Stripe vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Stripe and Fiserv sit at opposite ends of the payments industry, and almost every practical difference between them follows from one thing: whether the price is on the website. One of these companies tells a software platform what monetizing payments will cost before anyone picks up a phone. The other underwrites merchants through the banking system, owns the deepest point-of-sale ecosystem in America, and will not show you a rate card until you are three months into a sales cycle.

Feature Comparison

| Feature | Stripe | Fiserv |

|---|---|---|

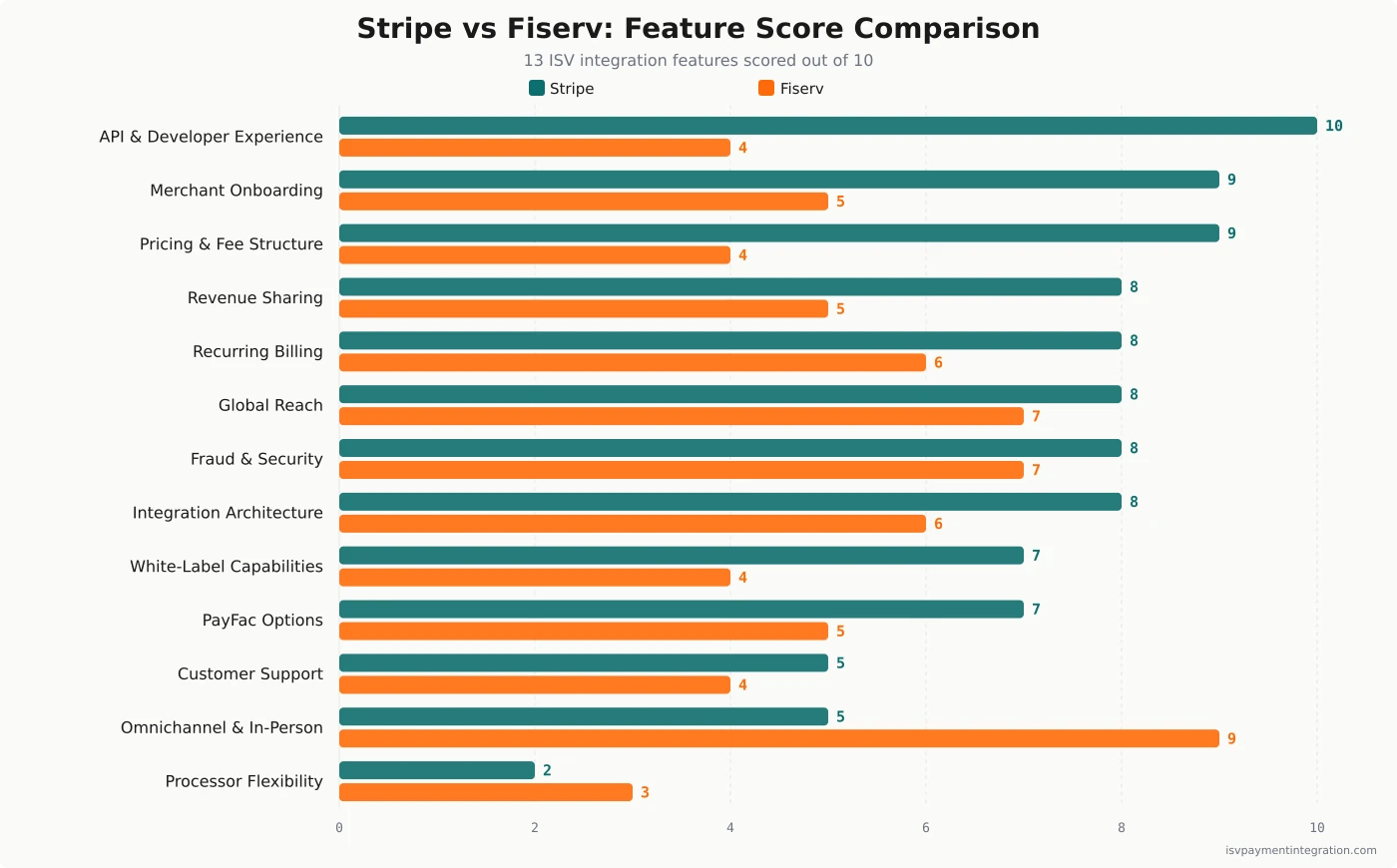

| API & Developer Experience | 10 | 4 |

| Merchant Onboarding | 9 | 5 |

| Pricing & Fee Structure | 9 | 4 |

| Revenue Sharing | 8 | 5 |

| Recurring Billing | 8 | 6 |

| White-Label Capabilities | 7 | 4 |

| Global Reach | 8 | 7 |

| Fraud & Security | 8 | 7 |

| Integration Architecture | 8 | 6 |

| PayFac Options | 7 | 5 |

| Customer Support | 5 | 4 |

| Omnichannel & In-Person Payments | 5 | 9 |

| Processor Flexibility | 2 | 3 |

Get this comparison as a shareable PDF

We'll send the Stripe vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Stripe

Best for developer-led vertical SaaS, marketplaces, and any platform whose merchants are online-first and onboard themselves. Accept a closed processing network, support that thins out below enterprise volume, and card-present capability that is adequate rather than category-leading.

Best for

Fiserv

Best for software serving merchants who transact across a counter, and for platforms whose underwriting risk profile needs bank sponsorship to clear at all. Accept that you will negotiate for months to learn your economics, and that the counterparty lost its chief executive and its president inside four weeks in mid-2026.

Stripe vs Fiserv: The Price Is on the Website, or It Isn’t

Almost every real difference between Stripe and Fiserv falls out of a single question, and you can answer it in about ten seconds without talking to a salesperson.

