Checkout.com vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Comparing these two on price is not difficult. It is impossible. Neither company discloses what a software business will pay or earn, and both describe that silence as a virtue rather than an omission. A feature checklist rescues nothing either, because the two barely compete for the same merchant. What is left is a question about leverage — and leverage, unlike a rate card, is something you can measure about yourself before either sales team returns your call.

Feature Comparison

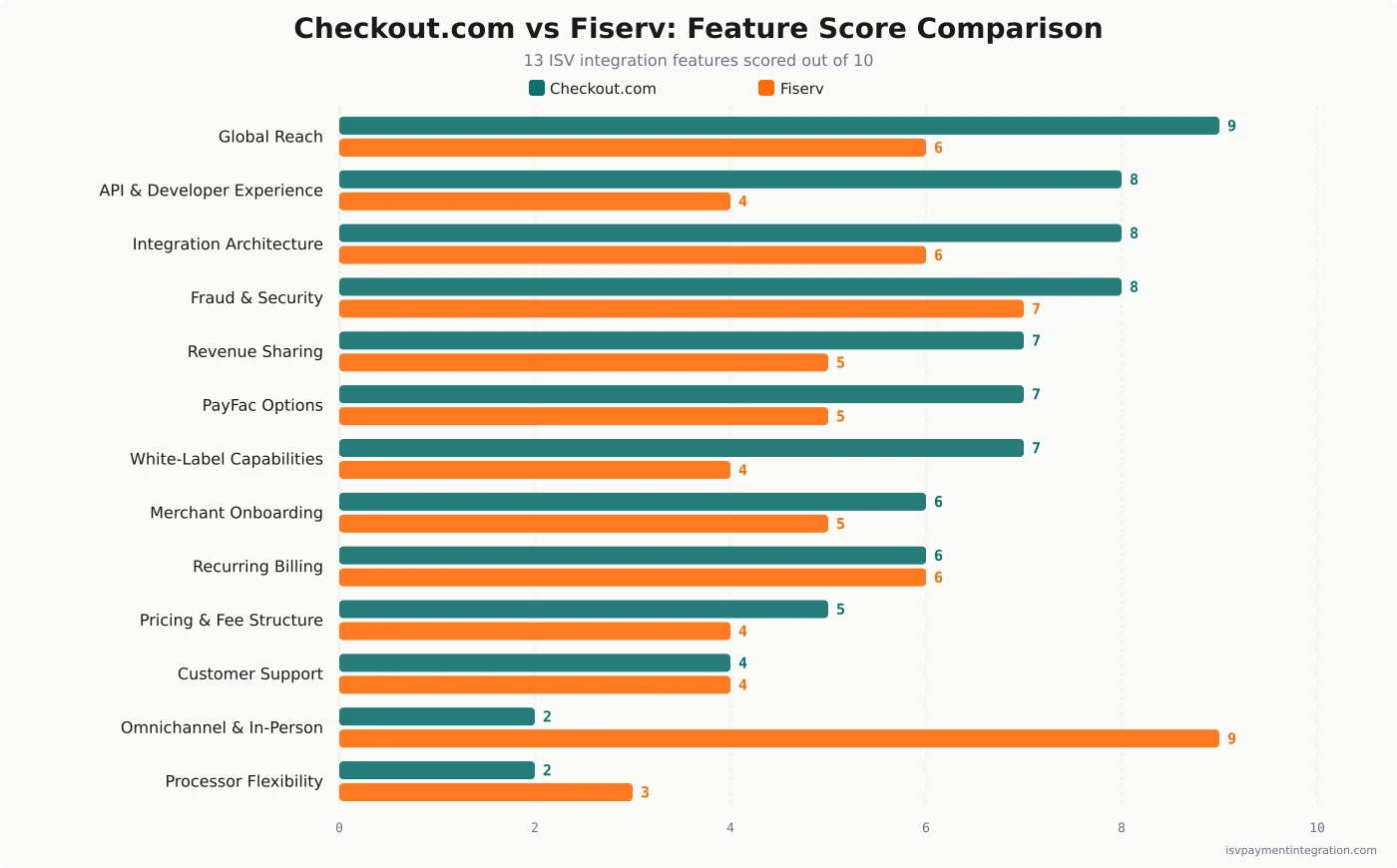

| Feature | Checkout.com | Fiserv |

|---|---|---|

| Global Reach | 9 | 6 |

| API & Developer Experience | 8 | 4 |

| Integration Architecture | 8 | 6 |

| Fraud & Security | 8 | 7 |

| Revenue Sharing | 7 | 5 |

| PayFac Options | 7 | 5 |

| White-Label Capabilities | 7 | 4 |

| Merchant Onboarding | 6 | 5 |

| Recurring Billing | 6 | 6 |

| Pricing & Fee Structure | 5 | 4 |

| Customer Support | 4 | 4 |

| Omnichannel & In-Person Payments | 2 | 9 |

| Processor Flexibility | 2 | 3 |

Get this comparison as a shareable PDF

We'll send the Checkout.com vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Checkout.com

Best for marketplaces, PSP-shaped platforms, and international commerce software whose sub-merchants transact entirely online, and that will use Commissions to charge each user a different fee. Accept that there is no card-present product at all, no published rate, and a private company whose financials you cannot inspect.

Best for

Fiserv

Best for vertical software in restaurants, retail, salons, and field services, where the merchant runs the day on a Clover — and for platforms whose merchant categories only clear underwriting inside a bank-sponsored ISO. Accept a revenue share you do not control, and a counterparty whose chief executive and president both walked out inside four weeks.

Checkout.com vs Fiserv: Neither Company Will Tell You the Price

Ten minutes of research lands you in the same cul-de-sac twice.

