Square vs Braintree

A feature-by-feature comparison for ISVs integrating payments.

Square and Braintree are both payment aggregators, not PayFac platforms — Square owns the in-person commerce experience, Braintree (now PayPal Enterprise Payments) owns developer-first online checkout. Neither hands an ISV true revenue share or white-label control, and that shapes the whole decision.

Feature Comparison

| Feature | Square | Braintree |

|---|---|---|

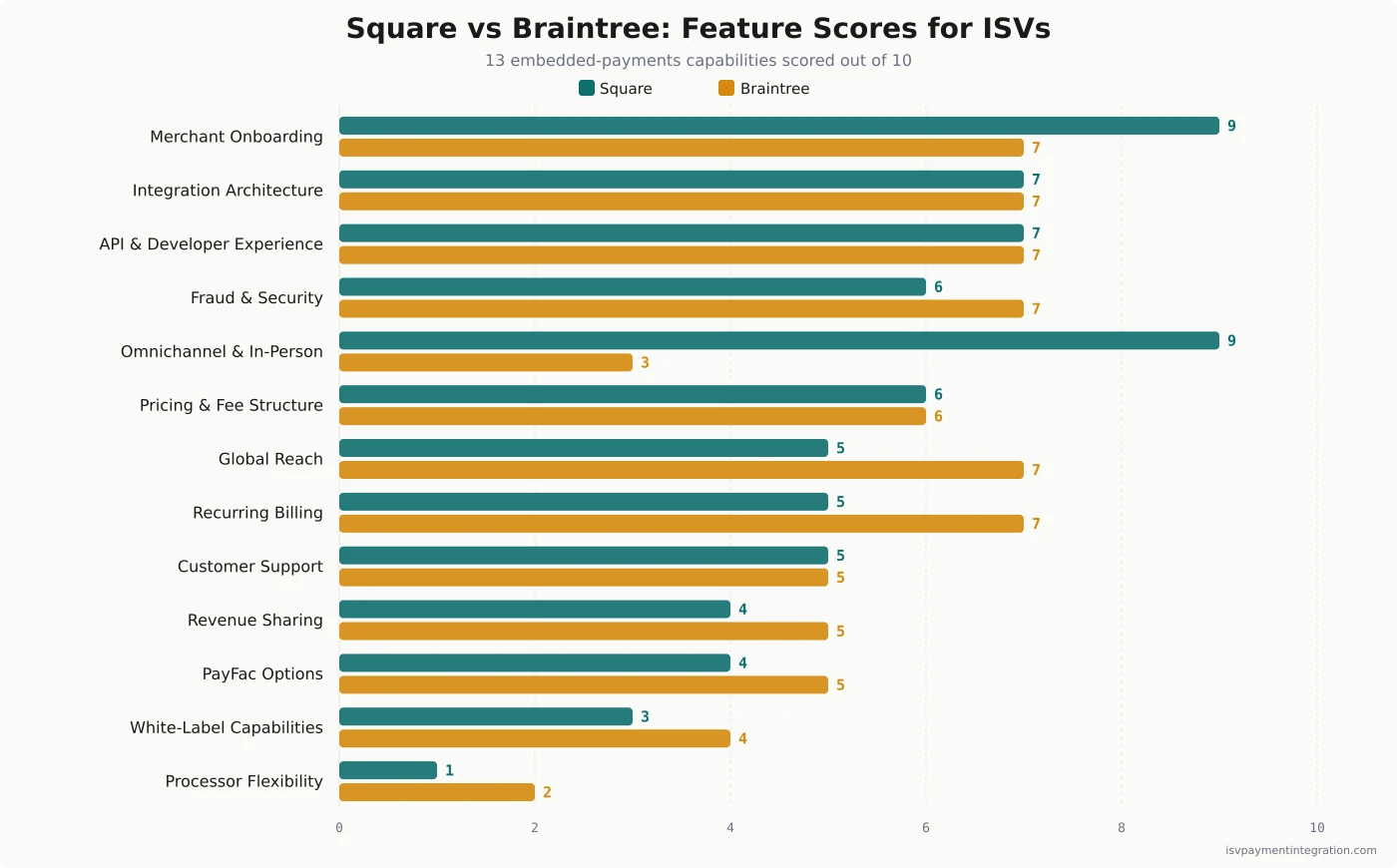

| Integration Architecture | 7 | 7 |

| API & Developer Experience | 7 | 7 |

| White-Label Capabilities | 3 | 4 |

| Processor Flexibility | 1 | 2 |

| Pricing & Fee Structure | 6 | 6 |

| Omnichannel & In-Person Payments | 9 | 3 |

| Fraud & Security | 6 | 7 |

| Revenue Sharing | 4 | 5 |

| Merchant Onboarding | 9 | 7 |

| Global Reach | 5 | 7 |

| Recurring Billing | 5 | 7 |

| Customer Support | 5 | 5 |

| PayFac Options | 4 | 5 |

Get this comparison as a shareable PDF

We'll send the Square vs Braintree breakdown to your inbox — ready to share with your team.

Best for

Square

Best for ISVs serving merchants with both physical and online sales who want unmatched POS hardware, instant onboarding, and a packaged commerce platform — accepting that merchants stay Square's customers.

Best for

Braintree

Best for online and enterprise ISVs that want developer-first APIs, native PayPal and Venmo acceptance, and global reach — accepting that Braintree's card-present product is an extension of an ecommerce account rather than a POS ecosystem, and that its marketplace split-payment product is sales-gated rather than self-serve.

