WePay vs Tilled

A feature-by-feature comparison for ISVs integrating payments.

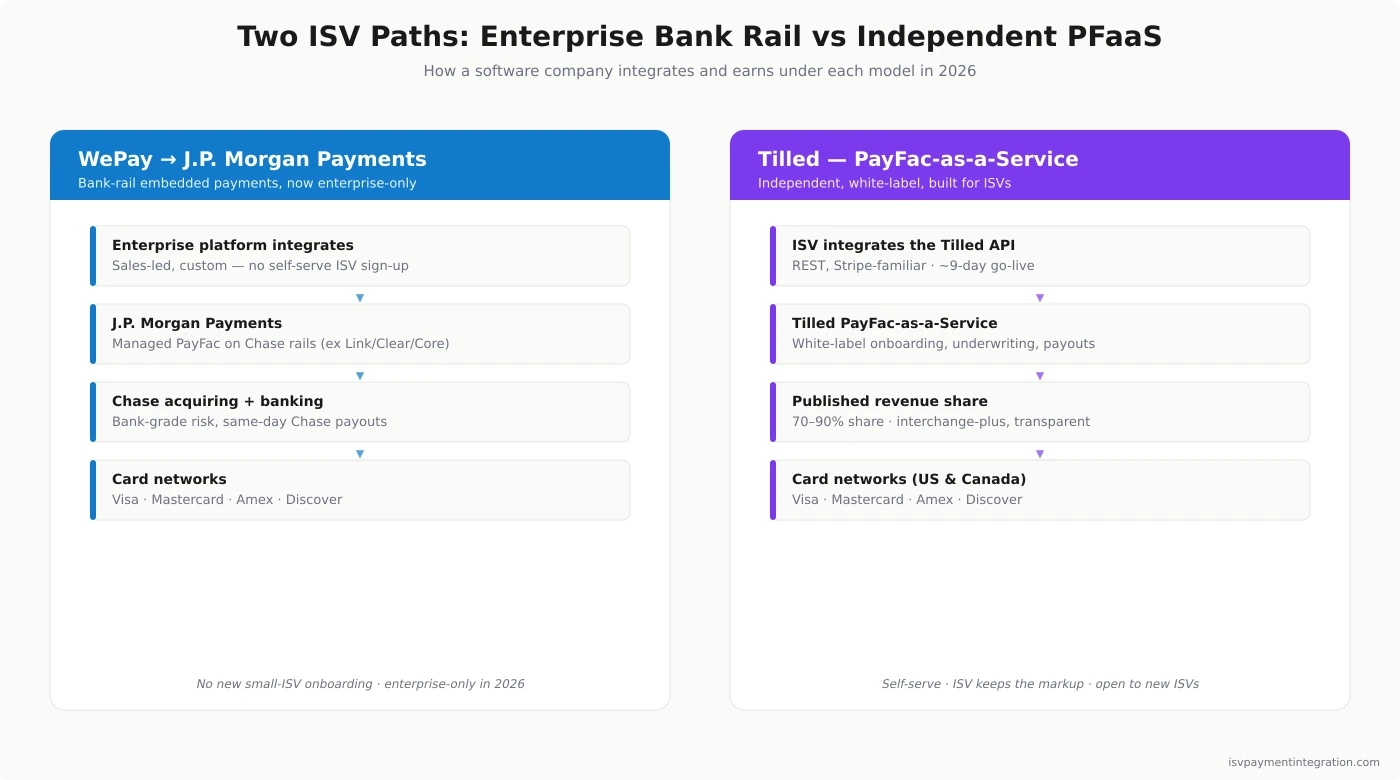

WePay's standalone ISV product is gone — folded into J.P. Morgan Payments, which now courts enterprise platforms. For a new software company, Tilled's independent PayFac-as-a-Service is the live option. Here is how the two compare and what displaced WePay partners should do next.

