Worldpay vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Worldpay and Fiserv are bank-distribution acquirers of comparable scale, and a side-by-side feature grid will tell you they are nearly the same product. The grid is measuring the wrong thing. What separates them for a software platform is the shape of the deal on offer — what your platform is permitted to become, and how much of the payment margin it is permitted to keep. In 2026 there is a second question stacked on top of the first: both of these companies are owned by parents in the middle of transitions they have not finished, and the two crises look nothing alike.

Feature Comparison

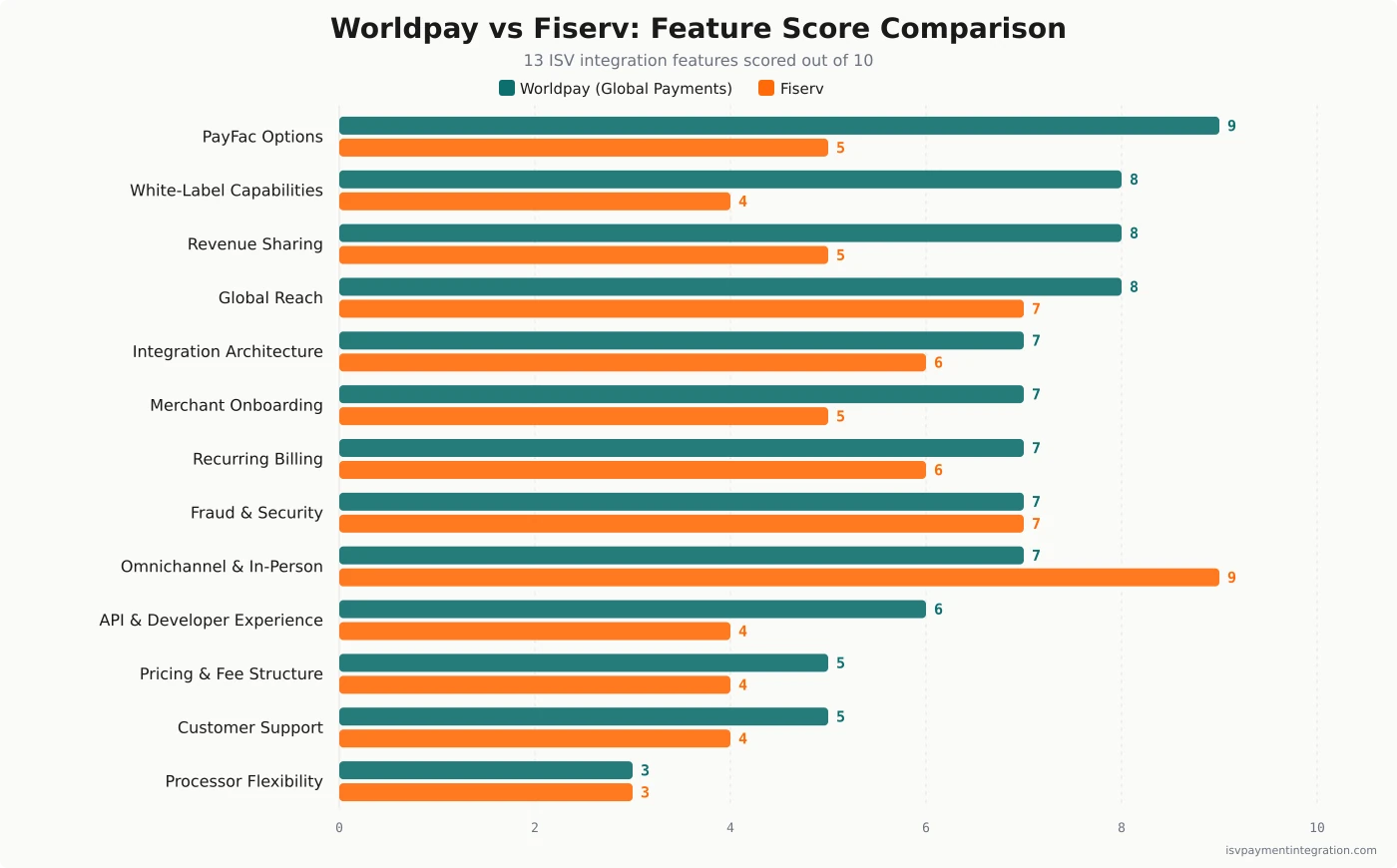

| Feature | Worldpay | Fiserv |

|---|---|---|

| PayFac Options | 9 | 5 |

| White-Label Capabilities | 8 | 4 |

| Revenue Sharing | 8 | 5 |

| Global Reach | 8 | 7 |

| Integration Architecture | 7 | 6 |

| Merchant Onboarding | 7 | 5 |

| Recurring Billing | 7 | 6 |

| Fraud & Security | 7 | 7 |

| Omnichannel & In-Person Payments | 7 | 9 |

| API & Developer Experience | 6 | 4 |

| Pricing & Fee Structure | 5 | 4 |

| Customer Support | 5 | 4 |

| Processor Flexibility | 3 | 3 |

Get this comparison as a shareable PDF

We'll send the Worldpay vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Worldpay

Best for vertical SaaS platforms with a credible route to payment facilitation — dealer management, field service, property management and similar verticals where Worldpay for Platforms already has named reference customers. Accept that your counterparty is mid-integration into Global Payments.

Best for

Fiserv

Best for POS-attached vertical SaaS in restaurant and retail whose merchants will actually use Clover hardware, and whose business plan does not depend on owning the payment margin. Accept that Fiserv's chief executive and president both departed within four weeks in mid-2026.

Worldpay vs Fiserv: The Comparison That Changed in January 2026

A year ago this was a comparison of two independent merchant acquirers. It is not that anymore.