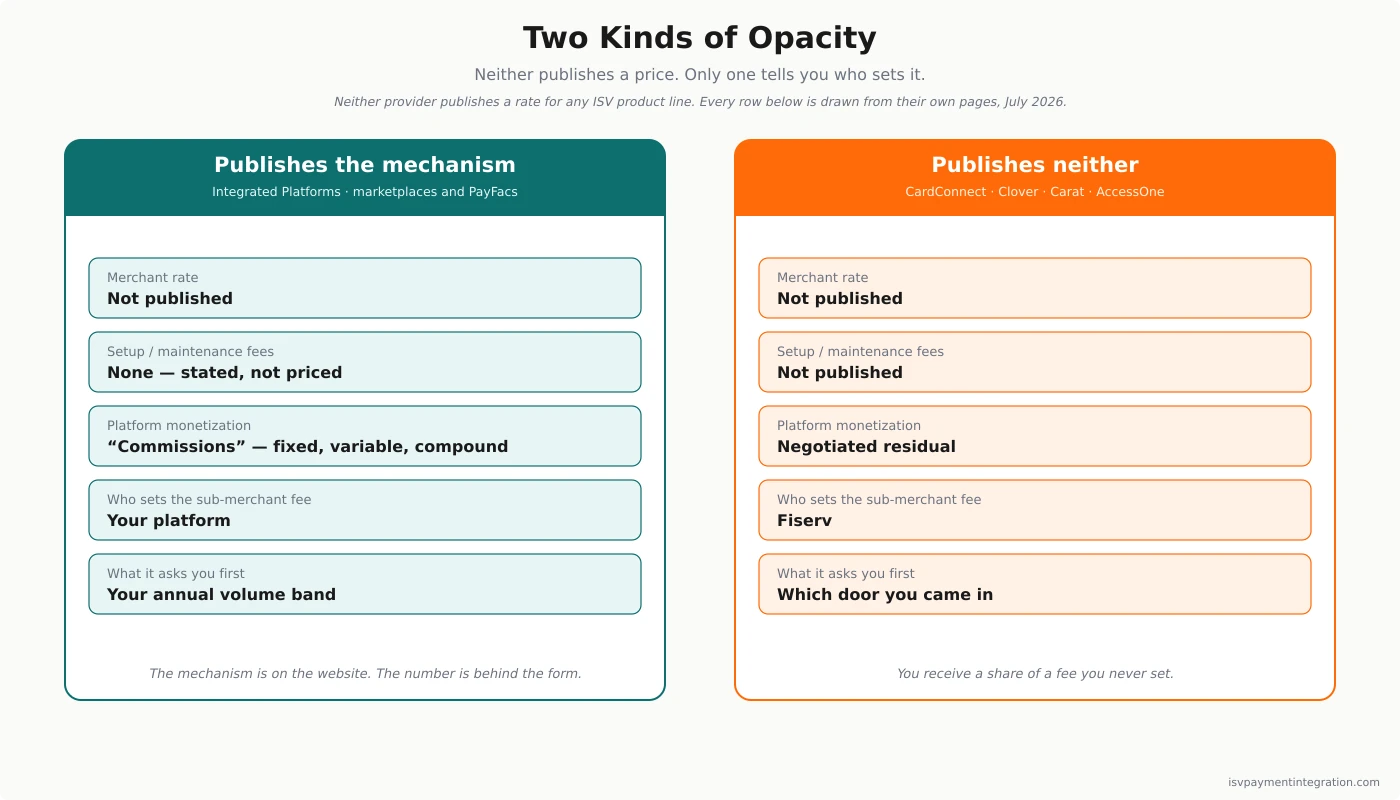

Checkout.com’s pricing page is headed, without apparent irony, “Refreshingly transparent pricing.” It names three structures — “Fully flat-rate,” “Simple interchange++ fees,” and “Free for charities” — and attaches a number to exactly none of them. In place of a number it offers a sentence: “Your business deserves tailored pricing based on your needs.” Underneath the sentence is a form.

Fiserv does not have that page. No rate card exists for CardConnect, none for Carat, and none for Clover’s processing. Nor is there an equivalent sentence explaining the absence, because Fiserv never claimed transparency in the first place and therefore owes no explanation for the lack of it. Clover’s App Market Developer Terms do publish one figure — a thirty percent cut of an app’s net revenue — but that prices the software, not the payment.

So both refuse. If you are a software company choosing where to embed payments — a marketplace, a vertical SaaS, anything with sub-merchants to onboard — you have just discovered that the two most important numbers in your business model are unavailable from both vendors on the shortlist.

What makes this a decision rather than a coin flip is that they refuse differently, and the difference tells you which of them you can negotiate with.

Quick Take: A Sales Form and a Switchboard

Checkout.com sells to software through a product it calls Integrated Platforms, positioned on its own page as “Payments for the platform economy” and aimed at marketplaces and payment facilitators by name. For a company that publishes no prices, its published mechanics are unusually specific. Money movement is broken into three named capabilities. Split payments divide funds “at authorization or capture” across multiple accounts. Balance transfers shift debits, credits, and refunds between accounts inside your platform. And Commissions — the one that matters — promises to “Earn on every payment with more control over commission types, including fixed, variable and compound fees per user.” Onboarding automates identity verification with real-time KYC and KYB, contextual fields, and instant status updates. Every button on the page reads some version of contact sales. In the United States, money transmission is provided by Checkout US Inc. under NMLS #1791692 — a licensed transmitter, not a bank.

Fiserv resists a single description, because Fiserv is four businesses wearing one logo, and an ISV that knocks at the wrong one loses months finding out. CardConnect is the gateway-and-embedded-payments route most software companies actually want. Clover is a point-of-sale operating system on which the merchant becomes Clover’s customer and your product becomes an app in Clover’s marketplace. Carat handles enterprise orchestration; AccessOne does patient financing.

