Global Payments vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

These are the two largest bank-distributed merchant acquirers an American software company is likely to evaluate, and on a capability grid they look interchangeable. The grid hides the thing that actually diverged in January 2026: one of these companies sold off every business that was not merchant acquiring, and the other still earns nearly half its revenue somewhere else entirely. Where a parent company's attention goes, its partner channel's roadmap follows.

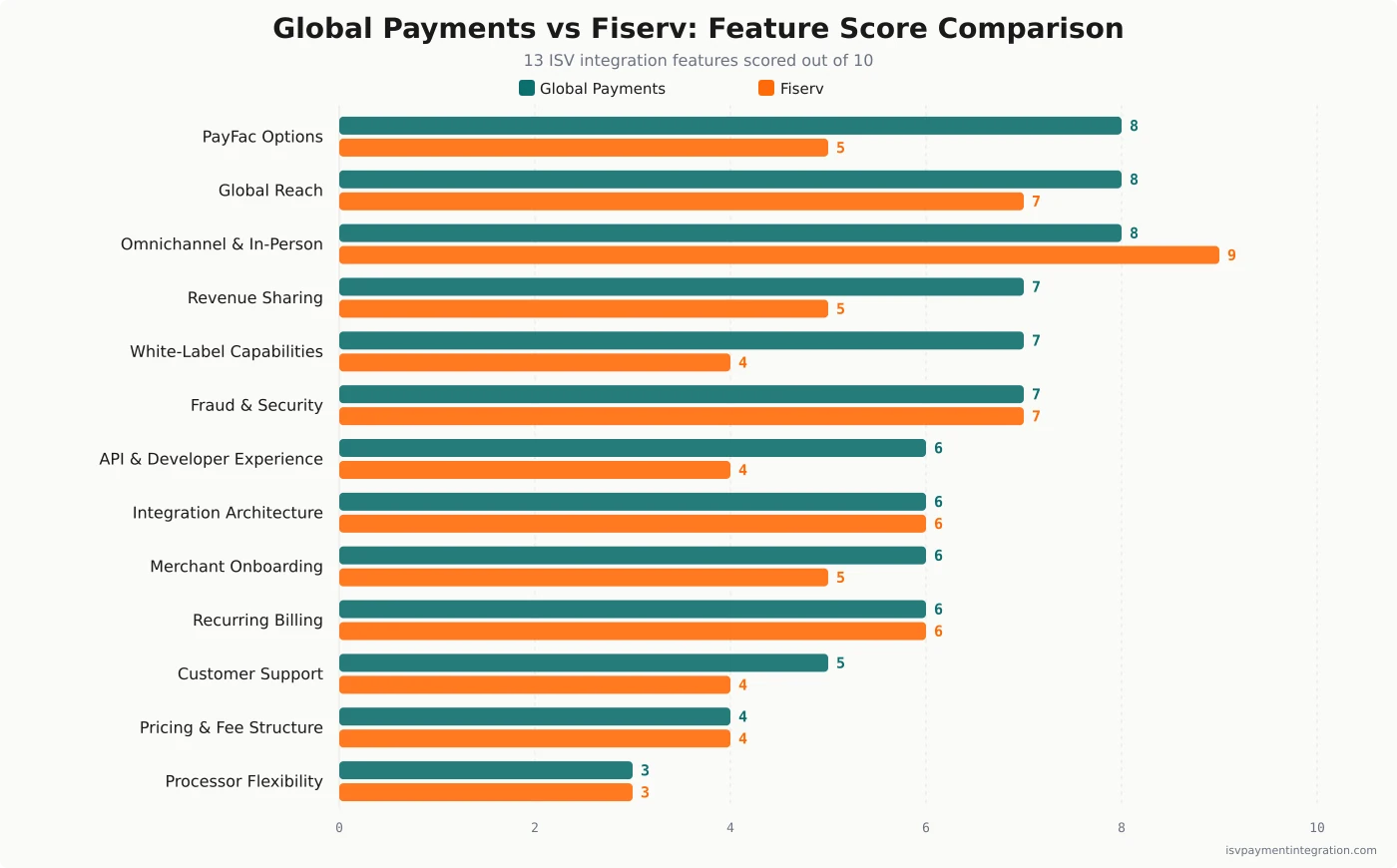

Feature Comparison

| Feature | Global Payments | Fiserv |

|---|---|---|

| PayFac Options | 8 | 5 |

| Global Reach | 8 | 7 |

| Omnichannel & In-Person Payments | 8 | 9 |

| Revenue Sharing | 7 | 5 |

| White-Label Capabilities | 7 | 4 |

| Fraud & Security | 7 | 7 |

| API & Developer Experience | 6 | 4 |

| Integration Architecture | 6 | 6 |

| Merchant Onboarding | 6 | 5 |

| Recurring Billing | 6 | 6 |

| Customer Support | 5 | 4 |

| Pricing & Fee Structure | 4 | 4 |

| Processor Flexibility | 3 | 3 |

Get this comparison as a shareable PDF

We'll send the Global Payments vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Global Payments

Best for vertical SaaS with a genuine roadmap to payment facilitation, and for platforms selling into merchants outside the United States where Worldpay's acquiring footprint earns its keep. Accept two ISV programs that have not been merged, and GAAP results distorted by acquisition accounting.

Best for

Fiserv

Best for restaurant and retail software whose merchants already run a terminal on a counter, and for platforms that would rather inherit seven sponsor banks' underwriting than build their own. Accept a parent that is contracting, and that lost its chief executive and its president inside four weeks.

