Xplor Pay Pricing

Pricing model: Interchange-plus, partnership-tier negotiated. Based on publicly available information from Xplor Pay's official site. Contact Xplor Pay directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | Interchange passthrough plus Xplor Pay markup and authorization fees; merchant statement itemizes each line |

| Markup | Revenue share negotiated by partnership tier (Referral, Embedded, White-Label, or PayFac-as-a-Service) and aggregate platform volume |

| Setup | No setup fee disclosed for ISV partners; onboarding time and engineering scope vary by tier |

| Monthly | Platform fees at the merchant level bundle PCI compliance support, gateway access, reporting, and customer service |

Hidden Costs to Watch

- ⚠ PCI non-compliance fee when the annual questionnaire is not completed

- ⚠ Chargeback and dispute handling charges per case

- ⚠ Cross-border and FX pricing negotiated separately; not published

- ⚠ ACH and alternative payment method pricing priced outside the card rev-share

- ⚠ Engineering scope shifts materially between Referral, Embedded, White-Label, and PayFac tiers

Alternatives

Xplor Pay Pricing for ISVs: What You Actually Pay in 2026

Xplor Pay pricing in 2026 is less a rate card and more a partnership framework. The brand launched on July 8, 2025 when Clearent rebranded under parent Xplor Technologies, and the shift came with a pricing conversation that looks different from the pre-rebrand integrated-payments story. ISVs no longer pick between “referral or nothing.” They pick a partnership tier, and the tier decides the economics.

This page walks through what Xplor Pay charges, what it refuses to publish, and how the four-tier model changes your cost of joining the rail. For legacy-brand context, see the Clearent pricing breakdown. For product verdicts and vertical fit, the Xplor Pay review covers the operational question.

