Square vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

The hardware is not what costs. Both companies let your software drive their card readers for no software fee at all, and both charge you the moment you want to be distributed through their marketplace instead. What separates them is a single clause: Clover requires every dollar to move on Fiserv's rails, so it never has to ask where a merchant came from. Square imposes no such rule, so its fee has to test attribution — and its own contract never says how.

Feature Comparison

| Feature | Square | Fiserv |

|---|---|---|

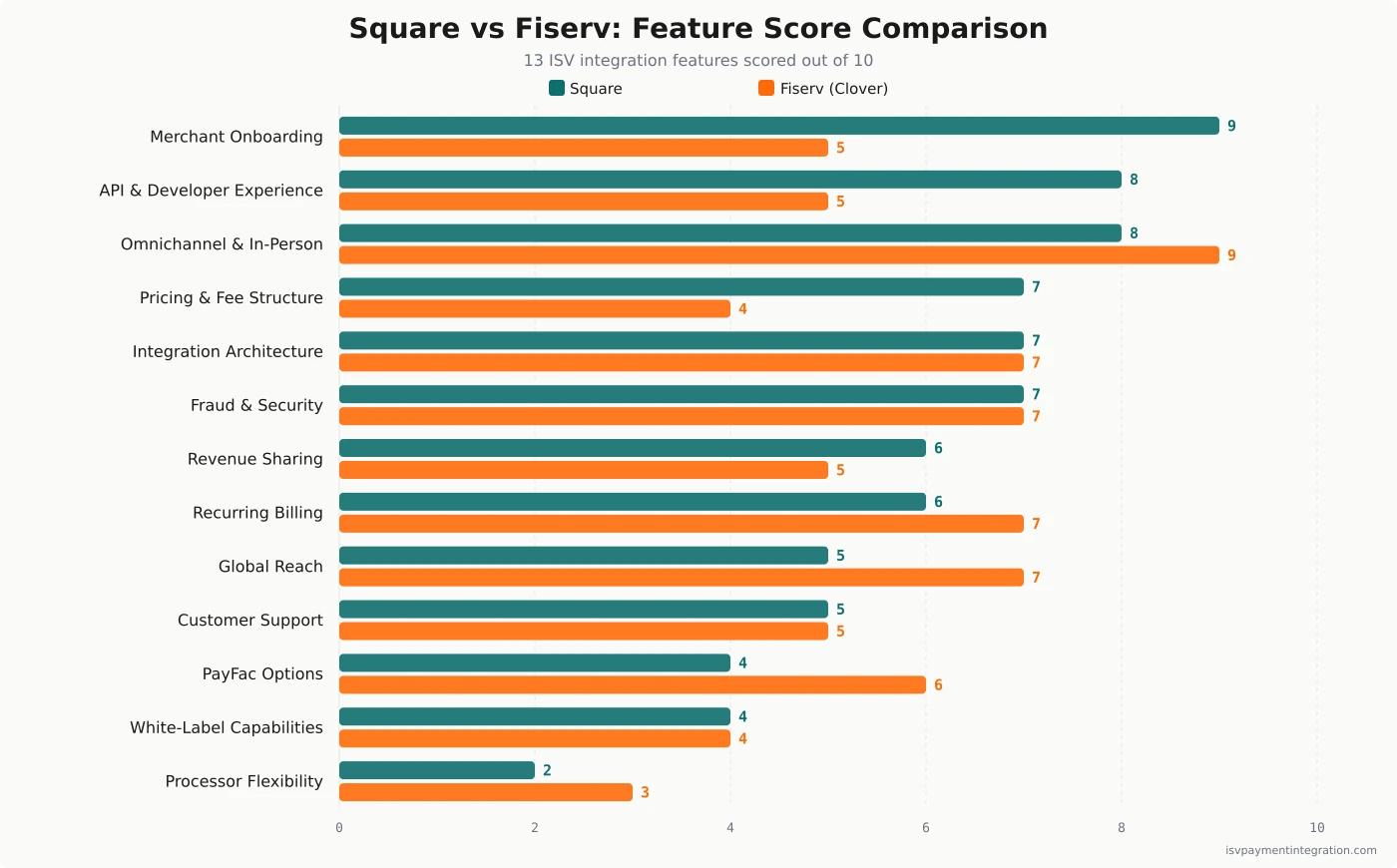

| Merchant Onboarding | 9 | 5 |

| Pricing & Fee Structure | 7 | 4 |

| API & Developer Experience | 8 | 5 |

| Revenue Sharing | 6 | 5 |

| Recurring Billing | 6 | 7 |

| Omnichannel & In-Person Payments | 8 | 9 |

| Integration Architecture | 7 | 7 |

| Global Reach | 5 | 7 |

| PayFac Options | 4 | 6 |

| Fraud & Security | 7 | 7 |

| Customer Support | 5 | 5 |

| White-Label Capabilities | 4 | 4 |

| Processor Flexibility | 2 | 3 |

Get this comparison as a shareable PDF

We'll send the Square vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

Square

Best for platforms with their own funnel, where the in-person surface is a card reader your app drives rather than a register the merchant lives inside. Accept that Square earns the processing margin on your merchants regardless, that its Mobile Payments SDK covers four countries, and that Square is the payment facilitator here — you will not become one.

Best for

Fiserv

Best for vertical software in restaurants, retail and salons where reaching merchants is harder than building the app. Accept that a listed Clover app pays thirty percent of net revenue whoever sourced the merchant, that Clover may amend that figure on notice and add a distribution fee on free installs, and that all billing and processing must stay on Fiserv or Clover rails.

Square vs Fiserv: The Fee Is Not on the Hardware

Almost every comparison of these two is a hardware review. The merchant pays for the hardware, of course. What neither company charges for is the right to point your software at it.

Both let third-party software drive their card-present hardware. Square publishes a Terminal API so that, in its words, “your custom Point of Sale (POS) application can take full advantage of Square Terminal.” Clover publishes semi-integration, “where developers use a powerful SDK to drive a Clover device with their existing software.” Take either route and neither developer agreement claims a share of your software revenue.

The money starts when you stop being a peripheral and ask to be distributed — listed in a marketplace, installed by merchants who found you there, billed through the platform’s own rails. That is where the two contracts diverge, and neither number appears in either company’s ISV pitch.

