Finix vs Xplor Pay

A feature-by-feature comparison for ISVs integrating payments.

Finix is payments infrastructure a software company builds on and eventually owns; Xplor Pay is a vertical-SaaS embedded-payments partner you plug into. The right pick depends on whether your ISV wants to run payments or have a partner run them with you.

Feature Comparison

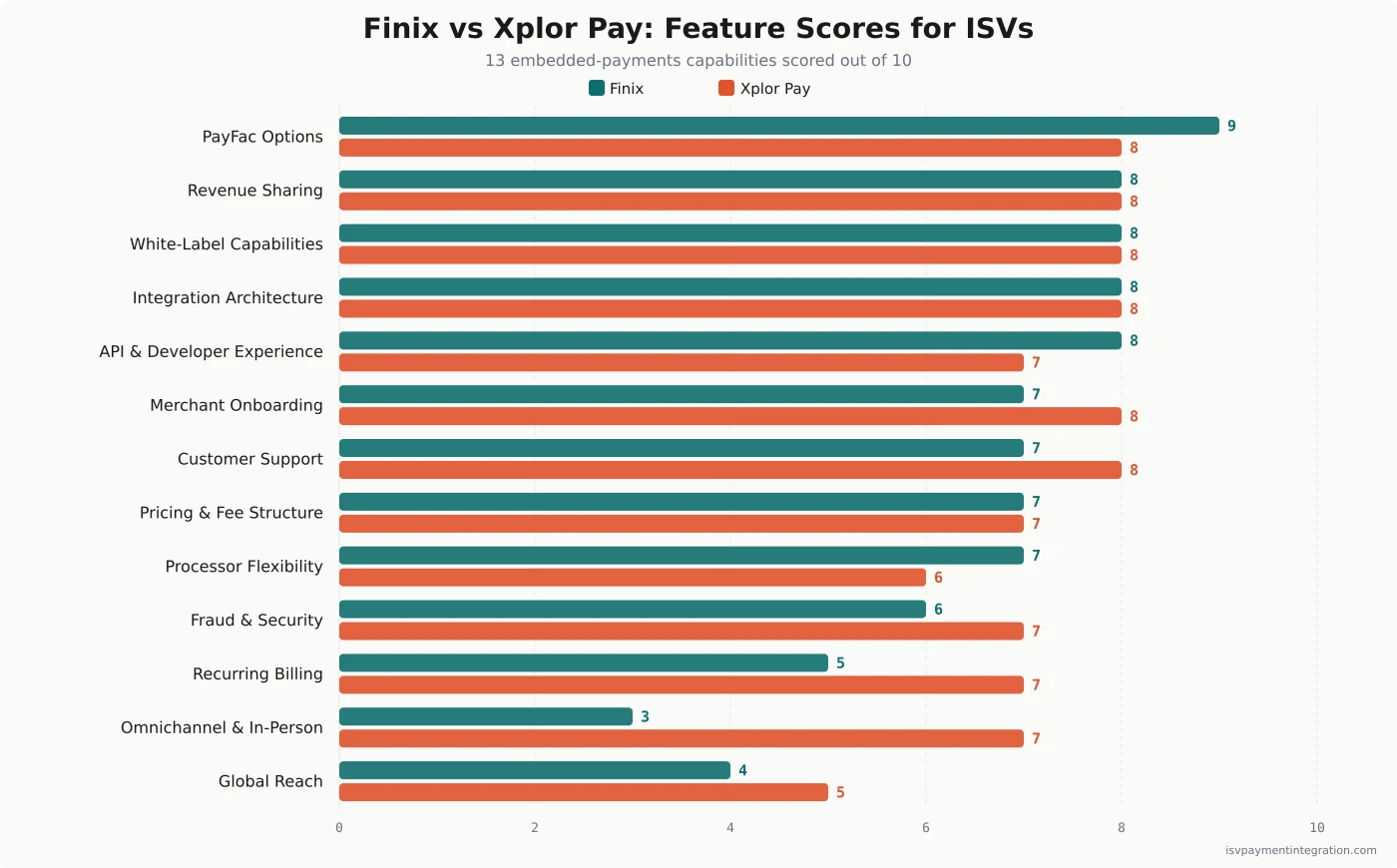

| Feature | Finix | Xplor Pay |

|---|---|---|

| Integration Architecture | 8 | 8 |

| API & Developer Experience | 8 | 7 |

| White-Label Capabilities | 8 | 8 |

| Processor Flexibility | 7 | 6 |

| Pricing & Fee Structure | 7 | 7 |

| Omnichannel & In-Person Payments | 3 | 7 |

| Fraud & Security | 6 | 7 |

| Revenue Sharing | 8 | 8 |

| Merchant Onboarding | 7 | 8 |

| Global Reach | 4 | 5 |

| Recurring Billing | 5 | 7 |

| Customer Support | 7 | 8 |

| PayFac Options | 9 | 8 |

Get this comparison as a shareable PDF

We'll send the Finix vs Xplor Pay breakdown to your inbox — ready to share with your team.

Best for

Finix

Best for developer-led ISVs and marketplaces in the US and Canada that want to own their payments stack, see transaction-level economics, and grow into a registered PayFac on a single platform.

Best for

Xplor Pay

Best for vertical SaaS ISVs that need in-person and online payments, cash-discount or surcharge margin programs, and a managed, consultative partner rather than infrastructure to operate themselves.

Finix and Xplor Pay both promise the same outcome — a new line of payments revenue for your software company — but they ask for opposite things in return. Finix hands an ISV the rails and the controls and expects the team to drive. Xplor Pay puts a partner in the passenger seat and offers to do most of the driving for you. Picking between them is less about feature checklists and more about how much of the payments business your software company actually wants to run.

