Clearent Pricing

Pricing model: Interchange-plus with negotiated ISV revenue share (legacy, pre-2025 rebrand). Based on publicly available information from Clearent's official site. Contact Clearent directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | Interchange-plus; markup never published, quoted per merchant by independent agents |

| Markup | Negotiated per ISV portfolio; revenue share tiers undisclosed publicly |

| Setup | Commonly $0 setup at signing; some contracts added onboarding fees |

| Monthly | Per-merchant monthly fees varied; no published ISV platform fee |

Hidden Costs to Watch

- ⚠ $395 early termination fee per merchant location on the standard 3-year contract

- ⚠ $24.99 monthly PCI non-compliance fee on accounts that failed validation

- ⚠ $29.95 annual fee in year one, increasing to $59.95 in year two and beyond

- ⚠ 3-year TSYS contract with automatic renewal and no prior notice

- ⚠ Independent-agent quote variance: two merchants on the same tier often paid different markups

- ⚠ Gateway and virtual terminal fees charged by third-party integrations, not Clearent directly

Alternatives

Clearent pricing at a glance (legacy contract era)

Clearent pricing for ISVs was an interchange-plus arrangement layered with a negotiated revenue share, wrapped inside a 3-year TSYS contract with an auto-renewal clause and a $395 per-location early termination fee. Clearent never published a rate card, so the real cost of any Clearent agreement depended on which independent sales agent wrote the deal and how hard the partner negotiated the markup.

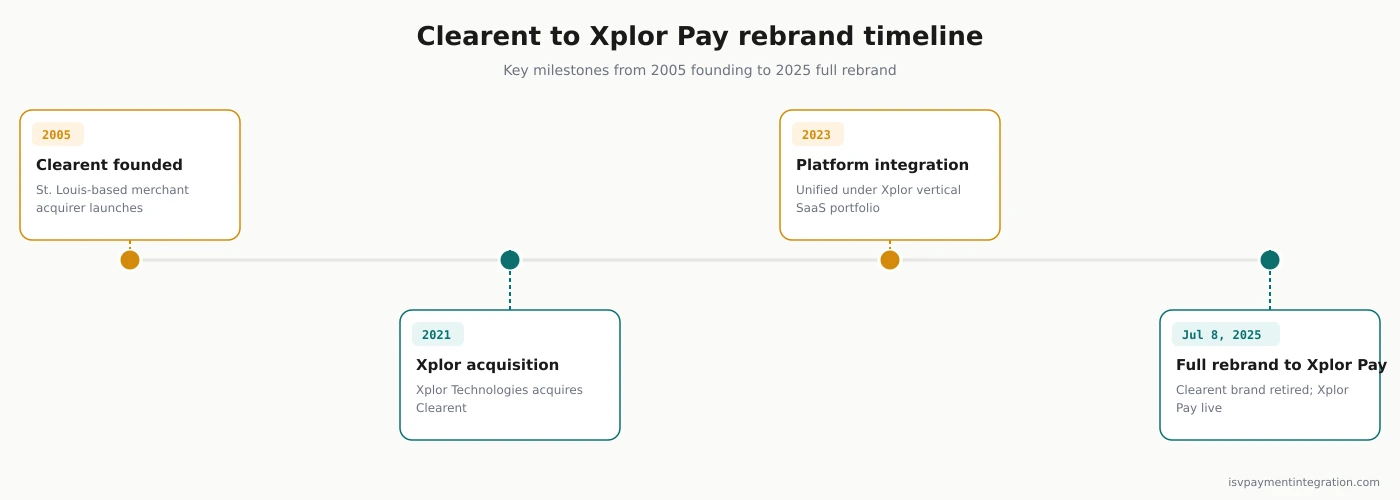

This page is the historical record. Clearent rebranded to Xplor Pay on July 8, 2025, and clearent.com/pricing now 404s. If you signed a Clearent agreement before the rebrand, the fees here are what you agreed to, and no public evidence says the schedule changed at the rebrand boundary. If you are evaluating payments for a new ISV integration today, the Xplor Pay pricing breakdown is the page you want.