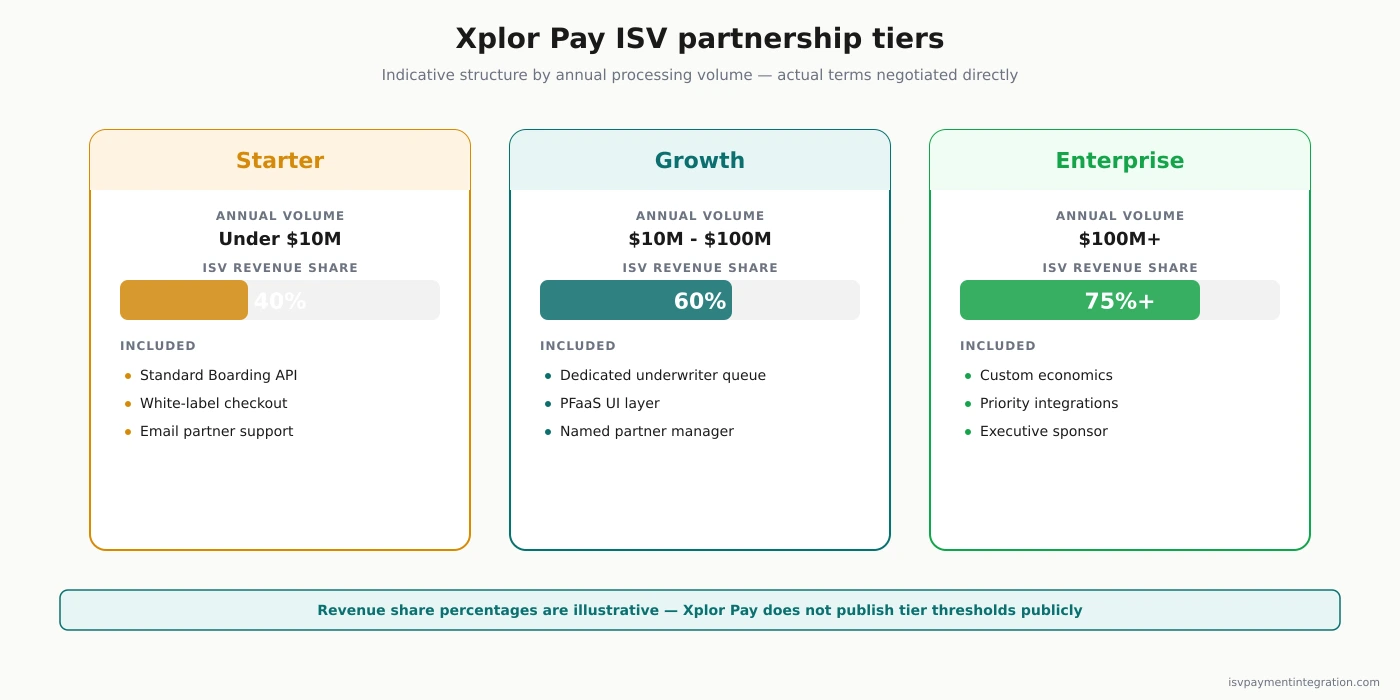

The Four Xplor Pay Partnership Tiers

The core of Xplor Pay pricing is the partnership tier you choose. Each tier shifts three things at once: the share of processing revenue that flows back to your platform, the engineering scope your team owns, and the PCI-DSS scope that sits on your side of the boundary.

Referral

The lightest tier. Your platform refers merchants, Xplor Pay underwrites and boards them, and your share is a negotiated slice of the processing margin on referred volume. Time-to-first-dollar is short and engineering is minimal. You give up most of the margin and almost all of the merchant relationship.

Embedded Payments

Integrated payments with your brand in the merchant UX. You use the Transaction API, Boarding API, and Reporting API, and your platform controls the payment surface inside your product. Rev share improves over Referral because you are doing more of the work. PCI scope expands with the direct API integration.

White-Label Payments

Xplor Pay runs the payments stack, but your brand is the only one the sub-merchant sees. This is the tier that matters for vertical SaaS platforms that sell payments as part of the product. Low-Code Components and Hosted Payments pages pull PCI scope back down even though your brand is front and center.

PayFac-as-a-Service

The deepest tier. Your platform behaves like a payment facilitator for its sub-merchants without registering as one. Xplor Pay holds the PayFac registration, the sponsor-bank relationship with Central Bank of St. Louis and Citizens Bank, and the bulk of the compliance burden. You capture the largest share of processing margin and take on the most operational weight.

Early-stage ISVs almost always start at Referral or Embedded. Platforms approaching $50M in annual processing volume across their sub-merchants begin to look at White-Label or PayFac-as-a-Service, because the rev-share math starts to cover the compliance overhead.

What Xplor Pay Does Not Publish

Xplor Pay does not publish a rate card, a rev-share percentage, or a volume threshold. That is the standard posture for platform-focused payments companies. Finix sales-gates everything under the “no-nonsense pricing” banner. Worldpay for Platforms, the former Payrix, routes /pricing to a 404. Global Payments treats US ISV pricing as an internal sales asset. Only Stripe Connect and Adyen for Platforms publish reference numbers, and even there the volume thresholds are opaque.

You cannot model Xplor Pay pricing from the website. You negotiate, and negotiation quality depends on your aggregate volume, your vertical, and the competing offers you bring.

Two data points are public. Xplor Pay’s statement-reading guide says merchant statements show “an interchange plan that shows interchange fees separately” plus “processing fees that originate from Xplor Pay” and any monthly fees. The cash-discounting program is marketed with a headline claim of “save up to 95% on processing fees” when eligible transactions route through a compliant surcharge or cash-discount flow. That is Xplor’s claim, and it applies to a subset of transactions, not the blended rate.

Hidden Costs Across Partnership Tiers

Partnership tier changes the shape of the cost stack as much as it changes the rev share. The line items below show up differently depending on the tier you pick.

PCI non-compliance fees. Applied at the merchant level when the annual PCI self-assessment is not completed. On PayFac-as-a-Service, you own the PCI workflow for your sub-merchants and the hit lands inside your program. On Hosted Payments or White-Label with Xplor-managed onboarding, exposure is smaller.

Chargeback and dispute fees. Per-case charges. Xplor Pay ships a Dispute Management API with API-based evidence submission. Neither the per-dispute fee nor the representment win rate is published.

Cross-border and FX. Not priced publicly. The parent group operates in 72-plus countries, but cross-border routing for the US payments rail is a case-by-case conversation.

ACH and alternative methods. ACH runs through the ACH Provider API and prices outside the card rev-share. eCheck economics differ from card interchange. If a material share of your GMV is ACH, model the two rails separately.

Equipment and gateway add-ons. Point-of-sale hardware, Virtual Terminal access, Text-to-Pay, and Mobile SDK deployments can carry separate fees. ISV-only integrations skip hardware; vertical SaaS platforms selling in-person acceptance to their sub-merchants pick this up.