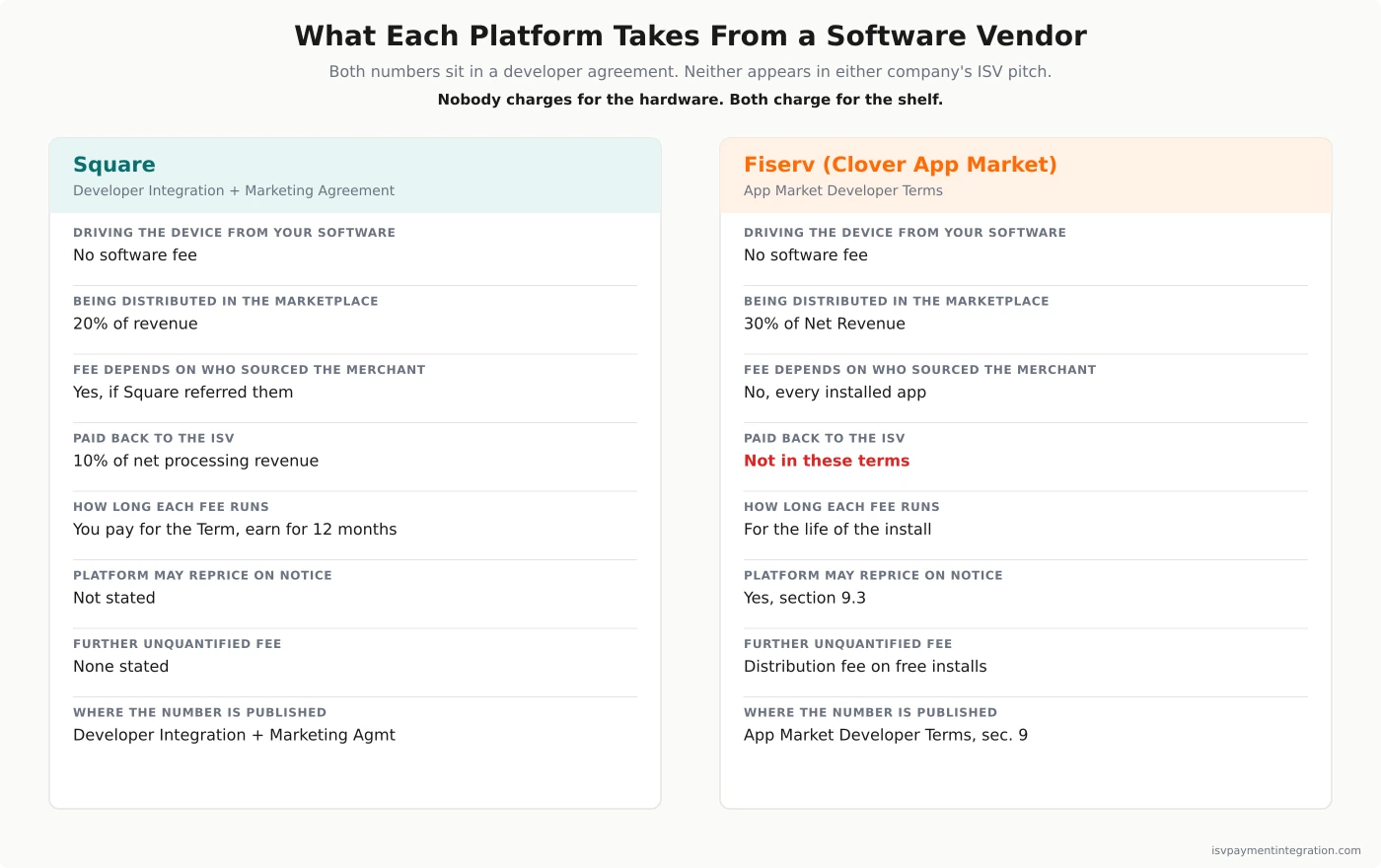

Clover’s App Market Developer Terms, section 9.2: “you will pay to Clover a transaction fee equivalent to thirty percent (30%) of the Net Revenue for each Installed App.” Square’s Developer Integration and Marketing Agreement, section 6(a): “Developer will pay Square … 20% of the revenue … paid by Merchants who become Developer Customers due to referral by Square.”

Twenty against thirty is not the story. The story is that Clover’s fee names no merchant and Square’s fee names a very specific one — and there is a clause elsewhere in Clover’s terms that explains exactly why Clover never has to ask.

Quick Take: Read Section 9.2, Then Read Section 6

Square sells a seller account and rents your software a doorway to the hardware attached to it. Your app never leaves your servers; it authorizes into the merchant’s Square account over OAuth and tells a device on a counter what to charge. Merchant rates are printed on squareup.com — from 2.6% + 15¢ in person down to 2.4% on the top plan, 2.9% + 30¢ for payments taken through the APIs, custom pricing available above $250,000 a year. And Square’s partner page invites you in without ceremony: “Don’t wait on us to get started — dive into building, launch your integration, and reach out once it’s live.”

Fiserv is harder to address, because the company an ISV signs with depends on which door it walked through. Fiserv’s own ISV Partner Program page sells scale and a gateway called CardPointe, promises “Managed PayFac Capabilities,” and — read it twice — never once mentions Clover in its body copy. Which is strange, because Clover is the Fiserv product most software vendors in this comparison are actually evaluating, and Clover has its own developer site, its own contract, and its own published economics.

This page prices the Clover route, because that is the route a vertical SaaS company takes. It is not the only one. CardPointe, Commerce Hub, Managed PayFac and Fiserv’s separate Revenue Share Alliance channel each carry terms this page has not seen, and none of them publishes a rate. Do not read “Fiserv takes 30%” as a statement about Fiserv. It is a statement about the Clover App Market Developer Terms.

Driving the Device Is Free. Both Times.

Start with the thing that costs nothing, because it is the finding most likely to save you money and it is missing from every comparison of these two.