Global Payments vs Fiserv: One Became a Pure-Play, One Did Not

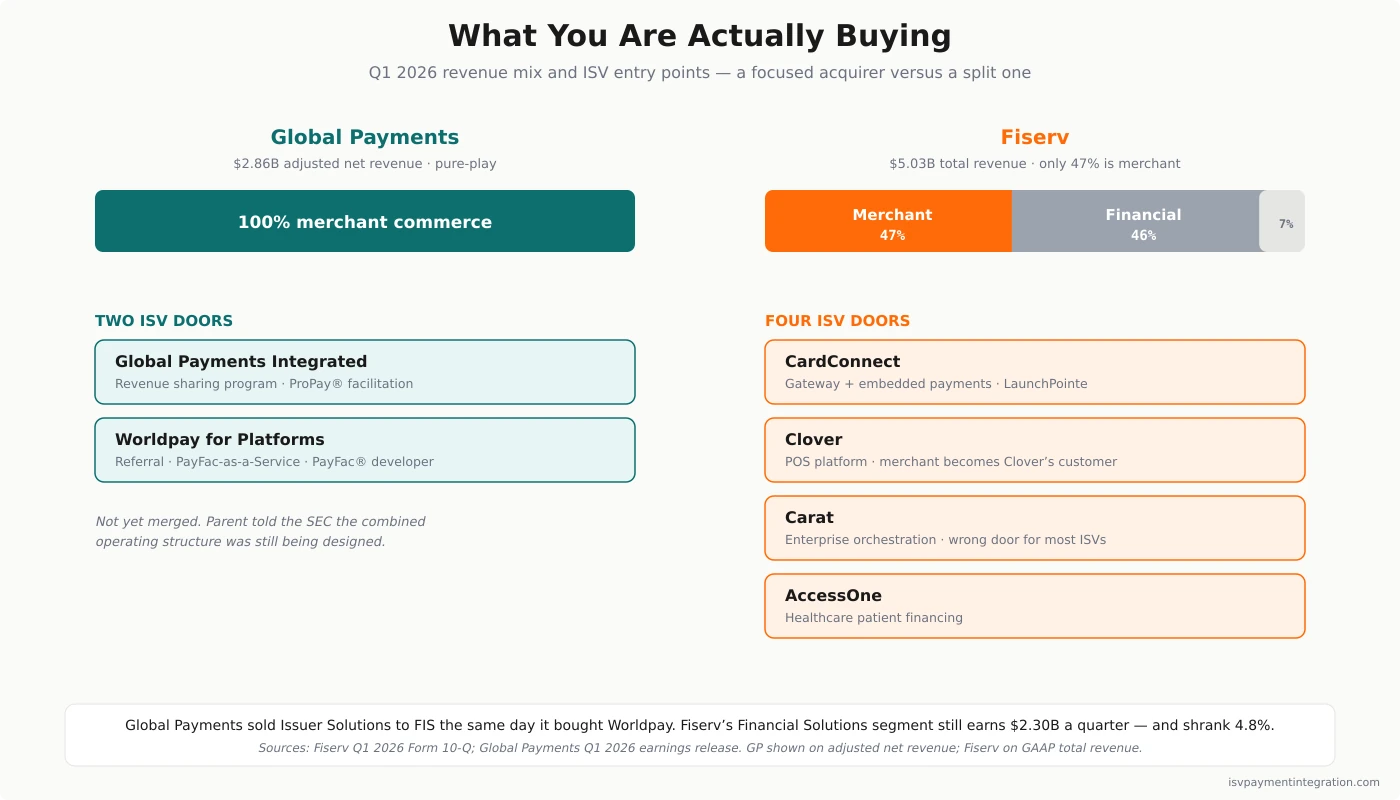

In January 2026, Global Payments did two things on the same day. It bought Worldpay for $24.25 billion, and it sold its Issuer Solutions business to FIS. Its chief executive described the result plainly when the quarter closed: “Global Payments as a focused, pure-play commerce solutions leader.”

Fiserv did not do that. It remains, as its own quarterly filings make clear, two roughly equal businesses under one roof: Merchant Solutions, and Financial Solutions — core banking, card issuing, and digital banking sold to financial institutions.

For a software company deciding where to embed payments, that structural difference is worth more than any feature grid. It determines whose roadmap you are on, whose capital allocation you compete for, and how much of your acquirer’s institutional attention your channel can realistically command.

The comparison one level down — the actual ISV products these two companies sell — belongs to Worldpay vs Fiserv, because Worldpay for Platforms is now Global Payments’ sharpest ISV weapon. This page is about the companies holding the pen.

Quick Take: A Focused Acquirer and a Split One

Global Payments is now what its balance sheet says it is. In the first quarter of 2026 — its first full quarter after the Worldpay close — it reported GAAP revenue of $2.97 billion and adjusted net revenue of $2.86 billion, with adjusted net revenue up roughly 5.5% on a normalized basis, adjusted operating margin expanding 110 basis points to 39.9%, and adjusted earnings per share up 10% to $2.96. It reaffirmed full-year guidance and announced a $500 million accelerated share repurchase. It is worth being honest about the other number: GAAP diluted earnings per share came in at a loss of $6.59, a consequence of acquisition accounting rather than of operations. Its ISV surface is two doors that have not yet been merged — Global Payments Integrated, whose own site now carries a banner reading “Global Payments Integrated is transitioning to the Global Payments brand,” and Worldpay for Platforms, which absorbed Payrix.

