WePay vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

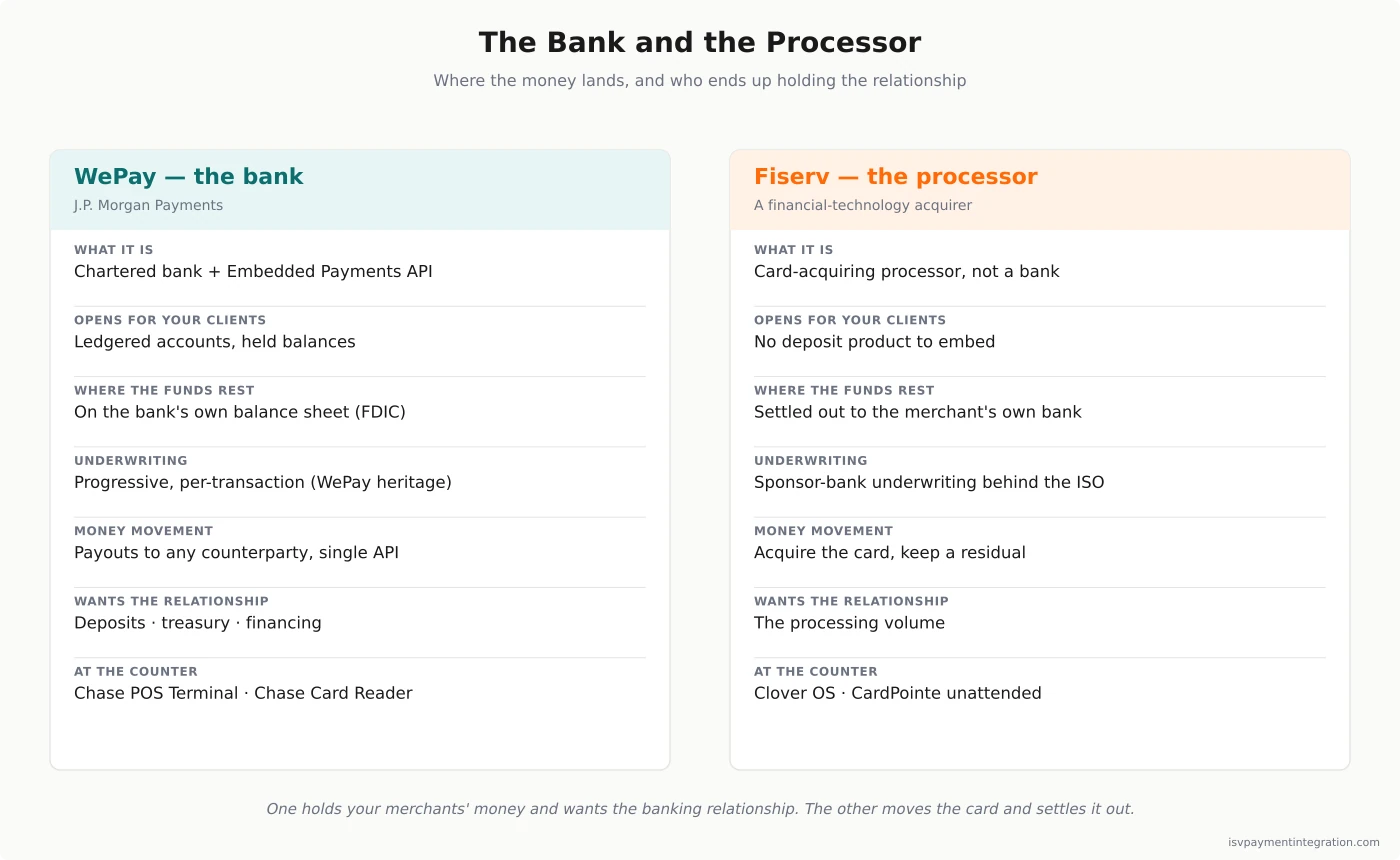

One of these companies is a bank that can open your merchants' accounts, hold their money and underwrite them transaction by transaction; the other is the machinery that moves a card payment and keeps a slice of it. WePay no longer stands on its own — it is the small-business engine folded inside J.P. Morgan Payments now — so the real decision a software platform faces is whether embedded payments should pull a banking relationship onto a bank's own balance sheet, or stay pure acceptance that settles out to whatever bank the merchant already uses.