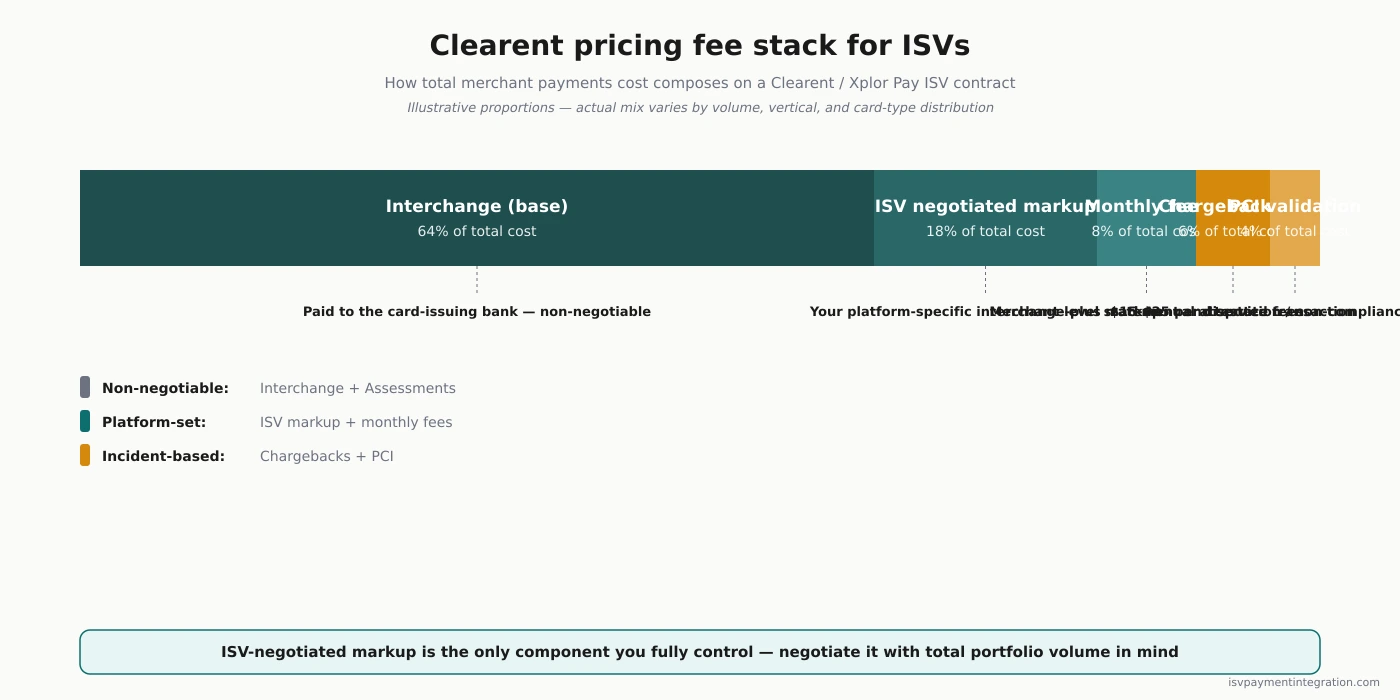

The Clearent pricing model: interchange-plus with ISV revenue share

Interchange-plus means you pay the card-network interchange rate (set by Visa, Mastercard, Discover, and Amex and published quarterly) plus a processor markup. On a Clearent statement, interchange passed through at cost, and Merchant Cost Consulting’s audits found no hidden padding on assessment fees. The markup was the number you negotiated, and it never appeared on a rate card.

For context, Helcim openly publishes interchange-plus tiers at 0.40% plus 8¢ on the first $50K monthly volume, scaling down from there. Clearent never told you what you were paying in that format. You learned your rate by reading your own statement line by line.

Revenue-share economics for ISV partners

ISV partners sat on top of the merchant-facing rate and negotiated a residual split on net processing revenue. Industry benchmarks for ISV revenue share at Clearent’s scale typically ran 20 to 60 percent of net processing revenue, tiered by portfolio volume. Clearent never published its own splits. Any specific figure you see quoted should be treated as a benchmark, not a Clearent number.