Finix vs Xplor Pay: The Core Difference for ISVs

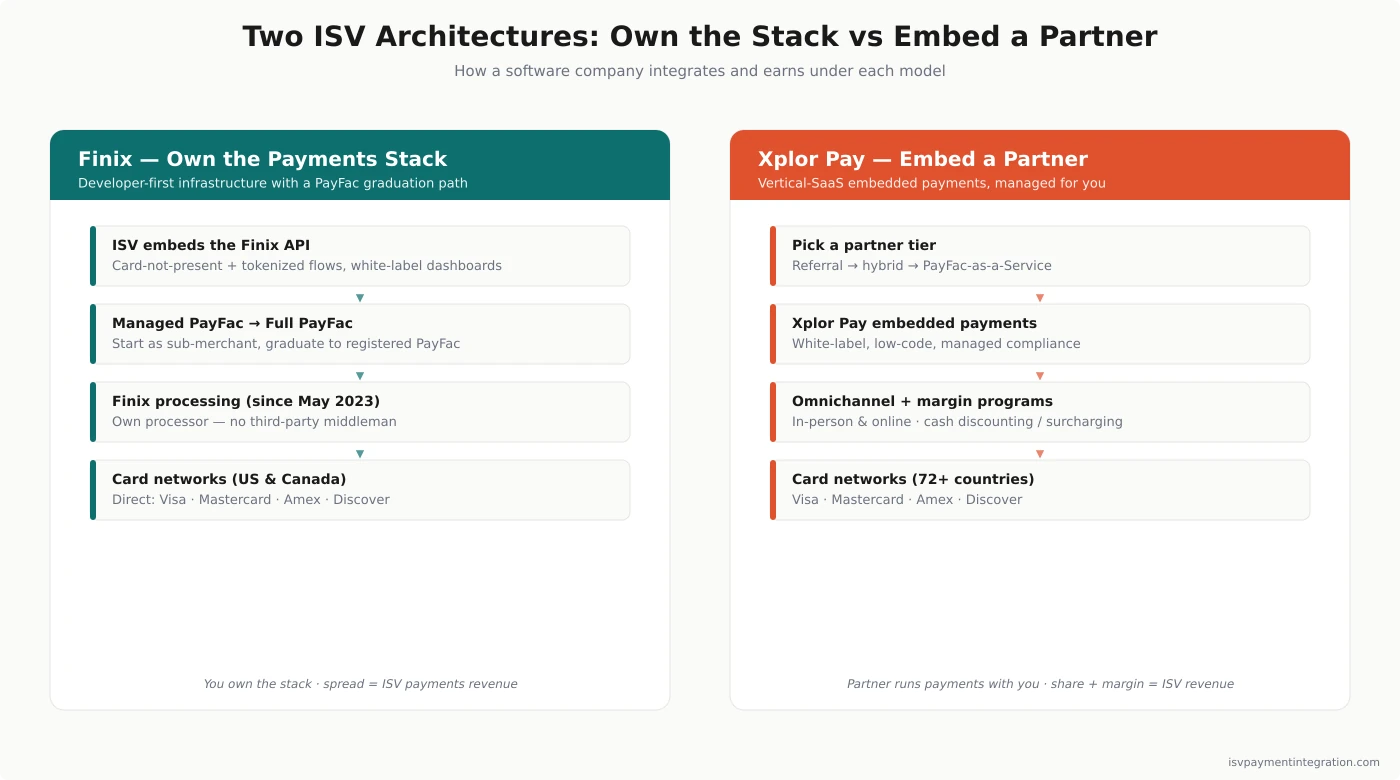

Finix is payments infrastructure you build on. It is an API-first stack designed for platforms and marketplaces that want the economics and control of a payment facilitator without first building one from scratch. The mental model is ownership: you embed the rails, set merchant pricing, watch the transaction-level numbers, and over time you can take on more of the PayFac responsibilities yourself.

Xplor Pay is a payments partner you embed with. It grew up inside Xplor Technologies serving real-world verticals — fitness studios, field-service crews, golf clubs, childcare centers — so its instinct is to package payments as a managed service that a software company switches on. The mental model is partnership: you choose how much of the payment experience to own, and Xplor Pay handles the parts you would rather not.

That split runs through every comparison below. Finix optimizes for control and transparency; Xplor Pay optimizes for speed, omnichannel coverage, and a relationship. Neither is “better” in the abstract — they suit different kinds of ISVs. The scorecard reflects it: the two platforms are close on integration, white-label, and revenue sharing, and they separate sharply on in-person payments and developer ownership.

What Finix Is in 2026: A Processor That Cut Out the Middleman

The most important fact about Finix is recent: on May 2, 2023, Finix became a registered payment processor with direct certification from all four major U.S. card networks — Visa, Mastercard, American Express, and Discover (Finix announcement). Before that, Finix routed transactions through a third-party processor. Now it sends authorization and clearing messages to the networks itself, with Pathward as the sponsoring bank. For an ISV, “full-stack acquirer processor” is not marketing — it means one fewer layer of cost and dependency between your software and the card networks.

Finix holds a registered payment facilitator license and Level 1 PCI DSS Service Provider certification, the highest tier. It processes more than 400 million transactions per day across the United States and Canada at a stated 99.999% API uptime. In October 2024 it closed a $75 million Series C led by Acrew Capital, bringing total funding to roughly $208 million (TechCrunch) — money explicitly raised to compete with Stripe in the platform payments market.

One limitation matters up front: Finix operates in the US and Canada only. There is no European acquiring, so a platform onboarding merchants abroad will hit a wall. Named software clients include Beyond, foreUP, Passport, Pay Theory, and Archy — a roster that skews toward vertical software companies embedding payments rather than consumer brands. If you want the granular read, the Finix review goes deeper on product and support.