Cash-discount program compliance. Routing merchants into the 95% surcharge program brings compliance obligations for signage, receipts, and state-level rules. Those sit with the merchant and, in practice, with you as the software layer.

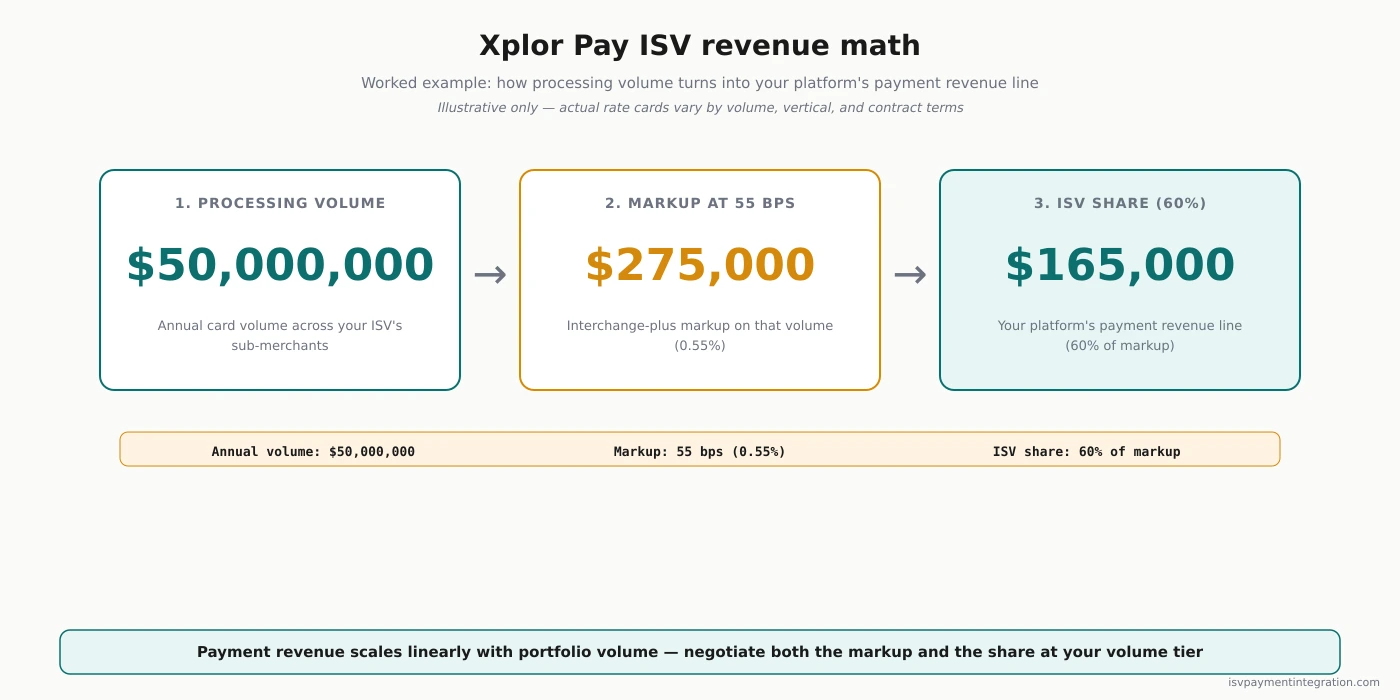

Worked Economics: An ISV at $50M Annual Volume

A software platform processing $50M annually across its sub-merchants sits in the range where all four Xplor Pay tiers are viable.

At Referral, the platform touches a small share of processing margin and carries almost no operational weight. At Embedded, rev share improves and engineering owns the Transaction and Boarding APIs. At White-Label, the platform sits inside the merchant UX, and the margin share steps up to compensate for the engineering and brand risk. At PayFac-as-a-Service, the platform captures the largest share and takes on compliance, risk-monitoring, and sub-merchant-lifecycle work.

Xplor Pay does not publish the specific basis points at each tier. In a live negotiation the numbers land against your volume commitment, your vertical, and the competing term sheets you bring. Treat the chart as the slope, not the absolute values.

The cost lever easy to miss is developer time. Xplor Pay’s post-rebrand toolkit (Low-Code Components, the Developer Center, the Full Integration Environment with production parity) compresses the engineering timeline on Embedded and White-Label integrations by weeks. For an ISV billing engineers at loaded cost, saved build time is a real line item against the rev-share math.