Feature Comparison

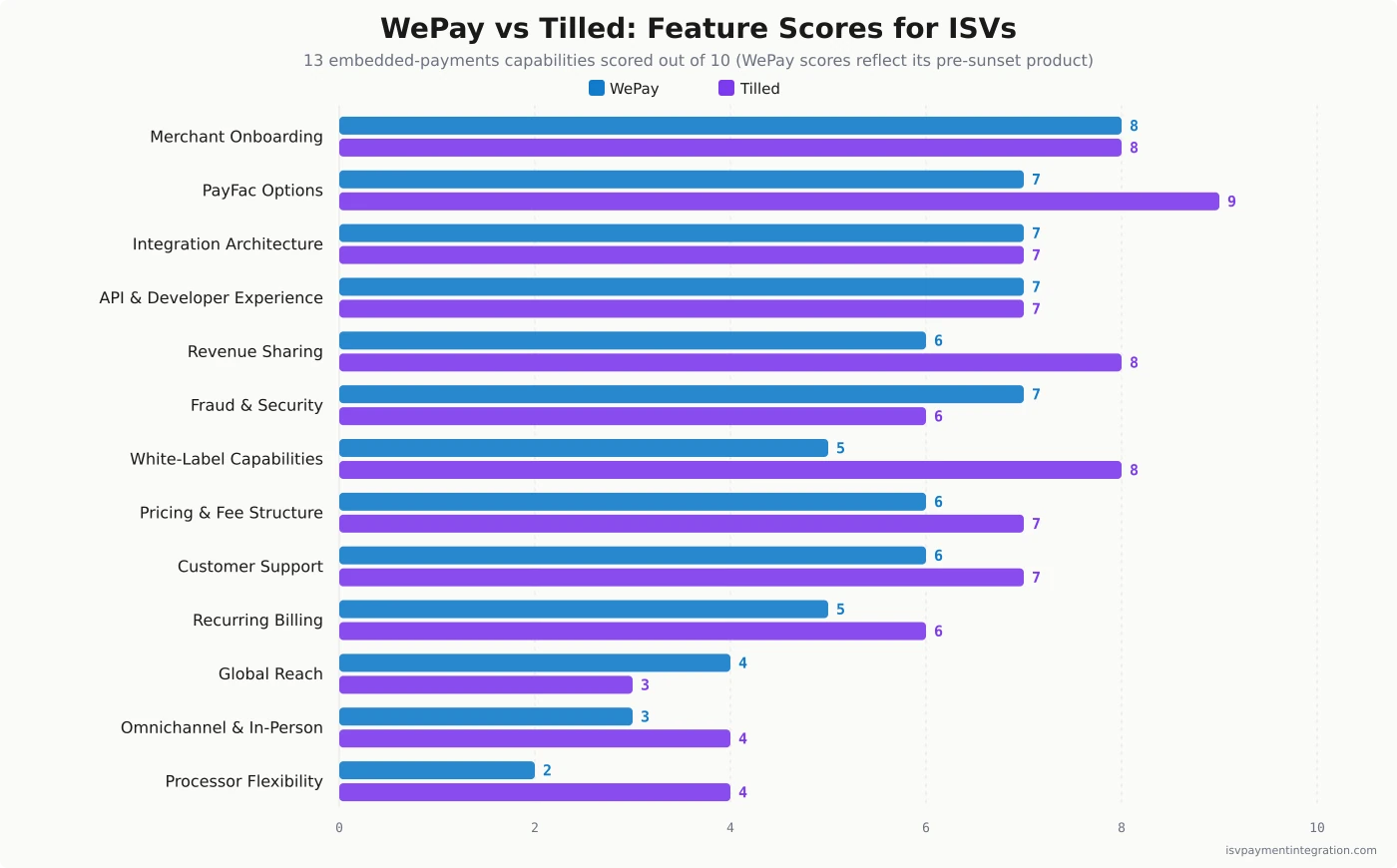

| Feature | WePay | Tilled |

|---|---|---|

| Integration Architecture | 7 | 7 |

| API & Developer Experience | 7 | 7 |

| White-Label Capabilities | 5 | 8 |

| Processor Flexibility | 2 | 4 |

| Pricing & Fee Structure | 6 | 7 |

| Omnichannel & In-Person Payments | 3 | 4 |

| Fraud & Security | 7 | 6 |

| Revenue Sharing | 6 | 8 |

| Merchant Onboarding | 8 | 8 |

| Global Reach | 4 | 3 |

| Recurring Billing | 5 | 6 |

| Customer Support | 6 | 7 |

| PayFac Options | 7 | 9 |

Get this comparison as a shareable PDF

We'll send the WePay vs Tilled breakdown to your inbox — ready to share with your team.

