NMI vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

Put NMI and Fiserv side by side and the feature grid quietly hides the real decision, because they are not the same layer of the payments stack. One is a white-label gateway that brokers your transactions to whichever acquirer you choose; the other is the acquirer — the rail, the sponsor banks, and the counter hardware — sold as a single integrated stack. A software platform is really deciding whether the gateway should stay independent of the acquirer underneath it, or be fused to it.

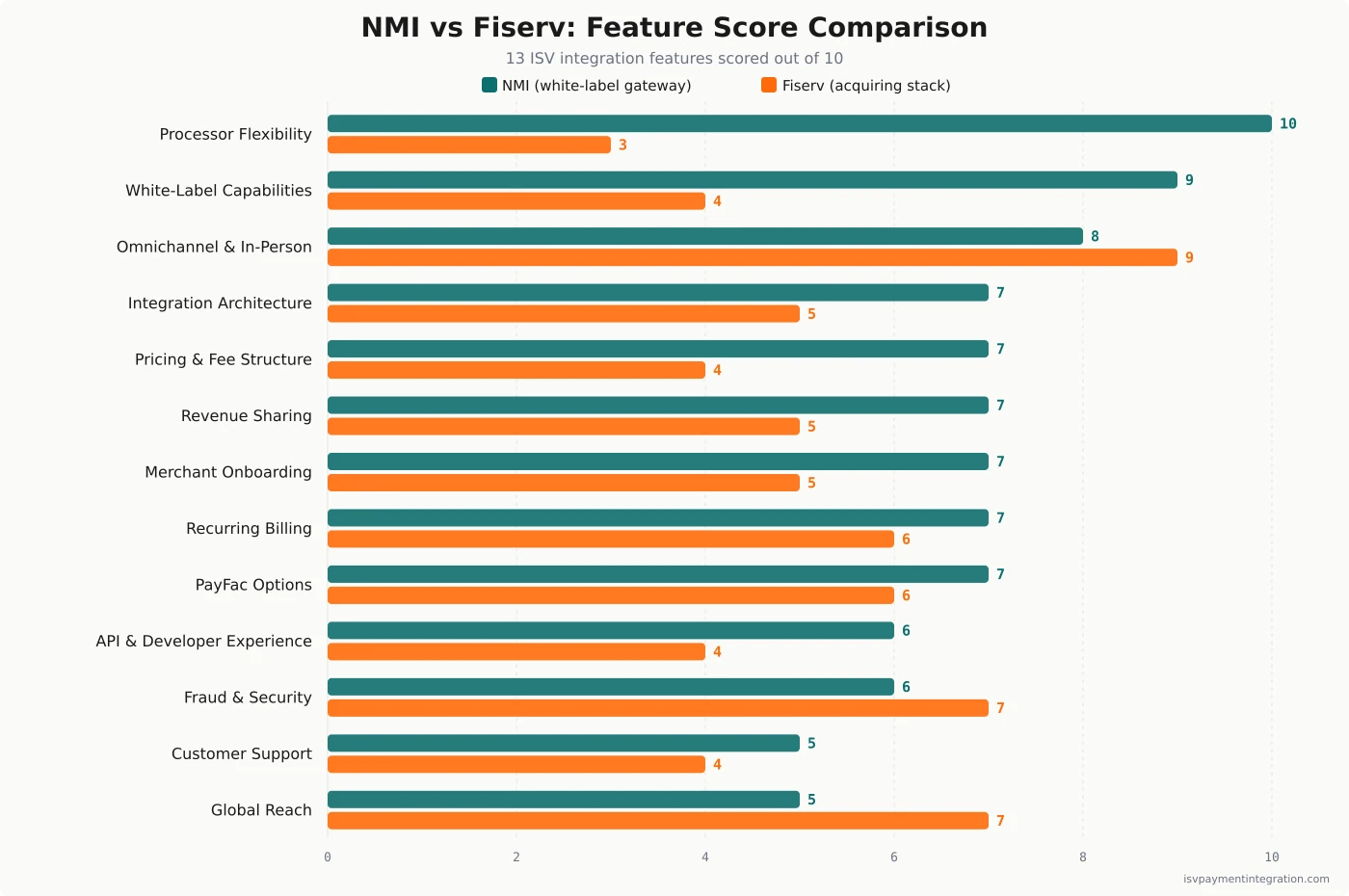

Feature Comparison

| Feature | NMI | Fiserv |

|---|---|---|

| Integration Architecture | 7 | 5 |

| API & Developer Experience | 6 | 4 |

| White-Label Capabilities | 9 | 4 |

| Processor Flexibility | 10 | 3 |

| Pricing & Fee Structure | 7 | 4 |

| Omnichannel & In-Person Payments | 8 | 9 |

| Fraud & Security | 6 | 7 |

| Revenue Sharing | 7 | 5 |

| Merchant Onboarding | 7 | 5 |

| Global Reach | 5 | 7 |

| Recurring Billing | 7 | 6 |

| Customer Support | 5 | 4 |

| PayFac Options | 7 | 6 |

Get this comparison as a shareable PDF

We'll send the NMI vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

NMI

Best for ISVs and SaaS platforms that want a fully white-labeled gateway keeping their own brand, logo and pricing model in front of merchants, that value connecting to many acquirers through one integration, and that serve card-present, unattended or cross-border merchants where processor choice matters. Accept that NMI is a gateway, not an acquirer — you still need a processor underneath it, and headline economics are negotiated with a partner rep.

Best for

Fiserv

Best for platforms whose merchants live behind a counter, or that want the gravitas of the world's largest merchant acquirer with its sponsor-bank underwriting and Clover ecosystem, and that prefer one vendor and one contract over assembling their own stack. Less ideal for platforms that want to keep the acquirer swappable, or that want a modern gateway they fully control.