Where does the money actually come from? Fiserv answers that in footers, and the answer changes depending on which footer you read. Its merchant-services site states: “Merchant services provided by First Data Merchant Services LLC, a registered Independent Sales Organization of Wells Fargo Bank, N.A.; Deutsche Bank AG; PNC Bank N.A.; MVB Bank; Pathward, N.A.; Citizens Bank, N.A.; and KeyBank, N.A.” Seven banks. But CardConnect — the door most software companies come in through — discloses a different roster on its own site: “CardConnect is a registered ISO of Citizens Bank, N.A., Providence, RI, KeyBank N.A., Cleveland, OH, Pathward N.A., Sioux Falls, SD, PNC Bank, N.A., Pittsburgh, PA, and Wells Fargo Bank, N.A., Concord, CA.” Five. No Deutsche Bank. No MVB.

Both were retrieved in July 2026. Both are accurate. The gap between them is the point: the institutions whose risk appetite decides which of your merchants get approved depend on which Fiserv entity your paper is with, their names appear in no pitch deck and no pricing page, and you cannot infer the roster for your door from the parent company’s own disclosure. The economics of every one of these paths are negotiated privately and published nowhere.

One company hands you a form. The other hands you a switchboard.

Commissions Versus Residuals: Who Sets the Fee

This is where the symmetry breaks, and it breaks hard.

Opacity has two axes, not one: what is hidden, and who controls the hidden thing. Checkout.com hides the number and publishes the mechanism. Commissions is a product feature with a documented shape — fixed, variable, or compound, applied per user — which means your platform decides what each sub-merchant pays. You are the pricing authority. What you do not know in advance is your own cost basis.

Fiserv hides the number and offers no mechanism at all. A CardConnect partner does not set merchant pricing; a CardConnect partner receives a residual, which Fiserv’s partner materials describe as flexible and performance-tied. The distinction is not semantic. In the first arrangement your margin is a spread you engineer, priced by you, against customers who are yours. In the second your margin is a percentage that someone else computes, from a schedule you never saw, on a fee you never quoted.

An ISV that has never run payments hears both as “revenue share.” They are not the same asset. One is a lever. The other is a dividend.

The Volume Band Is the Rate Card

Fill in Checkout.com’s contact form and it will, before anything else, ask you to select your annual processing volume in US dollars from nine brackets: not processing yet, $0–1 million, $1–10 million, $10–25 million, $25–100 million, $100–250 million, $250 million–$1 billion, $1–5 billion, and $5 billion-plus. It also asks which products interest you, and Integrated Platforms is one of the checkboxes.

Read that form as what it is. It is the rate card. Not because it contains rates, but because it announces the single axis along which your rate will be set, before a human being has spoken to you. Checkout.com is telling you, in the politest possible language, that the answer to “what will this cost” is a function of one variable, and inviting you to state the value of that variable yourself.

That is more information than it looks like. Procurement guidance published by third-party advisers puts the genuine negotiating threshold with tier-one acquirers in the tens of millions of dollars of annual processed volume; below it, platforms are described as negotiating from a weak position. Checkout.com’s own bracket structure is consistent with that shape — it distinguishes finely at the bottom and coarsely at the top, which is what a form does when the interesting conversations start several rungs up. Model your own numbers against it with the revenue calculator before you fill anything in, and read the Checkout.com pricing breakdown for what the twenty-five-odd named fee categories on its minimum-billing schedule imply about the shape of a real invoice.

Fiserv Hides a Counterparty, Not Just a Number

Now try the same exercise on Fiserv and notice that there is no form to fill in, because there is no single thing to ask.

The first question Fiserv’s structure poses is not how much volume do you have but which door did you come in. An e-commerce platform belongs at CardConnect. A restaurant-vertical SaaS belongs at Clover, on very different terms. A large enterprise belongs at Carat. And underneath CardConnect sit five sponsor banks rather than the seven standing behind Fiserv’s merchant business at large, which means the risk appetite governing your merchant approvals is set by a group of institutions you cannot enumerate from the parent’s disclosure and who never join the call.

You therefore cannot benchmark the deal you are offered, because you cannot identify the party whose economics it reflects. Two software companies of identical size can sign materially different CardConnect agreements, and neither will ever find out. Nothing about this is unusual by the standards of bank-sponsored acquiring. It is simply a different species of unknown than a withheld percentage. Checkout.com does not publish a price. Fiserv does not identify a counterparty.