What Xplor Pay Is in 2026: From Clearent to an Embedded Payments Partner

Xplor Pay is the platform formerly known as Clearent. On July 8, 2025, Clearent by Xplor rebranded to Xplor Pay (Xplor announcement), and the change was more than cosmetic. The company shifted from a traditional credit card processor — historically a referral-partnership business — to a “consultative, embedded payments partner,” adding PayFac-as-a-Service and tailored integrations so software companies can control as much, or as little, of the payment experience as they want. Chief Product Officer Nick Campbell framed the rebrand around giving software companies “speed, flexibility, and scalability” through a new suite of purpose-built APIs.

Behind it sits Xplor Technologies, a SaaS-plus-payments company operating across more than 72 countries, serving 130,000-plus businesses and processing over $47 billion in payments a year. Its verticals are distinctly real-world: fitness and leisure, recreation, golf and club, field services, personal services, and education. A March 2026 merger with Clubessential Holdings folded in additional club and golf depth. That heritage is why Xplor Pay treats in-person payments, hardware, and managed compliance as table stakes — its merchants have always swiped and tapped cards, not just charged them online.

The rebrand also addressed a real reputation problem. Legacy Clearent was known, in third-party merchant reviews, for the friction common to ISO-era contracts: multi-year terms, early-termination fees, and statement charges. The new PFaaS and embedded model is positioned as the answer to exactly that history — transparent, ISV-controlled, and built on a modern developer stack. The Xplor Pay review covers the post-rebrand product in detail.

Integration and Developer Experience

Finix is the more developer-native of the two, and the scorecard gives it the edge on API and developer experience (8 vs 7). Its documentation is thorough, its no-code dashboard won a 2024 UX Design Award, and several ISV reviews single out a dedicated Slack support channel that responds within a day — a sharp contrast to the ticket-queue experience at larger processors. The common complaint is that the API docs, while complete, are not as polished or conventionally formatted as the most developer-obsessed platforms. For a team that lives in the API, Finix feels like a tool built by people who expect you to read the reference.

Xplor Pay closed much of the developer gap during an 18-month build-out shipped alongside the rebrand: low-code components, full white-label options, a new Developer Center, a complete integration and test environment, and chargeback dispute-management tools that submit evidence by API. The emphasis is on getting a software company live quickly with branded, embedded payments rather than handing it a bag of primitives. Dental Intelligence, a named SaaS partner, credited the new platform with “dramatically reducing development time” while delivering a branded payments experience.

The practical read: if your engineers want to own every integration detail, Finix rewards that appetite. If you want pre-built components and a partner’s technical onboarding team to carry more of the load, Xplor Pay is designed around that — which is also why it leads on merchant onboarding and support.

PayFac Models: Build Your Own vs Embed a Partner

This is where the two philosophies are clearest, and where the PayFac-as-a-service decision actually gets made.

Finix offers two lanes on one platform. In the managed model, your merchants board as sub-merchants under Finix’s master payment facilitator account — Finix handles KYC/KYB, underwriting, and card-network registration, so your ISV gets instant onboarding without the compliance burden of becoming a registered PayFac. When you are ready, you can graduate to becoming your own registered PayFac inside the same system, owning the merchant relationship and capturing more of the economics. Finix calls this “a continuous path, not a rebuild,” and it is the strongest argument for an ambitious platform: you do not have to re-platform to grow into full PayFac status. That is why Finix edges the scorecard on PayFac options (9 vs 8).

Xplor Pay runs a flexible spectrum instead — referral, then hybrid, then full PayFac-as-a-Service — letting an ISV pick its level of responsibility and monetization. The difference is posture. Finix expects you to move toward owning the PayFac function; Xplor Pay is comfortable carrying it indefinitely while you focus on software. Both give software companies genuine embedded payments, but Finix sells the destination and Xplor Pay sells the journey at whatever pace you set.

