Checkout.com Pricing

Pricing model: Custom interchange++ (no published rate card). Based on publicly available information from Checkout.com's official site. Contact Checkout.com directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | Not publicly disclosed by Checkout.com. Third-party sources cite ~0.95% + $0.20 for European cards and ~2.90% + $0.20 for non-European cards at the standard tier. Enterprise reports cluster around interchange + 0.10%–0.40% + $0.08. None of these numbers appear on checkout.com — every cited figure traces back to comparison-blog research, not an official rate card. |

| Markup | Volume-tiered and negotiated per merchant. Sales qualification form ranges from under $1M to $5B+ annual processing. Independent procurement guides identify roughly £50M (~$63M) annual processing as the leverage threshold for genuinely negotiated rates. |

| Setup | $0. Explicitly confirmed on checkout.com/pricing — no setup fees, no account maintenance fees, no PCI fees, no early-termination fee on the published page. |

| Monthly | $0 monthly fee. A minimum billing threshold applies — the amount is not disclosed publicly. The legal page at checkout.com/legal/minimum-billing-fee enumerates 25+ fee types that count toward the threshold. |

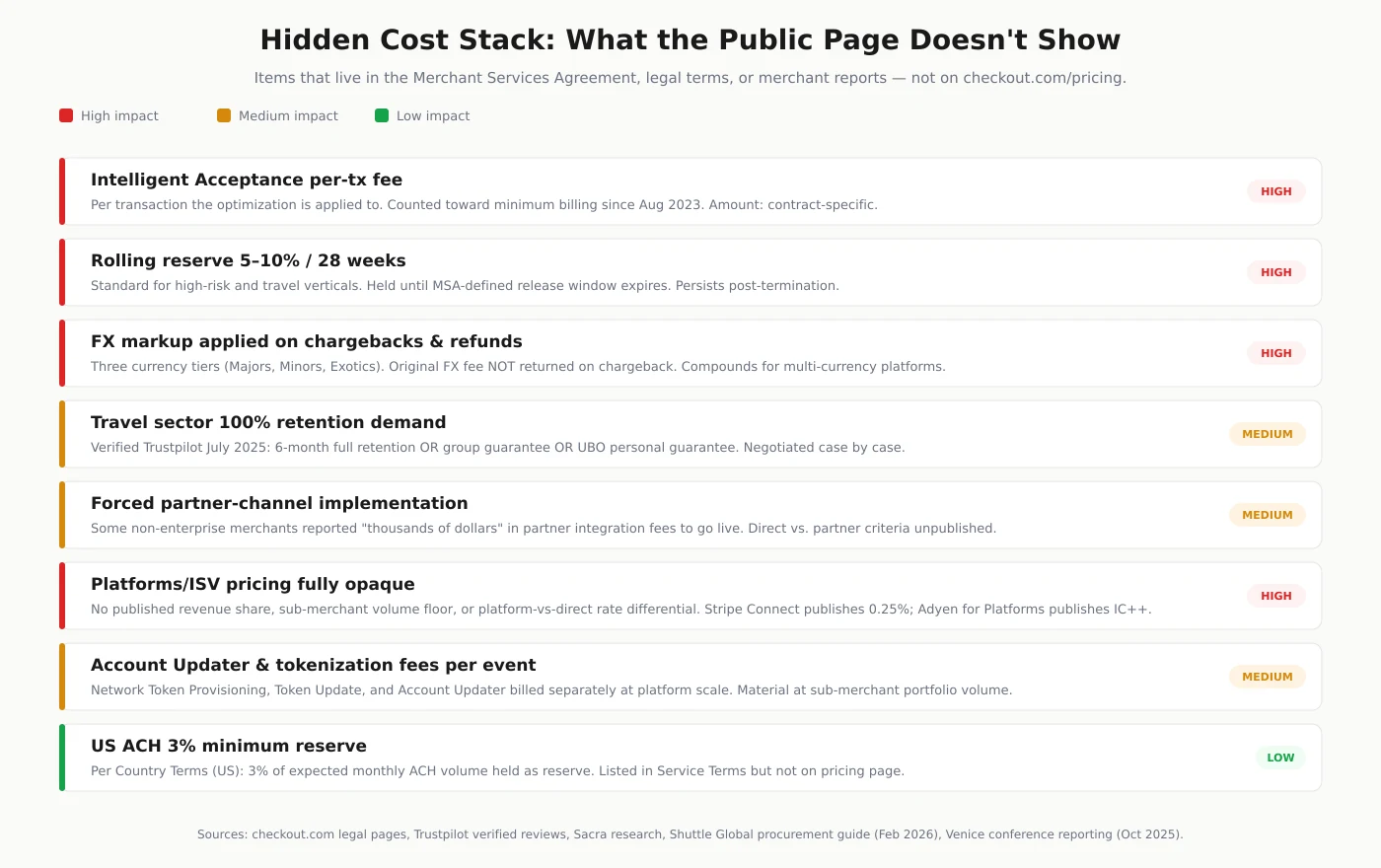

Hidden Costs to Watch

- ⚠ Intelligent Acceptance: charged per transaction once activated, with the per-transaction amount contract-specific. Has counted toward the minimum billing threshold since August 2023. G2 reviewers flag it as a margin-compression item that should have been bundled into the headline rate.

- ⚠ Rolling reserve of 5–10% of every charge, held 28 weeks. Standard for high-risk verticals and travel. Exact percentage and release schedule live in the Merchant Services Agreement, not on any public page. On account termination, both settlement payouts and reserves are held until the MSA-defined release window expires.

- ⚠ FX markup is contract-specific across three currency tiers (Majors, Minors, Exotics) and applies on refunds and chargebacks. The original FX fee is not returned when a chargeback hits, creating compounding exposure for multi-currency ISVs.