There is a version of this that favours Fiserv, and it should be said plainly. Sponsor banks will approve merchant categories that a licensed money transmitter running a closed acquiring stack declines outright. If a meaningful share of your addressable merchants cannot get boarded at all by an API-first processor, an unpublished residual from an institution that will board them beats a published mechanism from one that will not.

Where the Counter Ends the Argument

For a large class of software companies this entire essay is moot, and the reason fits in one sentence: Checkout.com does not sell a card reader.

Not a limited one. Not a competent-but-secondary one. As of July 2026, Checkout.com’s published product catalogue lists no terminal, no reader, and no in-person SDK: it names Accept Online, Flow, Payouts, Issuing, Payment Processing, Fraud Detection, Authentication, Intelligent Acceptance, Identity Verification, Vault, Real-Time Account Updater, and Network Tokens. Card-present acceptance is a category it has, on the evidence of its own site, chosen not to enter.

Clover, meanwhile, is the reason a great many vertical SaaS companies talk to Fiserv in the first place — countertop stations, handhelds, kitchen displays, and an app marketplace with genuine merchant distribution. If your merchants run restaurants, salons, retail floors, or field-service routes, a device is going on that counter, and the odds are good it is already a Clover.

Notice what the Clover route does to this page’s central question. Checkout.com withholds a number from you. Clover withholds the merchant. Board through Clover and the person tapping the card is Clover’s customer — billed by Clover, supported by Clover, looking each morning at Clover’s dashboard — and the fee that customer pays becomes one more figure you neither set nor see. The reach is entirely real. So is the third layer of opacity you are buying it with, and our embedded payments guide is mostly about platforms that worked that out a year too late.

Cross-Border Reach Versus Cross-Channel Reach

The geographic profiles invert the point-of-sale one.

Checkout.com’s pricing page claims processing in more than 150 currencies with domestic acquiring coverage in more than 45 countries, and the company maintains licensed legal entities across ten jurisdictions. It was built for platforms whose sub-merchants sit in different countries from their buyers, and its settlement and FX machinery reflects that origin.

Fiserv’s Q1 2026 Form 10-Q attributes roughly 16% of revenue to EMEA, LATAM, and APAC combined. The remainder is North America. Fiserv is not a small international business in absolute terms, but it is structurally a domestic acquirer with international operations attached, and the deep integration — the sponsor banks, the Clover installed base, the ISO channel — is American.

So the two forms of reach do not compete; they barely intersect. One provider extends across borders. The other extends across channels. A platform that needs both is running two integrations regardless of what any comparison page says, which is worth knowing before you treat this as an either-or.

Which Negotiation Can You Actually Win?

Collapse everything above into one question, and it is not a question about price. It is a question about whether you can even see the board you are playing on.

At Checkout.com, the axis is disclosed. The form tells you that your rate is a function of annual processed volume, and it tells you before a human being has spoken to you. That is a negotiation you can prepare for. You can work out, in an afternoon, whether the bracket you can honestly tick puts you in front of someone with discretion. If it does, tailored pricing follows, and Commissions lets you turn that cost basis into per-user margin however you like. If it does not, you will still be sold to — but you will be sold the pricing your bracket implies, and you will have known that going in.

At Fiserv, the axis is not disclosed, and that is the whole problem. A residual described only as “flexible and performance-tied” does not tell you what performance means. It might mean volume. It might mean merchant count, or vertical, or how much your book flatters whichever sponsor bank sits behind your paper. Nothing is published, so nothing can be modelled. The one form of leverage you can be confident of is asymmetric need: whether Fiserv’s channel wants what you bring — a vertical it cannot reach, merchants only its banks will board — more than you want what it has.

That is the honest asymmetry, and it is sharper than a price comparison. Checkout.com lets you compute your negotiating position before you enter the room. Fiserv does not let you compute it at all, and the exchange rate between what you bring and what you get is disclosed to you only once you are inside. Neither is disqualifying. But only one of them can be prepared for, and finding out the hard way costs a two-quarter sales cycle.