Square and Braintree get compared constantly, but for an ISV the honest starting point is that they are both payment aggregators, not payment-facilitator platforms — and in 2026 they are pulling in opposite directions. Square is doubling down on packaged, in-person-plus-online commerce for small businesses. Braintree, now folded into PayPal Enterprise Payments, is chasing large online enterprises, and the marketplace product an ISV would use is still live but sales-gated. Neither hands a software company the white-label control of a true PayFac, so the real question is which aggregator’s shape fits your product — and whether you should be looking at a third option entirely.

Square vs Braintree: The Core Difference for ISVs

Square is a commerce platform you build alongside. It owns payments, point of sale, hardware, and a stack of business tools, and an ISV plugs into that ecosystem through Square’s APIs. Its center of gravity is the physical world — a café, a salon, a pop-up — plus the online storefront attached to it. For a software company whose merchants ring up sales in person, Square’s hardware and instant onboarding are hard to beat.

Braintree is an online payment gateway you embed in a checkout. It is developer-first, owned by PayPal, and built for card-not-present commerce — subscriptions, e-commerce, in-app purchases. Its signature advantage is native PayPal and Venmo acceptance inside a single integration, plus a decade-old SDK ecosystem. Its center of gravity is the browser and the app, not the counter.

The shared limitation matters more than either strength. Both are aggregators: the merchant is the processor’s customer, not the ISV’s. Square holds the master merchant account and onboards your sellers as sub-merchants under its umbrella; Braintree sits inside PayPal’s ecosystem. Neither gives an ISV the margin spread, underwriting control, or full white-label experience that a PayFac-as-a-service provider does. That is the lens for everything below.