Best for

WePay

Best only for enterprise platforms with the scale and banking relationship to work directly with J.P. Morgan Payments. The standalone WePay product was retired in 2025 and no longer onboards small or mid-market ISVs.

Best for

Tilled

Best for new and small-to-mid-market ISVs that want transparent published pricing, fast white-label onboarding, and a PayFac-as-a-Service partner actively building for software companies in the US and Canada.

If you are comparing WePay and Tilled in 2026, start with the fact that changes the whole decision: WePay, as a product a software company can sign up for, no longer exists. The brand was absorbed into J.P. Morgan Payments, and the standalone platform that once powered GoFundMe and a thousand other sites was retired for new ISVs. So this is less a head-to-head between two live options and more a map of where the WePay era went — and why Tilled is the choice an ISV actually makes today.

Why This Comparison Changed in 2026

Visit go.wepay.com now and you get a tombstone: “WePay is now part of J.P. Morgan Payments.” No sign-up, no API docs, no pricing. Chase acquired WePay in December 2017 for a reported $400 million, and after years of running it as a semi-independent unit, J.P. Morgan said in May 2024 that WePay’s capabilities would be “fully integrated into our modern commerce platform” within roughly a year. By mid-2025 that migration was done and the WePay brand was effectively retired.

Tilled, by contrast, is very much alive — an independent company that coined the term “PayFac-as-a-Service” and has spent since 2018 building exactly the kind of embedded payments product WePay used to sell to small platforms. So the honest framing of WePay vs Tilled is this: a legacy bank rail that withdrew from the small-ISV market versus the independent challenger that moved in to serve it. The feature scores below reflect product capability, but for a new software company only one of these is a door you can actually walk through.

What Happened to WePay

WePay was founded in 2008 by Bill Clerico and Rich Aberman, who built it into the back-end payments infrastructure for online marketplaces and crowdfunding sites — GoFundMe, Constant Contact, and Meetup among more than a thousand platforms at its peak. Its pitch was simple: let platform businesses — and the small businesses transacting on them — accept payments without every merchant opening its own account. That was the same merchant-aggregation problem PayPal had attacked from the consumer side and Stripe would later attack from the developer side, and for marketplaces WePay was often the better-fit answer. It was a true platform-payments pioneer: split payments, customizable checkout, and APIs built for software companies long before “embedded payments” was a category. That heritage is why WePay still shows up in any serious comparison of ISV payment providers (WePay is now part of J.P. Morgan Payments).

Chase bought it to compete with Stripe and Square in the platform market. For a while it worked — WePay’s Link, Clear, and Core tiers gave ISVs a graduated path from simple merchant referral to full PayFac infrastructure on Chase rails. Then the strategy shifted. In July 2023, JPMorgan Chase abruptly offboarded a swath of long-standing WePay ISV and merchant clients, a move The Information framed as a retreat from the segment. Through 2024 the wind-down was staggered by contract — Keap, FundEasy, Yapsody, and others published migration notices — and most displaced partners moved to Stripe. By 2025 the door to new small-ISV business was closed.

Today J.P. Morgan Payments is an enterprise machine. It processes more than $10 trillion a day across 200-plus countries and is the largest US merchant acquirer, with roughly $2.6 trillion in 2024 volume. Its embedded-payments push now targets healthcare, automotive, energy, insurance, and marketplaces — it powers seller payouts for Walmart Marketplace, for instance. That is a different universe from the small businesses and software platforms WePay once onboarded.

What Tilled Is in 2026

Tilled is an independent payments company founded in 2018 in Boulder, Colorado by Caleb Avery, and it built its entire identity around PayFac-as-a-Service — turnkey, white-label payment facilitation that lets a software company embed payments and earn revenue share without registering as a PayFac or carrying the underwriting risk. Roughly 90% of its ISV partners deploy it fully white-labeled, with their own subdomain, branded merchant console, and branded emails; merchants never see the Tilled name.