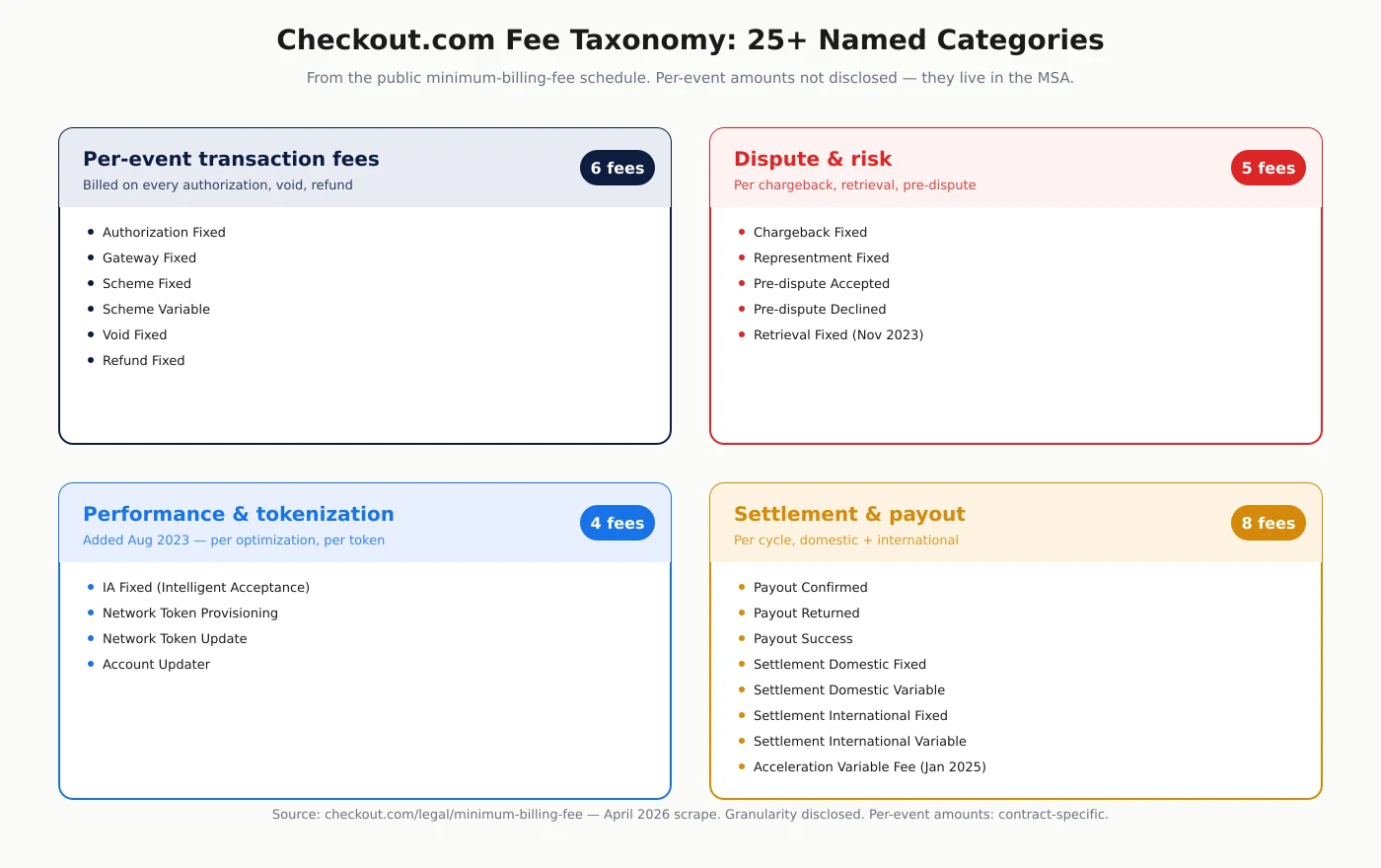

- ⚠ 25+ separately-billed fee categories on the minimum-billing-fee schedule: Authorization Fixed, Gateway Fixed, Scheme Fixed and Variable, Void, Chargeback, Representment, Pre-dispute Accepted/Declined, Retrieval, IA Fixed, Network Token Provisioning and Update, Account Updater, Payout Confirmed/Returned/Success, Settlement Domestic and International (Fixed and Variable), and an Acceleration Variable Fee added in January 2025.

- ⚠ Travel and high-risk verticals have documented 100% payment retention demands for 6 months plus minimum monthly processing thresholds, per a verified July 2025 Trustpilot review. Conditions are negotiated case by case.

- ⚠ Test-to-live forced partner-channel implementation has been reported to cost thousands of dollars for some non-enterprise merchants. Direct vs. partner channel access criteria are not published.

- ⚠ Platforms/ISV pricing is entirely opaque: no published revenue share, no sub-merchant volume floors, no rate differential between direct and partner channels.

- ⚠ US ACH transactions require a minimum reserve of 3% of expected monthly ACH volume per the Country Terms (US) section of the Service Terms.

