Braintree vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Both of these companies are obliged to tell the truth to regulators, which makes this the rare payments comparison where the decisive documents are not the marketing pages. Everything an ISV needs to separate them is on the public internet right now — and none of it is on the page either company would like you to read. The usual feature checklist answers a question no software platform actually has.

Feature Comparison

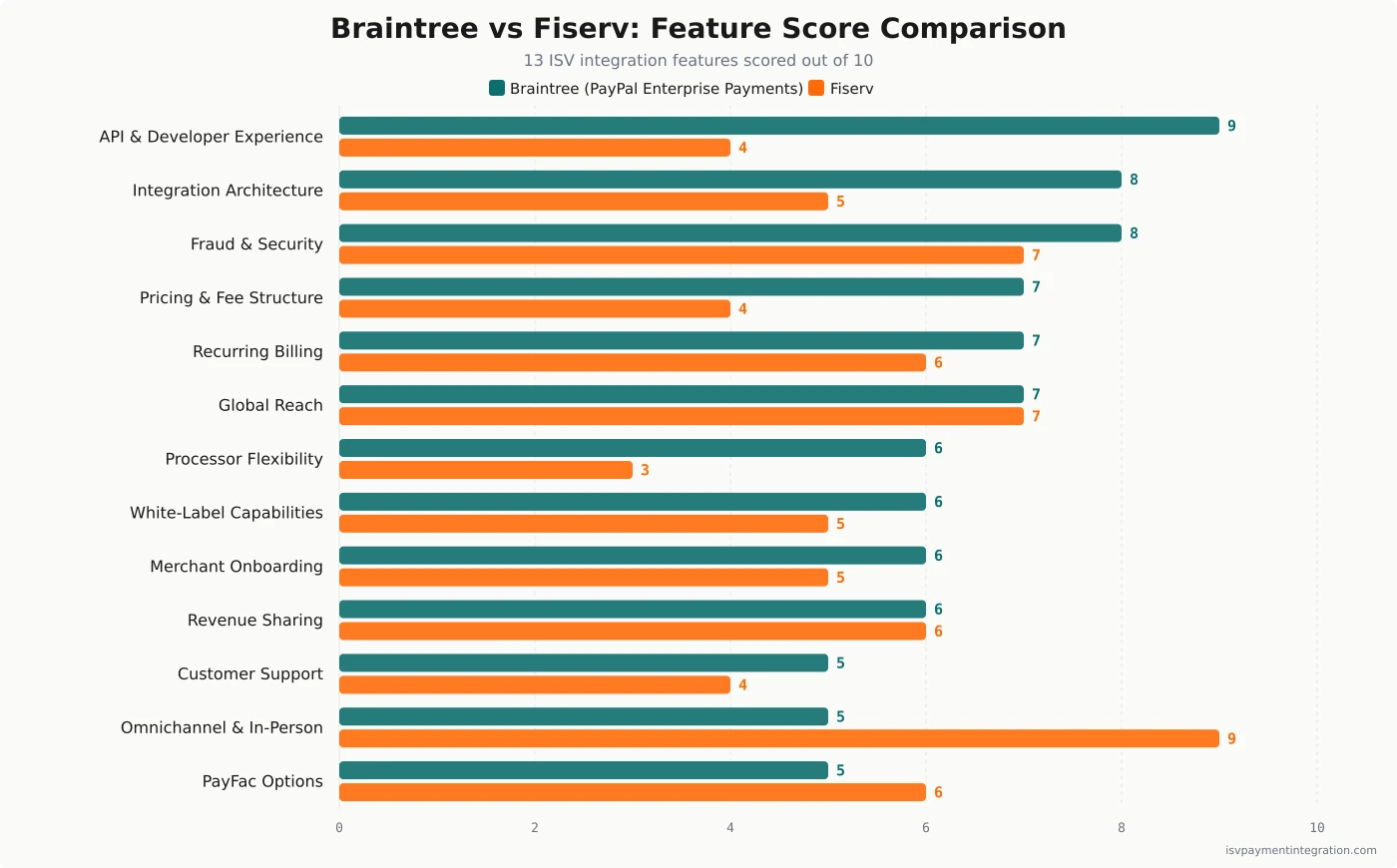

| Feature | Braintree | Fiserv |

|---|---|---|

| API & Developer Experience | 9 | 4 |

| Integration Architecture | 8 | 5 |

| Fraud & Security | 8 | 7 |

| Pricing & Fee Structure | 7 | 4 |

| Recurring Billing | 7 | 6 |

| Global Reach | 7 | 7 |

| Processor Flexibility | 6 | 3 |

| White-Label Capabilities | 6 | 5 |

| Merchant Onboarding | 6 | 5 |

| Revenue Sharing | 6 | 6 |

| Customer Support | 5 | 4 |

| PayFac Options | 5 | 6 |

| Omnichannel & In-Person Payments | 5 | 9 |

Get this comparison as a shareable PDF

We'll send the Braintree vs Fiserv breakdown to your inbox — ready to share with your team.