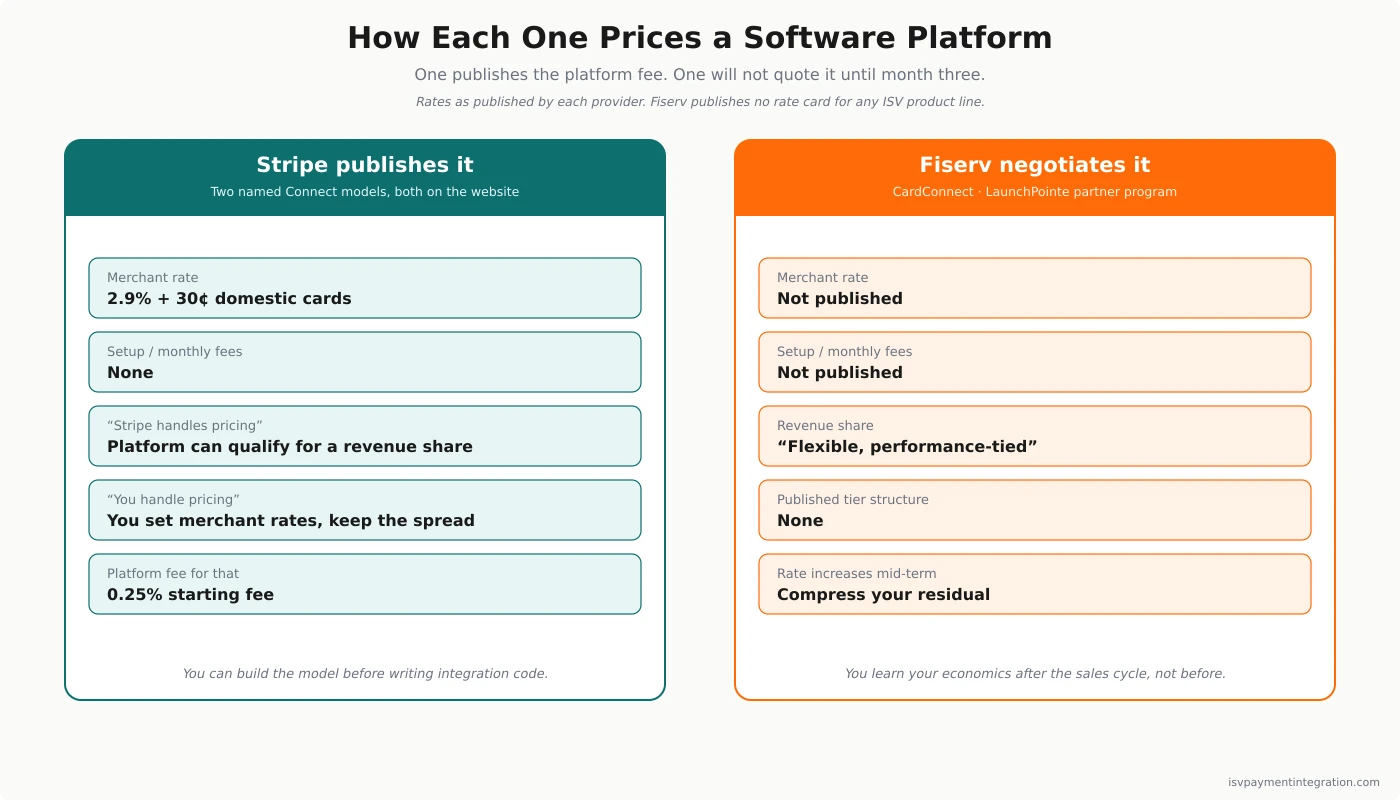

Go to stripe.com. The rate is there: 2.9% + 30¢ per successful domestic card transaction, no setup fees and no monthly fees. Go to the Connect page and the platform economics are there too — Stripe names two models, and tells you that deploying your own payments pricing carries a 0.25% starting fee.

Now try to find out what Fiserv charges a software platform to process a transaction. You cannot. Fiserv publishes no rate card for CardConnect, none for Carat, and none on any of its ISV-facing properties. What a partner earns on payments is negotiated, performance-tied, and disclosed to exactly one audience: the partner who has already spent three months in the sales cycle. The one figure Fiserv does commit to in writing prices software rather than payments — Clover’s App Market Developer Terms take thirty percent of an app’s net revenue.

That is not a criticism dressed as an observation. It is the entire trade. Fiserv’s opacity buys it something real — seven sponsor banks, a point-of-sale ecosystem no API-first company has matched, and underwriting capacity for merchants Stripe would decline. The question this page answers is whether that reach is worth what it costs you in certainty.

Quick Take: An API Company and a Bank-Distribution Company

Stripe sells software platforms a product called Connect, and it is unusually explicit about how a platform makes money on it. Stripe’s own pricing page names two models. Under “Stripe handles pricing for your users,” Stripe sets and collects processing fees from your merchants directly, and your platform “can qualify and earn a revenue share from Stripe” — included at no additional charge. Under “You handle pricing for your users,” recommended for marketplaces and platforms that want to deploy their own pricing strategy, your platform sets the rates its merchants pay, collects fees on every transaction, and keeps the spread. Stripe charges a 0.25% starting fee for that privilege, plus per-account and per-payout fees. Both models are on the website. Neither requires a phone call to understand.

