Clearent Review

Vertical SaaS payment infrastructure with named ISV partners in dental, medical aesthetics, and home services — now rebranded as Xplor Pay.

Overview

Clearent rebranded to Xplor Pay on July 8, 2025 and now positions as a vertical SaaS payment infrastructure company. The platform processes $37 billion annually across 106,000 merchants under the Xplor Technologies parent, with named ISV partners including Dental Intelligence, Aesthetic Record, and FieldEdge. For software companies, it competes on pre-tuned vertical underwriting, interchange-plus economics with ISV-controlled markup, and a five-day SFTP token migration path from incumbent processors.

For the latest on Clearent's ISV capabilities, documentation, and partner programs, visit xplorpay.com.

Pricing

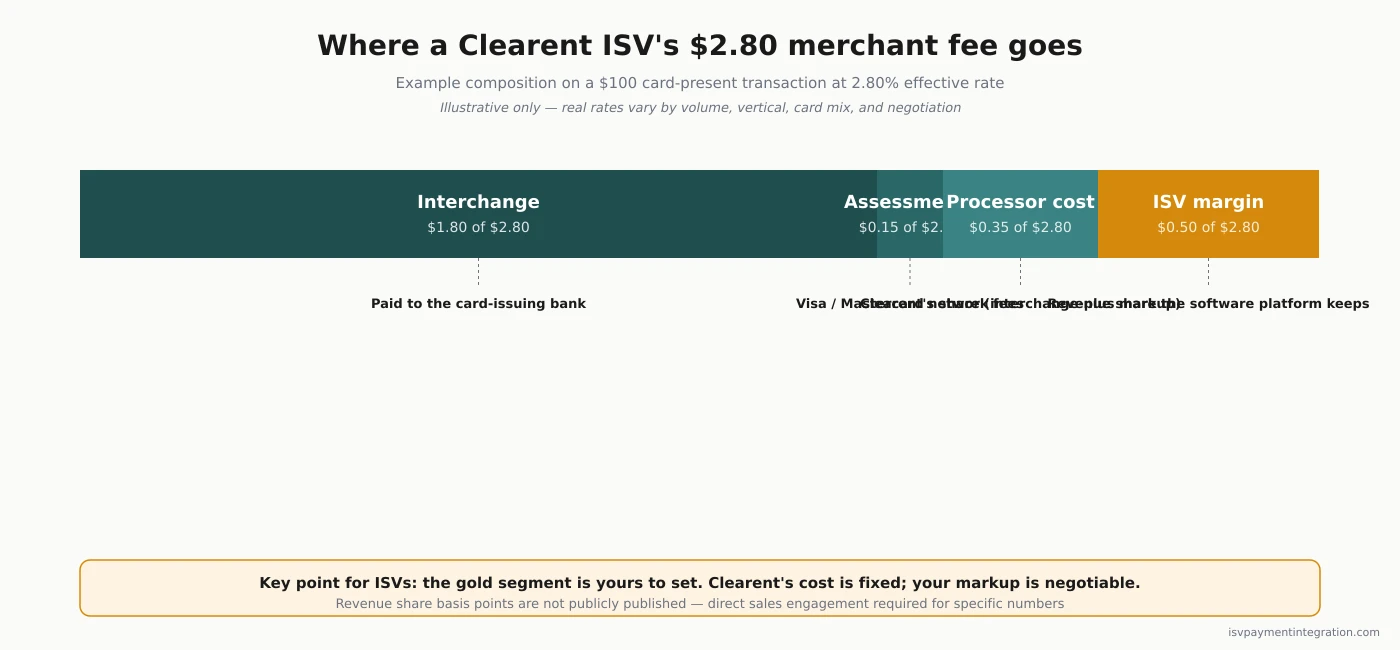

Interchange-plus with ISV-controlled merchant markup

True interchange-plus model where the ISV sets the merchant-facing rate. Typical markups audited around 0.50% + $0.10, with negotiated clients observed as low as 0.20% + $0.10. Revenue share not publicly disclosed; requires sales engagement. Standard contract: 3-year auto-renewing with $395 per-location early termination fee.