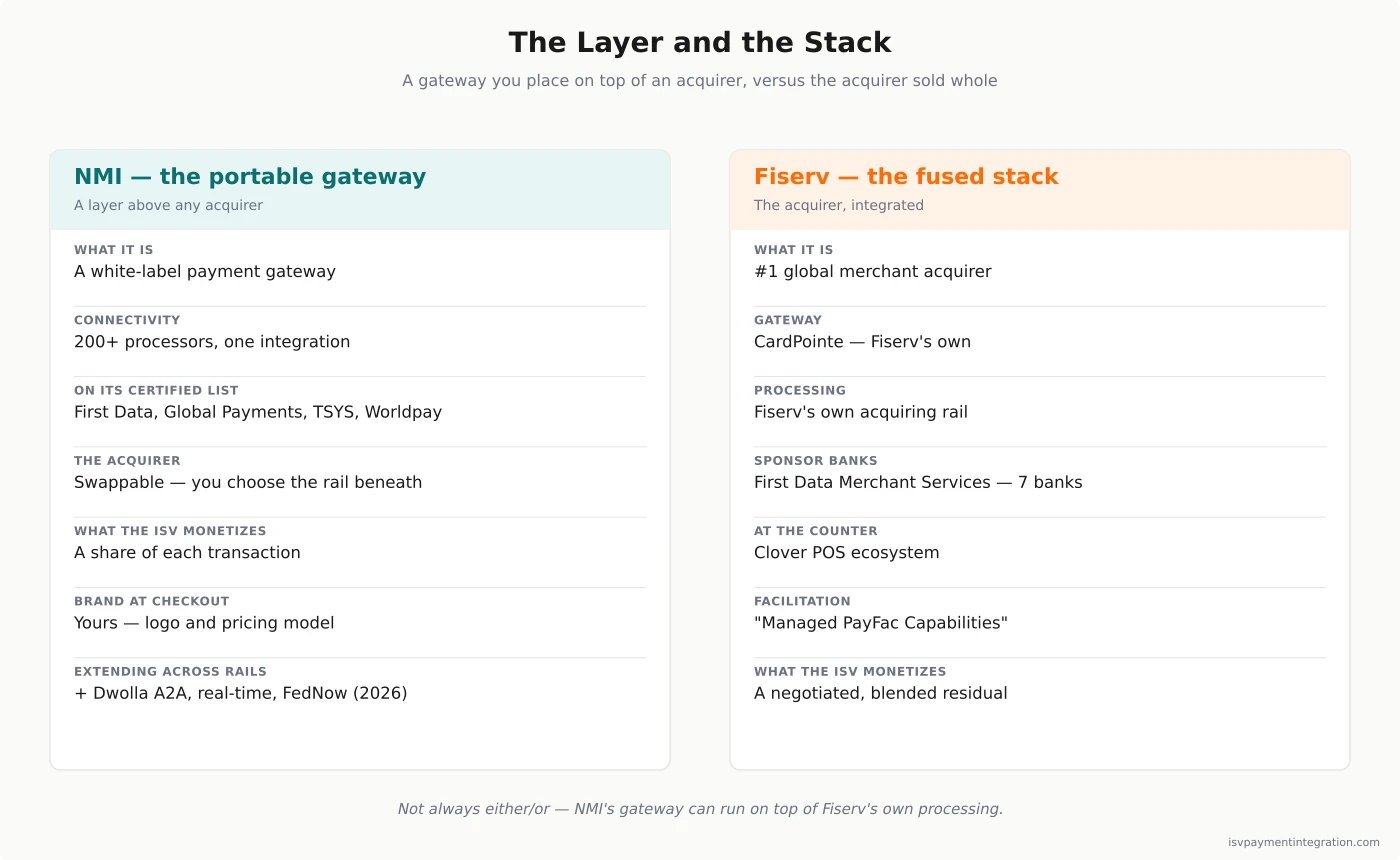

NMI vs Fiserv: The Layer and the Stack

The instinct with a comparison like this is to line the two companies up feature by feature and add the columns. It misleads here, because NMI and Fiserv do not sit at the same place in the payments stack. Fiserv is an acquirer — it holds the sponsor-bank relationships, moves the money, and sells software platforms an integrated stack that runs from its CardPointe gateway down through its own processing to the Clover device on a merchant’s counter. NMI is a gateway — a piece of infrastructure that sits above the acquirer, takes a transaction from a merchant’s checkout, and routes it to whichever processor the platform has chosen to sit underneath. NMI describes itself as an embedded-payments platform that has run its gateway “since 2001”; Fiserv’s own ISV page calls itself the #1 global merchant acquirer.

That difference in altitude is the whole comparison, and it decides more than any single feature score. One product is a layer you place on top of an acquirer and can move; the other is the acquirer, sold whole. A platform choosing between them is really choosing an architecture. And this particular pairing hides a wrinkle most head-to-heads miss: NMI’s own certified-processor list names First Data — Fiserv’s acquiring stack — so one of these two companies can be run directly on top of the other. That single fact, impossible to reproduce against an acquirer that only settles its own traffic, is where the decision actually turns.

Quick Take: A Gateway You Route and a Stack You Rent

NMI reaches a software company as a white-label gateway and the tooling around it. Its gateway page markets integration with 200+ payment processors, 125+ shopping carts and a wide range of devices, and its SaaS page invites platforms to “monetize payments and generate more revenue” while keeping “your logo, application, and customer experience front and