Feature Comparison

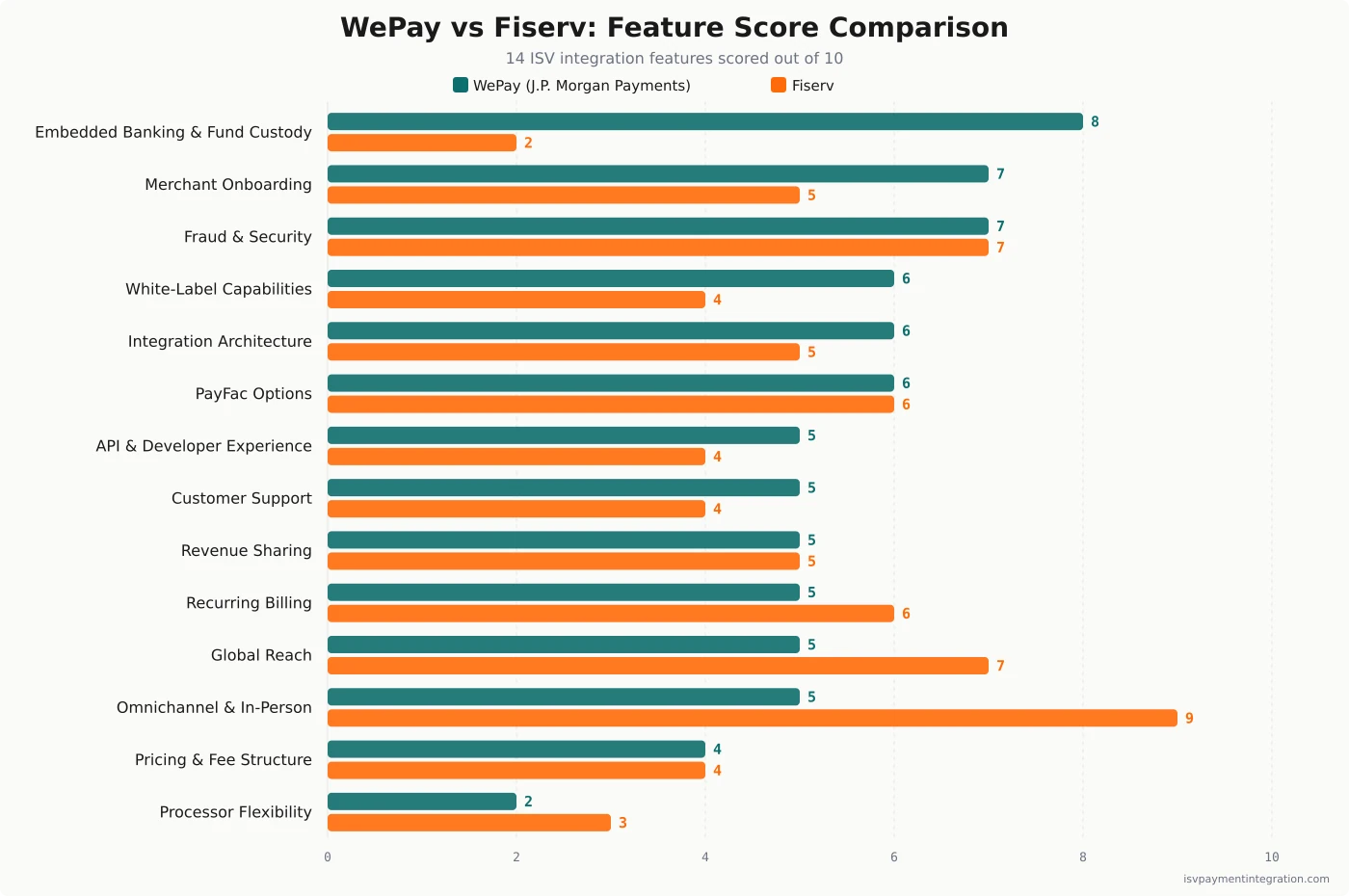

| Feature | WePay | Fiserv |

|---|---|---|

| Embedded Banking & Fund Custody | 8 | 2 |

| Merchant Onboarding | 7 | 5 |

| Fraud & Security | 7 | 7 |

| API & Developer Experience | 5 | 4 |

| Integration Architecture | 6 | 5 |

| Customer Support | 5 | 4 |

| PayFac Options | 6 | 6 |

| White-Label Capabilities | 6 | 4 |

| Revenue Sharing | 5 | 5 |

| Recurring Billing | 5 | 6 |

| Global Reach | 5 | 7 |

| Omnichannel & In-Person Payments | 5 | 9 |

| Pricing & Fee Structure | 4 | 4 |

| Processor Flexibility | 2 | 3 |

Get this comparison as a shareable PDF

We'll send the WePay vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

WePay

Best for marketplaces, platforms and vertical SaaS that need to move money — hold funds, split payouts to counterparties, open ledgered accounts — where a bank's balance sheet, real-time underwriting and treasury are themselves the product. Accept a US-first footprint, an enterprise sales cycle rather than an API key, and pricing negotiated relationship by relationship.

Best for

Fiserv

Best for software whose merchants live behind a counter or need the broadest US acquiring reach, and that wants its payments partner to stay a processor — invisible rails and a residual — rather than a bank that also wants the deposit and treasury relationship. Accept a negotiated rate you cannot benchmark and a route that opens through CardPointe, Clover or a Fiserv sales conversation.

WePay vs Fiserv: The Bank and the Processor

There is a fact about this matchup that no feature grid will show you, and it is the most interesting thing on the page. On June 14, 2026, Fiserv named a new chief executive, Takis Georgakopoulos. For the seven years before he arrived, from 2017 to 2024, he ran payments for J.P. Morgan’s Corporate & Investment Bank — the franchise that absorbed WePay. So when a software platform sits down to compare WePay against Fiserv today, it is comparing two companies that, four weeks before this was written, were shaped by the same person, now on opposite sides of the table.

