserv’s CardPointe residual — cannot be made from the documents this page read, because the ISV Partner Program page quotes no rate.

Which one should a vertical SaaS company choose?

Ask what the company is short of. If it is short of merchants, Clover’s App Market sells distribution, a counter-top installed base, and a billing relationship that keeps the ISV out of the payments business, at a stated marketplace rate with a notice period and a thirty-day exit. If it is short of margin and already knows how to find merchants, Adyen for Platforms lets the ISV set the merchant’s price, keep the spread, and see each component of the cost — in exchange for chargeback exposure, sub-merchant obligations, and a rate that is negotiated rather than promised. The percentages describe those trades. They do not decide them.