It is registered through Synovus (Pinnacle) and Citizens banks, holds Level 1 PCI Service Provider status, and has raised about $63 million across nine rounds, most recently a $12.5 million Series B in late 2024 led by Canvas Ventures to fund card-present and international expansion. One honest caveat for an ISV doing diligence: Tilled does not publish processing volume or named client counts, and its most recent filing in March 2026 was a small $1 million bridge rather than a new growth round — a fair question mark about scale. It is a credible independent, not a bank.

Geographically, Tilled processes in the United States and added Canada in July 2025 through a partnership with KORT Payments. There is no European, Latin American, or APAC acquiring — a real limit for ISVs with international merchants. Read the full Tilled review for the deeper product picture.

Integration and Developer Experience

On paper both platforms score 7 of 10 here, but only one is something you can integrate today. Tilled’s API is REST-based and deliberately Stripe-familiar, with a sandbox, webhooks, a Checkout Sessions API, and a JavaScript drop-in (Tilled.js) that keeps PCI scope low. Tilled publishes an average partner integration time of about nine days, which is fast for full payment facilitation. For a lean engineering team, that velocity is the main draw.

WePay’s API was also well regarded in its day — clean documentation, split payments, backed by Chase’s technical resources. But those developer resources now live inside J.P. Morgan Payments’ enterprise onboarding, which is a sales-led, custom-integration process rather than a self-serve sign-up. A small software company cannot simply grab WePay API keys and build. The practical developer-experience comparison in 2026 is Tilled’s nine-day self-serve path versus an enterprise procurement cycle.

PayFac Models and Onboarding

This is Tilled’s home turf — its core product is PayFac-as-a-service, and it scores 9 to WePay’s 7 on PayFac options. Tilled lets a software company function like a full payment facilitator — owning the merchant experience, setting sub-merchant pricing, and keeping the markup — while Tilled carries underwriting, compliance, KYC/KYB, MATCH and OFAC checks, dispute management, and reconciliation. Onboarding is API-driven with same-day activation, and both platforms tie at 8 of 10 on onboarding speed.

WePay ran a managed-PayFac model too: through its Core tier, Chase acted as the sponsor and handled compliance, so ISVs got PayFac economics without registering with the card networks. The capability was real. The catch is availability — that model is no longer sold to new small ISVs. If you are building an embedded payments program from scratch in 2026, the managed-PayFac option on the table is Tilled’s, not WePay’s. For the broader pattern, see how Tilled stacks up against Finix and Payrix, its closest live competitors.

Pricing and Revenue Economics

The pricing contrast is the sharpest part of this comparison, and it favors transparency. Tilled publishes its full schedule. Two public tiers run the model: a Start-Up plan at a 70% revenue share with a $500 monthly platform fee for ISVs processing under $5 million a month, and a Scaling plan at 80% revenue share and $2,500 a month above that, with an enterprise tier reaching roughly 90% share. Tilled’s underlying cost to the ISV — its Schedule A — is published at 7 basis points plus $0.05 per transaction plus $6 per active merchant per month, on an interchange-plus basis. An ISV marks merchants up from there and keeps its share of the spread as payments revenue.

WePay, in its last published form, used a flat-rate model around 2.9% plus $0.25 per transaction. J.P. Morgan Payments today publishes the successor in detail — a named Embedded Payments product with a full developer portal and API documentation for onboarding clients, managing funds, and triggering payouts from your platform — but it publishes no rate or price for that integration; the economics are negotiated enterprise by enterprise behind a sales process. For an ISV trying to model unit economics before committing engineering time, that asymmetry matters: with Tilled you can build a revenue forecast from a public rate card; with J.P. Morgan you cannot get a number without an enterprise conversation. Compare the published detail in the Tilled pricing and WePay pricing breakdowns.