What Square Is for ISVs in 2026

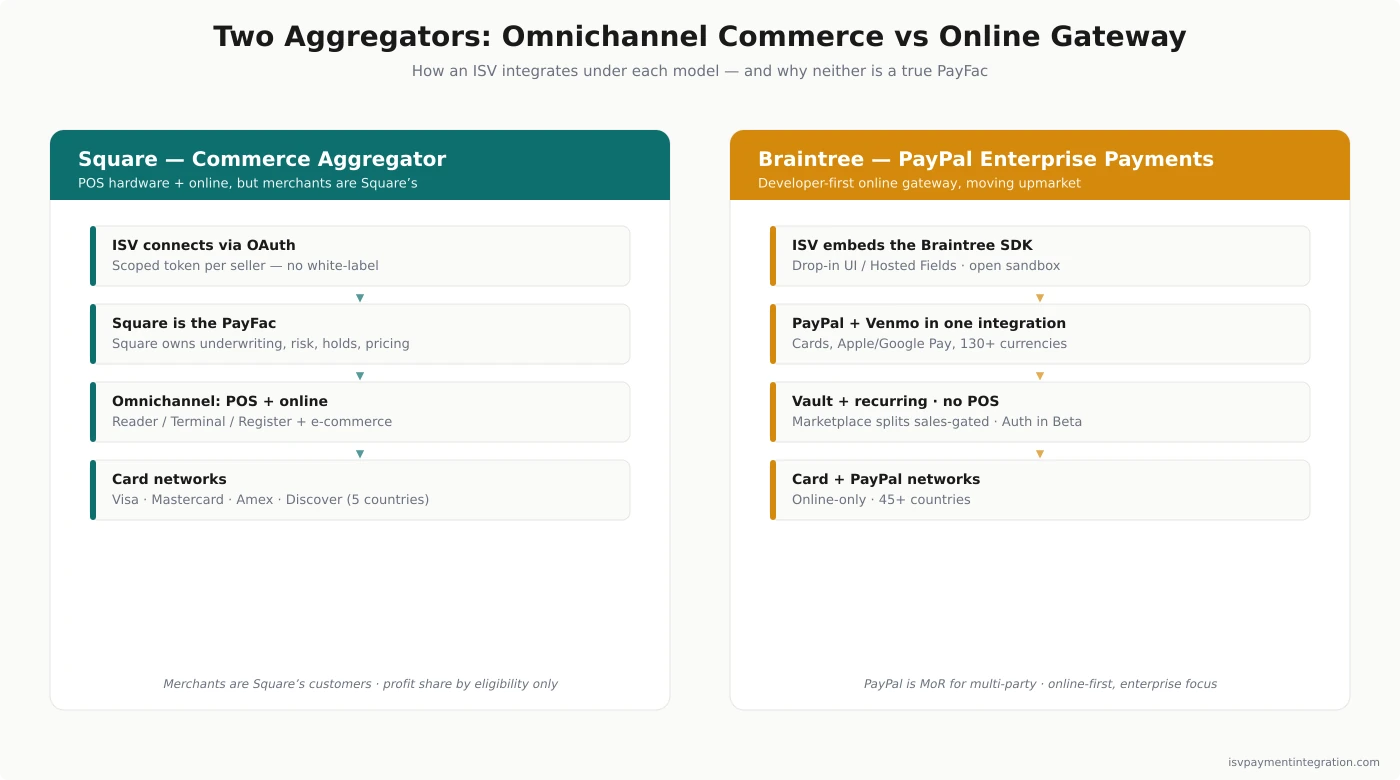

Square is a registered payment facilitator owned by Block, Inc. (now trading as XYZ rather than SQ). When an ISV builds on Square, sellers connect through OAuth and the ISV receives a token scoped to that seller’s account — the software can take payments and read data on the merchant’s behalf, but the merchant remains Square’s customer. Square owns underwriting, risk, holds, and the pricing the merchant pays. Square processed roughly $250 billion in gross payment volume in 2025, so the seller base an ISV can reach is large.

The developer platform is genuinely capable: 20-plus APIs and 100-plus endpoints spanning Payments, Checkout, Orders, the Web Payments SDK, the Mobile Payments SDK (now generally available), and the Terminal API, with backend SDKs in Python, Node, Ruby, PHP, Java, and .NET. Partner tracks exist — App Partner, Solutions Partner, Referral Partner — but there is no named “Square for Platforms” program that pays an ISV a share of transaction revenue. Building on Square gives you reach and hardware, not a payments revenue line.

The real edge is omnichannel hardware: Square Reader, Stand, Terminal, Register, and Kiosk form a polished, supported lineup no online-first competitor matches, all reachable through the Terminal API. The real limit is ownership — there is no white-label, Square branding appears throughout, and because Square controls each sub-merchant account, an abrupt hold or termination by Square hits the ISV’s product for that merchant with no contractual lever. The Square review digs into the day-to-day experience.

What Braintree Is for ISVs in 2026

Braintree has been a PayPal company since 2013, and in 2025 PayPal rebranded it as PayPal Enterprise Payments and folded it into the “PayPal Open” platform — the landing page now reads “Braintree is now PayPal Enterprise Payments.” It remains a developer-first gateway with a strong track record: Uber, Spotify, and Adobe are current named clients. Its defining feature for an ISV is acceptance — PayPal and Venmo in one integration, alongside cards, Apple Pay, and Google Pay, across 130-plus currencies.