On January 9, 2026, Global Payments closed its $24.25 billion acquisition of Worldpay and simultaneously handed its Issuer Solutions business to FIS. Worldpay is now a division. Its website still says Worldpay, under a banner that says it is now part of Global Payments.

Fiserv, meanwhile, spent the first half of 2026 losing the people who run it. Its chief executive resigned on June 12 with no severance. Its president resigned on July 7. Two securities class actions over statements about Clover’s growth are pending in federal court, and first-quarter revenue fell while operating income fell by more than a third.

So the honest framing of Worldpay versus Fiserv in 2026 is not which one has the better API. It is: which counterparty’s instability can your platform absorb, and what does each one actually pay you for the privilege? Those two questions have different answers, and the second one is where the real difference lives.

Quick Take: Two Acquirer-Owned ISV Arms, Both Unsettled

Worldpay sells software platforms through Worldpay for Platforms, which now absorbs Payrix — the payrix.com domain redirects into it, and Payrix survives as a product name rather than a company. Inside Global Payments it sits in a channel the parent named on day one. Announcing the close, Global Payments said it “will go to market through three channels: Enterprise, SMB, and Integrated & Platforms,” each with “tailored sales strategies and distinct product roadmaps,” backed by “over $1 billion annually” in innovation spend. That channel is not theoretical: in May 2026 the company announced that its Integrated and Platforms business had renewed and expanded its partnership with Lightspeed DMS, rolling out Payrix Pro embedded payments across Lightspeed’s 4,500-plus dealerships. The instability is structural rather than personal. In its Form 10-Q for the quarter ended March 31, 2026, Global Payments told the SEC it “was still in the process of modifying the design of our operating structure to combine the operations of the acquired Worldpay business with our existing Merchant Solutions business.” The channel exists. The org chart underneath it does not, yet.