That is a fitting way in, because the deeper you look the less these two are the same kind of company at all. WePay does not really exist as its own product anymore; J.P. Morgan Chase acquired it in 2017 and, over the following years, folded its capabilities into J.P. Morgan Payments. The old standalone site is gone — wepay.com now returns an empty storage bucket — and small-business acceptance is sold as Chase Payment Solutions, a part of J.P. Morgan Payments. Fiserv is the other thing entirely: a financial-technology company, the world’s largest merchant acquirer by its own accounting, that moves card payments and keeps a residual. One side of this comparison is a bank; the other is the acceptance infrastructure that thousands of those banks — and millions of merchants — depend on to move card volume.

Quick Take: A Bank’s Balance Sheet and an Acquiring Residual

WePay reaches a software platform as J.P. Morgan Payments. The clearest expression of what that means is the bank’s Embedded Payments product, whose developer portal describes it plainly: “Onboard clients, manage funds, and trigger payouts from your platform, integrated end to end through a single API.” A platform can create limited accounts for its clients, transaction accounts for itself or any counterparty, move money between them, and pay out exactly when needed — with J.P. Morgan carrying the identity verification and due diligence. The capabilities WePay is remembered for, digital onboarding and progressive underwriting, live inside that machine now, re-underwriting relationship risk with each incremental transaction. What a platform integrates here is a bank’s ability to open accounts and hold money, wrapped in an API.

Fiserv approaches software companies through its ISV Partner Program, and the numbers it puts forward are all about acquiring scale — it ranks itself first among the world’s merchant acquirers, points to 78 billion merchant transactions each year, and says its footprint touches almost every household in the country. Acceptance flows through the CardPointe gateway; CoPilot handles portfolio management; and the program names “Managed PayFac Capabilities” as the way Fiserv runs facilitation for a partner. Clover, the countertop commerce system, sits beside it, and for most vertical software those two products are the way into Fiserv. What a platform wires up here is acceptance: rails that authorize a card and push the settled money out to whatever bank the merchant keeps.

The two are not competing to be the better version of one product. They are answers to a prior question: should embedded payments bring a bank onto your platform, or bring the broadest possible card acceptance while a bank stays out of it?