Fiserv sells software platforms through CardConnect and its ISV Partner Program, and separately through Clover, which is a fundamentally different proposition. Behind both stands First Data Merchant Services, a registered ISO of seven sponsor banks — Wells Fargo, Deutsche Bank, PNC, MVB, Pathward, Citizens, and KeyBank. That is a distribution and underwriting moat no independent processor can replicate, and it is the strongest argument on Fiserv’s side of this page. The economics are negotiated, the revenue share is described in Fiserv’s own partner materials as flexible and performance-tied, and nothing about it is published.

The company behind that moat is having a difficult year. Chief executive Michael Lyons resigned on June 12, 2026, effective immediately, taking no severance and no accelerated equity vesting. Takis Georgakopoulos — previously Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank — replaced him two days later. On July 7, president Dhivya Suryadevara resigned “for good reason.” First-quarter 2026 revenue fell 2.0% and operating income fell 34.2%. Two securities class actions over statements about Clover’s growth are pending, both in the Southern District of New York, and nothing has been adjudicated. Our Fiserv review covers all of it.

Published Economics Versus Negotiated Economics

Here is what “published” is actually worth to a software company, stated concretely.

If you are modelling a payments business on Stripe, you can build the spreadsheet today. You know the merchant-facing rate. You know the 0.25% starting fee for running your own pricing. You know there is no setup fee and no monthly minimum. You can compute your take rate at every volume tier before you write a line of integration code, and you can decide whether payments is a viable revenue line before committing engineering headcount to finding out.