If neither leverage is one you hold, the correct move may be neither company. A published progression toward true facilitation does exist elsewhere in this market: Worldpay vs Fiserv covers a vendor that names its rungs, while the obligations you inherit by climbing them are set out under PayFac-as-a-Service. If the whole exercise is unfamiliar, start with what a payment facilitator actually is before negotiating to become one.

Counterparty Risk Is the Same Question, Asked Backwards

Run the two axes over the risk, and something falls out that the pricing section only hinted at. Each company is opaque on exactly one axis. They are opaque on opposite ones.

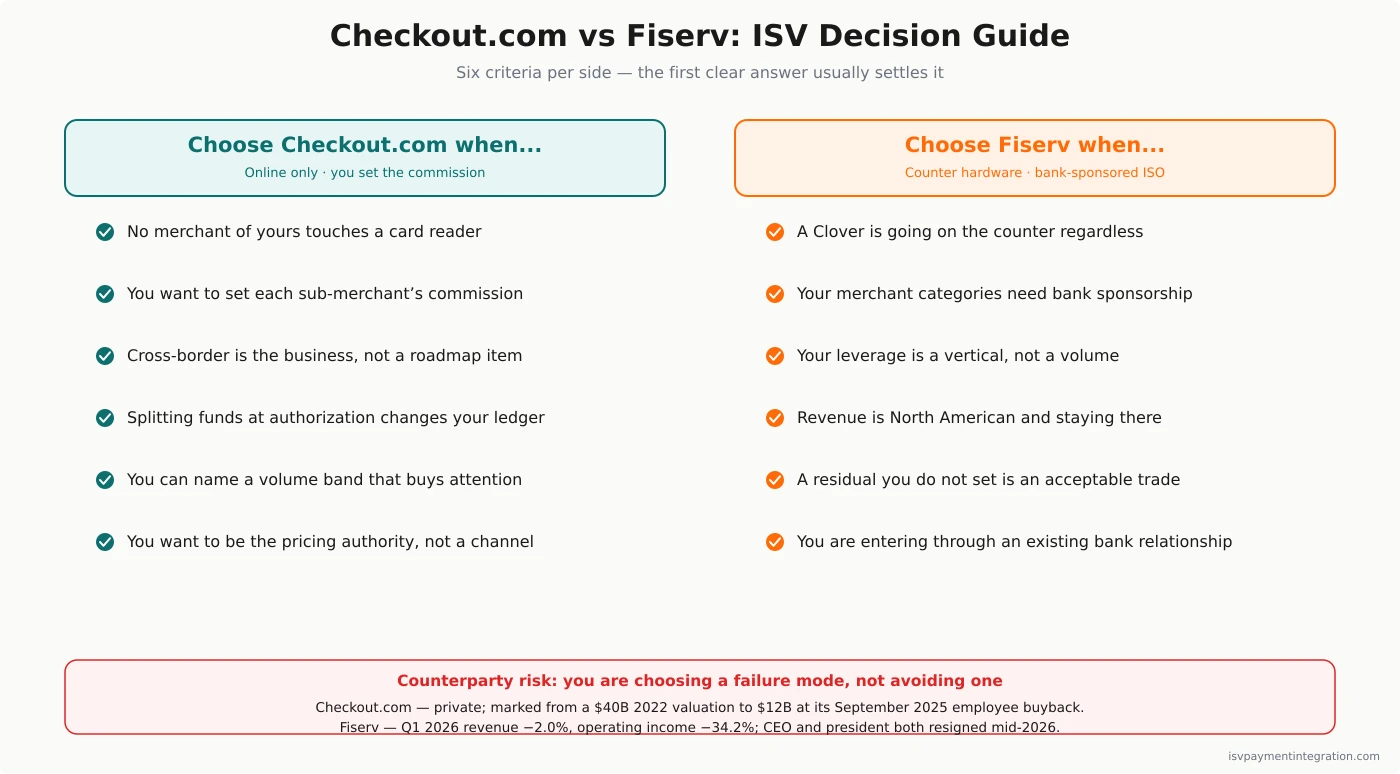

With Checkout.com you can identify your counterparty. It is one company selling one platform product. In the United States, per its own site footer, money transmission is provided by a single named entity, Checkout US Inc., under NMLS #1791692. What you cannot see is how that company is doing, because it is private and publishes no audited financials. The public arc runs from a $40 billion valuation at its 2022 Series D, to an internal mark of $9.35 billion in 2023, to a $12 billion valuation at an employee share buyback in September 2025 — three different kinds of number, not one trend line. The company states, unaudited, that it has returned to EBITDA profitability at a margin above 10% on volume exceeding $300 billion. None of it can be checked against a filing, because no filing exists. Public review sentiment is sharply split, with accounts that have a dedicated manager describing a different company than accounts without one.

With Fiserv you can see precisely how the company is doing, and as of its most recent quarter it is not good. Per its Q1 2026 Form 10-Q, revenue came in at $5.027 billion, down 2.0% year over year, and operating income dropped 34.2% to $918 million. Merchant Solutions, the segment an ISV actually sells into, was flat. Michael Lyons stepped down as chief executive with immediate effect on June 12, 2026. Fiserv’s Form 8-K says his exit “was not the result of any disagreement with the Company,” and records that he received only accrued salary. Takis Georgakopoulos succeeded him on June 14, 2026. On July 7, 2026, president Dhivya Suryadevara resigned “for good reason” — a contractual term meaning a qualifying event on the employer’s side, not a finding against anyone.