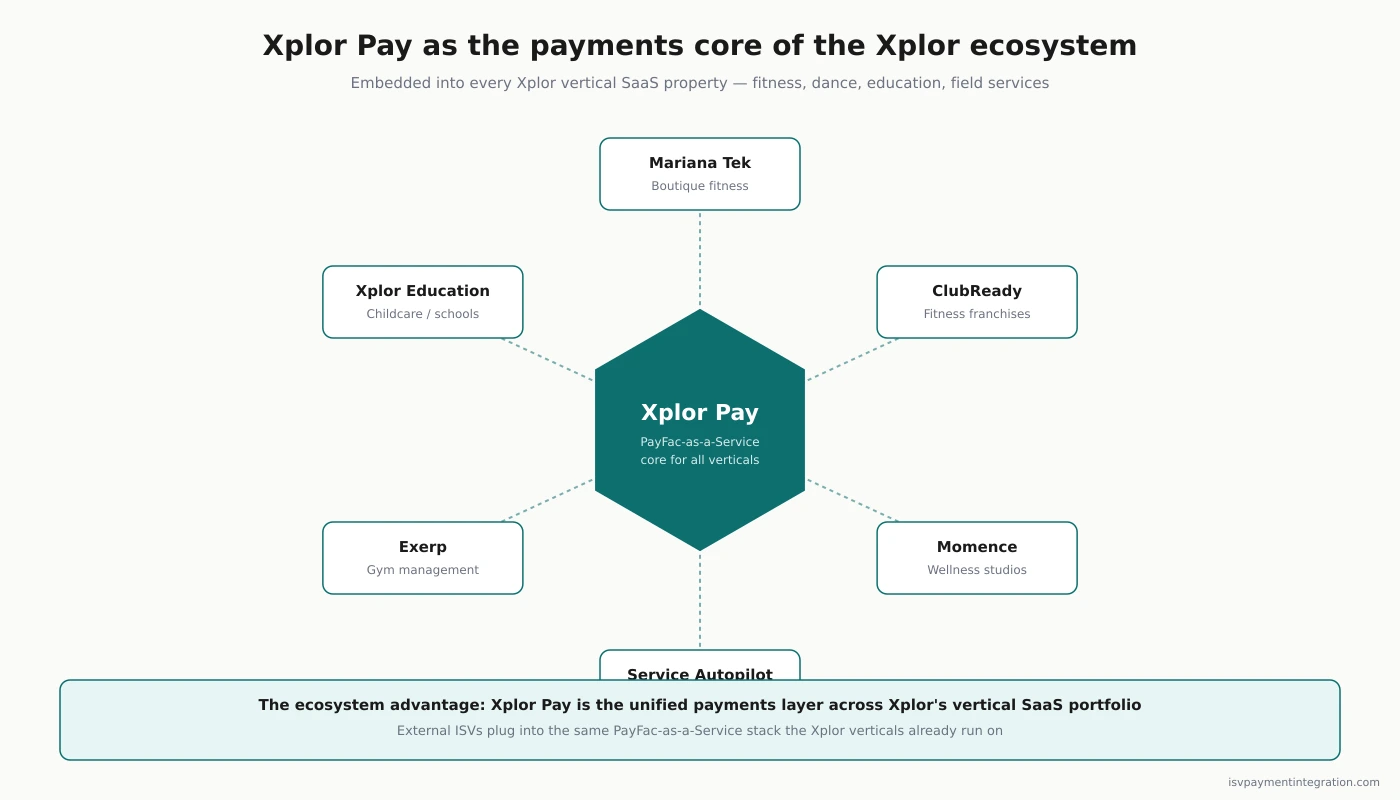

Xplor Pay Inside the Xplor Technologies Ecosystem

What separates Xplor Pay from a standalone processor is the ecosystem the rail connects to. Xplor Technologies owns a portfolio of vertical SaaS brands that already run on the same payments backbone: Mariana Tek in boutique fitness, ClubReady across the gym and studio space, Service Autopilot for field services, Exerp on the enterprise fitness side, and Momence for class-based businesses. Xplor Pay is the US payments layer underneath all of them.

Three things follow from that ownership structure.

Merchant density on the rail is pre-built. An ISV joining Xplor Pay joins the same backbone that supports tens of thousands of SMB merchants across those brands, which matters for risk-model tuning, sponsor-bank relationships, and underwriting speed on lookalike merchants.