The Executive Who Ran Both Sides

It is worth staying with the Georgakopoulos appointment, because it is not trivia — it is a signal about where Fiserv is heading. His entire immediate background is the bank-owned, embedded model. At J.P. Morgan he was Global Head of Payments for the Corporate & Investment Bank, the organization now selling the very Embedded Payments product on the other side of this comparison. Fiserv reached for that background at a moment of open turbulence: it lost its previous CEO on June 12, 2026 and its president on July 7, and it is defending securities class actions that, according to Fiserv’s own Form 10-Q, allege its statements about Clover’s growth were misleading. Those are allegations, not findings, and the company says it intends to defend them.

The reason this matters to a platform choosing a payments partner is forward-looking. Fiserv has just installed a leader whose expertise is exactly the thing Fiserv structurally is not — a bank that embeds accounts and deposits into platforms. It is reasonable to expect Fiserv to push harder toward embedded finance under him. But today, the distinction is stark and real: J.P. Morgan Payments already is the bank, and Fiserv is the processor that would have to build or rent the banking relationship it does not own. You are choosing between a capability that exists now and a direction of travel.

What You’re Actually Integrating: Accounts and Funds, or Card Acceptance

Strip the branding away and the integrations do different jobs. J.P. Morgan’s Embedded Payments is organized around money custody: its documentation walks through client onboarding, accounts, external accounts, transactions, notifications and reports. The verbs are open, hold, move, and pay out. A marketplace that owes hundreds of sellers, a platform that needs to escrow funds until a job is done, a software company that wants each customer to have a real ledgered account — those are the shapes this product is built for, and they are shapes a pure card processor is not built to serve, because acceptance ends when the money settles out to an external bank.

Fiserv’s integration is organized around acceptance. Through CardPointe a platform’s merchants take cards online and, with the gateway’s unattended support, at the counter; through Clover they run the physical point of sale. The verb is charge. It is an enormous, reliable, deeply distributed acceptance capability — but it stops at settlement. Fiserv is, famously, a giant of bank technology: its Financial Solutions segment runs core banking, account processing and digital banking for thousands of financial institutions. That, though, is a business Fiserv sells to banks — not something a software platform embeds through CardConnect or Clover. What the ISV integration gives you is acceptance; the money it acquires lands in the merchant’s own bank, and Fiserv keeps none of it on the platform’s behalf.