Full pricing breakdown →Pros

- ✓ Pre-tuned underwriting for vertical SaaS — dental, medical aesthetics, fitness, home services, field services, pet care

- ✓ True interchange-plus with ISV-controlled merchant markup — real margin flexibility

- ✓ Automatic Level 2/3 data capture — meaningful rate reduction for B2B-heavy verticals

- ✓ PayFac-as-a-Service layer for turnkey embedded payments without own PayFac registration

- ✓ Five-day SFTP + PGP vault-to-vault token migration reduces switching cost

- ✓ Named-executive ISV testimonials (Dental Intelligence) instead of anonymous case studies

Cons

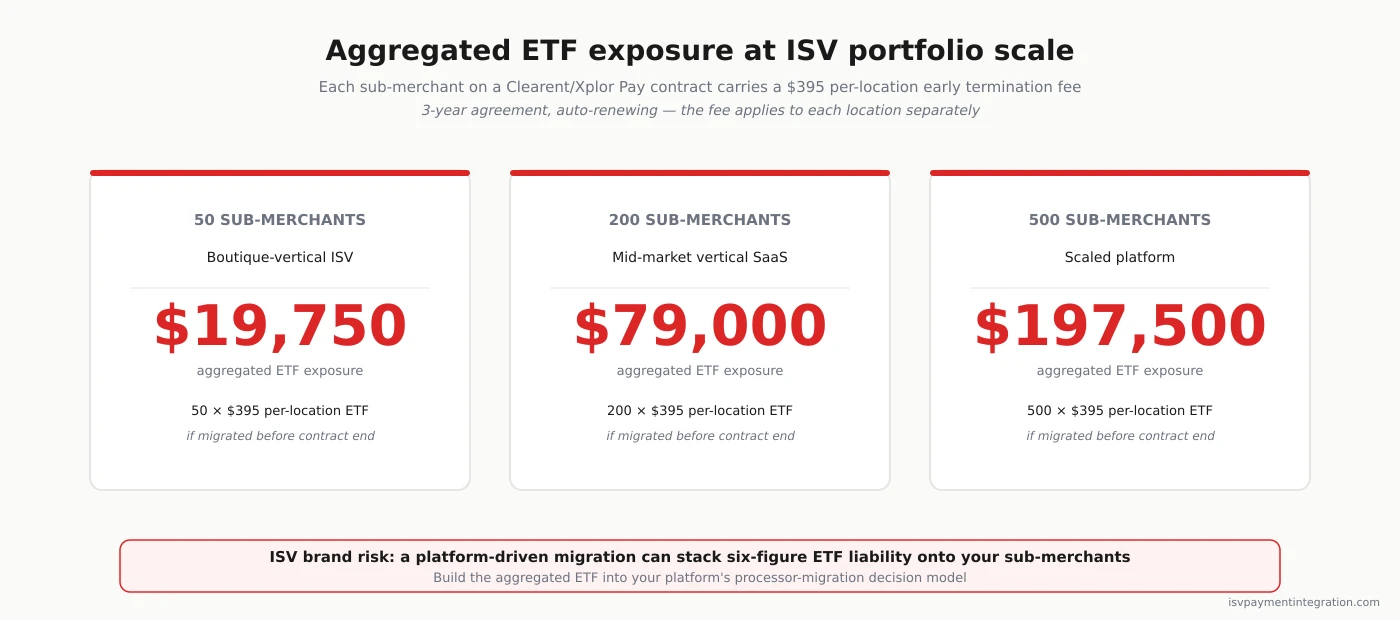

- ✗ $395 per-location ETF on 3-year auto-renewing contracts creates large aggregated exit-cost exposure at ISV-portfolio scale