Fiserv is the larger company and the less focused one. In the same quarter it reported total revenue of $5.027 billion — but only $2.373 billion of that, 47%, came from Merchant Solutions. Another $2.302 billion, 46%, came from Financial Solutions, the bank-technology business. Total revenue fell 2.0% year over year. Operating income fell 34.2%, to $918 million. Financial Solutions itself contracted 4.8%. Its ISV surface is four doors — CardConnect, Clover, Carat, AccessOne — and nobody has announced a plan to merge them.

Then there is the governance picture, which is not decorative. Fiserv’s chief executive, Michael Lyons, resigned on June 12, 2026, effective immediately, taking no severance and no accelerated equity. Takis Georgakopoulos, previously Global Head of Payments for J.P. Morgan’s Corporate & Investment Bank, replaced him two days later. On July 7, president Dhivya Suryadevara resigned “for good reason.” Two securities class actions over statements about Clover’s growth are pending, both now in the Southern District of New York. Our Fiserv review covers all of it; nothing has been adjudicated.

What “Pure-Play” Actually Buys an ISV

It is easy to dismiss pure-play as investor-relations vocabulary. For a partner channel, it is not.

A merchant acquirer that also runs a bank-technology business allocates engineering headcount, sales incentive, and capital between them. When the bank-tech side is nearly half the revenue and shrinking, the pressure to defend it is real, and it competes with your channel for the same quarterly attention. Fiserv’s Financial Solutions segment fell 4.8% year over year in the first quarter of 2026. Its Merchant Solutions segment was flat. Neither of those is a story about your ISV roadmap accelerating.

Global Payments, having sold Issuer Solutions to FIS, has no such internal competition left. Everything it does now is merchant commerce. That does not automatically make it the better partner — a focused company can still deprioritize your vertical, and it is currently spending much of that focus digesting a $24.25 billion acquisition. But it does mean that when Global Payments funds a roadmap, the roadmap is in your category.