center.” Alongside the gateway sit Merchant Central, its CRM-plus-underwriting console for onboarding and residuals, and NMI Payments, its all-in-one acceptance product. Across those, NMI is consistent about one thing: the platform stays in control of the brand and the pricing, and NMI supplies the rails-agnostic plumbing beneath it. At its scale — 1.2 million-plus active merchants, roughly 6.5 billion transactions a year and $502+ billion in annual payment volume across 6,000 channel partners — it is a large piece of infrastructure that almost never appears to the cardholder.

Fiserv courts the same software companies through its ISV Partner Program, and the program runs on three verbs its page states plainly: Integrate, Monetize, Grow. The acceptance gateway is CardPointe; CoPilot manages the partner’s portfolio; and the program advertises “Managed PayFac Capabilities” — payment facilitation Fiserv operates on the platform’s behalf. Running beside it is Clover, the point-of-sale ecosystem much vertical software connects to. The proof points Fiserv leads with are all acquiring scale: the world’s number-one merchant acquirer, 78 billion merchant transactions a year, reaching nearly 100% of U.S. households. What a platform buys here is not a layer to place on top of an acquirer; it is the acquirer itself.

Gateway or Acquirer: The Distinction That Reframes Everything

Because “gateway” and “acquirer” get used loosely, it is worth being precise, since the imprecision is exactly what makes this comparison confusing. An acquirer is the entity with card-network membership and a sponsor-bank relationship that can actually settle a card payment into a merchant’s account. Fiserv, through First Data Merchant Services, is that entity at enormous scale. A gateway is the software that carries an authorization from a checkout to an acquirer and back; it does not need a bank charter, and it does not have to be tied to any one acquirer.