Fiserv sells software platforms through CardConnect and its ISV Partner Program, and separately through Clover, which is a different proposition entirely. Behind both sits First Data Merchant Services, a registered ISO of seven sponsor banks — Wells Fargo, Deutsche Bank, PNC, MVB, Pathward, Citizens, and KeyBank. That is a distribution moat no independent gateway can replicate, and it is the strongest argument for Fiserv on this page. The instability here is at the top and it is recent. Michael Lyons resigned as chief executive and director on June 12, 2026, effective immediately, taking only accrued salary — no severance, no accelerated equity, no benefits continuation. The 8-K says the resignation “was not the result of any disagreement with the Company,” which is standard language that reads oddly next to an exit package of nothing. Two days later the board appointed Takis Georgakopoulos, who spent seventeen years at JPMorgan Chase and the last seven of them as Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank. On July 7, president Dhivya Suryadevara resigned “for good reason” — contractual language signaling constructive termination rather than a voluntary exit.

That last detail deserves a beat. Fiserv’s new chief executive spent most of a decade building the payments franchise at J.P. Morgan — the same franchise that absorbed WePay and competes with Fiserv for precisely the ISV embedded-payments business this page is about. Whatever else the appointment signals, it is not a signal that Fiserv intends to leave the platform channel alone.