Two securities class actions are pending in the Southern District of New York. The first concerns Clover: it alleges that what Fiserv told the market about that unit’s growth was false or misleading. The second alleges the same of statements made in connection with second-quarter 2025 earnings. Both are allegations, and only that. Fiserv’s own Form 10-Q records that, as of that filing, “the defendants have not yet answered or otherwise responded” to a single complaint, and the company says it intends to defend vigorously. Nothing has been adjudicated. Separately, and across its legal proceedings as a whole rather than these two cases in particular, Fiserv reports an accrual of $26 million and estimates possible exposure in excess of that accrual at $0 to roughly $160 million. In June 2026 it raised €1 billion of senior notes, which is not something a distressed borrower does. Our Fiserv review works through all of it.

What you cannot see at Fiserv is who, precisely, you are contracting with. The product line sets your terms. The sponsor bank behind it governs your merchants’ approvals. And the leadership above both changed twice inside four weeks. One biographical detail is worth more attention than it has received, on its own and without any inference attached to it: Georgakopoulos ran payments for J.P. Morgan’s Corporate & Investment Bank as its Global Head from 2017 until 2024 — the franchise that competes with Fiserv hardest for ISV embedded payments. Whatever Fiserv’s partner strategy becomes, it will be shaped by someone who spent seven years on the other side of it.

So the risk mirrors the price, but along the other axis. Checkout.com names its counterparty and withholds its balance sheet. Fiserv publishes its balance sheet down to the last accrual and leaves the counterparty in a footer. Neither publishes a price. Whichever you sign, you are buying a blind spot, and the only real choice is which one you are better equipped to live with.

Where Each Platform Wins

Choose Checkout.com when no merchant of yours will ever touch a card reader; when you intend to set each sub-merchant’s fee yourself and Commissions is the reason; when cross-border acceptance is the business rather than a roadmap item; when splitting funds at authorization rather than capture changes your ledger; or when you can name a processing bracket that buys you a real conversation.

Choose Fiserv when a Clover is going on the counter with or without you; when your merchant categories need bank sponsorship to clear underwriting at all; when the leverage you hold is a vertical rather than a volume; when your revenue is North American and staying there; or when your merchants already run on Fiserv rails and switching costs dominate everything else.