Alternatives

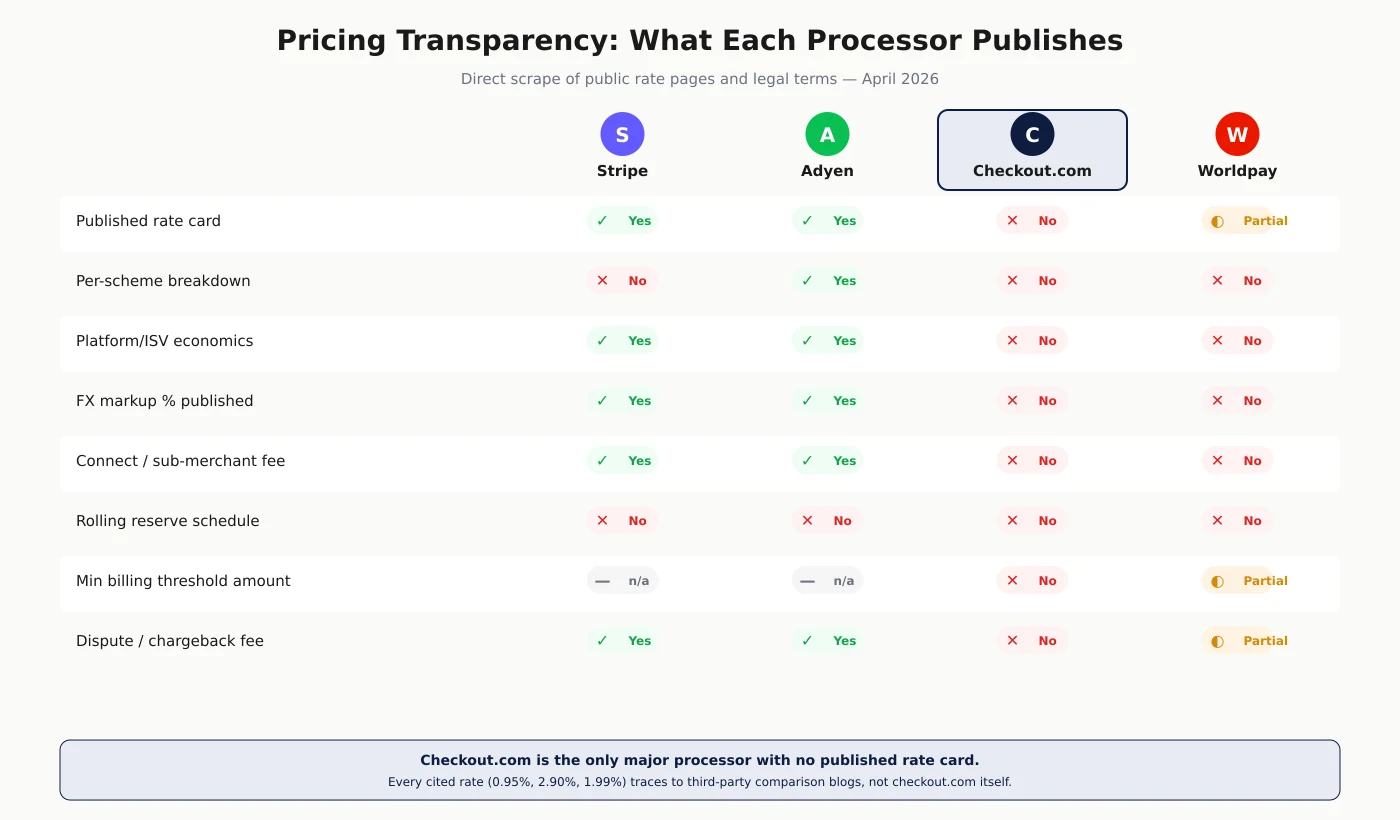

Checkout.com’s Pricing Page Has No Rates

Checkout.com is the only major payment processor that publishes zero rates publicly. The pricing page at checkout.com/pricing is a contact-sales lead-generation form. The official quote, captured directly from the live page in April 2026 and unchanged in the Wayback Machine archive going back to April 2024:

“Pricing that works for you. Your business deserves tailored pricing based on your needs. Create a plan by getting in touch with our team today.”

Every Checkout.com pricing article you find online cites a specific set of numbers — 0.95% + $0.20 for European cards, 2.90% + $0.20 for non-European cards, 1.99% currency conversion, 0.10%–0.40% interchange-plus markup. None of those rates appear on checkout.com. Not on the pricing page. Not in the legal terms. Not in the developer documentation. Not in the international coverage guide. Every cited number traces back to comparison-blog research, sales-call leaks, or fabrication — not an official rate card.

This page documents what Checkout.com actually publishes, what third-party sources widely cite, and what the gap means for ISVs and software platforms evaluating Checkout.com against Stripe, Adyen, and Worldpay in 2026.

What Checkout.com Actually Publishes (And What It Hides)

The verifiable facts from checkout.com itself, scraped directly:

- $0 setup fees, $0 account maintenance fees, no surprise fees. These are the only dollar amounts published anywhere on the pricing page.

- Three pricing structures named without rates: fully flat-rate, simple interchange++, and free for registered charities.

- 145+ processing currencies, domestic processing in 55 countries, ~20 settlement currencies (from the international coverage page).

- Active legal entities in 10 jurisdictions with country-specific terms: UK, France/EEA, UAE, New Zealand, Hong Kong, Australia, Singapore, Canada, Japan, United States.