What Worldpay Is for ISVs in 2026

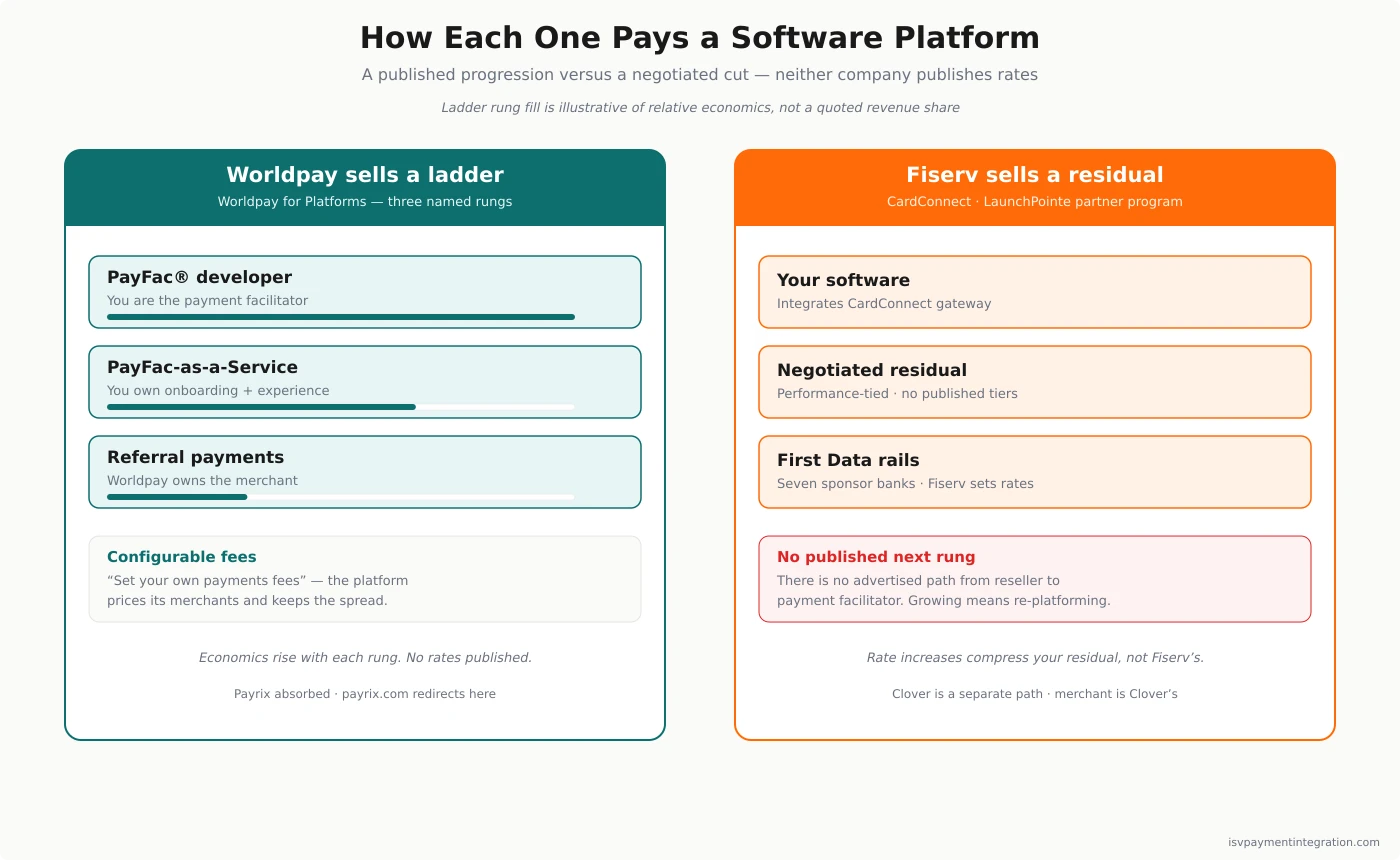

Worldpay for Platforms is built around a single premise: a software company should be able to start by referring merchants and end by becoming the payment facilitator, without changing vendors along the way. Worldpay names all three rungs on its own site.

Referral payments. Your platform refers merchants. Worldpay owns the relationship, the onboarding, and the risk. The lightest integration and the smallest share of the economics.

PayFac-as-a-Service. Your platform takes payment facilitator economics and controls the merchant experience, while Worldpay carries underwriting, compliance, and sponsor-bank access. This is where most growing platforms should be aiming, and it is what PayFac-as-a-Service means in practice.

PayFac® developer. Your platform becomes the payment facilitator outright — underwriting, compliance, merchant experience, all of it. The richest economics and by a wide margin the heaviest regulatory burden.

Underneath the ladder sits the mechanism that matters: configurable fees. Worldpay’s platform site advertises the ability for a platform to “set your own payments fees.” That single capability is the difference between collecting a referral cheque and running a payments business. It is what lets a software company price its merchants, keep the spread, and turn payments into a margin line rather than a rebate.

What Worldpay does not do is tell you what any of it costs. There is no rate card, no revenue-share table, and no published tier threshold anywhere on the platform site. The percentage bands you will find quoted on comparison sites — the familiar 30-50 / 50-70 / 70-90 ladder — do not appear in any Worldpay or Global Payments filing, earnings release, or product page. Treat any specific number you have not seen in your own term sheet as fiction. Our Worldpay pricing breakdown covers what the company does publish, which is its small-business interchange-plus rates, not its platform economics.

What Fiserv Is for ISVs in 2026

Fiserv is not one decision. It is four products, and picking the wrong one wastes a quarter.

CardConnect is the gateway and embedded-payments path, sold to software companies through the ISV Partner Program. Pricing is interchange-plus and entirely negotiated; Fiserv publishes no consumer-facing rate sheet for it. Revenue share is described in Fiserv’s own partner materials as flexible and performance-tied, which is another way of saying you will find out what you earn during the negotiation and not before.

Clover is the point-of-sale platform, and it is a genuinely different animal. An ISV integrates with Clover either by semi-integration — your software talks to Clover hardware — or by building an app that runs on Clover’s Android devices and distributes through the Clover App Market. In the second case you are a tenant in someone else’s marketplace, and the merchant is Clover’s customer, not yours.

Carat is enterprise omnichannel orchestration, aimed at very large merchants. AccessOne is patient financing for healthcare. Neither is the right target for most software platforms.

The routing rule is simple enough: e-commerce and vertical SaaS should evaluate CardConnect; POS-attached vertical SaaS should evaluate Clover; everything else is probably the wrong door. Our Fiserv review walks the four products in detail, and the Fiserv pricing breakdown covers what each one actually costs.