- ✗ Revenue share terms not publicly disclosed — real economics require sales engagement

- ✗ Billing-after-cancellation pattern documented across BBB, Slashdot, and independent complaint sources

- ✗ Post-rebrand account-level pricing changes reported on Capterra — existing accounts bear watching

- ✗ No independent benchmark of sub-merchant onboarding SLAs — vendor claims only

- ✗ Narrower geographic footprint than Stripe or Adyen — U.S., Australia, Europe only

ISV Fit

Strong fit for mid-market vertical SaaS platforms in dental, medical aesthetics, fitness, home services, field services, or pet care — verticals with pre-tuned underwriting and named reference partners. Weaker fit for early-stage ISVs prioritizing self-serve speed, platforms with churn-sensitive sub-merchant bases, or ISVs requiring published revenue share economics before commercial engagement.

Clearent Review: An ISV’s Perspective (2026)

Most Clearent reviews evaluate the platform through the lens of a small retailer swiping a credit card. This one doesn’t. This review looks at Clearent — now operating as Xplor Pay — through the lens that actually matters for software companies: embedding payments, onboarding sub-merchants, earning revenue share, and keeping your platform independent.

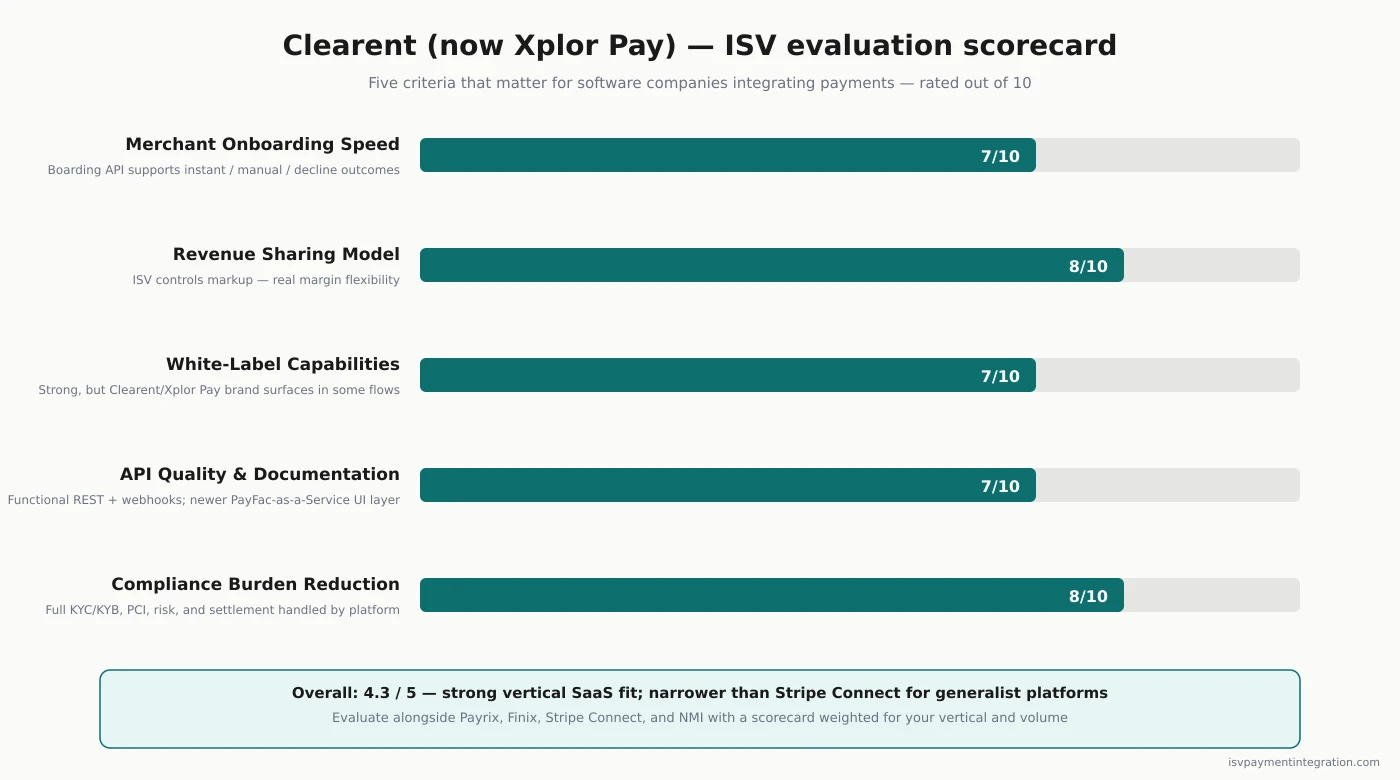

Clearent scores 4.3/5 in our ISV-focused evaluation. That rating weighs embedded-payment capability far more than the generic “is this a good processor for my coffee shop?” signal you’ll get on Trustpilot or Capterra. Software companies and small merchants are buying fundamentally different products from the same vendor.

Clearent Rebranded to Xplor Pay on July 8, 2025: What Changed (and What Didn’t)

On July 8, 2025, Clearent dropped the “by Xplor” suffix and rebranded to Xplor Pay. The legacy brand first merged with Transaction Services Group in 2021 to form Xplor Technologies; the 2025 rebrand was the final step in unifying the U.S. payments division under a single name.

What’s the same: the TSYS backend, existing merchant accounts, the 3-year contract structure, the $395 per-location early termination fee, the interchange-plus pricing model, and the developer tooling roadmap. If you were a Clearent ISV partner on July 7, you were an Xplor Pay ISV partner on July 9 with identical terms.