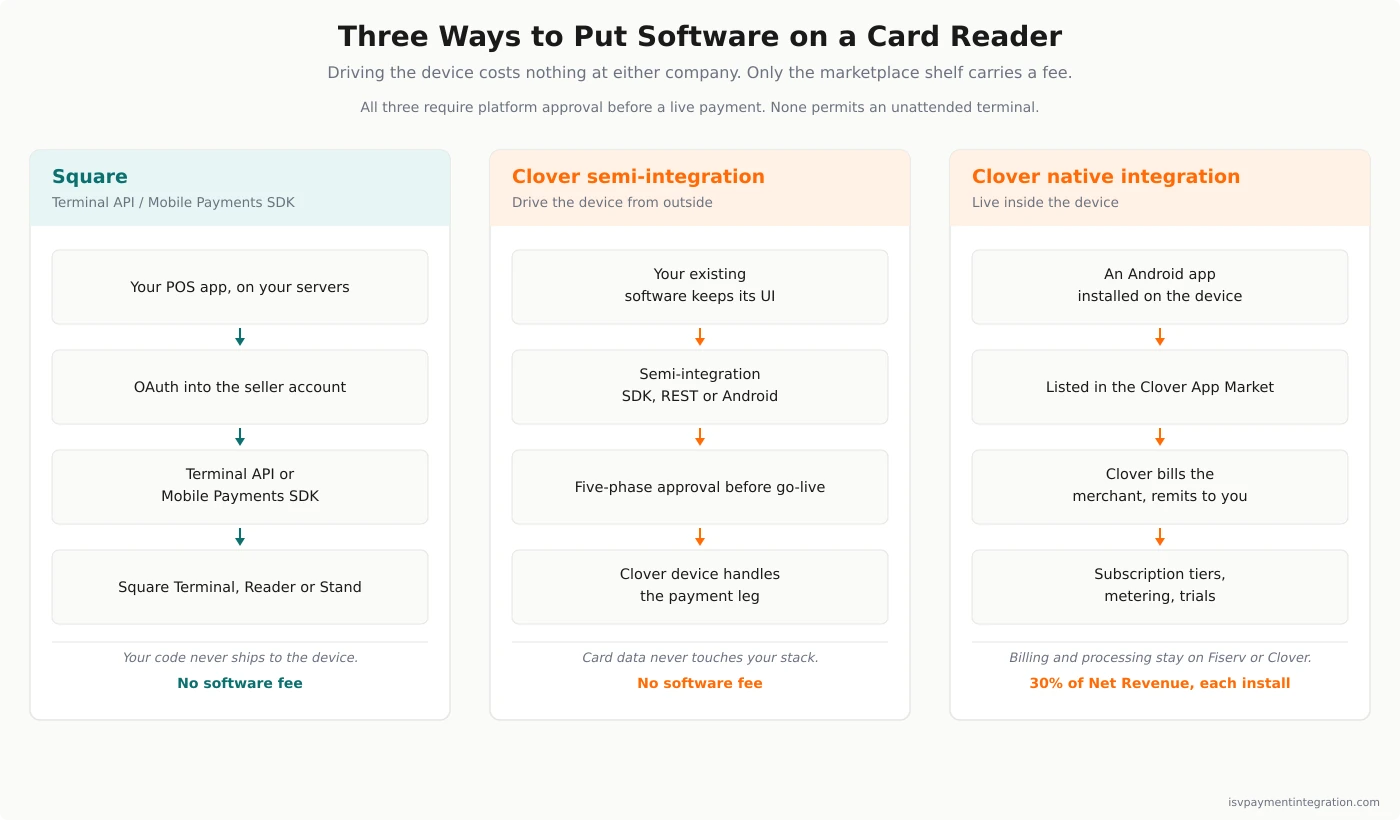

Clover semi-integration: your existing software keeps its own interface and drives a Clover device for the payment leg. Card data never touches your stack. There is no App Market listing, and section 9.2’s transaction fee attaches to “each Installed App” — so with no installed app, there is no fee. You clear a five-phase process (Application, Education, Development, Approval, Maintenance) and then you are a peripheral, not a tenant.

Square Terminal API and the Mobile Payments SDK: the same shape. A custom POS application drives a Square Terminal and receives the result over a webhook. It can customize the Terminal’s idle screen and build on-device screen workflows — confirmation, signature capture, data collection, a QR display. The Mobile Payments SDK pairs Square Readers to your own iOS or Android app, with Tap to Pay on both. Square takes no share of your software revenue for any of it.

So if the question is “what does it cost to put my software on a card reader,” the answer at both companies is nothing, and a great many ISVs should stop reading here and go build the semi-integration.

The bill arrives with distribution. Clover’s native integration — your software as an Android app installed on the device — is the only route into the App Market, and the App Market is where the thirty percent lives. Square’s App Marketplace is the analogous shelf. Neither company charges for the hardware access. Both charge for the shelf.

What the App Market Costs

Clover’s developer documentation states the split plainly — “You receive 70% of the amount that Clover collects from the merchant for an installed app” — and the contract behind it is blunter, and less flattering.

Section 9.1 sets the principle: “the overriding principle of the App Market is that any revenue derived from the Installed Apps (including any subscriptions, in-App features, add-ons, extras or the like) is subject to a Transaction Fee.” Section 9.2 sets that fee at thirty percent of Net Revenue — a defined term the operative clause does not define where it is used, and which the docs page glosses, non-contractually, as “the amount that Clover collects.” Those are not the same quantity, and where a marketing gloss and a contract disagree, the contract wins.