The Parafin-powered embedded-finance layer plugs into the same rail. ISVs can layer working-capital offers on top of processing and pick up a secondary revenue stream outside the card rev-share. That stream changes partnership economics in a direction most rate-card comparisons miss.

The developer toolkit is built for the companies inside the family. The Transaction API, Boarding API, Reporting API, Recurring Payments API, Dispute Management API, and Marketing API are the same primitives powering the owned vertical brands, which is why documentation and sandbox parity look more like a platform SDK than a processor integration guide.

Pre-rebrand, Clearent sold a processing service. Post-rebrand, Xplor Pay sells access to a platform rail that carries vertical SaaS workloads by default.

How Xplor Pay Prices Versus Peers

Against Stripe Connect, Xplor Pay trades published pricing transparency for vertical SaaS depth and a PayFac-as-a-Service path. Stripe Connect’s flat 2.9% plus 30¢ and per-active-account fees on Express and Custom are the clearest numbers in the segment, but Stripe’s model is margin-capture by the platform on top of Stripe’s processing cost. Xplor Pay’s interchange-plus posture, negotiated per tier, can land at a lower blended cost for the right volume profile.

Against Finix, the story is closer. Both are interchange-plus, both skip the public rate card, and both pitch PayFac-as-a-Service. Finix leans harder on pure PayFac infrastructure for platforms that want to own the stack. Xplor Pay leans on the four-tier choice architecture and the pre-existing vertical SaaS ecosystem.

Against Adyen for Platforms and Worldpay for Platforms, Xplor Pay sits in the ISV-friendly middle. Adyen is the most transparent on method-level interchange++ pricing but is oriented to large-enterprise platforms. Worldpay for Platforms (the former Payrix, now inside Global Payments after the 2025 merger) sells configurable fees but carries a heavier sales-gated posture. Global Payments ISV pricing sits on the acquirer-scale end, with Infrastructure Fees and annual account charges that do not appear on Xplor Pay’s collateral.

For a head-to-head, see Xplor Pay vs Stripe Connect or Xplor Pay vs Finix.

Frequently Asked Questions

Does Xplor Pay publish a rate card?

No. Xplor Pay publishes an interchange plan that itemizes interchange, processing markup, authorization fees, and monthly platform charges on each merchant statement, but the specific basis points and rev-share splits are negotiated per partnership. Only Stripe and Adyen publish reference numbers in this category.

Is Xplor Pay pricing the same as Clearent pricing?

The legal entity is still Clearent, LLC operating as Xplor Pay, and existing Clearent merchant accounts carry forward under the same contracts. The July 8, 2025 rebrand did not reset pricing for in-flight deals. New ISV partnerships signed under the Xplor Pay brand use the four-tier framework. For legacy-contract exposure, read the Clearent pricing page.

What revenue share can an ISV expect from Xplor Pay?

Xplor Pay does not publish rev-share percentages. They are volume-tiered and negotiated per partnership, and the tier you pick changes the baseline. Referral gives the smallest share for the smallest operational lift. PayFac-as-a-Service gives the largest share and the largest compliance and risk workload. Embedded and White-Label sit in between.

Are there setup fees for ISV partners?

The public ISV collateral on xplorpay.com does not name a setup fee. Engineering scope is the real upfront cost, and it varies by tier. A Referral integration lands in weeks. PayFac-as-a-Service is a multi-quarter build even with the low-code components.

Does Xplor Pay cover cross-border and alternative payment methods?

ACH is supported through the ACH Provider API and prices outside the card rev-share. Cross-border and FX pricing are not disclosed publicly. Xplor Technologies cites 72-plus countries and $47B-plus processed annually across the group, but the US payments rail negotiates cross-border scope case by case.

The Bottom Line on Xplor Pay Pricing

Xplor Pay pricing in 2026 is a partnership-tier conversation. The four-tier choice (Referral, Embedded, White-Label, PayFac-as-a-Service) is the primary cost lever. The unified Xplor Technologies rail is the ecosystem advantage. The developer toolkit is a total-cost-of-ownership line item most peer comparisons skip. The trade-off is the one every platform-focused payments company asks you to accept right now: no public rate card, every deal negotiated, and competing quotes doing the work your spreadsheet cannot.

For verdicts and vertical-fit analysis, read the Xplor Pay review. For legacy-brand context, the Clearent pricing breakdown covers the TSYS-era contract lineage that carries forward for in-flight Clearent merchant accounts.