Why Clearent never published a rate card

The independent-agent sales channel meant pricing discretion belonged to the rep closing the deal, not to a corporate pricing team. The legacy merchant-services playbook rewarded opacity: two merchants on similar volume could pay different markups, and the processor captured the spread. Modern ISV platforms like Stripe, Adyen, and Helcim moved away from that model. Clearent held onto it until the rebrand.

Published and documented fees on a Clearent account

The fees below appeared on documented Clearent contracts and merchant statements, sourced from CardPaymentOptions’ 2026 Clearent review and cross-referenced against BBB complaint text and our own Clearent review.

| Fee | Amount | Applied |

|---|---|---|

| Early termination fee | $395 per location | On cancellation before the 3-year term ended |

| PCI non-compliance fee | $24.99 per month | On accounts that failed PCI validation |

| Annual fee (year 1) | $29.95 | Charged once in the first year |

| Annual fee (year 2+) | $59.95 | Charged annually from year two onward |

| Contract length | 3 years | Auto-renewal without prior written notice |

| ”Regulatory” fee | Reported at $49.95 | Flagged by reps as waivable; not a standard contract line item |

| Alternate ETF figure | Reported at $295 | Tied to cancellations inside a 30-day window |

| Chargeback fee | Not publicly documented | Industry range: $15 to $25 per dispute |

| ACH / virtual terminal | Not publicly documented | Third-party gateway pricing applied on integrated accounts |

The first four rows are high-confidence numbers that appeared consistently across contract language and complaint records. The next two rows are reported figures with less consistent documentation, sourced from representative conversations rather than contract language. The last two rows were never published.

The $29.95 annual fee that became $59.95

The annual fee structure was the most-cited surprise in BBB complaints. Year one billed at $29.95, low enough to feel like a formality. Starting year two, the same fee jumped to $59.95 for the life of the agreement and through any auto-renewal. A merchant who filed the contract away at signing would not notice the doubling until it hit the statement 13 months later.

The $24.99 PCI non-compliance fee

PCI DSS compliance validation is required of every merchant that stores, processes, or transmits cardholder data. Clearent charged $24.99 per month on any account that failed to complete validation. That is $299.88 per year, per merchant. For an ISV with a sub-merchant portfolio, a platform that let validation lapse across even 10 percent of its merchants was leaking thousands a month in fees that had nothing to do with processing.

The $49.95 “regulatory” fee reps would waive

CardPaymentOptions flagged this one as an outlier. The fee appeared on some contracts as a “regulatory” or compliance surcharge but was not tied to any actual regulatory requirement, and reps reportedly waived it on request. The lesson is that the fee appeared on some agreements and not others, the exact variance pattern an ISV negotiating with an independent sales channel needed to audit for before signing.

Worked cost example: what a mid-volume ISV merchant paid

Take a sub-merchant processing $50,000 per month at an average ticket of $85. Assume a negotiated markup of 0.50% plus $0.10 per transaction, the midpoint of Merchant Cost Consulting’s audited range.

- Monthly transaction count: roughly 588

- Interchange cost (blended estimate at 1.80%): $900

- Clearent markup (0.50% + $0.10): $250 + $58.80 = $308.80

- Annual fee amortized (year 2+ at $59.95): $5 per month

Effective all-in processing cost: roughly $1,213.80 per month, or 2.43% of volume. That is before chargeback fees or third-party gateway charges. A non-PCI-compliant merchant adds $24.99 per month, pushing the effective rate to 2.48%. A merchant leaving in month 20 of a 36-month contract owes $395 on top of whatever processing revenue they were no longer generating.

None of those numbers appeared anywhere on Clearent’s public site. They came from the contract, the statement, and a negotiation with the agent who wrote the deal.

Contract terms that carried over to Xplor Pay

The contract paper is the part of Clearent pricing that matters most right now. It transferred intact to Xplor Pay.

3-year TSYS contract with auto-renewal

Clearent’s standard merchant agreement ran three years on TSYS rails, the same backend Xplor Pay uses today. The auto-renewal clause extended the term for another year unless the merchant provided written cancellation notice inside a narrow window before the renewal date. The window was not advertised. One six-year Clearent customer reported in a BBB complaint that they were told they had auto-renewed for another year and would owe $395 to close.