- A Platforms/Integrated Platforms product for PayFacs, marketplaces, and SaaS platforms — with onboarding, fund splitting, and sub-entity payouts. No revenue share or sub-merchant volume floor disclosed.

- A minimum billing threshold that 25+ separately-named fee categories count toward. The threshold amount is not disclosed.

- Chargebacks and assessments are passed through at cost to the merchant per the Service Terms, with recovery via settlement deduction, reserve debit, or invoice. No chargeback handling fee is published.

- A US ACH minimum reserve of 3% of expected monthly volume per the US Country Terms.

Everything else — the actual rate card, FX markup percentages, IA per-transaction amounts, platform revenue share, sub-merchant minimums, rolling reserve schedules, monthly billing thresholds — lives only in the Merchant Services Agreement that prospects sign after a sales call.

Where the 0.95% and 2.90% Numbers Came From

The most-cited Checkout.com rates appear in roughly this form across every comparison site: standard tier 0.95% + $0.20 for European cards, 2.90% + $0.20 for non-European cards. The numbers are repeated by Card Payment Options, Whop, Wise, Merchant Alternatives, and most SEO-driven payment-processing blogs.

They are credible because they are consistent across sources. They are unverifiable because the source of truth — a Checkout.com rate card — does not exist publicly. The most likely origin is a sales-quote leak from 2021 or 2022 that propagated across review sites and became the de facto industry citation.

Two observations make these numbers worth treating skeptically:

First, the 2.90% + $0.20 non-European rate is identical to Stripe’s published US card rate. If Checkout.com’s standard tier matches Stripe’s flat rate exactly, the “transparent interchange++” pitch loses its commercial logic at the SME tier — there is no actual savings versus a flat-rate competitor. That suggests either the cited number is correct and SME-tier Checkout.com offers no rate advantage over Stripe, or the cited number is wrong and the real SME rate is something different.