What Fiserv does not offer an ISV is a published route from reseller to facilitator. There is no equivalent of Worldpay’s three named rungs. You earn a residual on Fiserv’s rails, and Fiserv sets the rates on those rails. It has raised CardConnect processing rates before, and every such increase compresses the ISV’s residual without requiring the ISV’s consent.

The Ladder vs the Residual: How Each One Pays You

This is the whole comparison, compressed.

Worldpay sells you a ladder. Three named rungs, a published progression, and configurable fees that let you price your own merchants at the top. The economics improve as you take on more of the payments operation, and the vendor tells you in advance what taking on more looks like. You do not know the numbers until you negotiate, but you know the shape.

Fiserv sells you a residual. You integrate CardConnect, your merchants process on Fiserv’s rails, and you receive a negotiated share of the markup. There is no published next rung. If you want to become a payment facilitator, Fiserv is not the vendor that walks you there — you would be re-platforming, not graduating.

Neither model is wrong. A software company that never wants to own underwriting, never wants to touch compliance, and mostly wants payments to be a modest kicker on top of subscription revenue is well served by a residual. A software company whose long-run business case depends on the payment margin — where payments revenue is meant to eventually exceed software revenue — needs the ladder, because the residual has a ceiling and the ceiling is set by someone else.

Model both against your own merchant base before you sign anything. Our revenue calculator will do the arithmetic on take-rate versus volume; the strategic question it cannot answer is whether you intend to be a software company that accepts payments or a payments company that ships software.

Pricing: One Publishes Rates, One Publishes No Rate At All

For merchants, Worldpay publishes a small-business plan. For platforms, it publishes no rate. Fiserv publishes no rate for any product line on any of its three ISV-facing properties; the one fee it commits to in writing lives in Clover’s App Market Developer Terms.

That asymmetry is smaller than it looks. Neither company will quote your platform a rate from a website, and both will negotiate against your volume, your vertical, and your leverage. What differs is how much you can learn before you walk into the room. With Worldpay you can at least anchor on published small-business interchange-plus rates and reason upward. With Fiserv, and particularly with Clover, the stack of hardware cost, software subscription tiers, and per-transaction rates has no public baseline at all.

The practical advice is the same for both, and it is the advice nobody in a sales cycle wants to hear: get the rate-escalation clause in writing. Ask what happens to your residual when the processor raises its own rates mid-term. Ask for a notice period longer than thirty days, and ask for the right to terminate without penalty if the markup moves beyond a defined threshold. Fiserv has raised CardConnect’s rates during partner terms before. Worldpay’s parent is mid-reorganization and has not published what the combined partner program will look like. Both of those are reasons to paper the downside now.

Onboarding, Underwriting, and Who Owns the Merchant

Ask a single question of any payments partner and most of the rest resolves: after the merchant signs, whose customer are they?

Under Worldpay’s Referral rung, they are Worldpay’s. Under PayFac-as-a-Service they are substantially yours — you own onboarding and the experience, Worldpay owns the underwriting decision and the sponsor-bank relationship. Under PayFac® developer they are yours entirely, along with the compliance obligations that come with them.

Under Fiserv’s CardConnect they are Fiserv’s, mediated by your integration. Under Clover, they are emphatically Clover’s: the hardware carries Clover’s logo, the merchant dashboard is Clover’s, and your software is an app in Clover’s marketplace. That arrangement is a good deal if what you want is distribution into Clover’s merchant base. It is a bad deal if you were hoping to build an embedded payments business on top of a merchant relationship you control.

Platforms that want the merchant relationship and the branded experience should read our white-label payment processing guide before committing to either vendor.

Omnichannel and the Clover Question

Here is where Fiserv wins cleanly, and it is worth being blunt about it.