NMI is built as that second thing. It routes transactions to the processors and acquirers it integrates with rather than holding the sponsor-bank relationship itself — which is why its product surface is about connectivity and control, not underwriting and settlement. Its Transaction Routing feature, in its own words, “automatically determines which MIDs to route transactions to based on active routing directives using a single gateway account.” A platform can therefore keep one integration to NMI and change, add, or split the acquirer beneath it without rebuilding its checkout.

Fiserv collapses those layers into one. The gateway is CardPointe, the processing is Fiserv’s, and the sponsor banks are Fiserv’s — First Data Merchant Services is disclosed as a registered Independent Sales Organization of seven banks (Wells Fargo, Deutsche Bank, PNC, MVB, Pathward, Citizens and KeyBank), while the CardConnect door names five of them. That vertical integration is a genuine strength: one vendor owns the whole path, so there is one contract, one point of accountability, and underwriting muscle no independent gateway can match. It is also, by construction, not portable — the gateway and the acquirer are the same company.

The Tell: NMI Can Sit In Front of Fiserv

Here is the fact that dissolves the idea that this is a clean either/or. NMI’s own list of certified processors and acquirers names First Data — the acquiring stack that is now Fiserv — right alongside Global Payments, TSYS, Worldpay and Elavon. In other words, at the level of architecture, NMI’s white-label gateway can run on top of Fiserv’s processing. The gateway layer and the acquiring layer are separable enough, in principle, that one of these two companies could sit in front of the other. That separability is the point — not a promise that Fiserv will happily sell you a fresh agreement to sit behind a rival gateway and disintermediate its own CardPointe, and running through any third-party gateway can forfeit some of an acquirer’s native tooling. What it establishes is narrower and still decisive: the two layers are not welded, so the acquirer stays a choice you keep making rather than one the gateway makes for you.

That reframes the question from “NMI or Fiserv?” to something more useful: do you want the gateway decoupled from the acquirer, or fused to it? If decoupled, NMI gives you a portable control layer and you choose the acquirer underneath — possibly Fiserv, possibly Fiserv today and someone else tomorrow. If fused, Fiserv gives you one stack where you never have to think about the seam between gateway and acquirer, because there is no seam. Neither answer is wrong; they are answers to different priorities, and a platform that treats the two products as straight substitutes will mis-scope its own build.

What the ISV Actually Monetizes

Follow the money from the platform’s seat and the two models diverge again. A software company earns on embedded payments from the margin between what its merchants pay and what its supplier charges — but what it is marking up differs.

With NMI, the platform monetizes a gateway. Its SaaS page tells software companies they can “unlock new revenue streams by earning a share of each transaction,” and its Payments product has platforms “find, qualify, acquire and onboard merchants—all while sharing in the net payment revenue.” The processing cost sits in a separate, negotiated layer beneath the gateway, which means the platform can see and manage the two components independently — and can shop the acquiring layer without touching the gateway it has already built on.

With Fiserv, the platform monetizes a residual on Fiserv’s own acquiring. The ISV Partner Program’s whole middle verb is “Monetize” — but there is no published tier, percentage, or rate anywhere on its ISV-facing pages. The economics arrive through a partner conversation, bundled into a rate the merchant never sees itemized. That is not necessarily worse; a platform with real volume can negotiate a strong residual against the largest acquirer in the world. It is simply opaque by default, where NMI’s two-layer structure is legible by default.

Who Owns the Merchant — and the Exit

The decoupling question has a second edge: portability and lock-in. NMI’s marketing leans hard on it — “get to market faster, and continue to grow, without ever having to rip-and-replace your payments technology” — and the single-gateway-account routing model is what makes that credible. But it is worth being exact about what portability here does and does not mean, because the marketing invites an overread. It is integration-level, not merchant-level: the code your engineers built on NMI stays put when you change the acquirer beneath it, yet every merchant still has to be re-boarded and re-underwritten onto new MIDs at the new acquirer, tokens re-vaulted, funding and dispute history reset. Swapping the rail is an operational project, not a config change. What NMI removes is the rebuild of your own gateway integration — real, and worth a lot — not the migration of your book of business. NMI has been extending that same neutrality across payment types, too: in May 2026 it acquired the account-to-account provider Dwolla, adding API-first bank transfers, real-time payments and FedNow, and forming a combined business it says processes close to $700 billion a year — a figure that fuses card and account-to-account rails, so read it as breadth of rails, not a like-for-like answer to a card-volume number. The through-line is a layer that stays independent of any single rail.