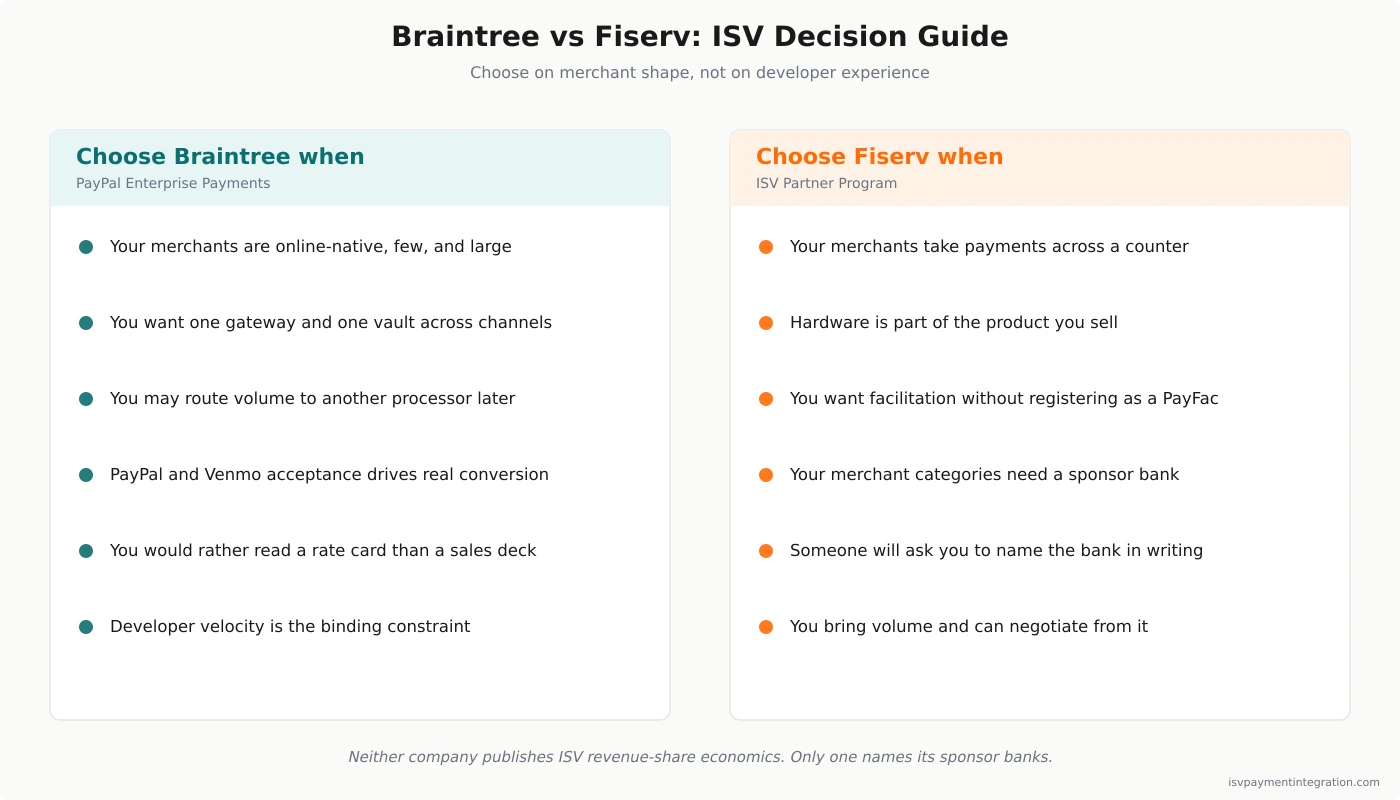

Best for

Braintree

Best for ecommerce-first software whose merchants are large and few, and where Venmo and PayPal wallet acceptance move conversion enough to matter. Accept that splitting a transaction requires a sales conversation and US-only sub-merchants, and that recurring billing and Marketplace cannot coexist.

Best for

Fiserv

Best for vertical SaaS in salons, restaurants, clinics and municipal offices — anywhere the terminal is part of the product and the merchant's working day runs on it. Accept a negotiated rate you cannot benchmark, an integration that opens with a sales cycle rather than an API key, and a counterparty midway through an executive transition it has not finished.

Braintree vs Fiserv: Read the Filing, Then the Footer

Most comparisons of these two open with the API. Open instead with two documents neither company advertises: PayPal’s latest quarterly filing, and the bottom of a Fiserv subsidiary’s homepage.

In its Form 10-Q for the quarterly period ended March 31, 2026, PayPal explains a rise in transaction expense as the result of an 11% increase in total payment volume “and a higher proportion of TPV from our Braintree products and services, which generally have higher expense rates than our other products and services.” Earlier in the same filing, Braintree is credited with roughly $410 million of transaction-revenue growth — against $140 million for PayPal-branded products and $70 million for Venmo.

So Braintree is at once PayPal’s largest single driver of transaction-revenue growth and the part of the book PayPal tells the SEC carries higher expense rates. Both are true. The second is less damning than it first sounds, and the next section explains why — but the shape is what matters: this is a company describing, in a document it can be sued over, a product whose economics differ from everything else it sells.