Clover is the strongest point-of-sale ecosystem a software platform can attach itself to. The hardware range is deep, the app marketplace is real, and the install base across restaurant and retail is enormous. If your merchants need a countertop terminal, a handheld, and a kitchen display, and you would rather integrate than manufacture, Clover is the answer and Worldpay is not.

Worldpay supports in-person acceptance broadly and competently. It does not have a hardware ecosystem in Clover’s league, and pretending otherwise would be dishonest.

The catch is the one above: Clover’s distribution is Clover’s, and the merchant you onboard through it is Clover’s customer. You gain reach and you surrender ownership. Whether that trade is good depends entirely on whether your business plan needs the merchant relationship or merely the transaction.

Counterparty Risk: Read This Before You Sign

Both of these companies are in motion, and the motion is different in kind.

Fiserv’s risk is at the top. Two securities class actions are pending, both now in the Southern District of New York. The lead case, In re Fiserv, Inc. Securities Litigation, No. 1:25-cv-06094, was filed July 24, 2025 and covers purchasers of Fiserv securities from July 22, 2024 to July 24, 2025; it alleges the company’s statements about Clover’s growth were false or misleading. Lead plaintiffs were appointed on November 17, 2025. A second action over Fiserv’s second-quarter 2025 earnings statements was consolidated in the Eastern District of Wisconsin as No. 25-cv-1716 and transferred to New York on April 28, 2026. At least six shareholder derivative complaints are pending alongside them, naming current and former officers. Fiserv has accrued $26 million against its legal proceedings and estimates possible exposure above that accrual at $0 to approximately $160 million.

Nothing has been adjudicated. As of Fiserv’s most recent quarterly filing, “the defendants have not yet answered or otherwise responded to any of the complaints in these actions,” and the company says it intends to defend vigorously. But in the same quarter, total revenue fell 2.0% year over year to $5.027 billion, operating income fell 34.2% to $918 million, and the Merchant Solutions segment came in flat at $2.373 billion. Then the chief executive and the president left. A partner agreement is only as good as the people who honor it, and at Fiserv those people changed twice in one quarter.

Worldpay’s risk is structural. Nobody has resigned. Instead, the entity you would be contracting with is being rebuilt around you. Global Payments Integrated — the parent’s legacy ISV arm — now carries a banner on its own site reading “Global Payments Integrated is transitioning to the Global Payments brand.” Worldpay’s branding has no announced retirement date. Two ISV motions, Worldpay for Platforms and Global Payments Integrated, sit inside one channel and still sell under two names. And Global Payments told the SEC it had not finished designing the combined operating structure as of March 31, 2026.

An ISV signing with Worldpay in 2026 is signing into an org chart its counterparty has not finished drawing. That is a milder problem than a leadership vacuum, and a more predictable one — acquisitions of this size take two to three years to metabolize, and Global Payments has kept acquired brands running for years before. But it is a real problem, and the mitigation is contractual: ask which legal entity holds your agreement, ask who owns the partner relationship in twenty-four months, and get the answer in writing rather than in a slide.

For the parent-company view of this, see our Global Payments review and the Worldpay vs Global Payments comparison, which pulls apart what is now one company with two brands.