If you are modelling the same business on Fiserv, you cannot do any of that. You will enter a negotiation whose outcome depends on your volume, your vertical, your merchant risk profile, and how well you negotiate. You will emerge with a residual structure that neither you nor your competitors can benchmark, because none of it is public. And Fiserv retains the ability to raise the underlying processing rates during your term — which compresses your residual without asking you.

Neither approach is dishonest. Negotiated pricing genuinely can beat published pricing at scale; that is why every large platform eventually negotiates. But the platform that negotiates from a published baseline has a floor, and the platform negotiating against an unpublished one has only whatever leverage its volume affords. Model both against your own merchant base with our revenue calculator, and read the Stripe pricing breakdown for what the headline rate conceals at scale — the effective blended rate is rarely the number on the homepage.

Onboarding: Minutes Versus Months

Stripe Connect onboards a sub-merchant programmatically. Your platform calls an API, the merchant completes a hosted flow, Stripe makes the underwriting decision, and the merchant can accept payments the same day. Stripe carries the risk of that decision. This is the single largest reason developer-led platforms default to Connect: it removes underwriting from your critical path entirely.

Fiserv’s onboarding runs through channels built for a different era. CardConnect boards merchants through partner and bank relationships on a timeline measured in weeks. That slowness buys something — Fiserv’s sponsor banks will underwrite merchant categories that Stripe declines outright, and for platforms serving higher-risk verticals, “slow but approved” beats “instant but rejected” every time.

Ask yourself which failure mode kills your business. If a merchant abandoning signup because onboarding took four days is fatal, Stripe. If half your addressable merchants cannot get approved by an API-first processor at all, Fiserv, and the wait is the price of admission.

Point of Sale: Where Fiserv Simply Wins

Stripe Terminal exists. It is a well-built card-present product, and for platforms whose merchants occasionally take an in-person payment it is entirely sufficient.

Clover is not that. Clover is a hardware ecosystem — countertop stations, handhelds, kitchen displays, an app marketplace with real distribution — that merchants build their operating day around. If your merchants run restaurants or retail storefronts, and they are going to put a device on a counter, that device is very likely a Clover, and your software’s job is to integrate with it rather than replace it.

The trade is ownership. On Clover, the merchant is Clover’s customer. The hardware carries Clover’s logo, the merchant dashboard is Clover’s, and your software is an app in Clover’s marketplace. You gain access to an enormous installed base and you surrender the merchant relationship. Platforms that want the merchant and the brand should read our embedded payments guide before assuming reach and economics are the same thing.

The PayFac Question

Neither of these is a route to becoming a registered payment facilitator, and it is worth being precise about why.

Stripe Connect gives a platform facilitator-like economics and control — you onboard merchants, you can set their pricing, you keep the spread — while Stripe remains the facilitator of record and carries the compliance obligation. For the large majority of software platforms that is the correct answer, because PayFac registration is expensive, slow, and mostly a way to acquire regulatory obligations you were previously renting.

Fiserv offers payment facilitation through specific arrangements, but publishes no progression from CardConnect reseller to facilitator. A platform that outgrows the residual model re-platforms rather than graduates.

If a published ladder toward true facilitation is what you actually want, neither company on this page offers one — but Worldpay vs Fiserv covers a vendor that does, and PayFac-as-a-Service explains what the middle rung obliges you to take on.

Counterparty Risk, Honestly Stated

Stripe is a private company that does not publish audited financials. That is its own species of opacity, and a platform betting its payment stack on Stripe is betting on a company whose numbers it cannot inspect. Stripe has been operating at very large scale for over a decade and shows no sign of distress, but “no sign of distress” is a weaker statement than “here are the filings.”

Fiserv publishes everything, which is how we know its first quarter of 2026 was bad. Total revenue fell 2.0% to $5.027 billion. Operating income fell 34.2% to $918 million. Its Merchant Solutions segment was flat. Two securities class actions are pending: the lead case, In re Fiserv, Inc. Securities Litigation, No. 1:25-cv-06094, filed in the Southern District of New York, alleges that Fiserv’s statements about Clover’s growth were false or misleading; a second action was consolidated in Wisconsin and transferred to New York in April 2026. Fiserv has accrued $26 million against its legal proceedings and estimates possible exposure above that accrual at $0 to roughly $160 million. Per its own filing, “the defendants have not yet answered or otherwise responded to any of the complaints.” Nothing is adjudicated. Fiserv raised €1 billion of senior notes in June 2026, which distressed borrowers cannot do.