Fiserv discloses the thing that matters about it in a place equally unvisited: a footer. This page is about those two disclosures, and about the fact that a software platform’s real decision turns on them rather than on the feature grid.

Quick Take: An Enterprise Rename and a Partner Program

Braintree is no longer marketed as Braintree. Its landing page at paypal.com opens with the line “Braintree is now PayPal Enterprise Payments,” and the primary call to action is Explore Enterprise Payments. The gateway underneath is excellent and unusually candid: a published card rate, itemized surcharges, a GraphQL API, and — remarkably for a payment company — documented orchestration guides for routing volume to Adyen, dLocal, EBANX, Fat Zebra, FlexFactor, Flutterwave, and Stripe. Braintree will help you send transactions to its competitors. Few processors put that in the docs.

What Braintree does not sell is a platform program. There is no partner tier, no published revenue share, no ISV portal. Where a software company wants to onboard sellers and take a cut, there are two documented routes, and both of them begin with a form.

Fiserv sells software companies through the ISV Partner Program — that is its actual name, on fiserv.com, under a page headed “Integrated Payments for ISVs.” The pitch is three verbs: Integrate, Monetize, Grow. The proof points are scale: #1 global merchant acquirer, 78 billion merchant transactions processed annually, nearly 100% of U.S. households reached. The gateway named there is CardPointe, the portfolio tool is CoPilot, and the page advertises “Managed PayFac Capabilities” — payment facilitation where, in Fiserv’s phrasing, “we handle the heavy lifting.”

Not one number on that page is a price.