Where Each Platform Wins

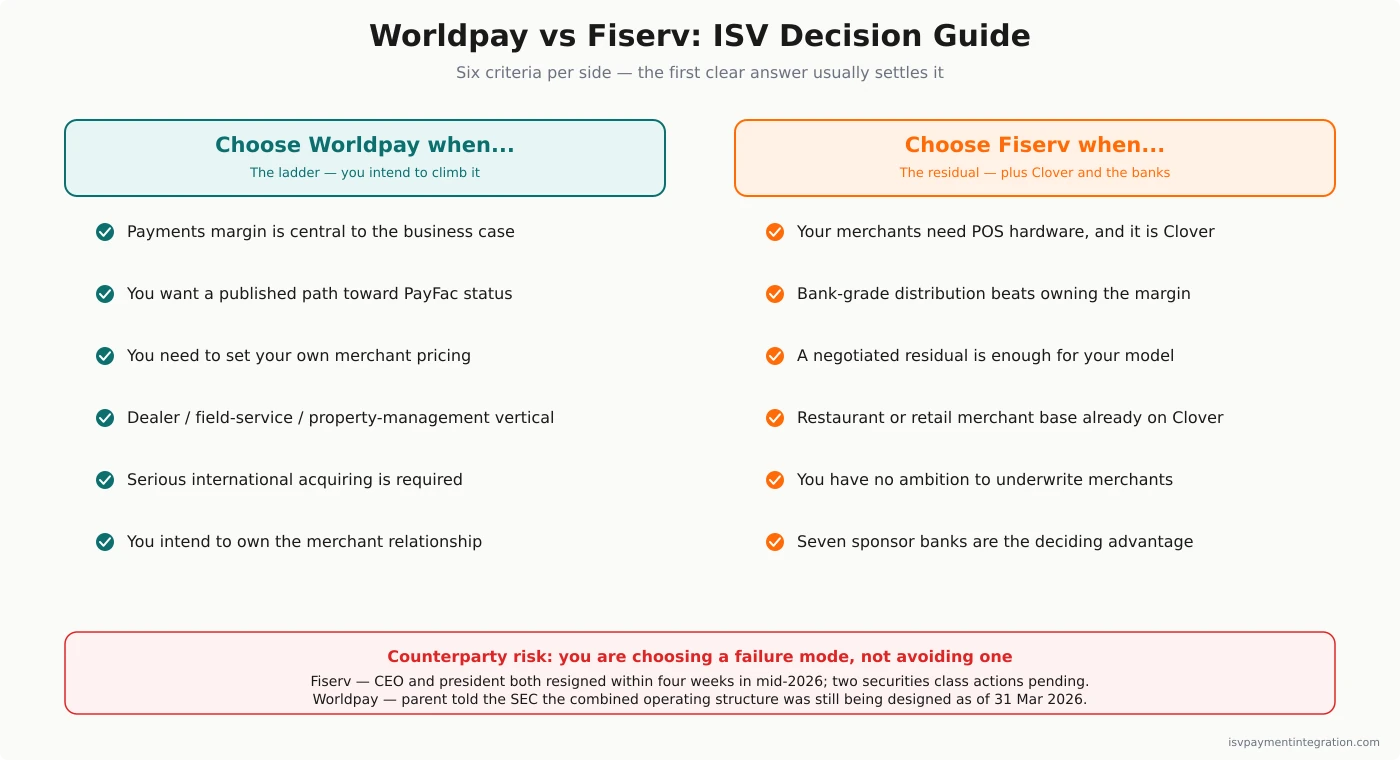

Choose Worldpay when payments margin is central to your business case; when you want a named, published progression toward payment facilitation rather than a permanent residual; when you want to set your own merchant pricing through configurable fees; when your vertical resembles the dealer-management, field-service, or property-management platforms Worldpay for Platforms already references; or when you need serious international acquiring.

Choose Fiserv when your merchants need point-of-sale hardware and Clover is the ecosystem they will actually use; when bank-grade distribution through seven sponsor banks is worth more to you than owning the payment margin; when your platform is content earning a negotiated residual and has no ambition to underwrite; or when the merchant base you serve is already on Clover and you are integrating to meet them there.

Choose neither when the thing you actually want is to own the merchant relationship, brand the entire payment experience, and keep the spread — and you want published economics before you sign. That is what purpose-built PayFac-as-a-Service providers exist for, and it is worth reading how Payrix compares to Stax before you assume the two incumbents on this page are your only options. Payrix, notably, is now inside Worldpay for Platforms — see our Payrix review for what that acquisition changed.