For ISVs, an account with 200 sub-merchants on staggered start dates has 200 renewal windows to track. Missing one means the merchant is locked in for another year with the same ETF exposure.

$395 per-location ETF, and the $295 wrinkle

The $395 figure is documented in the standard contract and repeats across independent complaint sources. The $295 figure surfaced in CardPaymentOptions’ review as a rep statement tied to cancellations inside a 30-day notice window. Treat that as a data point worth verifying against your specific contract, not as a guaranteed alternate figure.

Aggregated at ISV scale, $395 per location is where the real cost lives. A platform running 500 sub-merchants that decides to migrate off Xplor Pay inherits a theoretical $197,500 in ETF liability. The mitigations are negotiating the ETF down at signing (possible for ISVs bringing real volume) or running a phased migration that lets merchants age out of their terms.

What changed at the Xplor Pay rebrand

The Clearent-to-Xplor Pay rebrand on July 8, 2025 was primarily a marketing exercise. From a pricing standpoint, the rebrand did not retire the legacy fee schedule, change the TSYS backend, or void existing merchant contracts. Same rails, same paper, same fees.

One pattern is worth tracking. At least one Capterra reviewer explicitly stated that costs increased on their account at the rebrand boundary, with features and costs added without being requested. The complaint volume is low in absolute terms, but the signal suggests the rebrand coincided with account-level repricing for some segments. If you have a legacy Clearent contract, pulling a fresh statement from August 2025 onward and comparing it against a pre-rebrand statement is the only way to know what changed on your account.