And the counterparty is unsteady. Fiserv replaced its chief executive in June 2026, its president departed three weeks after that, and two unadjudicated securities class actions concerning Clover’s reported growth are pending. None of this touches the product architecture this page is about. It does touch who will be sitting across the table when your economics get set. Our Fiserv review carries the detail.

What PayPal’s Filing Does and Does Not Say

Public companies must explain their expenses, and the explanation is where strategy leaks. It is also where a careless reader goes wrong, so take the expense-rate sentence slowly.

Braintree is full-stack acquiring. It processes other companies’ card transactions end to end, which means interchange and card-scheme fees flow through PayPal’s transaction expense on every single sale. PayPal-branded checkout rides on funding sources and rails PayPal already owns, some of which cost it very little. A higher expense rate on Braintree volume is therefore substantially mechanical — it is roughly what any payment company’s unbranded processing looks like sitting next to its own wallet. It is not, by itself, evidence that Braintree is unprofitable, and this page does not claim that.

PayPal does, however, choose a word. It attributes the increase in its transaction expense rate to “unfavorable changes in product mix.” The mix that grew was Braintree’s.

And here is the part most write-ups skip, because it cuts the other way: from an ISV’s seat, a higher expense rate is not obviously bad news. It means less spread is being extracted between what the card networks charge and what you are charged. Platform economics and merchant pricing are different questions. A processor running a thin take rate on your volume has less room to squeeze you — and more reason to want you large.

Hold both facts at once. Braintree is growing fastest and costing most to run. Everything below is consistent with that shape. None of it is caused by it, and this page will not pretend otherwise.