Pricing and Revenue Economics for ISVs

Finix publishes more pricing detail than most. Its standard model for platforms is interchange-plus: card-not-present transactions run interchange plus a $0.15 per-transaction Finix markup, and card-present transactions run interchange plus $0.08. ACH processing is 0.75%, a recurring-billing add-on is roughly 0.40%, and there is a volume-tiered monthly platform fee (a starter tier under $1 million in annual processing has carried a $250 monthly fee in third-party reviews). A simpler flat-rate option sits around 2.75% plus $0.30. The important caveat: Finix does not publish a standard platform rate card for ISVs — its pricing page routes platform clients to sales, so real ISV pricing is custom and negotiated on volume. The interchange-plus numbers are the published markups, not a guaranteed all-in rate.

Xplor Pay does not publish partner pricing at all. It documents the models — referral, embedded, white-label, PFaaS — but no rev-share percentages or PFaaS rates appear publicly, so an ISV has to get them through a conversation. What Xplor Pay does put forward is a distinctive margin lever most infrastructure providers ignore: enhanced-pricing programs. Its cash discounting and surcharging suite — cash discount (dual pricing), surcharging, convenience fees, and service fees — is marketed as saving merchants up to 95% on processing fees (Xplor Pay). For an ISV, those programs reduce merchant attrition and create a larger margin pool to share in.

How that revenue actually reaches your ISV differs by model. Under Finix, you set each merchant’s rate and keep the spread above your interchange-plus cost, so your payments revenue scales directly with processing volume and you can see every fee component — interchange, network assessments, and processor margin — broken out per transaction. Under Xplor Pay’s partner program, your share is structured through the partnership tier you choose, and the cash-discount and surcharge solutions add a second margin layer that flat-rate models cannot match. The question for a software company is whether you would rather engineer your own pricing and own the fee stack, or let a partner package the economics and bring merchant-savings solutions to the table.

The economics question for any software company is the same on both platforms: the spread between what your merchants pay and what the network and processor charge is your payments revenue. Finix makes that spread visible at the transaction level so you can model it precisely. Xplor Pay wraps more of it in a managed relationship and adds margin programs on top. Whichever provider you pick, model the revenue share against your real merchant base — a low-volume cohort of small businesses behaves very differently from a handful of high-volume accounts. Compare the published detail side by side in the Finix pricing and Xplor Pay pricing breakdowns.

Omnichannel and In-Person Payments

This is the single widest gap on the scorecard, and for many ISVs it decides the whole question. Xplor Pay scores 7 to Finix’s 3 on omnichannel and in-person payments, and the reason is heritage. Xplor Pay’s merchants run gyms, salons, clubs, and field-service routes — businesses that take cards across a counter, on a terminal, and online. In-person processing, terminal support, and unified online-plus-offline reporting are core to the platform.

Finix is online-first. It supports tokenized card-not-present flows well, but in-person payment hardware and terminal management are not its strength. A purely digital SaaS product may never notice the difference. A vertical software company whose merchants need to swipe, dip, or tap a card in the physical world will notice immediately. If your ISV serves brick-and-mortar verticals, omnichannel coverage is not a nice-to-have, and Xplor Pay is built for it where Finix is not.

Compliance, Onboarding, and Support

Both platforms reduce PCI scope and automate underwriting, but they package it differently. Finix runs automated KYC/KYB through MicroBilt with sanctions screening against OFAC, Canada’s OSFI, and the Interpol watch list, and reports cutting manual review by roughly 40%. Its dashboard exposes more than ten automated report types covering settlement, fees, chargebacks, and funding — the same transaction-level transparency that makes its revenue modeling strong.

Xplor Pay leans on managed compliance and a partner-success model, which is why it leads the scorecard on both merchant onboarding (8 vs 7) and customer support (8 vs 7). Its chargeback dispute-management tools automate evidence handling, and its enhanced partner portal is built for software companies running a book of merchants. For partners scaling a portfolio, that support model adds dedicated partner managers, white-label merchant statements, and help desks that field merchant payment questions on the ISV’s behalf — operational coverage a lean software team rarely wants to staff itself. Finix counters with self-serve depth: its dashboard, reporting, and developer support are built so a technical team can resolve most payment and settlement issues without opening a ticket. The trade-off mirrors the rest of the comparison: Finix gives you the instruments and expects you to read them; Xplor Pay gives you a team and expects you to lean on it. Software companies coming off a friction-heavy legacy contract often value the managed approach precisely because they have been burned by the alternative.