Three more clauses deserve pricing before you build:

- 9.2(2) reserves Clover’s right to charge a distribution fee on apps merchants install for free. It is not quantified anywhere. Your total take rate therefore has no published ceiling.

- 9.3 reserves Clover’s right to “amend the amount of the Transaction Fee … upon prior written notice.” Thirty percent is today’s number, not a durable one.

- 20.2: “Clover may at any time terminate the Contract for any reason or no specific reason upon notice to you.” On termination, published apps come down “at the discretion and timing of Clover.”

Seventy-thirty is an ordinary app-store split. An ordinary app-store split with an unquantified second fee, a unilateral repricing right, and termination for no reason is a different instrument, and the version of it you sign will depend on your region — the agreement is partitioned into separate parts for the United States, Europe and Canada.

What the Marketplace Costs at Square

Square’s section 6 is titled Revenue Sharing; Taxes and Payments, and unlike Clover’s section 9 it runs in both directions.

Subsection (a) costs you: twenty percent of revenue from merchants who became your customers because Square referred them — paid by you, or retained by Square if you bill through its Subscriptions API. Subsection (b) pays you: “Square will pay to Developer a 10% referral fee based upon aggregate Payment Processing Adjusted Revenue … for the first twelve (12) months of card processing volume of Developer Customers who become new Merchants due to referral by Developer using their unique referral link.”

That is a payments revenue share, with a number on it, in a public contract, from the company routinely described as offering ISVs none. It is also narrower than it sounds, and an honest page says how:

- It is a new-logo bounty, not a share of your book: only new merchants, only through a unique referral link, only their first twelve months.

- “Payment Processing Adjusted Revenue” is what Square keeps after interchange, network fees, assessments, chargebacks, refunds and taxes. A slice of a slice.

- The fee you pay has no expiry and the fee you receive does. 6(a) runs for the Term against every product a referred merchant ever buys from you. 6(b) dies at month twelve.

- And 6(a) never says how a referral is proved. Section 6(b) specifies a “unique referral link”; 6(a) specifies nothing. A drafter who knew how to define attribution declined to, one subsection earlier. Get it defined in writing before you sign, because Square could reasonably argue that a merchant who found you on its Marketplace was referred by Square.

None of which appears on the App Partner Program page, which advertises only “Profit share eligibility,” with no rate, under the heading “Apply to get even more.”

Why Clover Doesn’t Need to Ask Where the Merchant Came From

Here is the clause that explains the whole comparison, and it is not a fee clause at all. From Clover’s monetization guide:

“All app fees, merchant app usage payments, and merchant-customer payment processing must be implemented within the Fiserv or Clover platforms.”

Every dollar your Clover app earns moves on Clover’s rails. Clover bills the merchant, collects, handles refunds and remits your share. You cannot invoice your own Clover merchant outside Clover, and you cannot process their customers’ cards outside Fiserv.

Once you own the rail, attribution becomes unnecessary. Clover does not have to know whether the merchant came from its four-thousand-person sales force or from your outbound team three years before Clover existed, because the money passes through Clover’s hands either way. A flat thirty percent on each installed app is the coherent design for a mandatory rail.

Square’s agreement contains no such rule. It does not require you to bill through Square, which is why it cannot simply take a flat cut — it has to identify which merchants it earned a cut on. Hence the words “due to referral by Square,” and hence the awkward silence about how that is measured.

So the difference is not that one company is open and the other closed. It is that one owns the rail and prices accordingly, and the other doesn’t and has to argue about provenance. Which of those you prefer depends on something dull: whether you would rather have a fee you can predict, or a fee you can dispute.

And the honest Clover counter deserves stating, because it is strong. If reaching merchants is the hard part of your business, thirty percent of revenue from a merchant you would never have met beats a hundred percent of revenue from a merchant who does not exist. Clover’s rail is also a distribution channel, a billing department and a collections department you did not have to build. That is what the thirty percent buys, and for a lot of vertical SaaS it is cheap.

One more line an ISV should not skip: Square earns the merchant’s processing spread — 2.6% + 15¢ in person — whether or not it ever touches your software revenue. Neither company is working for free, and the software take rate this page is about is, for most platforms, the smaller of the two numbers on the invoice.

Neither of Them Will Let You Run It Overnight

If your product is a self-service kiosk, read this before you buy hardware, because the boundary is not where most people assume.

Both companies permit customer-operated checkout. Square sells a first-party self-serve Kiosk that exists to “let customers build their own orders” — “Put the customer in charge,” says the page. Clover certifies its devices for semi-attended environments, which is its term for a terminal a customer operates.