Stability vs Flexibility: The Real Trade-off

The instinctive case for WePay was always stability — the backing of the largest US bank, Chase-grade risk and fraud infrastructure, and same-day payouts to Chase business accounts. The scorecard still gives WePay the edge on fraud and security (7 vs 6) and a slight edge on global reach. But the 2023 partner culling complicates the “stability” story: the very thing that looked like a strength — being inside a giant bank — is what let that bank exit the segment with limited notice when priorities shifted. WePay’s own customer reviews skew negative on exactly this theme, citing extended fund holds and email-only support with no recourse.

Tilled’s pitch is the opposite: flexibility and control. Transparent pricing, ISV-owned merchant relationships, contracts written to let partners move merchants off the platform, and a dev-first integration. The honest counterweight is scale — an independent startup that has not disclosed volume carries more platform-continuity risk than a trillion-dollar bank. The realistic read is that the bank offered stability until it didn’t, and the independent offers transparency and control with a scale question attached. For most new ISVs, control over your own payments economics has proven the more durable bet.

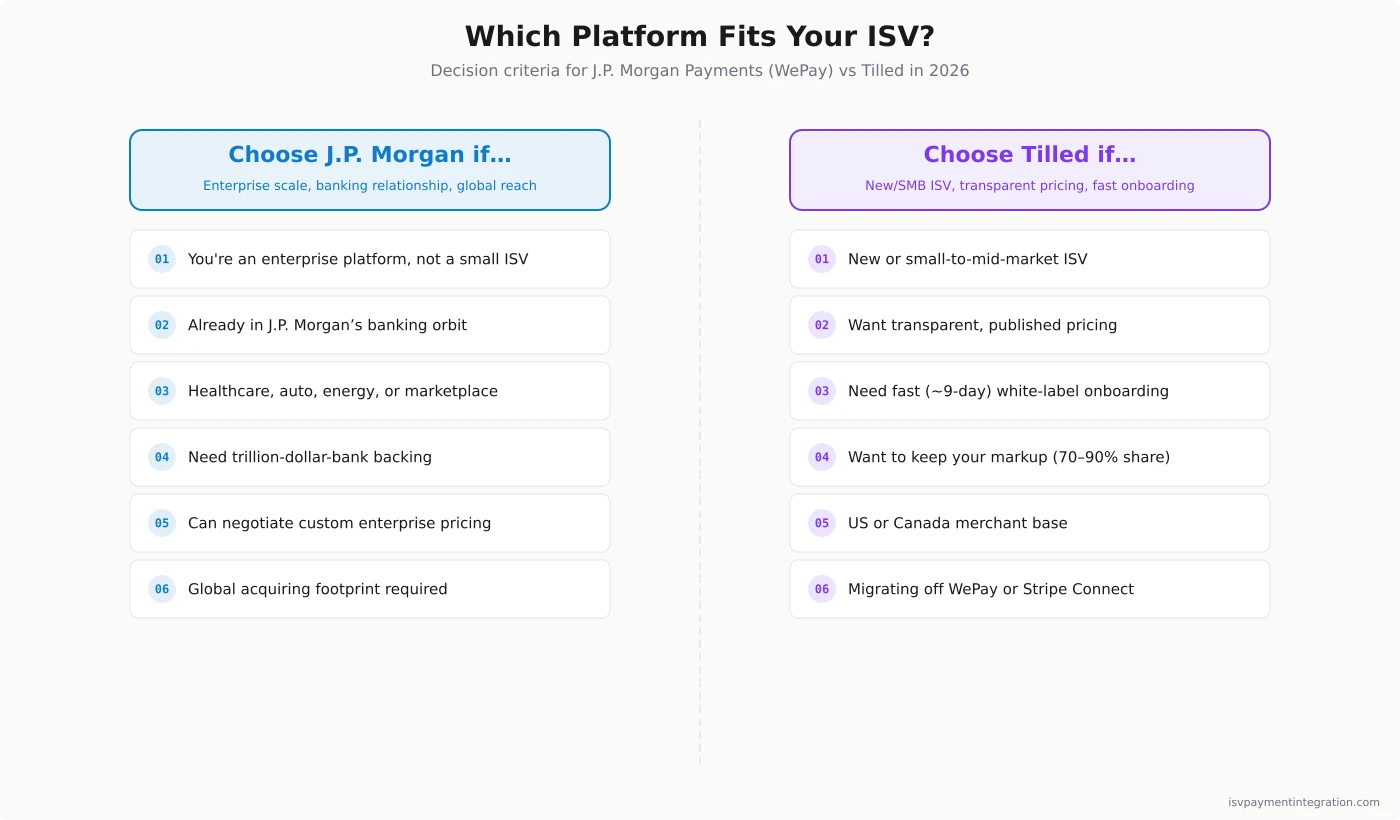

Where Each Platform Wins

Tilled wins for nearly every software company evaluating this in 2026: new ISVs, small-to-mid-market platforms, and teams that want published pricing, white-label control, fast onboarding, and a partner whose entire business is courting software companies. It is the natural home for builders who would otherwise start on Stripe Connect but want better revenue share and white-label control.

WePay — now J.P. Morgan Payments — wins only for enterprise platforms with the volume, vertical, and banking relationship to integrate directly with the bank’s commerce platform. If you are a large marketplace in healthcare, retail, or energy already in J.P. Morgan’s orbit, that’s a real option. If you are a displaced WePay partner, the practical migration path is Tilled, Stripe Connect, or Finix depending on whether you prioritize transparent revenue share, developer ubiquity, or infrastructure control.

WePay vs Tilled: ISV Decision Guide

Choose Tilled if you are a new or small-to-mid-market ISV that wants transparent published pricing, white-label control, fast self-serve onboarding, and US or Canada processing — which describes most software companies building payments today.