What changed: the marketing positioning shifted from “integrated payments processor with an ISV program” to “vertical SaaS payment infrastructure company.” Nick Campbell, Xplor Pay’s CPO, put it this way in the rebrand press release: “We’re making it quicker and easier for SaaS platforms to build payments the way they want to.” The positioning change matters because it signals where the roadmap investment is going — not where it currently is.

One consequence ISVs should monitor: at least one merchant on Capterra documented unexpected cost increases immediately post-rebrand. The rebrand appears to have coincided with account-level pricing restructuring for some segments. For full context on the current product, see our Xplor Pay review and the rebrand press release.

Clearent as an ISV Partner: The Real Product

Clearent/Xplor Pay processes $37 billion annually across 106,000 merchants under the Xplor Technologies parent — a scale that puts it in the mid-tier of U.S. processors. A meaningful portion of that volume flows through embedded-payments partnerships with vertical SaaS platforms, not direct merchant relationships.

Vertical SaaS partners and target verticals

Public case studies confirm the platform is built for software companies in specific verticals, not generic merchant aggregation. Named partners include Dental Intelligence (dental practice management), Aesthetic Record (medical aesthetics and medspa), SPOT Business Systems (dry cleaning and textile), and FieldEdge (HVAC and home services). Tyler Barefoot, CEO of Dental Intelligence, said the Clearent integration “dramatically reduced our development time” and enabled “a seamless, branded payments experience.”

The common thread across these verticals: recurring billing, high-frequency small-ticket transactions, and heavy compliance overhead (medical, legal, regulated) that benefits from a processor that has seen the vertical before. If your platform serves one of these verticals — especially dental, medical aesthetics, fitness and wellness, home services, or field services — Clearent has pre-built underwriting rules and risk models tuned to your merchants.

Automated sub-merchant onboarding

Clearent’s Boarding API supports three underwriting outcomes per sub-merchant: instant approval, manual review, or decline. The underwriting model uses machine-learning risk scoring to route low-risk applications straight through. Xplor Pay claims this reduces boarding from “days to hours or minutes” — though no independent merchant or ISV has published benchmark SLAs, so treat those numbers as vendor-stated rather than verified.