Second, the rates have not moved in publicly reported sources in over four years, despite Checkout.com’s documented strategic pivots — the 2023 valuation crash from $40B to $9.35B, the $306M 2023 loss, the 230-person layoff in January 2025, the Binance termination, the eBay 2025 win, the return to profitability in 2025. Pricing this stable across this much business volatility is implausible for a private processor whose terms are negotiated per-deal. The static rates likely reflect static citations, not static pricing.

For ISVs evaluating Checkout.com, the practical implication is: assume any third-party rate is a starting reference, not a commitment. The actual rate is whatever your sales conversation produces.

Is Checkout.com Better Than Stripe?

It depends on volume and what you measure. Three frames:

At the SME tier (under $1M annual processing): No clear advantage. The cited 2.90% + $0.20 non-European rate matches Stripe’s published US flat rate exactly. Stripe’s developer ecosystem, documentation, and commercial transparency are categorically better at this tier. ISVs choosing Checkout.com under $1M typically do so for European acquiring strength or specific scheme connections, not for price.

At the mid-market tier ($1M–£50M annual processing): Adyen’s published interchange++ schedule typically wins on transparency and often on price, because Adyen’s commercial discipline forces tighter margins. Checkout.com’s opaque pricing is a structural disadvantage for procurement teams that need to defend a vendor decision. Independent procurement guides identify roughly £50M (about $63M) annual processing as the threshold below which platforms “negotiate with Checkout.com from a weak position.”

At the enterprise tier (£50M+ annual processing): Checkout.com is widely reported to offer better total commercial terms than Stripe or Adyen, with stronger relational service. The Venice conference in October 2025 — attended by 300+ enterprise clients including Netflix, eBay, Pizza Hut, Coinbase, Farfetch, Sony, Sainsbury’s, Delivery Hero, Vinted, and Klarna — produced direct merchant quotes captured by independent analyst Geoffrey Barraclough: “Checkout has caught up with Stripe and Adyen on optimisation, but often offers better commercial terms and superior service.” Sacra’s research estimates the effective take rate at >$1B scale at roughly 0.22%, meaningfully below Stripe’s enterprise pricing.

The crossover sits at the leverage threshold. Below it, you pay the price of opacity. Above it, opacity becomes negotiable.

What Is a Checkout.com Fee? The 25+ Categories

Checkout.com’s minimum-billing-fee legal page enumerates the full fee taxonomy. None of the per-event amounts are public, but the categories themselves disclose what the contract will price.

Per-event fees on every transaction:

- Authorization Fixed (per auth attempt, including declines)

- Gateway Fixed (per API request)

- Scheme Fixed and Scheme Variable (Visa, Mastercard, Amex pass-through)

- Void Fixed (per voided auth)

- Refund Fixed (per refund processed)

Dispute and risk fees:

- Chargeback Fixed

- Representment Fixed (per dispute response submitted)

- Pre-dispute Accepted and Pre-dispute Declined (added August 2023, per-event)

- Retrieval Fixed (added November 2023, per evidence retrieval)

Performance and tokenization fees:

- IA Fixed (Intelligent Acceptance, added August 2023, per transaction the optimization is applied to)

- Network Token Provisioning and Network Token Update (added August 2023, per stored credential touched)

- Account Updater (added August 2023, per card-on-file refreshed)

Settlement and payout fees:

- Payout Confirmed, Payout Returned, Payout Success (added August 2023, per payout cycle)

- Settlement Domestic Fixed and Variable (added November 2023, per settlement instruction)

- Settlement International Fixed and Variable (added November 2023, per cross-border settlement)

- Acceleration Variable Fee (added January 2025, applied to early-funding requests)

The pattern is clear: Checkout.com bills granularly per scheme event, per API request, per dispute action, per token operation, per settlement cycle. Flat-rate competitors collapse most of these into the headline percentage. Interchange++ competitors disclose the breakdown but pin per-event amounts. Checkout.com discloses the categories without the amounts.

For ISVs running platform payments, this taxonomy matters because every category compresses payment margin somewhere your sub-merchants cannot see.

How Much Is the Fee on a $1 Transaction?

Checkout.com does not publish a rate, so this question can only be answered against third-party citations. Using the most-cited industry numbers:

- $1 European card payment at the cited 0.95% + $0.20 lands at roughly $0.21 — an effective rate near 21%.