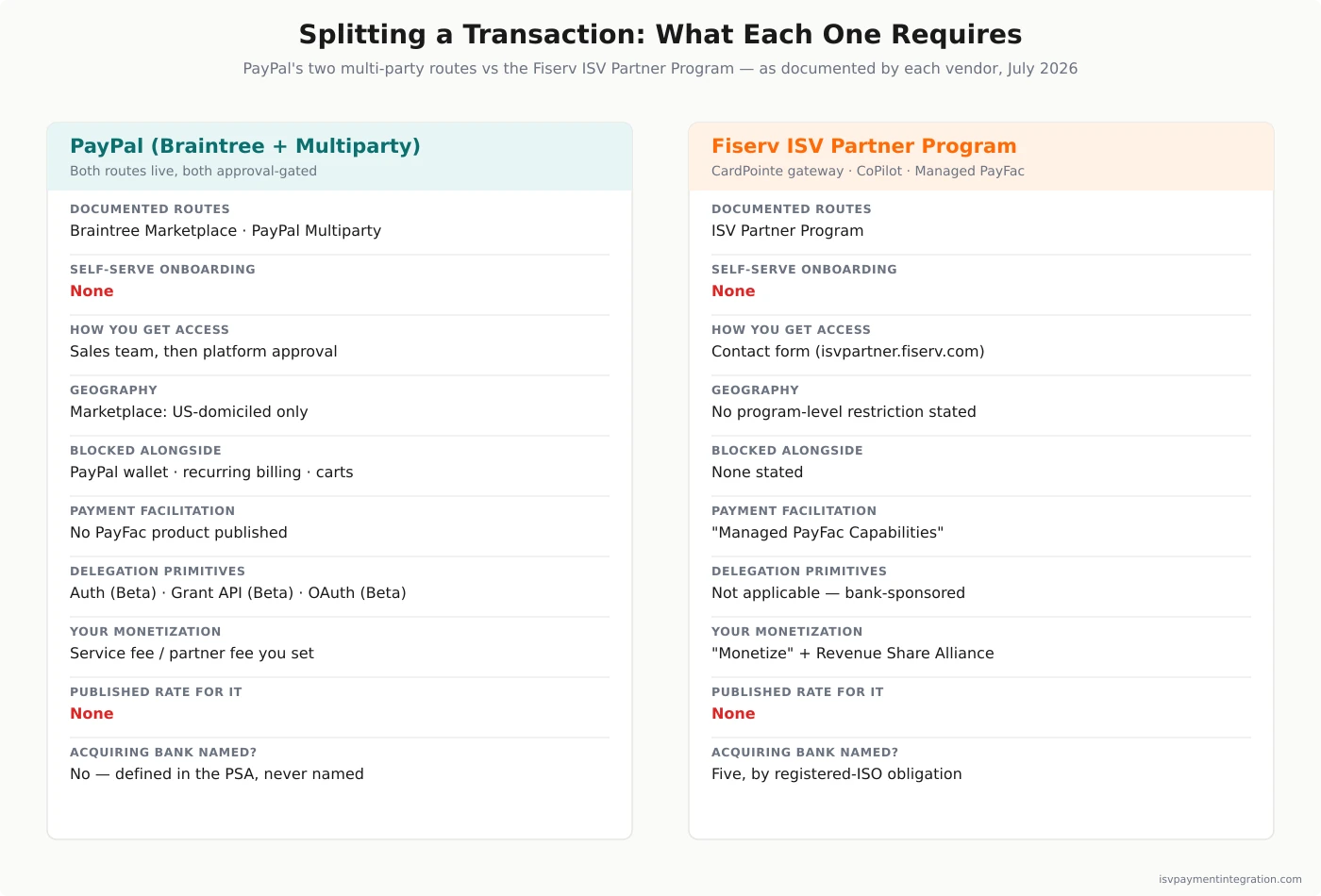

Two Routes to Multi-Party Payments, Both Behind a Form

If your software needs to split a transaction between itself and a seller, PayPal offers two documented paths. Neither is self-serve.

Braintree Marketplace onboards sub-merchants, designates a service fee, routes that fee to your account, and can hold funds in escrow. Four documented API features. It works, it is live, its documentation returns HTTP 200, and it has not been discontinued, whatever you may have read. It is, however, gated twice on the same page. The overview opens with an availability notice — “If you’re a new merchant looking for a marketplace solution, contact our Sales team” — and the compatibility section repeats it. Then the constraints, verbatim:

“Braintree Marketplace is only available for business models in which the master merchant and sub-merchants are all domiciled in the US. It is not compatible with PayPal, Braintree’s recurring billing, or most third-party shopping carts. Before you can get started, all merchant accounts need to be specially approved by us for use with Braintree Marketplace.”

Sit with the second sentence, and note what it means: the multi-party product is incompatible with the PayPal payment method — the wallet that is the reason many platforms chose Braintree in the first place. It is incompatible with recurring billing, so a vertical SaaS company running subscriptions for its merchants cannot also split their transactions. And it is incompatible with most third-party carts.

PayPal Multiparty, documented separately at developer.paypal.com, is the newer route under the Enterprise Payments banner. It covers seller onboarding, embedded integration, subscriptions, disputes, and partner fees — “commissions or brokerage fees for each transaction they facilitate on behalf of a seller.” It is a real platform product with real constraints: the platform fee must be in the transaction’s currency, the fee payee must attach a bank account, a partner’s live API-caller account cannot hold a PayPal balance, and platform fees are unsupported for first-party integrations. And it is gated too. You “apply for live credentials and go live after your platform or marketplace has been approved,” and the page’s own form promises that “a PayPal representative will contact you after they evaluate your business needs.”

Why the gate? Two explanations circulate, and only one survives contact.

The first is regulatory: card-network marketplace registration and sub-merchant underwriting and anti-money-laundering obligations bind every payment aggregator. True — but they bind every aggregator, and Stripe Connect onboards platforms and their sub-merchants programmatically under the same rules. Those obligations cannot by themselves explain this particular gate.

What remains is commercial: a preference for platforms of a certain size, which is at least consistent with the eligibility criteria PayPal names on its own fee page. That is an inference, not a disclosure, and the two explanations are not mutually exclusive. What is not in dispute is the gate itself, which is documented in PayPal’s own words on both routes.