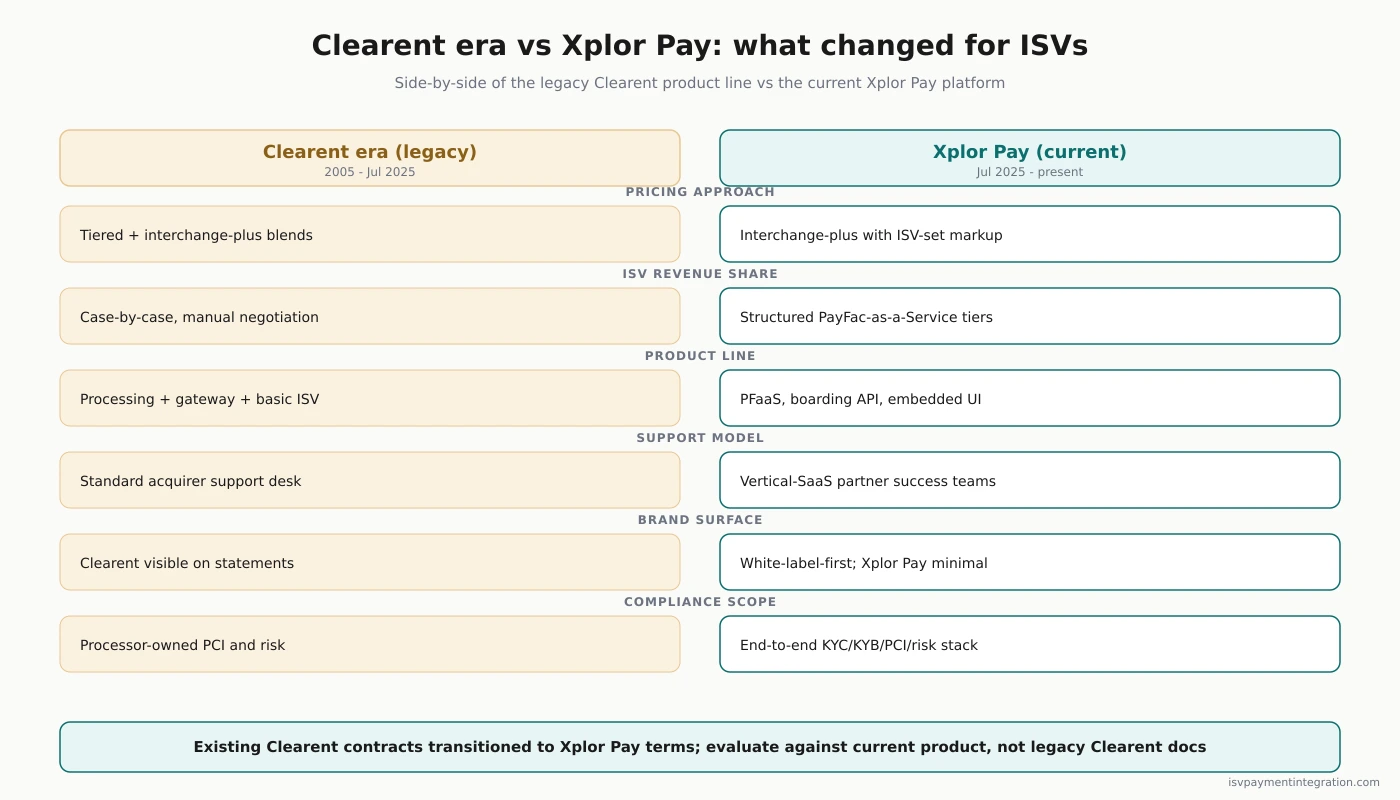

What did not change: the 3-year contract structure, the $395 per-location ETF, the auto-renewal mechanics, the interchange-plus model, the ISV-controlled markup, the TSYS backend, the five-day SFTP token migration, and the Empower surcharging program. If the original Clearent contract and the current Xplor Pay terms feel familiar, the paper was reused.

How Clearent priced against its peers

Against Helcim, the industry-transparency benchmark, Clearent’s quote-only model was structurally weaker. Helcim publishes its interchange-plus tiers down to the basis point and runs month-to-month with no contract. Clearent buried the same information inside a 3-year contract with a $395 ETF.

Against Stripe Connect and Finix, the modern ISV-first platforms, Clearent traded developer tooling and self-serve onboarding for relationship-managed vertical expertise. That trade still applies to Xplor Pay today. See Xplor Pay vs Finix for the comparison as it stands post-rebrand, and the Clearent review for verdicts on the non-pricing dimensions.

Frequently asked questions about Clearent pricing

Did Clearent ever publish a rate card?

No. Clearent ran on a quote-only model through its independent-agent sales channel. The interchange-plus markup, ISV revenue share tiers, and volume discounts were negotiated per merchant or per partner. That lack of transparency is one reason merchants frequently audited their own statements for padding after signing.

What is the Clearent early termination fee?

$395 per merchant location on the standard 3-year contract. Reports also surfaced of a $295 figure tied to cancellations inside a 30-day notice window, but the $395 number is the one documented in CardPaymentOptions’ review and recurring across BBB complaints. For an ISV running 200 sub-merchants, that is $79,000 of latent exit-cost exposure.

Does my Clearent contract still apply after the Xplor Pay rebrand?

Almost certainly yes. No public evidence indicates the fee schedule or contract terms changed materially at the July 2025 rebrand. Existing merchants moved to Xplor Pay with the same TSYS rails, ETF, and auto-renewal language. Confirm your specific terms with Xplor Pay before assuming continuity.

Did Clearent offer flat-rate pricing?

No. Interchange-plus was the only standard pricing model. Clearent’s Empower program offered a surcharge overlay that shifted processing cost to the cardholder, but that was a surcharging product, not flat-rate.

How did Clearent’s revenue share for ISVs work?

Negotiated privately per partner. Industry benchmarks for ISV revenue share at Clearent’s tier typically ran 20 to 60 percent of net processing revenue, scaled by portfolio volume. Clearent never published its own splits. Any specific basis-point figure quoted outside a signed agreement should be treated as a benchmark.

What a legacy Clearent contract tells you to demand today

The Clearent pricing lessons port to any interchange-plus processor you evaluate next, including Xplor Pay. Get the markup in writing before signing. Cap or waive the annual fee in the contract, not in a sales email. Prorate, negotiate down, or remove the ETF for ISV portfolios above a volume threshold you specify. Get a full list of every recurring per-merchant fee with amounts attached.

Clearent pricing was what it was because the ISV channel accepted opacity as a cost of doing business. Finix, Stripe Connect, and a properly-negotiated Xplor Pay agreement do not require that trade. For verdicts and use-case fit, the Clearent review covers the non-pricing angles. For current-brand pricing, head to the Xplor Pay pricing page.