- $1 non-European card payment at the cited 2.90% + $0.20 lands at roughly $0.23 — an effective rate near 23%.

- $1 currency-converted transaction stacks an additional 1.99% per the cited FX figure, pushing the effective rate above 24%.

Small-ticket transactions are economically destructive at every card processor; the fixed component dominates. Stripe’s $1 transaction costs $0.33 (2.9% + $0.30) — an effective 33% rate. PayPal’s $1 transaction costs $0.34 (2.59% + $0.49 commercial). The cited Checkout.com $0.21–$0.23 is competitive at $1 ticket size — but the cited rates are not Checkout.com’s published rates, so this comparison is a directional estimate, not a quoted commitment.

For ISVs whose sub-merchants sell low-ticket items (digital downloads, subscriptions under $5, micro-transactions), the practical advice is the same regardless of processor: bundle, raise minimums, or move to ACH for invoices. No card processor’s published rate makes $1 sales economically attractive.

Which Payment Gateway Has Fewer Charges?

The answer depends on what “fewer charges” means: line-item count on the invoice, total cost, or transparency of the breakdown.

Fewest line items: Stripe’s flat-rate Standard plan. A US merchant on Stripe’s published 2.9% + $0.30 sees one rate per card transaction, predictable Connect application fees if using a platform model, and minimal scheme pass-throughs. The invoice is the simplest in the industry.

Most transparent breakdown: Adyen’s published interchange++ schedule. Every card-scheme cost is itemized at cost, with Adyen’s processing fee separated explicitly. Mid-market merchants can audit every line. Adyen’s commercial discipline drives sharper rates than Checkout.com’s opaque negotiations at the $10M–$50M tier.

Fewest line items at SME tier: Square or PayPal. Both bundle most fees into the per-transaction percentage. The trade-off is no underlying visibility — you get a clean invoice and you accept whatever margin the processor took.

Lowest total cost at enterprise scale: Checkout.com is reported to win, but only above the leverage threshold. Below £50M annual processing, the 25+ fee categories generate more line items than any competitor with comparable transparency. Above £50M, the negotiated rates compress and the line-item count becomes a feature, not a bug — granular pricing visibility lets large merchants optimize routing, decline retries, and FX corridors against actual unit economics.

Hidden Costs ISVs Should Watch

The published Checkout.com page has none of these. The Merchant Services Agreement has all of them.

Intelligent Acceptance per-transaction fee. Once activated, IA charges a contract-specific fee on every transaction it applies an optimization to. The fee has counted toward the minimum billing threshold since August 2023. G2 reviewer commentary on the IA fee: “Some features that are additionally charged (e.g. intelligent acceptance) should be included in the price.” For ISVs, IA is a pure margin compression item — your sub-merchants see the optimization uplift in their approval rates, but the fee comes out of your platform take.

Rolling reserve at 5–10% for 28 weeks. Standard for high-risk verticals, travel, and merchants with elevated chargeback ratios. Per Checkout.com’s own blog at checkout.com/blog/what-is-a-rolling-reserve, the reserve holds for 28 weeks. The exact percentage and release schedule live only in the MSA. On account termination, both settlement payouts and reserves are held until the MSA-defined release window expires — Checkout.com’s support documentation confirms: “All funds (settlement payouts and cumulative reserves) will be kept by Checkout.com until all reserves are released.”

FX markup applied to chargebacks and refunds. Checkout.com groups currencies into Majors (USD, EUR, GBP, etc.), Minors (~75 emerging-market currencies), and Exotics. The markup percentage per tier is contract-specific. The trap: FX markup applies on refunds and chargebacks, and the original FX fee is not returned when a chargeback hits. ISVs running multi-currency platforms face compounding FX exposure that is difficult to disclose to sub-merchants because the per-tier rates are not public.

Travel-vertical 100% retention demands. A verified Trustpilot review from a Spanish travel business in July 2025 documents the final Checkout.com onboarding terms after a 3+ month approval process: a group guarantee, a UBO personal guarantee, or 100% payment retention for 6 months — plus a minimum monthly processing threshold of €7,500 with no justification provided. The reviewer notes the Checkout.com representative admitted other travel clients had “similar problems” and conditions “might go away after a few months.”

Forced partner-channel implementation. A separate verified Trustpilot review from December 2024 documents a UAE merchant unable to move from test to live without engaging a partner who charged “thousands of dollars for implementation/integration.” Checkout.com’s documentation confirms a two-track structure (Platforms for SaaS, Platforms for PayFac) but publishes no criteria for direct vs. partner-channel access.