One further data point on maturity. Braintree Auth — the OAuth flow that lets a platform act on a merchant’s behalf — is written “Braintree Auth (Beta)” in the documentation navigation, as are Grant API and OAuth in the Additional Features list. Labeled Beta is not the same as unsupported, deprecated, or abandoned; these are production surfaces. But an ISV should know that the delegation primitive it would build on carries that label today.

Now the concession this page owes you. Fiserv is not the open alternative. Fiserv publishes no rate on any of its three ISV-facing properties, and offers no self-serve onboarding whatsoever; its “Managed PayFac” is a sales motion attached to a bank underwriting queue. The gates simply differ in kind. Braintree gates the product. Fiserv gates the price.

Nobody Names the Bank, and Only One of Them Has To

Every card transaction settles through a financial institution. The question is whether the company you integrate with will tell you which one.

Start with the contract. The Braintree Payment Services Agreement, last updated March 2, 2026, defines the role and leaves it empty: “‘Acquirer’ means the financial institution that provides acquiring services to Merchant with respect to the Braintree Payment Services.” It goes further — above certain Visa and Mastercard thresholds, it tells you, you will be required by the networks to enter a Commercial Entity Agreement with “each Acquirer” that processes your card payments. A US merchant is thus told it may one day have to sign an agreement with an institution the document never identifies. Search that agreement for a bank name and you will not find one.

The Marketplace documentation is no more forthcoming. Its glossary defines escrow as “an option that allows you to hold funds through our banking partner until you decide to disburse them.” Our banking partner. Singular, unnamed, in the very guide explaining how to hold other people’s money.

Now CardConnect’s homepage footer: “CardConnect is a registered ISO of Citizens Bank, N.A., KeyBank N.A., Pathward N.A., PNC Bank, N.A., and Wells Fargo Bank, N.A.” Five institutions, named, on the public internet, before you sign anything.

Do not mistake that for generosity. A Visa and Mastercard registered ISO is obliged to name its sponsor banks in merchant-facing material. CardConnect discloses because it must. PayPal is not in that category, so there is nothing it is failing to disclose against. And the obligation has limits worth stating plainly: CardConnect’s ISO footer lists five banks, but whether those same institutions sponsor the ISV Partner Program specifically is not stated anywhere Fiserv publishes.

That asymmetry is still the most decision-relevant thing on this page. One company is compelled to name institutions, and does. The other is not, and does not. If your platform holds sub-merchant funds, a legal obligation is the only reason a name reaches you at all — which is precisely why you should get the institution named in your own contract rather than hoping to find it in a footer. What a payment aggregator is explains why this distinction is structural rather than cosmetic.

Two Card-Present Products, One Operating System

It is often written that Braintree is online-only. It is not, and the claim is several years stale.

Braintree ships a card-present product built on Verifone terminals: EMV contact and contactless, magnetic stripe, P2PE, PCI PTS-certified hardware, gift cards, buy-now-pay-later through Affirm and Klarna “where configured,” and support for retail, restaurant, and bill-payment scenarios. There is even a legacy in-person solution it supersedes. A single vault spans both channels.

Read how Braintree frames it, though. The guide’s stated purpose is to help you “extend an existing Braintree ecommerce setup to your physical stores.” The web account is the noun. The terminal is the extension. That is a channel.

Clover is not a channel. Clover is the machine a restaurant opens in the morning and closes at night — it takes the order, prints the ticket, runs the register, and happens to accept a card. A vertical SaaS product that integrates with Clover integrates with the merchant’s operating system, and inherits a very large installed base along with a very large partner it does not control.