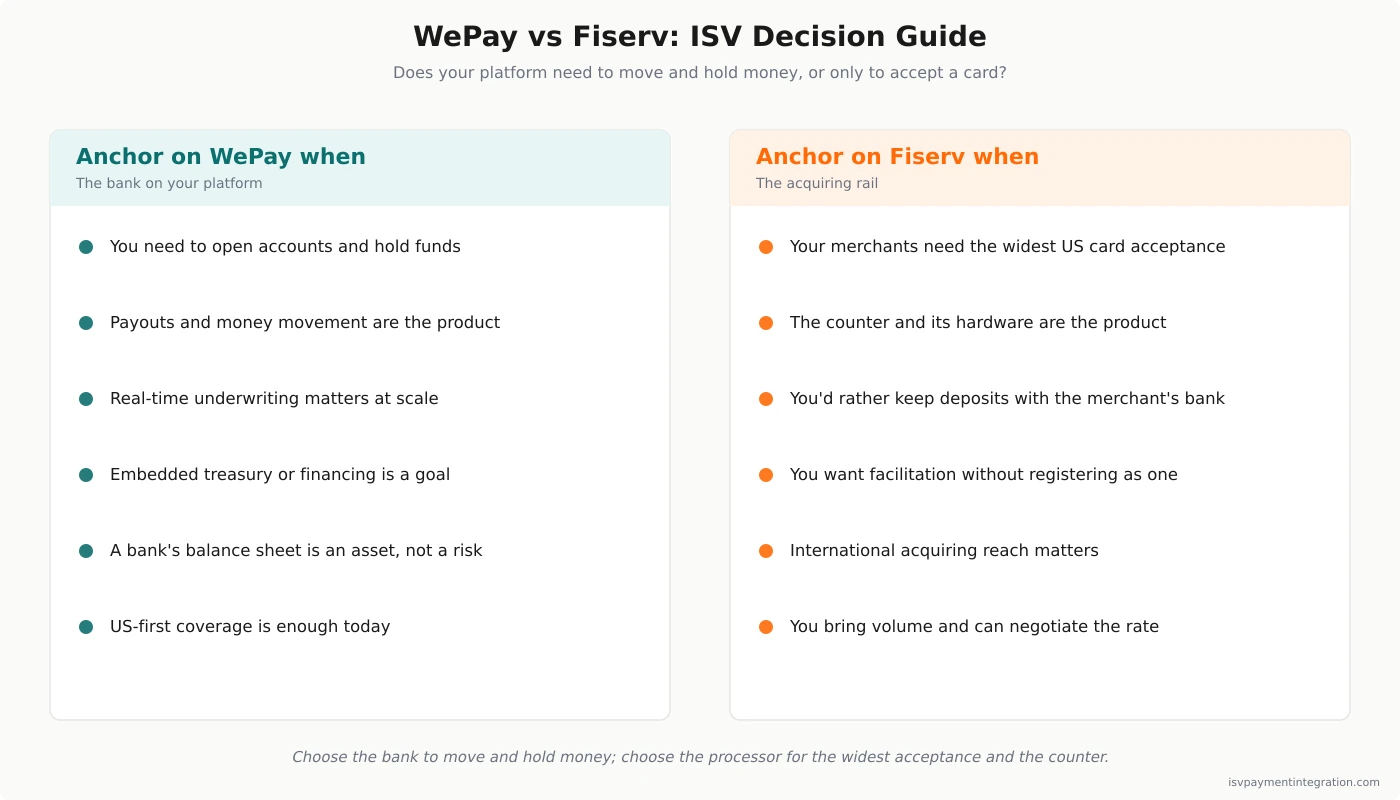

So the first question is not “which API is nicer.” It is “does my platform need to move and hold money, or only to accept a card?” If your product is fundamentally a marketplace, a payout engine, or an accounts-holding platform, J.P. Morgan’s model reaches somewhere Fiserv’s does not go. If your product needs cards taken cleanly across a wide merchant base — especially at a physical counter — Fiserv’s reach is the deeper well.

Where the Money Lands — and Who Keeps the Relationship

This is the axis most comparisons of these two miss, and it is the one that actually decides the fit. When you embed J.P. Morgan Payments, the funds move through accounts the bank opens and controls. Its Embedded Finance page markets exactly this: “Accept, manage and transfer funds” from inside your platform, with account solutions, treasury and value-added services layered on. Whether a given balance is a fully insured merchant deposit or a settlement position held in flow depends on how the product is configured — but either way the money runs across the bank’s own rails rather than passing straight through to an outside account. That proximity is the strategy, not a side effect: a bank that powers your platform’s payments is well placed to grow into the treasury, credit and account relationship with your merchants. Its client stories point the same way — BILL extending credit to small businesses “in minutes” through an API sub-ledger, an insurer moving regulated payments through J.P. Morgan Concourse. The relationship, not just the swipe, is what a bank is reaching for.

Fiserv’s ISV integration is built to do none of that. Through CardConnect or Clover it monetizes the transaction and passes the funds onward; on that path there is no account for your merchant’s operating balance to sit in and no treasury layer to switch on. For a platform, the two models are a genuine trade-off. Route payments through the bank and your merchants can gain accounts, faster access to funds, working capital and treasury — real value — but a very large institution now sits inside that relationship, its embedded product is pitched at enterprise scale (the sign-up is a sales conversation, not a self-serve key, and a small ISV may not clear the bar), and its roadmap answers to a bank’s priorities rather than yours. Keep Fiserv as a pure acquiring rail and the banking relationship stays with the merchant and whatever bank they already use; you forgo the embedded-finance upside, but nothing on the acquiring path is angling to move your merchants’ money onto someone else’s books.

That is the fork. It is not about which company is bigger — both are vast — but about whether you want a bank’s balance sheet inside your platform or deliberately kept out of it.

What WePay Became: The SMB Engine Inside J.P. Morgan Payments

If you evaluated WePay years ago as the processor behind GoFundMe and countless marketplaces, it is worth updating the picture, because the thing you would be buying today is not that company. J.P. Morgan describes the acquisition candidly in its own words: WePay is “a prime example of our acquisition strategy,” and it has “integrated WePay’s capabilities into the broader J.P. Morgan Payments suite.” Two of those capabilities are named specifically — digital onboarding, which the bank says it is “replicating WePay’s approach across the business,” and progressive underwriting, which lets it re-underwrite risk transaction by transaction at scale. The person who was WePay’s chief product officer for small business, John Frerichs, now heads SMB Payments at J.P. Morgan.