Opaque platform/ISV pricing. Checkout.com’s Integrated Platforms product is publicly documented as supporting sub-entity onboarding, payment splitting at auth or capture, fixed/variable/compound commission structures, and instant payouts. No revenue share percentage, sub-merchant volume floor, or platform vs. direct rate differential is published. Compare to Stripe Connect (0.25% application fee published) and Adyen for Platforms (interchange++ pass-through published).

Account Updater and tokenization fees on the platform layer. For ISVs storing cards across a sub-merchant portfolio, every Network Token Provisioning, Network Token Update, and Account Updater event is a separate fee. At platform scale, these add up to a meaningful portion of cost-of-payments that flat-rate competitors fold into the headline.

The £50M Negotiation Threshold

Independent procurement research from Shuttle Global’s enterprise platform comparison guide (February 2026) identifies the leverage threshold at roughly £50M (approximately $63M) annual processing volume. The direct quote: “Adyen publishes Interchange++ pricing, which is transparent and auditable. Checkout.com pricing is custom and enterprise-negotiated (opaque).” Below £50M, platforms “negotiate with Checkout.com from a weak position.” Above £50M, Checkout.com often offers better commercial terms than Adyen’s standardized model.

For ISVs and SaaS platforms aggregating sub-merchant volume, this threshold matters because aggregate platform processing — not individual sub-merchant volume — typically drives the negotiated rate. A platform with 1,000 sub-merchants averaging $50K/year each lands at $50M aggregate; a platform with 200 sub-merchants averaging $300K/year each lands at $60M. The threshold is reachable for mid-sized vertical SaaS platforms with concentrated payment volume — and unreachable for early-stage platforms with long-tail sub-merchant distributions.

The practical procurement implication: if your platform is above the threshold, push for full interchange-plus disclosure, capped IA per-transaction fees, MSA carve-outs on rolling reserve for known low-risk verticals, and explicit FX markup tables per currency tier. If your platform is below the threshold, expect to take a published-tier rate and revisit at scale.

Checkout.com for ISVs and Platforms

Checkout.com’s Integrated Platforms product is the ISV-facing offering. The technical capability set, documented at docs.checkout.com/platforms (last updated December 2025):

- Sub-entity onboarding with pre-built KYC/KYB collection and verification workflows

- Payment splitting at auth or capture — funds can split between the platform and one or more sub-entities at the moment of authorization or at capture, supporting both marketplace and integrated-software models

- Commission structures — fixed-amount, variable-percentage, or compound (multiple commissions per sub-user, per transaction)

- Balance transfers between platform and sub-entities without round-tripping through external bank rails

- Instant payouts and custom payout schedules — sub-entities can receive funds on demand or on platform-defined cadences

- Local-currency payouts in 145+ processing currencies and ~20 settlement currencies

What is not disclosed:

- Revenue share or take-rate model between platform and Checkout.com

- Sub-merchant volume floors for accepting platform-channel sign-ups

- Direct vs. partner-channel pricing differential for the platform itself

- Eligibility criteria for being approved as a direct platform vs. routed through an implementation partner

- Per-sub-merchant fee — whether Checkout.com bills a per-active-sub-merchant fee on top of transaction economics, as Stripe Connect does ($2 per active Express or Custom account per month)

The opacity is the whole story for ISV procurement. Stripe Connect publishes its fee structure on a public page. Adyen for Platforms publishes its model. Checkout.com Integrated Platforms publishes the product capabilities and sends procurement teams to a sales call for the economics. Whether that opacity is acceptable depends on aggregate platform volume, internal procurement discipline, and the strategic value of Checkout.com’s authorization optimization on the specific scheme mix the sub-merchants run.

Pricing Transparency: Checkout.com vs Stripe vs Adyen

Three different commercial postures, three different ISV procurement experiences:

Stripe. Full published flat-rate schedule on stripe.com/pricing. Connect application fees published. Country-specific rates published. Custom interchange-plus available above ~$100K/month aggregate processing, terms negotiated. The ISV procurement experience is “review the public page, model the math, sign the standard agreement.” Custom pricing is an exception, not the default.

Adyen. Full published interchange++ schedule. Card-scheme costs explicit. Adyen’s processing fee separated. Volume-based commercial discounts negotiated, but the underlying interchange++ structure is auditable line-by-line. The ISV procurement experience is “review the public schedule, validate the line items against your card mix, negotiate the processing-fee component.”