Where Each Platform Wins

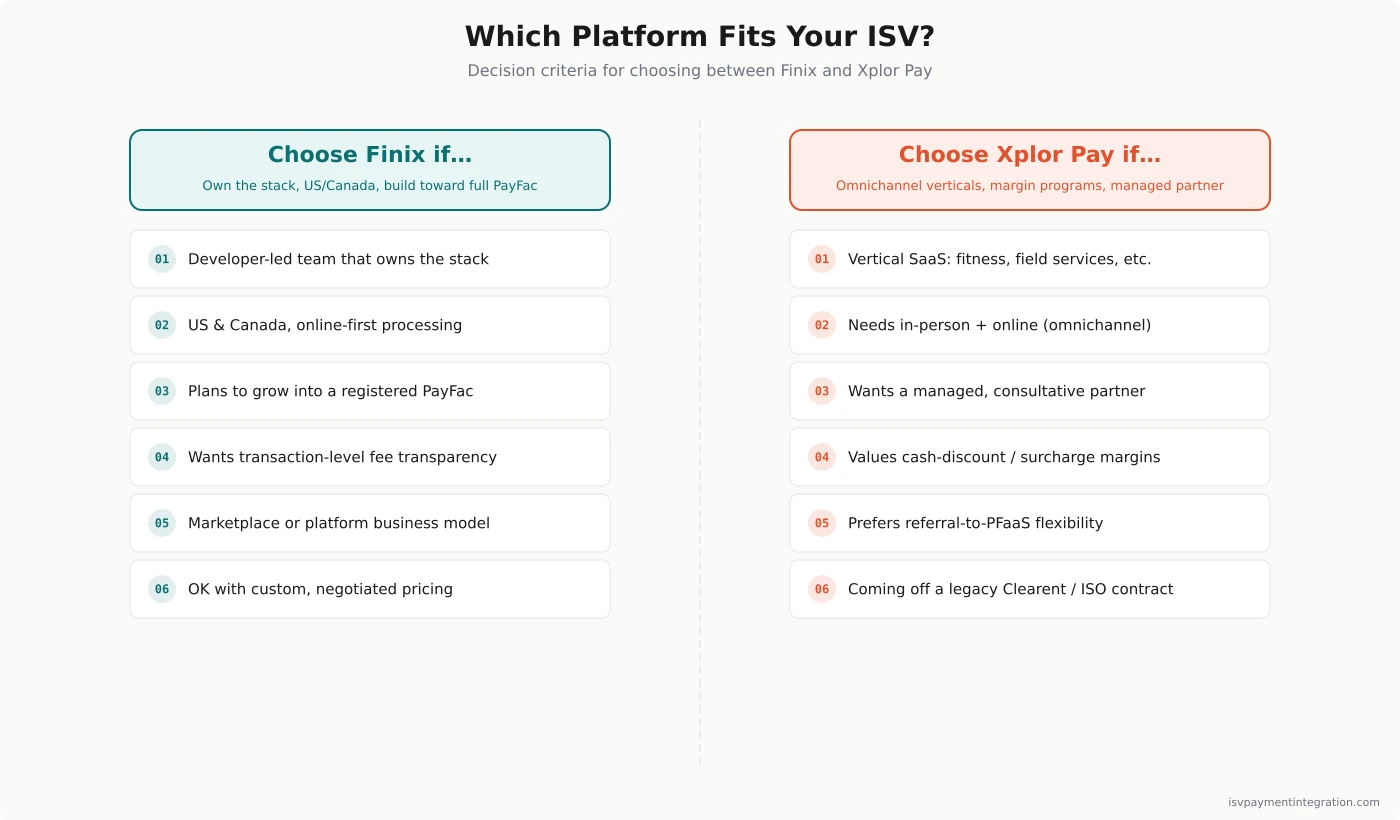

Finix is the better choice when your ISV is developer-led, processes primarily in the US and Canada, and wants to own its payments infrastructure with full visibility into the economics — especially if you plan to grow into a registered PayFac without re-platforming. Marketplaces and platforms that have outgrown aggregator pricing and want transaction-level control are squarely Finix’s audience. Its closest competitors for that buyer are Stripe Connect and Payrix / Worldpay for Platforms, and Finix sits in the mid-market slot between them.