What both prohibit is unattended. Square’s Mobile Payments SDK documentation: “Using the Mobile Payments SDK to implement payment solutions in unattended terminals or unattended kiosks is strictly prohibited. For example, an outdoor vending machine is unattended because it can be accessed by users outside of normal business hours and might not be in the line of sight of a seller or worker.” Square defines attended narrowly, and all three conditions must hold: the device cannot be physically reached by buyers outside business hours; it must be in the line of sight of the seller or a worker; and staff must be trained and available to help.

Clover’s semi-integration documentation puts it more flatly: its devices are “only certified for use in attended and semi-attended environments, as defined in the PCI PTS POI Evaluation FAQ,” and integrations that use a Clover device in an unattended environment are “neither allowed and nor approved.”

The practical line, then, runs through business hours and line of sight, not through who taps the screen. A self-order kiosk in a staffed restaurant is fine at both. A pay station in an unstaffed lobby at 2 a.m. is fine at neither, and no amount of SDK cleverness changes that. If genuinely unattended acceptance is your product, note that Fiserv promotes a guide to unattended payments whose accompanying artwork is a CardPointe unattended solution — not a Clover device. The certification that blocks you on Clover does not necessarily block you at Fiserv.

The Six Rows an ISV Actually Needs

Laid out flat, with the marketing removed. Read the third row twice.

| What an ISV needs | Square | Fiserv (Clover App Market) |

|---|---|---|

| Cost to drive the card reader from your software | Nothing (Terminal API, Mobile Payments SDK) | Nothing (semi-integration SDK) |

| Cost to be distributed through the marketplace | 20% of revenue, Square-referred merchants only | 30% of Net Revenue, each installed app |

| Does the fee depend on who sourced the merchant? | Yes — “due to referral by Square,” undefined | No — every installed app |

| Paid back to the ISV | 10% of net processing revenue, first 12 months | Not published in these terms |

| Platform may change the rate on notice | Not stated | Yes, section 9.3, plus an unquantified distribution fee |

| Sponsor or acquiring relationship named | JPMorgan Chase and/or Bancorp, in the Commercial Entity Agreement | CardConnect is a registered ISO of Citizens, KeyBank, Pathward, PNC and Wells Fargo |

Two cautions on that table. Clover’s “Net Revenue” and Square’s “the revenue” are different defined terms and are not strictly comparable on their face — a rate comparison across two contracts is an estimate, not an audit. And row four says “not published in these terms” rather than “not published,” because Fiserv runs partner channels — the Revenue Share Alliance, Clover Connect — whose economics live in instruments this page has not read.

Both Companies Reported the Same Quarter

They filed for the identical period, the three months ended March 31, 2026. Compare only the lines that match.

At the segment level: Block reported Square segment net revenue of $2.11 billion, up 14%, on Square gross payment volume up 13%, “driven primarily by strength in Food and Beverage sellers.” Fiserv’s comparable segment, Merchant Solutions, was flat at $2.37 billion, and the Processing sub-line inside it fell 8.7%. Fiserv remains the far larger acquirer; in the quarter, only one of these two merchant businesses grew.

At the company level the two are not comparable, and this page will not pretend otherwise: Block’s consolidated operating loss of $172.0 million reflects a business that is mostly Cash App, and Fiserv’s consolidated revenue of $5.03 billion — down 2.0%, with operating income down 34.2% — reflects a business that is mostly not merchants.

One line is worth quoting exactly, because it is easy to over-read: “Square generated gross profit of $981.5 million in the first quarter of 2026, up 9% year over year, driven by financial solutions, most notably Square Loans.” Gross profit, not segment profit; and lending is what Block credits for the growth, while GPV grew 13% on its own. Square is not a lending company that happens to process cards. But its fastest-growing profit line in the quarter was not processing.

Fiserv, for its part, is being sued. Two putative securities class actions, both unadjudicated, allege that statements about Clover’s reported growth were false or misleading; Fiserv describes them in its own Form 10-Q and says it intends to defend them vigorously. Nothing has been proven, and this page takes no view on the merits. It notes only that the platform whose section 9.3 lets it reprice your app on notice is the same platform whose growth those complaints concern, and that the company changed chief executives in June 2026 and lost its president three weeks after that. Our Fiserv review carries the procedural detail.

