Fiserv Pricing

Pricing model: Negotiated interchange-plus across CardConnect, Clover, and Carat. Based on publicly available information from Fiserv's official site. Contact Fiserv directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | Not publicly disclosed by Fiserv on any product surface. CardConnect runs interchange-plus with performance-tied ISV revenue share — basis points and per-transaction fees negotiated per partner. Clover stacks hardware purchase, monthly software-subscription tiers, and per-transaction processing rates, all negotiated by merchant. Carat is enterprise quote-only. CardConnect raised processing rates by 0.10% plus $0.05 per transaction across all major card networks effective April 1, 2024 — the most concrete public cost data point in the entire Fiserv pricing surface. |

| Markup | Volume-tiered and partner-negotiated. Fiserv's ISV Partner Program revenue share is, in the program's own framing, 'flexible,' 'performance-tied,' and 'never set in stone.' Independent partner reports indicate meaningful negotiation friction below multi-million-dollar platform-aggregated annual processing volume; serious ISV economics typically begin in the $5M+ aggregated platform volume range. |

| Setup | Not published. Implementation fees vary by product line — CardConnect integration is generally low or no setup for standard tokenization patterns, but custom embedded-boarding or sub-merchant onboarding APIs can carry implementation costs. Clover hardware is a real upfront purchase ($499-$1,799 per device class typical retail). Carat enterprise integration carries quote-based implementation fees. |

| Monthly | Multiple monthly fee surfaces depending on product. CardConnect's gateway-only and platform-fee structure is partner-specific. Clover monthly software-subscription tiers (Starter, Standard, Advanced, Plus) range broadly across verticals — exact tier pricing varies by Clover device class and vertical, and is set per-merchant. PCI compliance fees, statement fees, and chargeback fees apply across all paths. |

Hidden Costs to Watch

- ⚠ April 2024 CardConnect rate increase: +0.10% + $0.05 per transaction across all major card networks effective April 1, 2024. The increase passes through to ISV revenue-share margins, compressing residuals on every transaction processed under that contract structure. No public schedule for whether/when further pass-through increases will hit.

- ⚠ Clover hardware purchase costs: countertop terminals, mobile devices, handheld units, and accessory peripherals are real CapEx purchases ranging $499-$1,799 per device. ISVs whose merchants buy through the platform inherit this cost in the merchant's first-month bill.

- ⚠ Clover monthly software-subscription tiers: Starter, Standard, Advanced, Plus — pricing varies by vertical and device class, set per-merchant. ISVs reselling Clover see this as a recurring line on every merchant's statement, separate from processing rates.

- ⚠ PCI compliance fees: typically $5-$25/month per merchant location. Charged separately from processing. Some Fiserv contracts include PCI fees in the bundle; many do not. ISVs need to ask explicitly.

- ⚠ Chargeback fees: charged per dispute regardless of outcome, typically $15-$25 per chargeback. Adds up materially for ISVs in higher-risk verticals (subscription, restaurant chains, travel).

- ⚠ Statement fees, batch settlement fees, and 'paper statement' fees: small recurring line items that aggregate to non-trivial monthly cost across a multi-thousand-merchant ISV portfolio.

- ⚠ Cross-border transaction fees: typically additional 0.4%-1.0% on transactions where the issuing card's country differs from the merchant's country. Material for ISVs serving international-facing merchants.

- ⚠ Currency conversion markup: applied to multi-currency transactions, typically 1%-3% over the wholesale FX rate. Matters for ISVs with merchants accepting non-USD cards or operating multi-region.

- ⚠ Early termination fees: contract-specific. Many Fiserv contracts include three-year auto-renewing terms with prorated termination penalties for early exit. ISVs need to read partner agreement carefully.

- ⚠ Integration and ongoing maintenance: developer time for initial CardConnect or Clover integration, plus ongoing API-update maintenance as Fiserv evolves the platform. Not a Fiserv line item, but a real cost ISVs underwrite.