For ISVs, what matters is the API contract itself: a documented REST endpoint for submitting merchant applications, webhook callbacks for status changes, and the ability to present boarding as your platform’s branded flow rather than a redirect to Clearent. This capability sits underneath the company’s newer PayFac-as-a-Service product, which layers low-code UI components on top for ISVs that don’t want to build their own onboarding UI.

Token migration from incumbent processors

If you’re already an ISV running on a different processor and evaluating a switch, the friction isn’t code — it’s moving your sub-merchants’ stored card tokens without breaking their recurring billing. Clearent supports vault-to-vault token migration via secure SFTP with PGP-encrypted payloads and commits to completing the import within five business days. That’s an under-discussed capability but a real switching-cost eraser for platforms with large stored-card portfolios.

Revenue Share & Economics for ISVs

The core question for any ISV evaluating a payments partner: how much margin do I actually keep per transaction? Clearent’s structure answers this differently than Stripe Connect (fixed platform fee) or a direct PayFac registration (full interchange arbitrage).

The interchange-plus + ISV markup structure

Clearent operates on a true interchange-plus model where the ISV controls the markup charged to its sub-merchants. The ISV keeps the spread between the interchange-plus cost (set by the processor) and the merchant-facing rate. This gives software platforms real pricing flexibility — you can compete on rate in commodity verticals or extract margin in verticals where your software’s value dominates the buying decision.

Merchant Cost Consulting’s audit of Clearent contracts found interchange-plus markups typically around 0.50% plus $0.10 per transaction, with one verified client quoted as low as 0.20% + $0.10. Negotiation is real but non-public; rates depend on volume, vertical, and relationship.

Why revenue share figures aren’t public

No ISV partner has publicly disclosed specific revenue share basis points or percentage splits. Xplor Pay’s marketing cites aggregate outcomes — “the average merchant saves $9,500 a year,” “a healthcare SaaS partner saved $84,000 annually,” “a dental SaaS partner grew per-location volume from $18,000 to $390,000+” — all of which are company-authored statistics rather than independent benchmarks. If you’re building a business case around specific revenue share economics, you’ll need a direct sales engagement to get real numbers tied to your projected volume.

Level 2/Level 3 data optimization for B2B

One economics detail that disproportionately matters for ISVs serving B2B verticals: Clearent’s platform automatically captures and submits Level 2 and Level 3 interchange data on qualifying transactions. For SaaS platforms serving professional services, government contracting, construction, or wholesale distribution — where corporate and procurement cards dominate — L2/L3 optimization can shave 50-100 basis points off effective rates. Not every processor handles this natively. It’s a quiet edge for the right ISV vertical.

Merchant Pain Points ISVs Must Understand

Here’s the honest part of this review. When you integrate Clearent as your platform’s payments partner, your sub-merchants inherit Clearent’s contract structure and customer service. Every complaint filed against Clearent by an SMB becomes, to some degree, a complaint against your software’s payment experience. ISVs have to underwrite this risk, not wave it away.

Contract structure and early termination

Clearent’s standard agreement runs three years, auto-renews without prior notice, and charges a $395 early termination fee per merchant location. For a single small business, that’s an annoyance. For an ISV running 200 sub-merchants on Clearent, that’s $79,000 of latent exit-cost exposure sitting on your portfolio. Multiple BBB and Capterra complaints describe the auto-renewal as the primary source of merchant frustration — one six-year customer reported being told they had auto-renewed for another year and would owe $395 to close. If your platform’s brand absorbs that interaction, you need to know.

Rate creep and post-rebrand price changes

On April 1, 2022, Clearent issued a flat 0.09% rate increase across all Visa, Mastercard, American Express, and Discover settled volume. Merchants received it as a notification, not a negotiation. Rate increases of this type are standard across the industry, but the pattern ISVs should track is the cadence: Clearent has historically been described as a “rates rarely change” processor, and the 2022 increase broke that narrative for existing accounts.