Choose neither when what you want is a named, published ladder from reseller to facilitator, with the price of each rung disclosed before you climb it. Neither company on this page publishes one. Look at Global Payments vs Fiserv for the incumbent-versus-incumbent version of this choice, and at Stripe vs Fiserv for what it looks like when one side does publish.

Checkout.com vs Fiserv: ISV Decision Guide

- Will any merchant of yours ever take a payment across a counter? If yes, Checkout.com is disqualified on the spot. It sells no hardware.

- Do you want to set your sub-merchants’ fees, or receive a share of fees set for you? This is the single sharpest fork on the page.

- What bracket would you honestly tick on the volume form? If it is one of the bottom two, expect the pricing your bracket implies.

- Is your leverage volume, or is it distribution? One buys a discount at Checkout.com. The other buys one at Fiserv.

- Do your merchant categories clear underwriting at a money transmitter, or do they need a sponsor bank? Approval reach is not a feature; it is a precondition.

- Are your merchants and their buyers in different countries? If routinely, that is Checkout.com’s home ground and Fiserv’s away fixture.

- Which blind spot can you live with? A counterparty you can name but cannot audit, or a balance sheet you can read behind a counterparty you cannot identify.

Adjacent evaluations worth reading: Adyen vs Checkout.com if a published interchange-plus markup would settle the argument, Checkout.com vs Worldpay for the same opacity question against a vendor with a named partner ladder, and our Checkout.com review for the provider assessment underneath this comparison.

Frequently Asked Questions

Does Checkout.com publish its rates?

No. Its pricing page names three structures — fully flat-rate, simple interchange++, and free for charities — and states, verbatim, “Your business deserves tailored pricing based on your needs.” It commits publicly to no setup fees and no account maintenance fees, but no percentage or per-transaction amount appears anywhere on the site. Any specific Checkout.com rate you have seen quoted online comes from a third-party comparison article, not from Checkout.com, and should be treated as an unsourced starting reference rather than a commitment.

How does an ISV earn revenue on Checkout.com’s Integrated Platforms?

Through a published feature called Commissions, described on Checkout.com’s own product page as letting a platform “Earn on every payment with more control over commission types, including fixed, variable and compound fees per user.” Your platform sets what each sub-merchant pays and keeps the difference over your own cost. Split payments can divide funds at authorization or at capture, and balance transfers move money between accounts inside your platform. The mechanism is documented. The cost basis it sits on top of is not.

Does Fiserv publish an ISV revenue share?

No — not for CardConnect, not for Clover, not for Carat. Its partner materials characterise revenue share as flexible and performance-tied, and attach no tier structure or figure to that description. The more consequential point is structural rather than numerical: a CardConnect partner has no fee-setting authority whatsoever. It is paid a share of fees that Fiserv determines. A spread you engineer and a share you are allotted are different economic instruments, and only one of them is a lever you can pull when your margin needs to move.

Which is better for in-person payments, Checkout.com or Fiserv?

The question does not really have two sides, because Checkout.com does not compete in the category. As of July 2026 its published product catalogue lists no terminal, no reader, and no in-person SDK; card-present acceptance is a market it has chosen to stay out of. Fiserv, through Clover, sells one of the deepest point-of-sale ecosystems available to a software partner. So if any merchant of yours will ever take a payment face to face, the comparison terminates here, on this criterion, before pricing or architecture is reached at all.

Should Checkout.com’s valuation write-down or Fiserv’s lawsuits rule either one out?

Neither should disqualify anyone, but each should tell you which protection to negotiate for, and they are not the same protection. From Checkout.com — whose numbers you cannot see — the thing worth contracting for is visibility into your own cost basis: a floor beneath the rate your Commissions sit on top of, and a commitment that your pricing improves when your volume band does. From Fiserv — whose numbers are on file but whose counterparty is not — the thing worth contracting for is identity and notice: name the product line and the sponsor bank in the agreement, and secure written notice plus a penalty-free exit before any change to the underlying schedule can compress your residual. Ask each vendor to close the gap it created.