The counter-argument for Fiserv is genuine and deserves stating fairly. Being half a bank-technology company is precisely why Fiserv has seven sponsor banks standing behind First Data Merchant Services — Wells Fargo, Deutsche Bank, PNC, MVB, Pathward, Citizens, and KeyBank. That is a distribution and underwriting moat no independent gateway can replicate, and it exists because Fiserv sits on both sides of the bank relationship. Breadth is the price of the moat.

Two Doors Versus Four Doors

Neither company gives a software platform one obvious entry point. They are fragmented differently.

Global Payments has two ISV doors. Global Payments Integrated is the legacy program, formed when TSYS combined with OpenEdge, and it advertises a revenue sharing program alongside ProPay®, its payment-facilitation product. Worldpay for Platforms is the newer, embedded-native track that absorbed Payrix and names three explicit tiers. Which door you land behind depends largely on which sales team reaches you first, and the parent told the SEC it “was still in the process of modifying the design of our operating structure” as of March 31, 2026. This is a real problem for a partner, and a temporary one.

Fiserv has four ISV doors, and they route to different businesses entirely. CardConnect is the gateway and embedded-payments path, sold through the ISV Partner Program. Clover is a point-of-sale platform where the merchant becomes Clover’s customer and your software is an app in Clover’s marketplace. Carat is enterprise orchestration for very large merchants. AccessOne is patient financing for healthcare. The routing rule is unforgiving: e-commerce and vertical SaaS should evaluate CardConnect, POS-attached vertical SaaS should evaluate Clover, and most platforms have no business behind the other two doors at all. This is not a temporary problem. It is what a decade of acquisitions looks like when nobody consolidates.

Counting doors is not a trivial exercise. Every extra door is a separate contract, a separate developer surface, a separate residual structure, and a separate account team who will not know what the other one promised you.

Payment Facilitation: Two Routes Versus None Published

If your platform intends to eventually become a payment facilitator, this section decides the page.

Global Payments offers two published routes. ProPay is a registered payment-facilitation program on the Integrated side, described in its own materials as letting a partner set fees and split funds. Worldpay for Platforms names PayFac-as-a-Service and PayFac® developer as explicit rungs, with configurable fees allowing a platform to price its own merchants. Neither route is cheap and neither is fast, but both are advertised — which means both are negotiable.

Fiserv publishes no equivalent progression. Payment facilitation is available through specific arrangements, but there is no advertised path from CardConnect reseller to facilitator. In practice a platform that outgrows the residual model re-platforms rather than graduates, and re-platforming a live merchant base is close to the most expensive thing a software company can do to itself.

Neither company publishes a single revenue-share percentage. Any number you have seen quoted for either — and there are widely circulated bands — does not trace to a Global Payments or Fiserv source. Model the economics against your own merchant base with our revenue calculator, and read PayFac-as-a-Service for what the middle rung actually obliges you to take on.

Point of Sale: Clover Is Still the Answer

Global Payments has Genius, its unified point-of-sale platform, and it is being cross-sold aggressively into the estate Worldpay brought with it. It is a serious product.

It is not Clover. Clover’s hardware range, app marketplace, and installed base across restaurant and retail remain the deepest a software platform can attach to. If your merchants are going to put a terminal on a counter and that terminal is going to be a Clover, the argument mostly ends there — and it ends in Fiserv’s favor regardless of what the parent company’s revenue mix looks like.

The trade is the one that always accompanies distribution. On Clover, the merchant is Clover’s customer. You gain reach into an enormous base and surrender ownership of the relationship. Platforms that want the merchant and the brand should read our embedded payments guide before assuming reach is the same thing as economics.

Financial Stability: Growing Versus Contracting

Strip out the narrative and put the first quarter of 2026 side by side.

Global Payments grew adjusted net revenue roughly 5.5% on a normalized basis, expanded adjusted operating margin 110 basis points to 39.9%, grew adjusted EPS 10% to $2.96, reaffirmed its full-year outlook, and launched a $500 million buyback. Its GAAP bottom line was a $6.59 per-share loss, driven by acquisition accounting rather than trading.