Post-rebrand, a separate issue surfaced: a Capterra reviewer explicitly stated “Was good under Clearent, when it became Xplor Pay they increased costs, added features/costs not requested.” This suggests the 2025 rebrand coincided with pricing restructuring for at least some merchant segments. The Capterra complaint volume isn’t catastrophic in absolute terms — but the pattern matters, because an ISV learning about a sub-merchant rate change after the fact is an ISV spending a support quarter explaining it.

Cancellation friction — the billing-after-close pattern

Three separate third-party sources document the same underlying pattern: merchants who request cancellation continue to see charges posted to their bank accounts for months afterward. A BBB complaint shows a timeline from December 2023 through September 2024 of post-cancellation billing on an inactive account; a Slashdot reviewer reported charges continuing despite formal closure; West Coast Body and Paint published a case where a COVID-era account freeze was reversed without authorization and $817 of unauthorized fees accrued over seven months.

These aren’t high-volume complaints — with 106,000 merchants, 21 BBB complaints in the last 12 months is statistically low. But the pattern recurs across independent sources, and for ISVs deciding whether to push volume onto this platform, it’s worth building into your risk model. A merchant who cancels your software because of a post-close billing dispute is a churn event that belongs in your decision, not the processor’s.

What Merchants Actually Praise

Not every Clearent merchant is angry — the platform has genuine strengths that show up in reviews with enough specificity to believe.

Interchange-plus transparency when properly set up. Merchants on interchange-plus agreements consistently describe the rate visibility as the primary value. “Clearent is typically very ethical when it comes to rates and fees,” wrote Merchant Cost Consulting after auditing multiple client accounts for assessment padding and finding none. If you negotiate the right contract, the pricing stays honest.

Level 2/3 data optimization for B2B. For merchants in B2B-heavy verticals, the automatic L2/L3 data handling reduces effective rates on corporate card transactions — a concrete cost advantage that doesn’t require merchant action to capture.

CRM and POS integration praised in specific verticals. Erika Z., an automotive shop owner, cited the CCC auto-body software integration as the main reason for staying with Clearent. Jacki W., an operations director, described “great support when I have an issue to resolve” and seamless CRM integration. Jo Ann G., an administrator, praised the ability to reach a live representative quickly. These positive signals concentrate in day-to-day operational contexts — not in billing disputes or cancellations.

No setup fee on many agreements. Merchants commonly note $0 onboarding cost as a meaningful differentiator versus processors that charge $100-$300 upfront. This matters to ISVs too: it means your sub-merchants don’t face an activation barrier at signup.

How Clearent Compares to Other ISV-Focused Processors

Every ISV should evaluate at least three processors before committing, because the “best” processor depends on vertical, volume, and how much of the payments stack you want to own.

vs Payrix — PFaaS pioneer vs vertical SaaS incumbent

Payrix was one of the first PayFac-as-a-Service providers and is now owned by Worldpay. Clearent’s PayFac-as-a-Service is newer but sits inside a less-acquired parent. If you value PFaaS heritage and Worldpay’s global reach, Payrix has the edge. If you value vertical focus and a smaller parent with more room to prioritize ISVs, Clearent is stronger. See the Payrix vs Tilled analysis for the neighboring comparison.

vs Finix — relationship-managed vs developer-first

Finix optimizes for developer self-service and maximum independence from large processors. Clearent is relationship-managed with dedicated ISV solution engineering support. Early-stage ISVs often prefer Finix’s self-serve speed; mid-market ISVs in regulated verticals often prefer Clearent’s human partnership.

vs Stripe Connect — SaaS platform generalist vs vertical specialist

Stripe Connect remains the default for SaaS platforms that want the broadest geographic coverage, the best developer tooling, and the widest feature surface. Clearent wins when your vertical matters more than geography and you need tuned underwriting for specialized verticals. Reference NMI vs Stripe for how Stripe compares to a gateway-first alternative.

vs NMI — gateway-first vs full-stack PFaaS

NMI positions as a payment gateway with flexible acquirer relationships; Clearent is a full-stack PFaaS with embedded acquiring. If you want to maintain multiple acquirer relationships, NMI is more flexible. If you want single-vendor accountability, Clearent is cleaner.