Alternatives

Fiserv Pricing for ISVs: What You Actually Pay

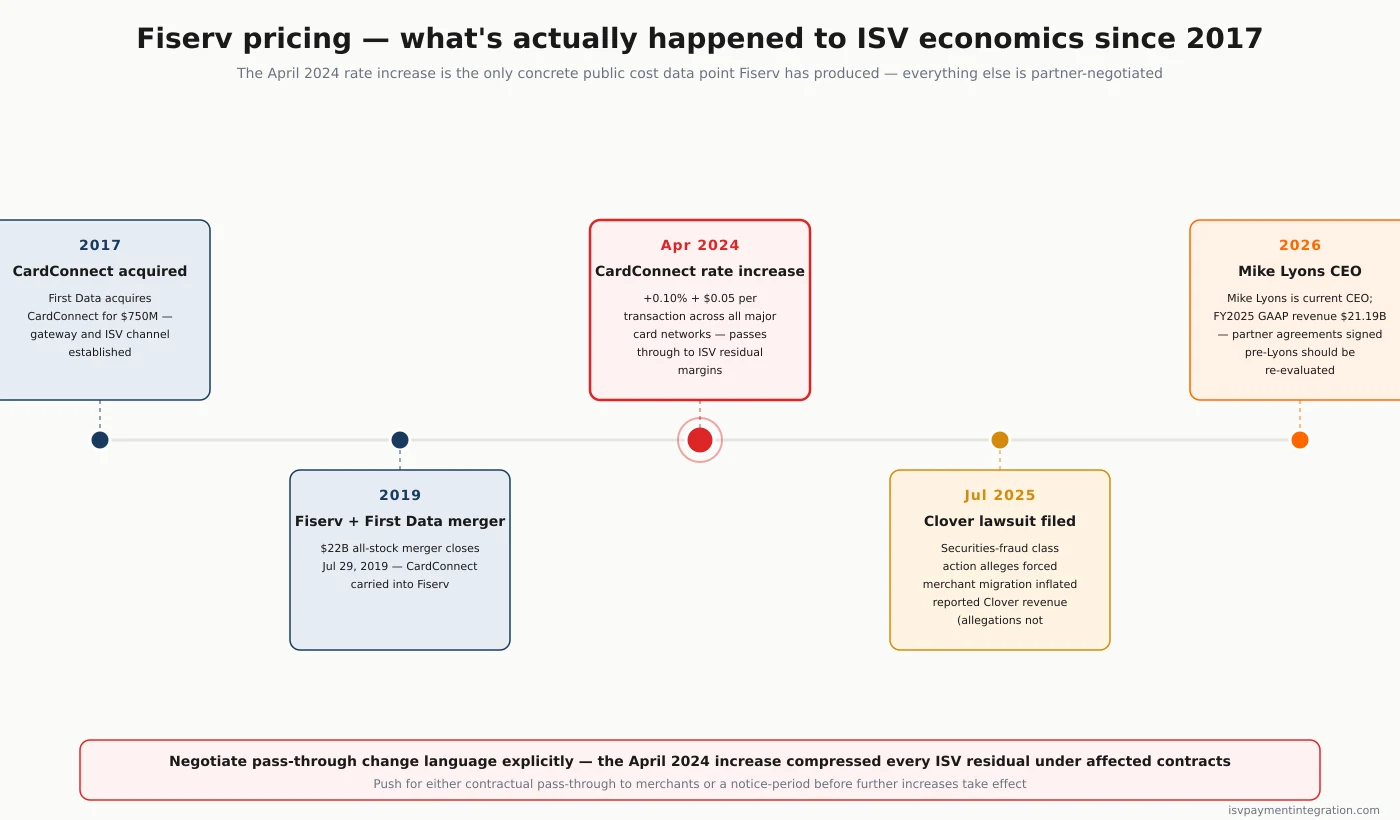

Fiserv pricing is the most opaque commercial surface in the major-acquirer landscape. Across CardConnect, Clover, Carat, and AccessOne — the four ISV-relevant product lines under the Fiserv corporate umbrella — there is no published rate card. The most concrete public cost data point Fiserv has produced in two years is the April 2024 CardConnect rate increase (+0.10% + $0.05 per transaction across all major card networks). Everything else is partner-negotiated, merchant-negotiated, or quote-based.

This page walks through what’s actually known, what’s negotiable, and what hidden costs ISVs should be modeling into their unit economics before signing any Fiserv partner agreement.