Which raises a question about the operating system’s catalogue. Fiserv’s merchant site says Clover has “integrations with 400+ apps.” CardConnect’s homepage, describing the same Clover to the same audience, says “a library of 300+ apps.” Two Fiserv properties, fetched the same afternoon in July 2026, off by a hundred. And a third wrinkle: the ISV Partner Program page — the one Fiserv points software vendors to — never mentions Clover at all, while Fiserv separately maintains a developer product called Commerce Hub that the ISV page also never mentions. These are small things. They are also the kind of small thing that tells you how many separate teams are maintaining the story, which is why an ISV should confirm which Fiserv entity is on its contract before assuming any capability transfers between them.

The Published Rate Has Conditions

Braintree publishes its rates, and the page is unusually complete. For standard merchants on the US schedule: 2.89% + $0.29 for cards and third-party digital wallets, last updated May 7, 2026. Pass-through American Express, $0.15. Non-USD presentment, plus 1%. Cards issued outside the US, plus 1%. Chargebacks, $15. Venmo, 3.49% + $0.49. ACH at 0.75% capped at $5, or 1.5% + $0.10 same-day. Registered 501(c)(3) charities pay 2.19% + $0.29. Chargeback Protection starts at 0.4% per transaction; Fraud Protection Lite is $0.05 per inquiry.

Then, at the bottom of the table, footnote 1:

“Custom flat rates, interchange plus pricing, and discounted rates are available for established businesses based on business model and processing volume.”

The fact that footnote establishes is narrow and worth stating exactly: the published rate is conditional, and the conditions PayPal names are business model and processing volume. The list price is the price for platforms that have not yet met criteria PayPal declines to quantify.

The inference — mine, not PayPal’s — is that a rate card with eligibility criteria attached is doing sorting work as much as pricing work, and that the criteria tell you which way it sorts. Read it alongside the expense-rate disclosure and it is at least coherent. Treat it as a reading, not a finding.

Fiserv skips the sorting and opens at the conversation. There is no card rate for CardPointe, no Clover rate, no Carat rate, and no ISV revenue-share figure anywhere in the ISV Partner Program; the page ends at a contact form. Anyone quoting you a specific Fiserv revenue-share percentage is quoting something Fiserv did not publish.

Work both against your own volume with the revenue calculator, and read the Braintree pricing breakdown and Fiserv pricing before taking any headline number at face value.

These Two Are Not Chasing the Same ISV

The comparison most software companies run — which API is nicer, which rate is lower — resolves in Braintree’s favor and then leads them somewhere they did not want to go.

Braintree’s trajectory is enterprise. The rename says so, the sales gate on both multi-party routes enforces it, and the fee page’s own eligibility criteria describe who the product is for. If your merchants are few, large, and online, this is a superb piece of engineering to build on and you will be a welcome customer.

Fiserv’s trajectory is the opposite, and it is not subtle about it. Its named ISV case study is BookedBy, which builds salon software; BookedBy’s Sean Maney is quoted saying his users “get payments, hardware, and BookedBy software all-in-one.” That is a small-merchant, counter-attached, hardware-bearing business, and Fiserv wants a thousand more of them. It will not tell you what it pays you until you ask, but it has a program, a portfolio tool, a managed-facilitation product, and a legal obligation to name its banks.

Choose on merchant shape, not on developer experience. The developer experience is a three-month cost. The merchant shape is the business.

For adjacent evaluations: PayPal vs Braintree disentangles the two products now sharing one brand, Stripe vs Fiserv covers the API-first alternative that does publish platform economics, and Braintree vs Adyen is the right page if enterprise scale is the actual requirement.

Braintree vs Fiserv: ISV Decision Guide

- Do you need to split a transaction between yourself and a seller? Both PayPal routes require approval before live credentials. Braintree Marketplace additionally restricts you to US-domiciled sub-merchants and takes away recurring billing and the PayPal wallet. Decide whether you can live without those before anything else.

- Are your merchants’ payments happening on a counter? If the device matters more than the checkout page, Clover is the answer and the rest of this list is academic.

- Do you run subscriptions for your merchants? Braintree Marketplace and Braintree recurring billing are documented as incompatible. This eliminates a surprising number of vertical SaaS architectures.