Who Clearent Fits — and Who It Doesn’t

Strong fit

- Mid-market vertical SaaS platforms in dental, medical aesthetics, fitness, home services, field services, pet care, or property management — verticals with pre-tuned underwriting

- ISVs with $10M-$500M annual processing volume that want relationship-managed support over pure self-service

- Platforms serving B2B-heavy verticals that benefit from automatic Level 2/3 data optimization

- ISVs migrating from another processor that value the 5-day SFTP + PGP token migration

- ISVs that want a PayFac-as-a-Service layer without building their own PayFac registration

Weaker fit

- Early-stage ISVs prioritizing self-serve integration speed — consider Stripe Connect or Finix

- ISVs with churn-sensitive sub-merchant portfolios where the $395 ETF and billing-after-cancellation pattern create unacceptable brand risk

- Platforms requiring published revenue share economics before commercial engagement

- ISVs that need white-label embedded payments with zero processor brand visible to sub-merchants — the Clearent/Xplor Pay brand still appears in some merchant-facing interactions

- ISVs serving geographies outside the U.S., Australia, and Europe — the global footprint is narrower than Stripe or Adyen

Frequently Asked Questions

Is Clearent legit? Yes. Clearent processes $37 billion annually across 106,000 merchants under the Xplor Technologies parent, maintains an A+ Better Business Bureau rating, and has been in continuous operation since 2005. The A+ rating coexists with documented cancellation-friction complaints — both facts are true.

What does Clearent do? Clearent is a U.S. credit card processor with interchange-plus pricing and a specialized ISV/SaaS embedded-payments program. It operates as Xplor Pay as of July 8, 2025. For software companies, it competes as a PayFac-as-a-Service partner — handling merchant underwriting, risk, compliance, and settlement so ISVs can embed payments without registering as their own payment facilitator.

Is Clearent the same as Xplor Pay? Yes. Clearent rebranded to Xplor Pay on July 8, 2025. Same company, same TSYS backend, same contract structure, same existing merchant accounts. The change is brand and positioning, not infrastructure. Read the rebrand announcement for context.

What is Clearent’s early termination fee? $395 per merchant location on a standard 3-year agreement. The contract auto-renews without prior notice. For ISV partners, this fee applies to each sub-merchant separately — which means a 200-merchant portfolio carries $79,000 of aggregated ETF exposure if the platform chooses to migrate.

Is Clearent good for software companies and SaaS platforms? Depends on vertical. Clearent is strong for mid-market ISVs in dental, medical aesthetics, fitness, home services, field services, and pet care — verticals where the platform has pre-tuned underwriting and named reference customers. It’s weaker for early-stage ISVs that prioritize self-serve speed or platforms with geographically diverse sub-merchant bases outside the U.S.

The Bottom Line for ISVs

Clearent — now Xplor Pay — is a legitimately strong partner for ISVs that fit a narrow profile: mid-market, vertical SaaS, U.S.-centric, relationship-managed. The product does what it claims, the ISV case studies are named and real, and the interchange-plus economics are honest when negotiated properly.

The risks are contract structure and merchant experience, not product quality. If your platform absorbs the $395 ETF exposure and the occasional billing-after-cancellation incident without brand damage, Clearent is worth a serious evaluation. If your sub-merchant base is churn-sensitive or your brand can’t afford processor friction, evaluate Finix, Stripe Connect, or Payrix against Clearent before committing. For the current product positioning, read the Xplor Pay review; for pricing specifics, see the Clearent pricing breakdown.