Which Contract Fits Your Product

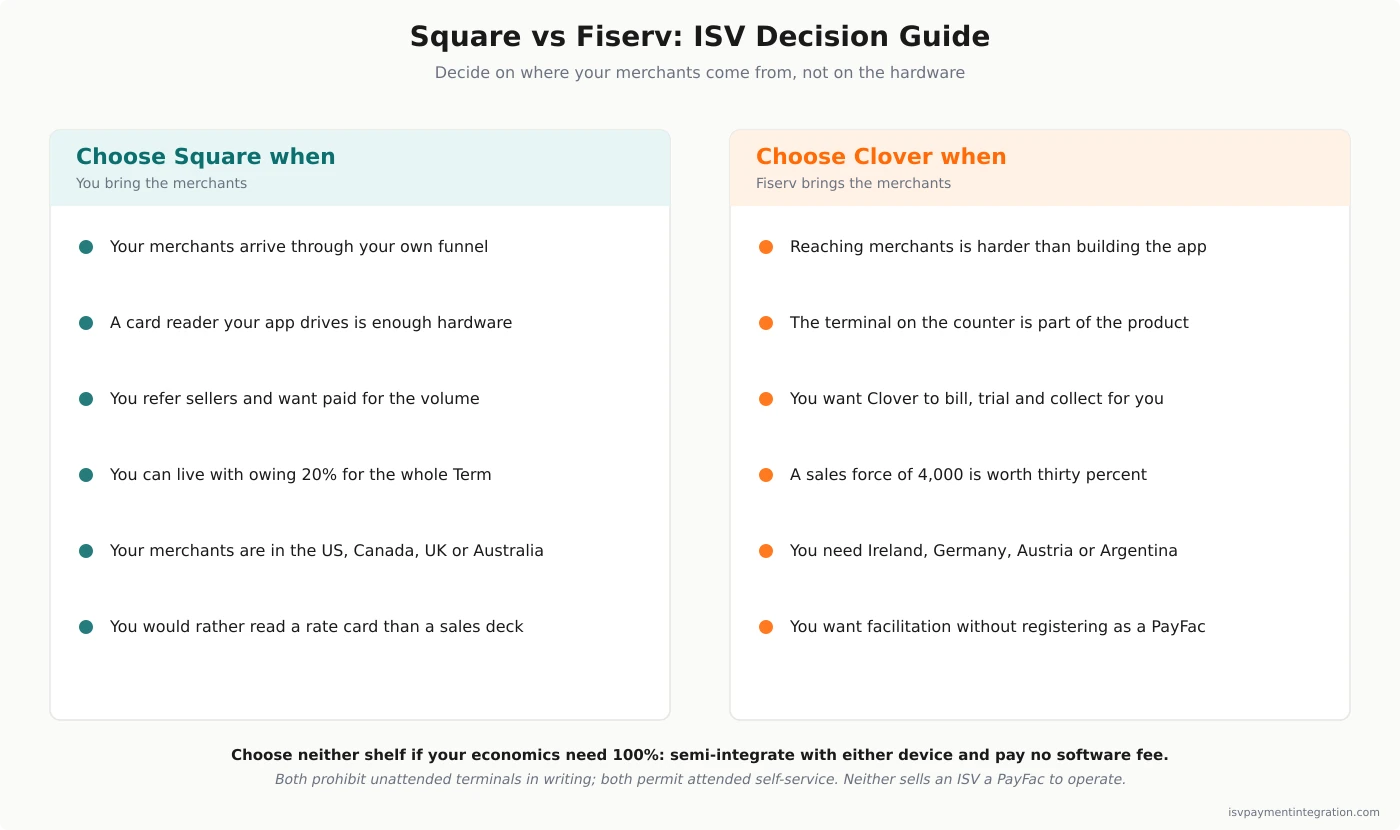

Take Square when merchants come from your own funnel. The twenty percent never triggers, and the ten percent referral fee runs in your favour for a year on every seller you send. Accept that the fee you owe outlives the fee you earn, that the Mobile Payments SDK covers four countries, that Square reviews your application signature before you take a live payment, and that Square is the payment facilitator — you are not going to become one here. If facilitation is the goal, start with what a PayFac actually is; neither company on this page sells an ISV one it can operate, though Fiserv will run one on your behalf.

Take Clover when reaching merchants is the hard part and building the app is the easy part. A native app puts your software on a device already on the counter, in front of a sales force Clover’s documentation puts at over 4,000, with billing, trials, proration and collections handled for you. Thirty percent is the price; it applies whoever sourced the merchant; section 9.3 says the number can move; and there is a distribution fee with no published figure. Decide whether the distribution is worth it before you write the Android app, not after.