Practically, that means a few things for a platform. The WePay brand survives mostly as a wrapper; new small-business acceptance is Chase Payment Solutions, and platform-scale money movement is Embedded Payments. J.P. Morgan Payments publishes no rate or price for that integration — economics are set enterprise by enterprise, so treat any specific WePay or Chase number you find elsewhere as unconfirmed. The footprint is US-first. And the counter is more covered than the old WePay ever was: J.P. Morgan was the first bank to launch Tap to Pay on iPhone and now sells a Chase POS Terminal and a Chase Card Reader. What you are choosing, then, is not a scrappy independent gateway; it is a line of business inside the largest U.S. bank, with the strengths and the gravity that implies.

Fiserv’s Answer: Reach Without a Balance Sheet

Set against a bank, Fiserv’s pitch is reach, and it is a serious one. By its own count it is the biggest merchant acquirer anywhere, clearing on the order of 78 billion transactions a year, which buys a platform dependable settlement, funding, and underwriting that stretches across a sprawling and uneven merchant base. Its Managed PayFac Capabilities let a software company hand Fiserv the compliance and sponsorship burden while still showing merchants a facilitation experience under its own brand — sub-merchant onboarding, split funding and the rest — without standing up as a facilitator in its own name. That is a real product. It simply arrives priced behind a sales desk instead of on a page anyone can read.

Reach also means the counter, and that is Clover’s ground. A merchant does not treat Clover as a checkout widget bolted to its software; it is the register, the ticket printer and the order screen the business runs on all day, so vertical software that plugs into Clover is plugging into the tool its merchant already lives inside. CardConnect carries the same acceptance into unattended lanes, and the wider CardConnect–Clover–Carat lineup is mapped in the Fiserv review. What Fiserv keeps back is the figure a platform most wants to see: the ISV Partner Program page presents a CardPointe gateway, a CoPilot portfolio tool and a Managed PayFac line, then stops at a lead form, with no processing rate and no revenue-share percentage printed anywhere on it. Its one published price sits in the Clover App Market, whose developer terms claim 30% of an app’s net revenue — a charge on software, not on a swipe. Bargaining against that silence is the subject of the Fiserv pricing breakdown; for a rail that, unlike Fiserv, publishes its platform pricing outright, see Stripe vs Fiserv.

The Consolidation on Both Sides

Neither company is a stable independent you are quietly slotting into. That is a fact worth pricing, and the two risks are different in kind. On the J.P. Morgan side, the risk is being small inside something enormous: the WePay integration retired a standalone product and moved onboarding onto the bank’s own platform, a bank’s roadmap answers to a bank’s priorities rather than a platform’s, and a small ISV can find the enterprise sales motion a poor fit. On the Fiserv side, the risk is a company in visible transition — a new CEO after a leadership vacuum, a president’s departure weeks later, and unresolved securities litigation over Clover that, per its own filings, it is defending. A platform choosing between them is not choosing stability over instability; it is choosing which kind of consolidation it would rather build on, and writing its agreement — notice periods, an exit path, portability of the merchant relationship — accordingly. For the adjacent reads, Stripe vs WePay frames the same J.P. Morgan Payments successor against an API-first rail, and WePay vs Tilled sets it against an independent payment-facilitation platform that publishes its share.

WePay vs Fiserv: ISV Decision Guide

- Does your platform need to move and hold money, or only to accept a card? Marketplaces, payout engines and accounts-holding products reward J.P. Morgan’s Embedded Payments; a platform that only needs cards taken cleanly is well served by Fiserv’s acceptance rail. This one question predicts most of the rest.

- Do you want a bank’s balance sheet inside your product, or deliberately kept out? J.P. Morgan opens accounts and holds funds in flow inside your platform, and can grow into the treasury and account relationship; Fiserv’s acquiring path settles funds out to the merchant’s own bank and reaches for none of that.

- Does the sale happen at a physical counter? When a hardware operating system matters more than the web checkout, Clover’s decade-plus head start decides it, and J.P. Morgan’s in-person options — real as they now are — are the lighter side.