The asymmetry is instructive. With Stripe you are exposed to risks you cannot see. With Fiserv you are exposed to risks you can read in a 10-Q, including the fact that the executives who negotiate partner terms changed twice in one quarter. Neither is obviously worse. Only one is quantifiable.

Where Each Platform Wins

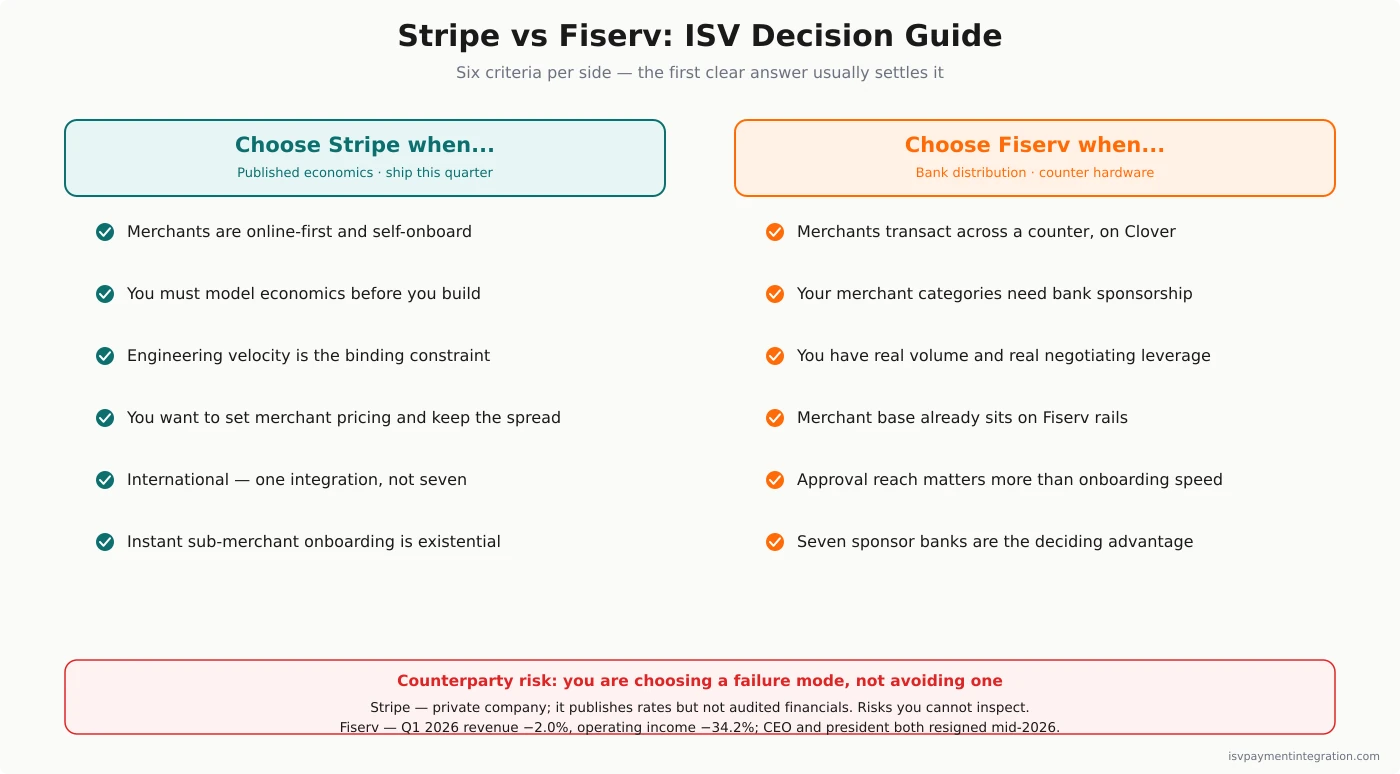

Choose Stripe when your merchants are online-first and onboard themselves; when you want to model payment economics before writing integration code; when engineering velocity is the binding constraint on your roadmap; when you want to set your own merchant pricing and keep the spread; or when your platform is international and you would rather have one integration than seven.