Take neither shelf if your economics only work at a hundred percent. Semi-integrate with either device, keep your billing, and pay nothing for the privilege — accepting that you will have to find every merchant yourself. And if your roadmap is genuinely unattended, or you must own the merchant relationship and set the rate, that is PayFac-as-a-service territory and a different comparison. If you are weighing Square against a pure gateway, Square vs Braintree covers that axis; Stripe vs Fiserv is the version of this page where one side publishes a platform rate on its website.

Square vs Fiserv: ISV Decision Guide

The scorecard above summarises capability. Fit is decided by one sentence in one contract, and for these two companies that sentence is about the rail. Clover owns the rail your app’s money moves on, and prices every install accordingly. Square does not own it, and so has to argue about who found the merchant.

Before you commit engineering time, price the take rate against your own channel mix. Our embedded payments revenue calculator handles the payment volume; the software split you now have the numbers to model yourself.

Frequently Asked Questions

Does Square offer ISVs a revenue share?

Yes — but not with a plain API key, which is why so many write-ups say it doesn’t. Sign Square’s Developer Integration and Marketing Agreement and section 6(b) commits Square to pay “a 10% referral fee based upon aggregate Payment Processing Adjusted Revenue … for the first twelve (12) months of card processing volume” of merchants you refer through a unique link. Read the qualifiers: new merchants only, twelve months only, and calculated on what Square keeps after interchange, network fees, chargebacks and taxes. Section 6(a) of the same agreement takes 20% of your software revenue from merchants Square referred to you, for the whole Term. One of those two numbers expires and the other does not. The App Partner Program page advertises only “Profit share eligibility,” with no rate.

How much does Clover take from an app developer?

Thirty percent of Net Revenue, on each installed app, per section 9.2 of the Clover App Market Developer Terms — which is why the developer docs say “You receive 70% of the amount that Clover collects.” Two things that split hides: section 9.2(2) reserves a separate, unquantified distribution fee on apps installed for free, and section 9.3 lets Clover amend the transaction fee on prior written notice. The published rate has no published ceiling.

Can I put software on a Clover or Square device without paying a revenue share?

Yes, on both, and this is the least-known fact in this comparison. Clover’s semi-integration lets your existing software drive a Clover device through an SDK; there is no App Market listing and no installed app, and section 9.2’s fee attaches to “each Installed App.” Square’s Terminal API and Mobile Payments SDK do the same for Square hardware. Neither company charges a software revenue share for the hardware access itself. What you give up is distribution: no marketplace listing, no platform billing, and every merchant is one you found.

Can I use Square or Clover for a self-service kiosk?

For an attended one, yes — Square sells its own self-serve Kiosk, and Clover certifies devices for “semi-attended” use. For an unattended one, neither. Square’s Mobile Payments SDK docs state that using it in “unattended terminals or unattended kiosks is strictly prohibited”, and require the device be within a worker’s line of sight during business hours. Clover’s docs state its devices are “only certified for use in attended and semi-attended environments” and that unattended integrations are “neither allowed and nor approved.” The test is business hours and line of sight, not whether the customer taps the screen. For genuinely unattended acceptance inside Fiserv, ask about the CardPointe path rather than Clover.

Which one is cheaper for an ISV?

It depends on how you distribute, not on the headline rate. Semi-integrate with either platform and the software fee is zero at both. List in the Clover App Market and you pay thirty percent of net revenue on every install, whoever found the merchant. List with Square under its developer agreement and you pay twenty percent, but only on merchants Square referred — and Square pays you back ten percent of net processing revenue on merchants you refer, for a year. Also remember what neither fee covers: Square earns the merchant’s processing spread of 2.6% + 15¢ in person regardless, and Fiserv earns its own negotiated spread. Model your channel mix before treating any of these numbers as a price.

Does Fiserv publish its processing rates?

Not for processing. Its ISV Partner Program page sells scale and capability without quoting a rate, and CardConnect publishes no merchant rate sheet — pricing there is interchange-plus and negotiated. But it is wrong to say Fiserv publishes nothing an ISV can plan against: Clover’s developer agreement states the exact split Fiserv takes from software sold in its App Market. For a vertical SaaS company that number is more decision-relevant than a processing rate, because it applies to your subscription line rather than to your merchant’s cost of acceptance. It is also not the whole picture — Fiserv’s Revenue Share Alliance and Clover Connect channels carry economics that appear in neither of the two contracts this page reads.