How Fiserv’s Pricing Surface Is Structured

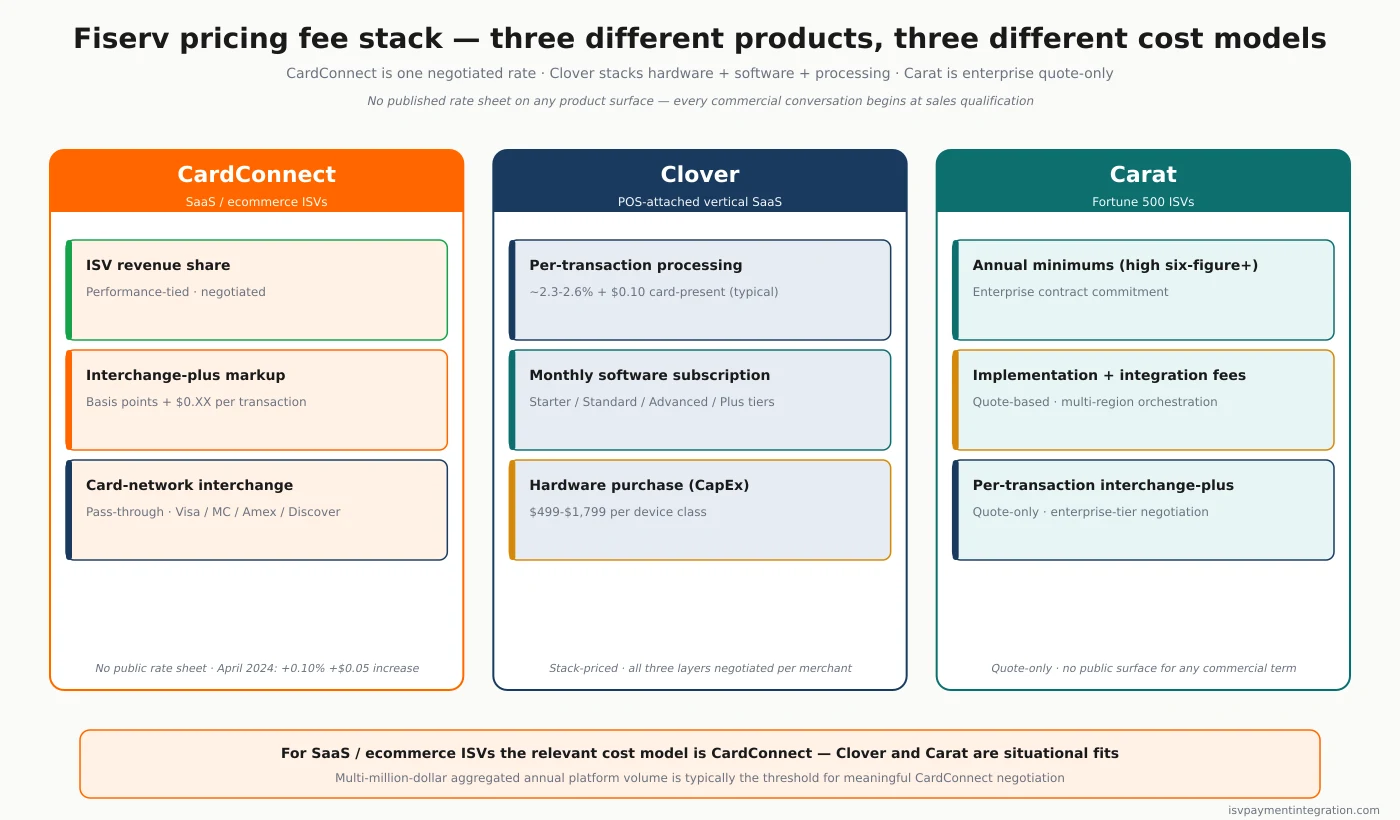

The first thing to understand: Fiserv is not one pricing model. It’s four, because Fiserv is four products.

CardConnect — the ISV gateway and embedded-payments product — uses interchange-plus with performance-tied revenue share via the ISV Partner Program. ISVs negotiate basis-point markup over interchange, plus per-transaction fees, plus a revenue-share percentage that depends on platform-aggregated volume, vertical mix, and the ISV’s commitment around merchant boarding velocity.

Clover — the POS hardware and commerce-OS platform — uses a three-layer pricing stack: (1) hardware purchase (real CapEx, $499-$1,799 per device class typical retail), (2) monthly software-subscription tiers (Starter, Standard, Advanced, Plus — pricing varies by vertical and device), and (3) per-transaction processing rates negotiated per merchant.

Carat — the enterprise omnichannel commerce engine — is enterprise quote-only. There is no public rate, no published tier, and no Carat developer portal that exposes commercial terms. Carat sales conversations begin at qualification and run through enterprise contracts, typically with annual minimums in the high-six to low-seven figures.

AccessOne — the consumer/patient financing product — operates on a different commercial structure entirely (financing economics rather than processing margin) and applies only to healthcare ISVs.