Checkout.com. No published rates. Three pricing structures named without amounts (flat, interchange++, charity-free). 25+ fee categories enumerated in legal, none with disclosed per-event amounts. Volume buckets in the sales qualification form from $0–$1M to $5B+. The ISV procurement experience is “submit the qualification form, take the sales call, sign the MSA, see your rates after the contract is signed.”

For ISVs whose business model depends on disclosing payment economics to investors, sub-merchants, or internal finance teams, Checkout.com’s opacity is a structural cost. For ISVs whose business model benefits from negotiated rates that don’t have to be publicly defended, the opacity is a feature.

The 2023–2025 Recovery and What It Means for Pricing

Checkout.com’s commercial trajectory since 2022 is relevant context for pricing negotiations in 2026.

Peak: $40B valuation (January 2022 Series D). Hypergrowth assumptions baked into the price.

Trough: $9.35B internal valuation (2023). Documented $306M loss on the year, up from $38M in 2022. Binance terminated in August 2023 over AML concerns. Crypto exposure cut to ~4% of processing volume. 230-person layoff in January 2025.

Recovery: $12B valuation (September 2025 employee share buyback, per CNBC). EBITDA margins returned positive at >10%. $300B in 2025 processed volume. 63 merchants processing >$1B annually in 2025, up from 39 in 2024. eBay signed as a 2025 partnership win. CEO Guillaume Pousaz publicly repositioned the company as “mainstream enterprise” at the October 2025 Venice conference.

For ISVs negotiating in 2026, the pricing implication is mixed. The recovery means Checkout.com is not desperate for revenue — they have the leverage to walk away from unprofitable deals. The opacity means published-rate stability across this entire business cycle is implausible, so any third-party citation is a directional reference at best. The mainstream-enterprise repositioning means SMB and high-risk vertical applications face stricter underwriting (the documented Travel sector retention demands fit this pattern).

The procurement reality: 2026 Checkout.com pricing is healthier and tighter than 2023 pricing, with less commercial flexibility on the deals they want and stricter terms on the ones they don’t.

How to Negotiate With Checkout.com (ISV Playbook)

For ISVs and platforms with the volume to justify the conversation, six negotiation moves derived from public procurement guidance and verified merchant reports:

1. Lead with aggregate platform volume, not individual sub-merchant volume. Your leverage is the total processing you bring, not the size of any one sub-merchant. Calculate aggregate annual card volume across all sub-merchants and lead the qualification form with that number. The £50M (~$63M) leverage threshold is aggregate, not per-merchant.

2. Demand full interchange++ disclosure, not a blended rate. Anchor on Adyen’s published schedule as the comparison. Refuse the “fully flat-rate” pricing structure unless you specifically want fee predictability over rate optimization. Ask for the scheme-fee schedule, the processor markup, and the fixed-fee schedule as three separate line items.

3. Cap Intelligent Acceptance per-transaction fees explicitly. IA defaults to a contract-specific per-transaction fee with no cap. Negotiate either a per-transaction cap, a percentage cap as a share of optimization uplift, or an explicit opt-in per scheme so you can route around IA on schemes where the uplift doesn’t justify the fee.

4. Negotiate rolling reserve carve-outs for low-risk verticals. The default 5–10% / 28 weeks is calibrated for high-risk and travel. If your sub-merchants are SaaS subscriptions, established e-commerce, or B2B invoicing, push for a reserve floor of 0–2% with a 4–8 week release window, justified by chargeback ratios in your existing portfolio.

5. Get the FX markup table per currency tier in writing. Three tiers (Majors, Minors, Exotics) with contract-specific markups. Get the per-tier basis-point markup explicitly, including the markup applied to refunds and chargebacks. If you process in any Exotic currencies, model the all-in cost across the full transaction lifecycle, not just the auth.

6. Document termination protections for the reserve and settlement holdback. The default MSA terms hold settlement and reserves for the full release window after termination. Negotiate either a shorter release window for low-risk verticals or an early-release provision tied to specific chargeback-ratio thresholds. Without an explicit clause, you cannot exit Checkout.com cleanly.

For platforms below the leverage threshold, the practical move is different: sign the standard agreement, aggregate volume aggressively for 12–18 months, and renegotiate at the £50M threshold with a documented track record of low chargebacks and stable processing. The leverage you build matters more than the rates you start with.

For deeper context on the ISV procurement framework, see what is an ISV in payments, embedded payments vs integrated payments, and the comparison breakdowns at Checkout.com vs Fiserv, Stripe vs Checkout.com, and Adyen vs Checkout.com. Pair this analysis with the Checkout.com ISV review for the operational evaluation alongside the pricing context.