Fiserv shrank. Total revenue down 2.0% to $5.027 billion. Operating income down 34.2% to $918 million. Selling, general and administrative expense up 12.1%. Merchant Solutions flat; Financial Solutions down 4.8%.

Neither company is fragile. Fiserv is a roughly $21 billion revenue business that raised €1 billion of senior notes in June 2026, which is not something the capital markets permit a distressed borrower to do. But an ISV signing a multi-year partner agreement is making a bet on which counterparty will still be investing in the channel in 2028, and the direction of travel is not ambiguous.

For the litigation, the disclosed accrual, and the executive departures in full, see our Fiserv review and the Authorize.net vs Fiserv comparison, which covers the same operating context from a gateway’s perspective.

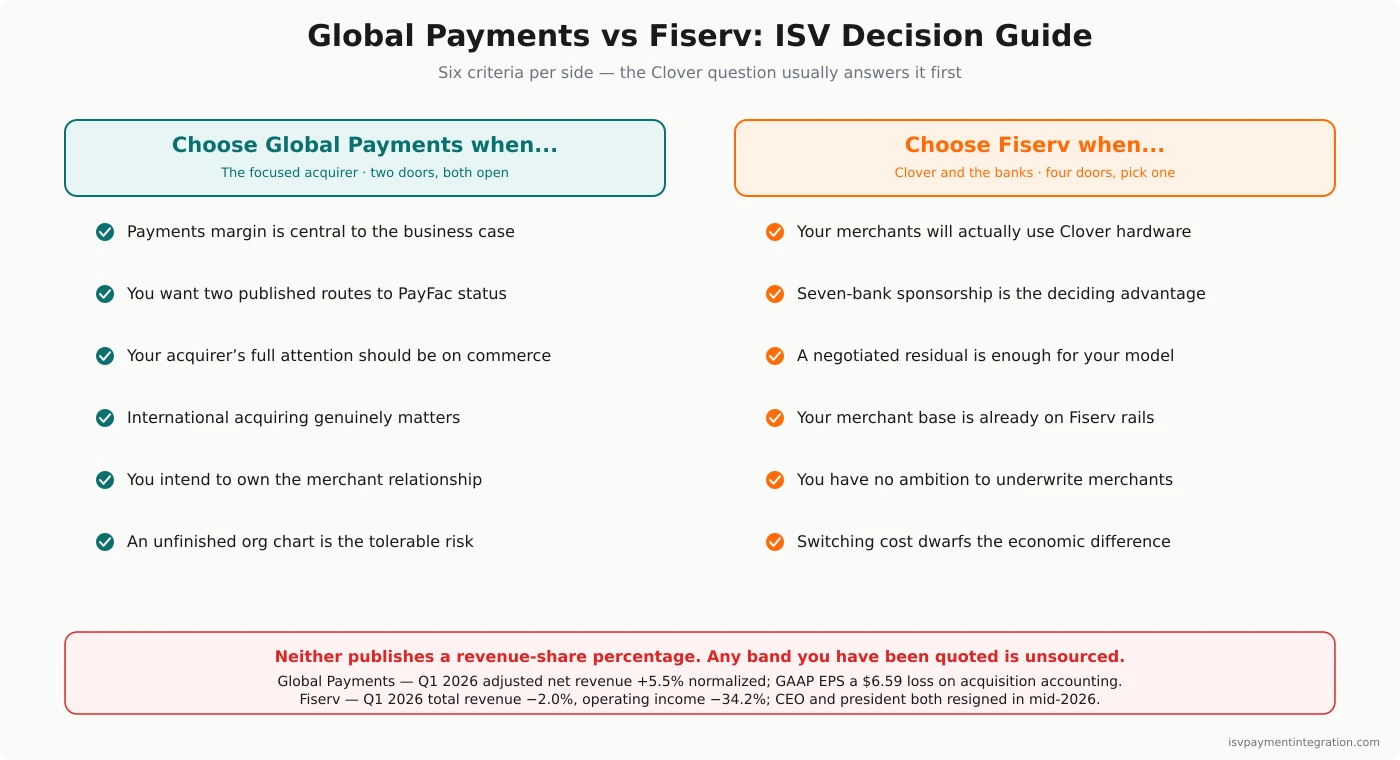

Where Each Platform Wins

Choose Global Payments when your business case depends on payments margin and you want an acquirer with two published routes to facilitation; when you want your partner’s entire company pointed at merchant commerce; when international acquiring matters; or when you would rather inherit an unfinished org chart than an unfinished leadership team.