For most SaaS and ecommerce ISVs reading this page, CardConnect is the relevant pricing structure — the rest of this page focuses there, with a separate section on Clover for POS-attached vertical SaaS.

CardConnect’s Interchange-Plus — What’s Negotiated

Fiserv’s ISV Partner Program economics break into three commercial layers, each negotiated separately.

The interchange-plus markup

Interchange — the base cost charged by the card networks (Visa, Mastercard, American Express, Discover) — passes through to the merchant unchanged. CardConnect adds a per-transaction markup expressed as basis points over interchange, plus a flat per-transaction fee. The markup is partner-negotiated and depends on aggregated platform volume, vertical risk profile, average transaction size, and the ISV’s commitment around merchant onboarding velocity.

There is no public schedule for what markup an ISV at $1M aggregated annual volume gets versus an ISV at $10M aggregated annual volume. Independent partner reports indicate that meaningful interchange-plus negotiation begins in the multi-million-dollar aggregated annual processing range — below that, the markup typically lands close enough to flat-rate alternatives that the gateway-first complexity isn’t worth it.

The performance-tied revenue share

The ISV’s revenue share is the percentage of the markup-plus-spread that flows back to the platform. Fiserv’s partner materials is that the revenue share is “flexible,” “performance-tied,” and “never set in stone.” In practice, that means the share is volume-tiered, can step up as the ISV hits onboarding-velocity or volume milestones, and can step down if onboarding pace slows. The exact tier breaks are not publicly published.

For ISVs underwriting CardConnect economics, the revenue-share negotiation matters more than the headline markup. A 0.20% interchange-plus markup with a 70% ISV revenue share is materially better economics than a 0.15% markup with a 40% revenue share — even though the headline rate looks worse.

The April 2024 rate-increase pass-through

This is the most material recent change to CardConnect’s commercial surface. Effective April 1, 2024, CardConnect raised processing rates by 0.10% plus $0.05 per transaction across all major card networks. The increase passes through to ISV revenue-share margins on every transaction processed under affected contract structures.

For an ISV with a 70% revenue share on a 0.20% interchange-plus markup, the April 2024 increase added 0.07% directly to the ISV’s residual line on a per-transaction basis (assuming the merchant rate moved up to absorb the increase). For ISVs whose merchant rates were contractually fixed, the increase compressed the ISV residual instead. ISVs should ask their Fiserv partner rep two questions explicitly: (1) does the partner agreement have language around pass-through future increases, and (2) what is the notification period before further increases take effect.

Clover Pricing — Hardware, Software, and Processing Stacked

Clover is structurally different. Where CardConnect is one negotiated rate, Clover is three separate cost layers stacked together.

The hardware layer

Clover sells real hardware. Countertop terminals (Clover Station Solo, Clover Station Duo), mobile devices (Clover Flex, Clover Mini), handheld units, and accessory peripherals (cash drawers, receipt printers, kitchen displays) all carry upfront purchase costs in the $499-$1,799 per device range at typical retail. ISVs reselling Clover or building Clover App Market integrations see this as the merchant’s first-month CapEx purchase, separate from any processing line.

For ISVs whose value proposition is hardware-attached vertical SaaS (restaurant POS, retail multi-location, salon scheduling), the hardware cost is part of the platform’s bill. For ISVs whose merchants already own Clover hardware, the cost is amortized.

The software-subscription layer

Clover’s monthly software tiers — Starter, Standard, Advanced, Plus — are vertical-specific subscription tiers that gate features (inventory management, employee management, reporting depth, gift card capabilities, kitchen display integration). Tier pricing varies by vertical and by Clover device class; exact pricing is set per-merchant during the boarding flow.

ISVs reselling Clover see the software-subscription line on each merchant’s recurring statement. ISVs building Clover App Market integrations layer their own subscription on top of Clover’s; the merchant ends up paying the Clover tier plus the ISV’s app subscription.

The processing layer

Per-transaction processing rates on Clover are negotiated per-merchant, just like CardConnect — but the negotiation surface is shorter (merchants are typically not at a scale that allows custom interchange-plus) and the default rates are flat-tier (typically 2.3%-2.6% + $0.10 for card-present, 3.5%-3.7% + $0.10 for card-not-present at the standard tiers, though exact rates vary).

ISVs reselling Clover have less leverage on the processing rate than ISVs negotiating CardConnect at platform-aggregated volume. The trade-off is that Clover’s hardware-and-OS attachment delivers a different value proposition — the merchant gets the integrated experience, and the ISV’s revenue model often shifts toward the App Market subscription line rather than the processing residual.