Worldpay vs Fiserv: ISV Decision Guide

Work through these in order. The first one that produces a clear answer usually settles it.

- Do your merchants need POS hardware? If yes, and Clover is the ecosystem, that is a strong pull toward Fiserv regardless of the economics.

- Is payments revenue meant to become a major line on your P&L? If yes, the residual model has a ceiling and Worldpay’s ladder does not.

- Do you intend to underwrite merchants, ever? If yes, only one of these two vendors has a published path there.

- Whose customer is the merchant, in your plan? If the answer is “ours,” Clover is disqualifying and CardConnect is compromised.

- Can you tolerate a partner mid-reorg, or a partner mid-leadership-change? You are picking one. Decide which failure mode you can manage.

- How much leverage does your volume give you? Both vendors negotiate everything. Neither publishes platform economics. Volume is the only argument either one respects.

- What happens to your margin if the processor raises rates mid-term? Ask before signing. Get it in the contract.

For the adjacent comparisons, see Global Payments vs Fiserv — increasingly the same question one level up the org chart — and Authorize.net vs Fiserv if a pure gateway is also in your evaluation.

Frequently Asked Questions

Is Worldpay the same company as Global Payments now?

Legally, yes. Global Payments completed its acquisition of Worldpay on January 9, 2026, in a transaction valued at $24.25 billion, and announced the completion on January 12. Commercially, not yet. Worldpay still sells under its own brand, worldpay.com carries a banner reading “Worldpay is now part of Global Payments,” and the two ISV programs — Worldpay for Platforms and Global Payments Integrated — remain separate product lines inside a single Integrated & Platforms channel. Global Payments stated in its Form 10-Q for the quarter ended March 31, 2026 that it was still designing the combined operating structure and would not report against new segments until that work completed.

Who is Fiserv’s CEO?

Takis Georgakopoulos, appointed June 14, 2026. He replaced Michael P. Lyons, who resigned as chief executive and director on June 12, 2026, effective immediately, receiving no severance and no accelerated equity vesting. Georgakopoulos previously spent seventeen years at JPMorgan Chase, including seven as Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank. Fiserv’s president, Dhivya Suryadevara, separately resigned “for good reason” on July 7, 2026.

Does Worldpay or Fiserv pay ISVs a better revenue share?

Neither publishes revenue-share percentages, so any specific figure you have seen quoted online is unsourced. What differs is the structure. Worldpay for Platforms names three monetization tiers — Referral payments, PayFac-as-a-Service, and PayFac® developer — and advertises configurable fees that let a platform set its own merchant pricing. Fiserv’s CardConnect pays a negotiated, performance-tied residual with no published tier structure and no stated path to payment facilitation. A platform that intends to grow into owning the payment margin has a defined route with Worldpay and does not with Fiserv.

Can an ISV become a PayFac with Fiserv?

Not through a published program in the way Worldpay describes. Fiserv offers payment-facilitation enablement through specific arrangements, but it is not the primary business model and there is no advertised progression from CardConnect reseller to facilitator. Worldpay for Platforms names PayFac® developer as the top rung of its ladder explicitly. If becoming a payment facilitator is on your roadmap, that difference is the single most important thing on this page.

Should Fiserv’s lawsuits and executive departures stop me from signing?

Not by themselves, and anyone telling you otherwise is selling something. Nothing has been adjudicated: per Fiserv’s own Form 10-Q, defendants have not yet answered any complaint, no class has been certified, and the company intends to defend vigorously. Fiserv remains a roughly $21 billion revenue business with seven sponsor-bank relationships and capital-markets access — it raised €1 billion in senior notes in June 2026. What the situation should change is your paperwork, not your shortlist. Ask for a written rate-lock, a ninety-day notice period on fee changes, and a termination right without penalty if the markup moves beyond a threshold you define. The people who negotiated Fiserv’s partner agreements in 2025 are not the people who will honor them in 2027.