Fiserv’s advantage runs the other way, and it is real. Because it is the acquirer, it brings sponsor-bank distribution, the underwriting reach to board heterogeneous or higher-risk merchants, and — through Clover — a hardware ecosystem a restaurant or salon runs its whole day on. Those are things a neutral gateway structurally cannot hand you. The trade is that they also raise the cost of leaving: a merchant base sitting on Clover devices and Fiserv settlement does not casually migrate, and that stickiness is precisely the moat Fiserv is selling. Be honest, though, that NMI’s model has its own gravity well. A platform whose checkout, card vault and merchant operations are built deep into NMI’s gateway and Merchant Central has a real switching cost too — leaving NMI means re-tokenizing the vault and rebuilding the integration, and the fraud and risk picture is now split across two parties rather than owned by one. NMI keeps the acquirer swappable partly by making the gateway the thing you are married to. Portability and distribution are both assets. They just pull in opposite directions, and a platform should know which lock-in it is choosing, because it is always choosing one.

Where Fiserv Is Simply Bigger

None of the above should read as a thumb on the scale. On several axes Fiserv is plainly the heavier platform, and pretending otherwise would misfit a platform whose merchants need exactly what Fiserv is best at. It is the number-one merchant acquirer on earth, it processes tens of billions of merchant transactions a year, and its acceptance reaches almost every U.S. household — supply-side scale a twenty-year-old independent gateway does not match. At the counter, Clover’s installed base and hardware breadth are a category of their own. And the sponsor-bank roster behind First Data Merchant Services is the kind of banking distribution that took decades and acquisitions to assemble.

If a platform’s merchants are counter-attached, need heavy underwriting, or benefit from a marquee acquirer’s name on the paperwork, that gravity is the deciding factor and NMI’s neutrality is beside the point. Read the feature grid on this page for what it is, too: a score of ISV-integration surface — the API, the white-labeling, the routing, the onboarding tooling — not a measure of who carries settlement and underwriting risk. That last capability is Fiserv’s structurally, being the acquirer itself, and it is not a row you will find on the chart. The gateway-versus-acquirer framing tells you where each company is strong; it does not exempt you from matching that strength to the merchants you actually serve.

The Price Neither Publishes

It is worth conceding a symmetry that cuts against the easy narrative. It is fair to say Fiserv publishes no processing rate and no PayFac ladder on any of its ISV-facing properties; the figure that reaches a platform is whatever its partner rep negotiates, never anything posted publicly. But it is not fair to say NMI hands you a rate card either. NMI publishes no headline gateway price; its economics are partner-negotiated too, arranged with a sales team rather than posted on a pricing page.

So both companies gate the price. The difference this comparison actually turns on is not who is more forthcoming about the number — it is where the acquirer lives. With NMI the acquirer is a separate, swappable layer you negotiate on its own; with Fiserv the acquirer is the vendor, and the residual is one blended figure inside a single relationship. Read the Fiserv pricing breakdown and the NMI pricing breakdown side by side and the contrast is architectural, not a matter of one being cheaper than the other on a sticker.

Most ISVs Are Choosing an Architecture, Not a Vendor

Here is the reframe that makes the decision tractable. The choice is rarely “which of these two processors is better,” because they are not two processors — they are a gateway layer and an acquiring stack. The real question is how you want your payments architecture to be shaped, and it resolves cleanly once you ask it that way.

If you want to own the payment experience end to end, keep the acquirer swappable, and treat payments as a portable capability inside your software, NMI is the design that fits. You build once on its white-label gateway, choose an acquirer to sit beneath it — even Fiserv, if its economics win — and keep the option to change that acquirer later without disturbing the integration your engineers already shipped. Payments become a layer you control rather than a vendor you are married to.