Xplor Pay is the better choice when your ISV serves real-world verticals that need both in-person and online payments, when margin programs like cash discounting matter to your merchants, and when you would rather have a managed partner than operate payments yourself. Vertical SaaS companies in fitness, field services, healthcare, and education — the kinds of businesses Xplor already serves — fit naturally. If you are weighing it against the aggregator default, the Xplor Pay vs Stripe comparison covers that angle, and because Xplor Pay was Clearent until mid-2025, the Finix vs Clearent page points at the same platform under its former name.

Finix vs Xplor Pay: ISV Decision Guide

Choose Finix if your team wants to own the payments stack, you process in the US and Canada, you value transaction-level fee transparency, and you intend to grow into a full PayFac on a single platform.

Choose Xplor Pay if you build vertical SaaS, your merchants need in-person and online payments, you want cash-discount or surcharge margin programs, and you would rather embed a consultative partner than run payments infrastructure yourself.

Most software companies serving physical-world verticals land on Xplor Pay for the omnichannel coverage and managed model; developer-led platforms chasing infrastructure ownership land on Finix. Get an ISV payments assessment if you want help mapping your specific merchant base and volume to the right model.

Frequently Asked Questions

How much does Finix charge per transaction?

Finix uses interchange-plus pricing for platforms: card-not-present transactions are interchange plus a $0.15 Finix markup, and card-present transactions are interchange plus $0.08. ACH processing is 0.75%, and a recurring-billing add-on adds about 0.40%. There is also a volume-tiered monthly platform fee. Finix does not publish a standard platform rate card, so an ISV’s actual per-transaction cost is negotiated based on processing volume — the published figures are the markup components, not a guaranteed all-in rate.

Who are Finix’s competitors?

For ISV and platform payments, Finix competes most directly with Stripe Connect (the aggregator default), Payrix / Worldpay for Platforms (its closest enterprise PayFac rival), and Adyen for Platforms at the high end. Lower-tier alternatives include NMI, Tilled, and Stax Connect. Analysts generally place Finix in the mid-market slot — above NMI and Tilled in capability, below Adyen’s volume minimums, and head-to-head with Payrix for US vertical SaaS platforms.

Is Xplor Pay the same as Clearent?

Yes. Clearent by Xplor rebranded to Xplor Pay on July 8, 2025. It is the same processor and platform, now positioned as an embedded payments partner with a PayFac-as-a-Service offering rather than a traditional credit card processor. Legacy Clearent merchant accounts moved under the Xplor Pay brand, which is why comparison pages may reference either name for the same company.

Which platform is better for in-person and omnichannel payments?

Xplor Pay, clearly. It scores 7 to Finix’s 3 on omnichannel and in-person payments because its platform was built for real-world verticals that take cards on terminals as well as online. Finix is online-first and does not emphasize in-person hardware, so any ISV whose merchants need to swipe, dip, or tap cards should favor Xplor Pay.

Can an ISV become its own PayFac with either platform?

Both support it. Finix lets an ISV start as a sub-merchant under its managed PayFac and graduate to a fully registered PayFac on the same platform — “a continuous path, not a rebuild.” Xplor Pay offers a spectrum from referral to hybrid to full PayFac-as-a-Service, letting an ISV choose how much PayFac responsibility to take on and when. Finix is built around moving toward ownership; Xplor Pay is comfortable carrying the PayFac function for you indefinitely.