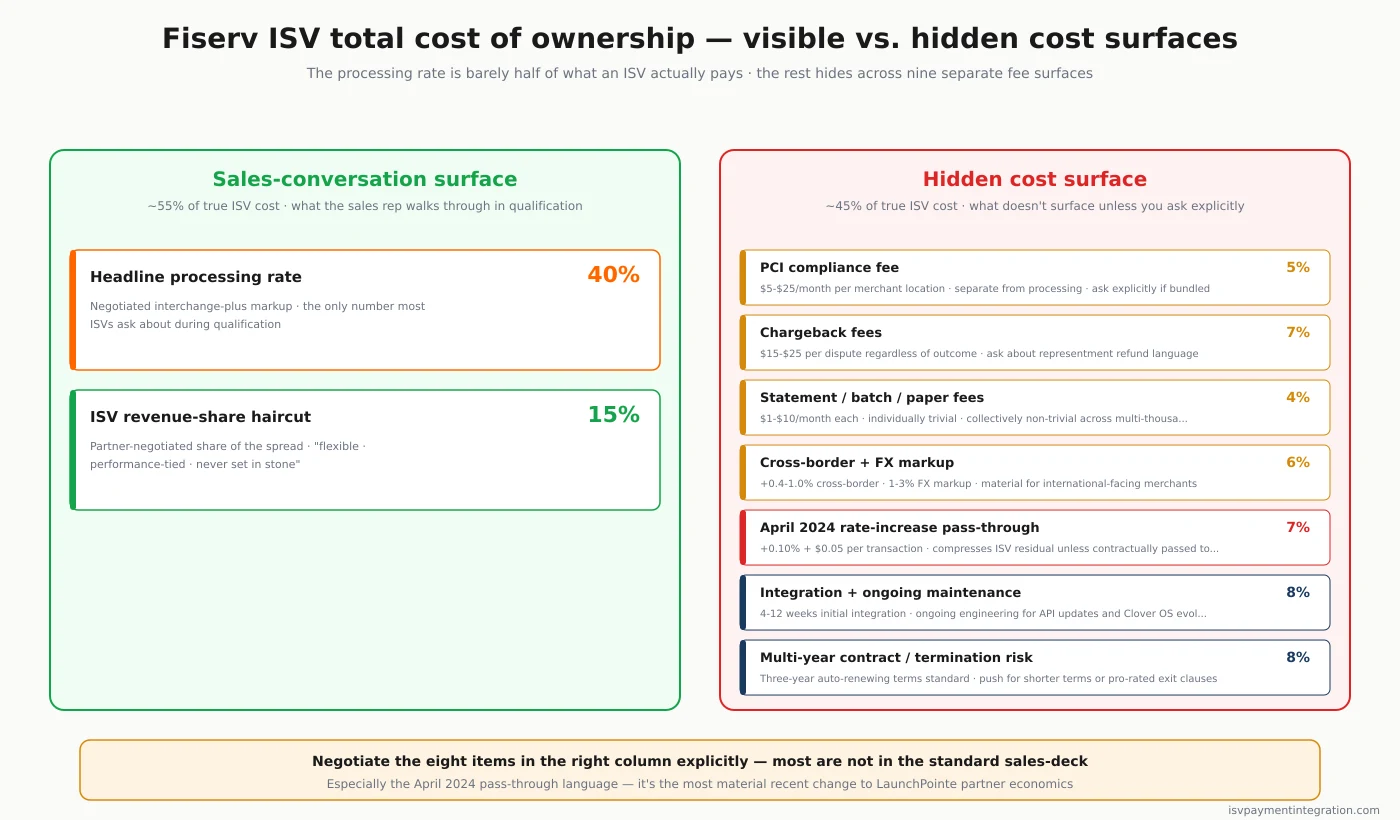

Hidden Costs ISVs Need to Model

Beyond the headline negotiated rates, ISVs integrating CardConnect or Clover should budget for several recurring costs that often don’t surface in the initial sales conversation.

PCI compliance fees — typically $5-$25/month per merchant location. Charged separately from processing. Some Fiserv contracts include PCI fees in the bundle; many don’t. ISVs need to ask explicitly during negotiation, and confirm whether the fee is per-merchant or per-location for multi-location merchants.

Chargeback fees — charged per dispute regardless of outcome, typically $15-$25 per chargeback. Material for ISVs in higher-risk verticals (subscription SaaS, restaurant chains, travel, event ticketing). Ask explicitly whether chargeback fees apply at first dispute or only at representment, and whether successful representment refunds the fee.