If you would rather not run the seam between gateway and acquirer at all — if one vendor, one contract, and the largest acquiring rail with a hardware ecosystem attached is worth more to you than portability — Fiserv is the design that fits. You accept a negotiated residual and a degree of lock-in in exchange for reach, underwriting, and the counter. The mistake is to run the feature bake-off, notice that NMI wins on flexibility and Fiserv wins on scale, and never realize those are not competing scores on one axis but two different shapes for your stack. Decide the shape first. For the adjacent evaluations, Stripe vs Fiserv covers the API-first acquirer that does publish its platform economics, and Adyen vs NMI weighs a global single-stack acquirer against the same neutral gateway — with the twist that Adyen, unlike Fiserv, is its own acquirer end to end and cannot be placed behind NMI the way First Data can. Model the revenue either way with the revenue calculator, and read the full NMI review and Fiserv review for the ground-level detail.

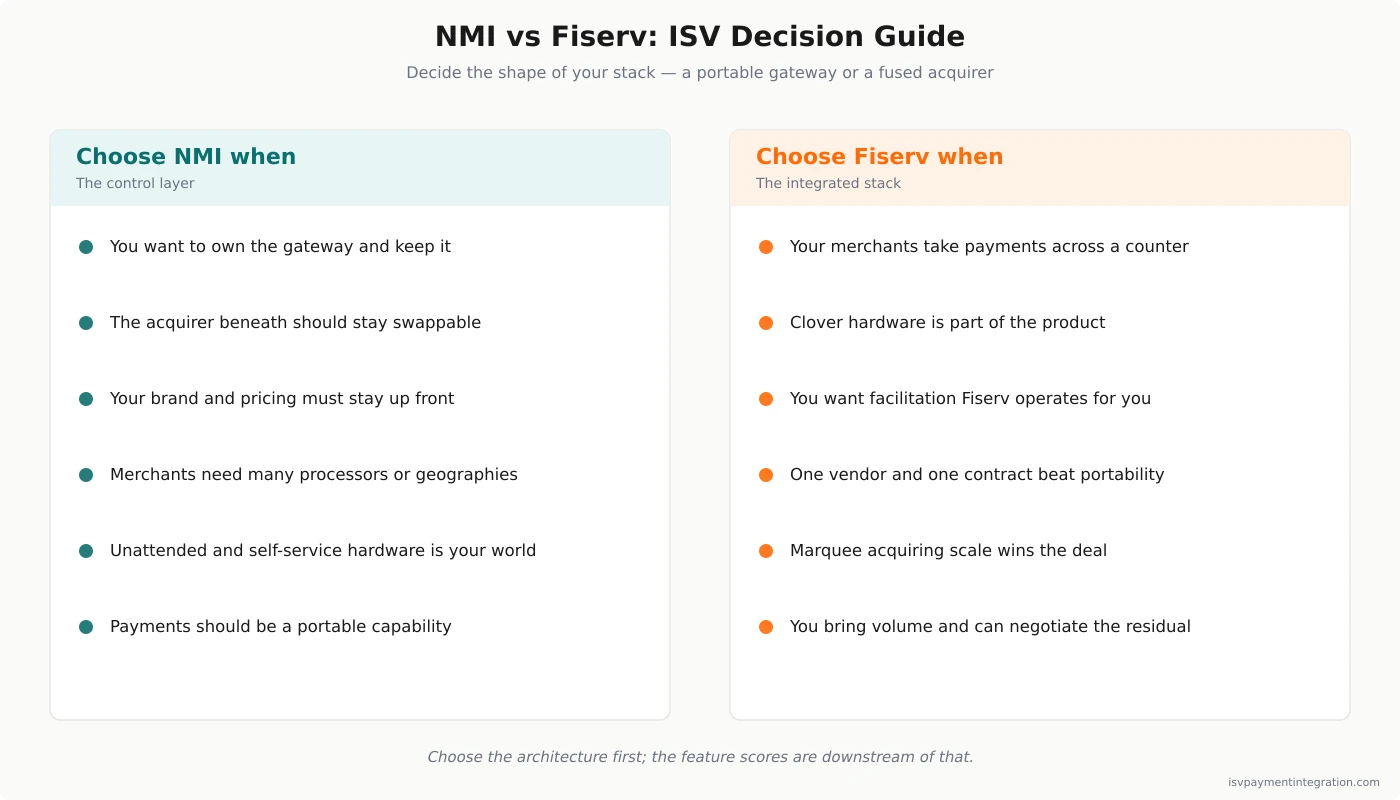

NMI vs Fiserv: ISV Decision Guide

- Is the gateway something you want to own and keep? If payments should be a portable capability inside your software, a white-label gateway you build once and keep points to NMI. If you would rather not own that layer at all, Fiserv absorbs it.