Choose WePay (J.P. Morgan Payments) only if you are an enterprise platform with the scale and banking relationship to negotiate a direct integration; new small-ISV onboarding under the WePay brand has ended.

If you inherited a WePay integration or are weighing legacy options, get an ISV payments assessment and we will map your merchant base and volume to the right live platform.

Frequently Asked Questions

Is WePay still available, and is it owned by Chase?

WePay is owned by JPMorgan Chase, which acquired it in December 2017, but it is no longer available as a standalone product. By mid-2025 WePay was fully folded into J.P. Morgan Payments, and go.wepay.com now redirects to J.P. Morgan. New ISVs cannot sign up for WePay; the bank’s embedded-payments offering is sold through J.P. Morgan Payments to enterprise platforms.

What happened to WePay, and who founded it?

WePay was founded in 2008 by Bill Clerico and Rich Aberman and became the payments back-end for crowdfunding sites and marketplaces like GoFundMe. Chase acquired it in 2017, ran it as a platform-payments unit, then in July 2023 began offboarding many small ISV partners. The brand was integrated into J.P. Morgan Payments by 2025. Most displaced partners migrated to Stripe, Tilled, or Finix.

How much do WePay and Tilled charge?

WePay’s last published rate was a flat 2.9% plus $0.25 per transaction; J.P. Morgan Payments now publishes no public pricing and negotiates per enterprise. Tilled publishes its schedule: a 70% revenue share with a $500 monthly fee under $5M/month, 80% and $2,500/month above that, and an enterprise tier near 90%. Tilled’s underlying cost is interchange plus roughly 7 basis points, $0.05 per transaction, and $6 per active merchant monthly.

Who are WePay’s biggest competitors?

In the ISV and embedded-payments market, the competitors that absorbed WePay’s niche are Stripe Connect (the developer-default), PayPal (through Braintree for platforms), Tilled (PayFac-as-a-Service with published pricing), Finix (infrastructure-layer PayFac), and Payrix, now part of Worldpay for Platforms inside Global Payments. For a displaced WePay partner, Stripe and Tilled are the most common destinations.

Is Tilled a true PayFac alternative to a bank-backed processor?

Yes, for the segment WePay served. Tilled’s PayFac-as-a-Service gives a software company the full economics and control of being a payment facilitator — sub-merchant onboarding, underwriting, payouts, and revenue share — without registering with the card networks or carrying the compliance burden. It is independent and processes in the US and Canada, so it suits North American ISVs rather than platforms needing global acquiring.