Statement fees, batch settlement fees, paper statement fees — small recurring line items ($1-$10/month each). Individually trivial; collectively non-trivial across a multi-thousand-merchant ISV portfolio.

Cross-border transaction fees — typically additional 0.4%-1.0% on transactions where the issuing card’s country differs from the merchant’s country. Material for ISVs serving international-facing merchants (US-based merchants accepting EU consumer cards, etc.).

Currency conversion markup — applied to multi-currency transactions, typically 1%-3% over the wholesale FX rate. Matters for ISVs with merchants accepting non-USD cards or operating multi-region.

Early termination fees — contract-specific. Many Fiserv partner agreements include three-year auto-renewing terms with prorated termination penalties for early exit. ISVs need to read the partner agreement carefully and negotiate exit clauses upfront, especially around platform M&A scenarios.

Integration and ongoing maintenance — not a Fiserv line item, but a real cost ISVs underwrite. Initial CardConnect integration typically runs 4-12 weeks of developer time depending on the integration depth (tokenization-only versus full sub-merchant boarding). Ongoing maintenance for API updates, new compliance flows, and Clover OS updates requires ongoing engineering capacity.

Where Fiserv’s Pricing Lands Against the Alternatives

Fiserv pricing only makes sense when modeled against a specific alternative. The full pricing-vs-pricing math — break-even thresholds, fee-stack comparisons, hidden-cost differentials — lives on the dedicated comparison pages:

- Stripe vs Fiserv — bundled Connect platform fee vs. negotiated CardConnect interchange-plus

- Global Payments vs Fiserv — two interchange-plus negotiated stacks side by side, post-Worldpay

- Adyen vs Fiserv — single-platform global pricing vs. US-centric multi-product fragmentation

- NMI vs Fiserv — gateway-only fees plus separate acquirer vs. CardConnect’s vertically integrated stack

- WePay vs Fiserv — JPMorgan Payments’ published-tier model vs. CardConnect’s partner-negotiated model

For also-relevant pricing-page references: Stripe pricing, Adyen pricing, Global Payments pricing, JPMorgan / WePay pricing, and NMI pricing walk through each alternative’s standalone fee structure.

The high-level pricing shape: CardConnect typically out-performs Stripe Connect’s bundled fee at multi-million-dollar aggregated annual platform volume, ties or loses below that threshold, and competes head-to-head with Global Payments and JPMorgan on enterprise ISV economics. The honest answer is that the cheapest processor isn’t always the best choice for ISVs — total cost of ownership, residual transparency, and contract-termination risk often matter more than the headline rate.

What ISVs Should Negotiate Explicitly

The Fiserv negotiation process is partner-led and partner-specific, but several terms recur as worth pushing on across most ISV partner agreements.

- The headline interchange-plus markup — basis points and per-transaction. Push for explicit volume-tier breakpoints in writing.

- The revenue-share percentage — both the starting tier and the step-up schedule as the ISV hits volume or onboarding milestones.

- Pass-through change language — what happens if Fiserv raises processing rates again (as in April 2024). Push for either contractual pass-through to merchants or notice-period protection.

- Sub-merchant boarding APIs and turnaround time — how fast does the CardPointe boarding flow approve a new merchant in your highest-priority vertical. Push for SLA language around boarding-decision time.

- PCI fee inclusion — confirm whether PCI fees are bundled or separate. Push for inclusion at the highest volume tiers.

- Chargeback fee structure — first-dispute versus representment, refund-on-successful-representment. Push for refund language.

- Termination clauses — multi-year terms are standard; push for shorter terms or pro-rated exit on platform M&A.

- Account-coverage continuity — the layoff history through 2024-2025 means partner-rep turnover is a real risk. Push for named-account-coverage language.

The cheapest processor isn’t always the best choice for ISVs. A platform that costs slightly more per transaction but offers better revenue sharing, faster merchant onboarding, transparent pricing structures, or lower contract-termination risk often delivers higher net payment revenue and lower platform-overhead cost. Fiserv’s value proposition — seven-bank ISO sponsorship distribution, white-label CardConnect branding, the Clover POS-OS ecosystem — has to be weighed against the negotiation friction, opacity, and operating-context risks.

For the full ISV-fit analysis across CardConnect, Clover, and Carat, see the Fiserv ISV review. For head-to-head pricing comparisons, see Stripe vs Fiserv, Global Payments vs Fiserv, and NMI vs Fiserv.