- Do you want the acquirer to be swappable? NMI lets you change the processor beneath a single integration; Fiserv is the processor, so switching means leaving.

- How much do you value one throat to choke? One vendor and one contract across gateway, processing and banking is Fiserv’s structural advantage. Assembling the layers yourself is the price of NMI’s flexibility.

- Is the point of sale a physical counter? When the terminal runs the merchant’s day, Clover’s hardware operating system tilts the decision toward Fiserv regardless of gateway preferences.

- Do your merchants need many processors or geographies? Routing across 200+ processors from one account is NMI’s home ground; a single acquiring stack is not built to be multi-homed.

- Whose brand sits in front of the merchant? NMI is built to keep your logo and pricing model front and center; Fiserv’s CardPointe can be white-labeled, but Clover wears its own name at the counter.

- What are you actually monetizing? A share of transactions on a gateway you control, versus a negotiated residual on Fiserv’s acquiring — legible layers against a blended figure.

Frequently Asked Questions

Is NMI a payment processor or a gateway, and how is that different from Fiserv?

NMI is a payment gateway, not an acquiring processor. It carries a transaction from a merchant’s checkout to whichever processor or acquirer the platform has chosen, and it markets integration with 200+ payment processors from a single gateway account — but it does not hold the sponsor-bank relationship or settle funds itself. Fiserv is the opposite: it is an acquirer, the #1 global merchant acquirer, with its own processing and sponsor banks disclosed through First Data Merchant Services. So you are not comparing two like-for-like processors; you are comparing a portable gateway layer against a vertically integrated acquiring stack. That distinction, more than any feature, is what should drive the choice.

Can I use NMI and Fiserv together rather than choosing one?

Often, yes — and this is the detail most head-to-heads miss. NMI’s own certified-processor list names First Data, the acquiring stack that is now Fiserv, alongside Global Payments, TSYS, Worldpay and Elavon. That means a platform can run NMI’s white-label gateway on top of Fiserv’s processing, keeping NMI as the control layer while Fiserv provides the rail underneath. The genuine either/or only appears if you want Fiserv’s fully integrated stack — CardPointe plus Clover plus its settlement — as a single package. If what you value is a gateway you own and an acquirer you can swap, NMI in front of an acquirer of your choice is a legitimate architecture rather than a fallback — though running any gateway in front of an acquirer can mean giving up some of that acquirer’s native, integrated tooling, so weigh it against what you would lose.

Which one lets an ISV keep its own brand at checkout?

NMI, more completely. Its SaaS page is explicit that a platform keeps “your logo, application, and customer experience front and center,” and its gateway is designed to be white-labeled end to end, so the cardholder need never see NMI. Fiserv’s CardPointe gateway can also be white-labeled, and the acquiring rail itself is invisible to the buyer — but Clover is the exception, because that hardware wears its own brand on the merchant’s counter. If an unbranded, fully-owned payment experience is central to your product, NMI is built around that goal; with Fiserv it depends heavily on whether your merchants are on Clover devices.

How does an ISV make money on each platform?

The mechanics differ. With NMI, a software platform earns “a share of each transaction” on a gateway it controls, with the processing cost sitting in a separate, negotiated layer beneath — so the revenue and the cost are two legible components you can manage independently. With Fiserv, the platform earns a residual through the ISV Partner Program’s “Monetize” track, but that figure is negotiated and blended into a rate with no published tier or percentage. Neither posts a public rate card, so both require a sales conversation; the difference is that NMI’s two-layer structure keeps the gateway margin and the processing cost visibly separate, while Fiserv’s arrives as one number.

Which is better for in-person and counter-based merchants?

Fiserv, clearly, when the counter is central. Clover is a full countertop operating system — handling the register, order flow, receipts and inventory — and its market tenure and device footprint are things a gateway’s certifications alone do not reproduce, with Fiserv settling the payments behind it. NMI is strong in-person too — it certifies a wide device estate, counts 235K+ connected devices and 300+ EMV certifications, and is genuinely best-in-class for unattended and self-service acceptance like kiosks, parking and vending. So the nuance is the vertical: for a full countertop point-of-sale ecosystem, Fiserv’s Clover leads; for unattended and self-service hardware behind your own software, NMI’s device breadth and flexibility are hard to beat.