Choose Fiserv when your merchants transact across a counter and Clover is the device they will use; when your merchant categories need bank sponsorship to get approved at all; when scale and negotiation leverage genuinely put you in a position to beat published rates; or when your merchant base already sits on Fiserv rails and switching costs dominate the arithmetic.

Choose neither when you want to own the merchant relationship outright, brand the entire payment experience, and see a published progression toward facilitation. That is PayFac-as-a-Service territory. See Worldpay vs Fiserv for an incumbent that publishes such a ladder, and Global Payments vs Fiserv for the parent-company view of the same choice.

Stripe vs Fiserv: ISV Decision Guide

- Do your merchants take payments across a counter? If yes, and the device will be a Clover, that usually settles it.

- Can your merchant categories get approved by an API-first processor? If not, bank sponsorship is not a nice-to-have.

- Do you need to model payment economics before you build? Only one of these publishes the numbers to do that.

- Is engineering velocity or underwriting reach your binding constraint? They point in opposite directions.

- Will you set your own merchant pricing? Stripe charges a published starting fee for it. Fiserv will quote you.

- How much volume do you bring? Negotiated pricing beats published pricing only when you have leverage. Be honest about whether you do.

- Which opacity can you live with — a private company’s unpublished financials, or a public company’s unpublished rate card?

For adjacent evaluations, see NMI vs Stripe if an unbundled gateway is on your list, Stripe vs Adyen for the enterprise end of the API-first market, and Authorize.net vs Fiserv for a gateway-first alternative to the incumbent.

Frequently Asked Questions

Is Stripe cheaper than Fiserv for an ISV?

Unanswerable as asked, and that is the point. Stripe publishes its rates: 2.9% + 30¢ per domestic card transaction with no setup or monthly fees, and a 0.25% starting fee for platforms that deploy their own payments pricing. Fiserv publishes no rate card for any ISV-relevant product line. A high-volume platform with real negotiating leverage can often beat Stripe’s published rate through Fiserv’s interchange-plus structure. A platform without that leverage usually cannot, and will spend months finding out.

Can an ISV earn revenue share with Stripe Connect?

Yes, through either of two published models. If Stripe handles pricing for your merchants, your platform can qualify to earn a revenue share from Stripe at no additional charge. If you handle pricing, your platform sets the rates its merchants pay, collects fees on each transaction, and keeps the spread, with Stripe charging a 0.25% starting fee plus per-account and per-payout fees. Both models are described on Stripe’s own pricing pages, which is more than can be said for most of the industry.

Does Fiserv publish ISV revenue-share rates?

No. Fiserv publishes no rate card and no revenue-share structure for CardConnect, Clover, or Carat. Its partner materials describe revenue share as flexible and performance-tied. Any specific percentage you have seen quoted for Fiserv’s ISV economics does not come from Fiserv. Everything is negotiated per partner, and the outcome depends on your volume, vertical, and leverage.

Is Stripe or Fiserv better for in-person payments?

Fiserv, decisively. Clover is the deepest point-of-sale hardware ecosystem an ISV can integrate with — countertop stations, handhelds, kitchen displays, and an app marketplace with genuine distribution. Stripe Terminal is a capable card-present product but is not an ecosystem merchants organize their operations around. The trade is that on Clover, the merchant becomes Clover’s customer rather than yours.

Should Fiserv’s lawsuits and executive departures rule it out?

No, but they should change what you sign. Nothing has been adjudicated — per Fiserv’s own Form 10-Q, defendants have not yet answered any complaint, and the company intends to defend vigorously. Fiserv remains a roughly $21 billion revenue business with seven sponsor-bank relationships and demonstrated capital-markets access. What changed is that the executives who negotiate partner economics turned over twice in one quarter. Insist on a written rate-lock, at least ninety days’ notice before any fee change, and the right to walk away without penalty if the markup climbs past a ceiling you set in advance.