- Will anyone ever ask you to name the institution holding your sub-merchants’ funds? Only one of these companies is under an obligation to answer.

- Do you want payment facilitation without registering as a facilitator? Fiserv advertises Managed PayFac. Braintree does not offer one. See PayFac-as-a-Service.

- Might you move volume to another processor later? Braintree publishes orchestration guides to seven of them, including Stripe. That is real optionality, and it is unusual.

- How big is your typical merchant? PayPal’s fee page reserves custom pricing for “established businesses based on business model and processing volume.” Ask honestly whether that describes you, and what the list rate costs you until it does.

Frequently Asked Questions

Has Braintree been discontinued or replaced by PayPal?

Neither. The paypal.com landing page states “Braintree is now PayPal Enterprise Payments,” which is a rename and a repositioning, not a shutdown. The gateway, the SDKs, the GraphQL API, and the fee schedule are all live and maintained; the fee page was last updated on May 7, 2026, and the Payment Services Agreement on March 2, 2026. What changed is the audience the product is sold to. See PayPal vs Braintree for how the two products differ where they overlap.

Is Braintree Marketplace still available?

Yes. Its documentation is live and describes four working API features — sub-merchant onboarding, onboarding confirmation, transactions with service fees, and escrow. It is not discontinued. It is approval-gated: new platforms are told twice on the overview page to contact Braintree’s sales team, and every merchant account must be “specially approved.” The hard constraints are that master and sub-merchants must all be US-domiciled, and that it does not work alongside the PayPal payment method, Braintree’s recurring billing, or most third-party shopping carts. PayPal separately documents a Multiparty solution with partner fees, which is also gated on platform approval.

Does Braintree offer ISVs a revenue share?

No, and this is a common misreading. Braintree publishes no platform or partner revenue-share program. What it offers is a mechanism: an approved Marketplace master merchant sets a service fee on each sub-merchant transaction, and PayPal’s Multiparty documentation describes partner fees and commissions on the same principle. In both cases you are keeping a fee you set, not earning a share of PayPal’s. Fiserv runs an ISV Partner Program built around monetization and a separate Revenue Share Alliance channel — and publishes no rate for either. Neither company will tell you the number before you ask.

Which one can act as a payment facilitator for my platform?

Fiserv, on the evidence each company publishes. Fiserv’s ISV page advertises “Managed PayFac Capabilities,” describing payment facilitation where Fiserv carries the compliance burden. Braintree publishes no payment-facilitation product; Braintree Marketplace and PayPal Multiparty are aggregation models, and the OAuth-style delegation primitives — Braintree Auth, Grant API, OAuth — are all labeled Beta in PayPal’s own documentation navigation. That label means pre-general-availability, not unsupported. If facilitation is your destination, start with what a PayFac is and PayFac-as-a-Service.

Is Braintree really online-only?

No. Braintree ships a card-present product on Verifone terminals supporting EMV contact and contactless, magnetic stripe, P2PE, gift cards, and buy-now-pay-later via Affirm and Klarna where configured, across retail, restaurant, and bill-payment use cases. The distinction that matters is framing: Braintree’s own guide describes the product as a way to “extend an existing Braintree ecommerce setup to your physical stores.” Clover, by contrast, is the system the merchant runs the business on. One is a channel added to a web account; the other is the counter itself.

Which bank holds the funds in a Braintree Marketplace escrow?

Braintree does not say. Its Marketplace documentation defines escrow as an option to “hold funds through our banking partner until you decide to disburse them” — one banking partner, unnamed, in the guide that explains how to use the feature. The Braintree Payment Services Agreement is no more specific: it defines “Acquirer” as “the financial institution that provides acquiring services to Merchant,” and names none. CardConnect, by contrast, names five sponsor banks in its homepage footer — because a registered ISO is required to. If your platform holds sub-merchant funds and expects to answer an auditor, a regulator, or an enterprise customer’s security questionnaire about where that money sits, get the institution named in your agreement before you write the integration.