- How much does US-only versus international acceptance matter? WePay’s successor centers small-business acceptance on the US; Fiserv brings the international First Data acquiring network as well.

- Do you need facilitation economics without registering as a facilitator? Both answer this — J.P. Morgan by carrying onboarding and accounts, Fiserv through its named Managed PayFac Capabilities — so weigh it on funds custody and reach, not on whether the option exists.

- How will you price a rate neither company publishes? J.P. Morgan Payments and Fiserv both negotiate embedded and ISV economics privately; model your revenue against your own volume with the revenue calculator rather than a headline number.

- Which consolidation can your agreement survive? One partner is a line of business inside a bank whose priorities can shift with the bank’s; the other is a public company mid-transition. Write notice, exit and portability terms for whichever you choose.

Frequently Asked Questions

Is WePay still a company I can sign up with, or is it J.P. Morgan now?

Functionally it is J.P. Morgan. JPMorgan Chase acquired WePay in 2017 and integrated its capabilities into J.P. Morgan Payments; the standalone wepay.com site is no longer live. New small-business acceptance is sold as Chase Payment Solutions, and platform-scale money movement is J.P. Morgan’s Embedded Payments product. The WePay name survives mainly as a wrapper, and the digital onboarding and progressive-underwriting capabilities WePay was known for now run inside the bank. So when you compare “WePay vs Fiserv,” you are really comparing J.P. Morgan Payments against Fiserv — a point Stripe vs WePay makes in the same way.

What is the real difference between WePay and Fiserv for an ISV?

One is a bank and the other is a processor, and that shapes everything. J.P. Morgan Payments can open ledgered accounts for your platform’s clients, hold balances in flow, move money between counterparties and pay out — its Embedded Payments product is organized around funds custody, on the bank’s own balance sheet. Fiserv is a financial-technology company that bills itself the #1 global merchant acquirer; through the CardConnect or Clover integration it charges the card and settles the proceeds out to the merchant’s bank, keeping none of it on the platform’s path. (Fiserv does run core-banking and deposit systems — but for banks, through a separate business, not through the ISV integration.) If your platform needs to move and hold money, the bank reaches somewhere the acquiring rail does not; if it needs the widest card acceptance and a counter hardware ecosystem, Fiserv is the deeper option.

Does either WePay or Fiserv publish its pricing?

Neither publishes the number that matters to a platform. J.P. Morgan Payments negotiates embedded and platform economics enterprise by enterprise and shows no rate for the integration on its developer pages; Fiserv shows no CardPointe rate or ISV revenue-share figure on its ISV Partner Program page, which ends at a contact form. The one rate Fiserv does publish is the Clover App Market’s, which takes 30% of an app’s net revenue — a fee on software, not on card processing. Treat any specific WePay, Chase or Fiserv rate you find on a third-party page as unconfirmed, and model your economics against your own volume.

Which is better for in-person and counter payments?

More even than it used to be, but Fiserv still wins when the counter is the center of gravity — and the reason starts on the WePay side. The WePay many platforms remember was online-first, built for marketplaces and crowdfunding; its successor is not. J.P. Morgan was early to Tap to Pay on iPhone and now ships a Chase POS Terminal and a Chase Card Reader, so a platform building on it can take an in-person card cleanly. What that stack does not include is a Clover — a single device a merchant runs the entire working day on, with years of installed base, an app ecosystem, and CardConnect extending acceptance into unattended lanes. If your software lives in restaurants, salons or field crews where the hardware in a hand is part of what you sell, that depth belongs to Fiserv and it decides the question; if your merchants are online-first, WePay’s bank-side money movement counts for more than the terminal.

Why does Fiserv’s new CEO matter to this comparison?

Because it tells you where Fiserv is trying to go. Takis Georgakopoulos, named Fiserv’s CEO on June 14, 2026, spent 2017 to 2024 running payments for J.P. Morgan’s Corporate & Investment Bank — the same organization that absorbed WePay and now sells the Embedded Payments product on the other side of this comparison. His background is the bank-owned, embedded-finance model that Fiserv, as a processor, does not natively have. It is reasonable to expect Fiserv to push toward embedded finance under him, but that is a direction of travel, not a capability you can integrate today. Right now, J.P. Morgan Payments already is the bank, and Fiserv is the acquiring rail — which is the distinction this whole comparison turns on.