Choose Fiserv when your merchants will actually use Clover hardware and that is the workflow you are integrating into; when seven-bank sponsorship and underwriting distribution are the deciding advantage; when a negotiated residual is a perfectly adequate outcome for your model; or when your merchant base already sits on Fiserv rails and the switching cost dwarfs the difference.

Choose neither when you want to own the merchant relationship, brand the whole experience, and see your economics in writing before you sign. Purpose-built PayFac-as-a-Service providers exist for exactly that, and the Payrix story is instructive — read our Payrix review to see what became of an independent PFaaS provider after it was acquired into a large acquirer’s stack.

Global Payments vs Fiserv: ISV Decision Guide

- Will your merchants use Clover? If yes, that usually settles it, whatever the parent-company story says.

- Do you intend to become a payment facilitator? One of these two has published routes. The other does not.

- Whose customer is the merchant, in your plan? Clover answers this for you, and the answer is not “yours.”

- How much does your acquirer’s focus matter to your roadmap? One company sold everything that was not merchant commerce. The other still earns 46% of revenue from bank technology.

- Can you tolerate an unfinished org chart, or an unfinished leadership team? You are choosing one of them.

- Which door will you actually enter through? Ask that question of both vendors, by name, and get the answer before the contract rather than after.

- What happens to your economics if the processor raises rates mid-term? Neither publishes rates. Both negotiate. Put the escalation clause in writing.

For the two brands inside Global Payments, see Worldpay vs Global Payments. For a gateway-first alternative to both, see NMI vs Global Payments.

Frequently Asked Questions

Is Global Payments bigger than Fiserv?

No. Fiserv is the larger company by revenue — $5.027 billion in the first quarter of 2026, against $2.97 billion GAAP for Global Payments. But that comparison flatters Fiserv, because only 47% of its revenue is merchant acquiring. Fiserv’s Merchant Solutions segment produced $2.373 billion in the quarter, against Global Payments’ $2.86 billion of adjusted net revenue from a business that is now entirely merchant commerce. On the axis an ISV cares about, the two are close — and Global Payments is growing while Fiserv’s total revenue fell 2.0%.

What does it mean that Global Payments is a “pure-play”?

On January 9, 2026, Global Payments completed its $24.25 billion acquisition of Worldpay and simultaneously divested its Issuer Solutions business to FIS. The company now describes itself, in its chief executive’s words, as “a focused, pure-play commerce solutions leader,” meaning it no longer runs a card-issuing or bank-technology business alongside merchant acquiring. Fiserv still does: its Financial Solutions segment produced $2.302 billion of revenue in the first quarter of 2026, 46% of the company total.

Which one is better for an ISV that wants to become a PayFac?

Global Payments, without much argument. It offers two published routes: ProPay, a registered payment-facilitation program on the Global Payments Integrated side, and PayFac® developer, the top rung of Worldpay for Platforms. Fiserv offers payment facilitation through specific arrangements but publishes no progression from CardConnect reseller to facilitator, which in practice means outgrowing the residual model requires re-platforming rather than graduating.

Do Global Payments or Fiserv publish ISV revenue-share rates?

Neither does. Global Payments Integrated advertises a revenue sharing program, and Worldpay for Platforms advertises configurable fees that let a platform set its own merchant pricing, but no percentage is attached to either. Fiserv publishes no rate card for any of its ISV-relevant product lines; the single fee it commits to in writing is the App Market Transaction Fee in Clover’s Developer Terms. Percentage bands quoted on comparison sites do not trace to any filing, earnings material, or product page from either company. The only number that means anything is the one in your own term sheet.

Should Fiserv’s executive departures change my decision?

They should change your contract, not necessarily your shortlist. Fiserv’s chief executive resigned on June 12, 2026 with no severance, his successor was appointed two days later, and the president resigned on July 7. Two securities class actions are pending and nothing has been adjudicated. Fiserv remains a roughly $21 billion revenue business with seven sponsor-bank relationships. What changes is that the people who negotiated your partner terms may not be there to honor them. Ask for a written rate-lock, a ninety-day notice period on any fee change, and a termination right without penalty if the markup moves past a threshold you define.