Two 2026 facts reshape the ISV picture. First, Braintree’s strategy shifted: PayPal’s CFO confirmed in December 2024 that Braintree is moving from chasing maximum processing volume to a value-over-volume model — fewer thin-margin deals, more higher-margin enterprise relationships. It is moving upmarket, away from the long tail of small platforms. Second, and more concrete, Braintree Marketplace is no longer a product you can simply sign up for. The sub-merchant split-payment product an ISV would use for multi-party flows still has live documentation, but PayPal now gates it behind its sales team — the overview page tells new merchants twice to “contact our Sales team,” and the product carries hard limits: US-domiciled master and sub-merchants only, and no compatibility with PayPal, recurring billing, or most shopping carts. The other multi-party mechanism, Braintree Auth, is an OAuth connect flow that PayPal’s own documentation still labels Beta. Neither is at parity with Stripe Connect, and neither is something you can adopt without a sales conversation.

What remains is a strong single-merchant and enterprise toolkit: Drop-in UI and Hosted Fields for low-PCI integration, the Vault for tokenized recurring billing, mobile SDKs, a no-obligation sandbox, Fastlane accelerated checkout, and payment orchestration. It is firmly online-first — there is no Braintree POS hardware. For an ISV, Braintree is a checkout and subscription engine with PayPal’s network attached, not a platform-payments product. See the Braintree review for the full breakdown.

Integration and Developer Experience

Both score 7 of 10 here, and both are legitimately good — this is a tie on quality with a difference in philosophy. Braintree leans full-control: multi-language SDKs, a GraphQL API, Drop-in UI or granular Hosted Fields, and an open sandbox you can prototype in before applying for production. For a team that wants to hand-build a checkout and keep card data off its servers at SAQ-A scope, Braintree’s decade of SDK maturity shows.

Square leans packaged: the same breadth of backend SDKs, plus a free website builder and low-code tools that get a non-technical merchant live fast. The trade is depth versus speed — Square optimizes for a seller activating in minutes, Braintree for a developer customizing every field. An ISV should pick based on who does the integrating: an engineering-led platform will feel at home in Braintree, while an ISV that wants merchants self-serving onto payments will lean Square.

Omnichannel vs Online-Only

This is the widest gap on the scorecard and often the deciding factor: Square scores 9 to Braintree’s 3 on in-person and omnichannel payments. Square unifies in-person and online sales on one dashboard, syncing inventory and customer data across the counter and the website, backed by its hardware lineup. For any ISV whose merchants take cards in the physical world — restaurants, salons, retail, services — that omnichannel coverage is decisive.

Braintree is not online-only — that claim is several years stale — but it does not play at Square’s level here either. It ships a card-present product on Verifone terminals with EMV, contactless, magstripe and P2PE, and PayPal documents it as a way to “extend an existing Braintree ecommerce setup to your physical stores.” The web account is the noun; the terminal is the extension. Square inverts that: the counter is the product, and the dashboard follows it. If your merchants only ever transact online, this gap is irrelevant and Braintree’s developer depth wins; the moment a merchant runs their day on the device, Square is the one of the two built for it.

Pricing and Revenue Economics for ISVs

Both publish clear rates, and both updated them recently. Square’s October 2025 overhaul set in-person card-present pricing at 2.6% + 15¢ on the free plan (down to 2.5% and 2.4% on the $49 and $149 monthly plans), online at 2.9% + 30¢ on paid plans (3.3% + 30¢ free), and keyed transactions at 3.5% + 15¢, with custom pricing above $250,000 a year. Braintree, per its official schedule last updated in May 2026, charges 2.89% + $0.29 for cards, 3.49% + $0.49 for Venmo, 0.75% (capped at $5) for ACH, with interchange-plus available on custom deals generally above $100,000 a month. No monthly or gateway fee on either. Model the all-in processing fees, though, not the headline rate — both pass through extras like premium-software fees, instant-transfer fees, and add-on costs for advanced fraud and chargeback protection.

But the number that matters to an ISV is not the merchant rate — it is your cut, and here both are vague on the marketing pages and specific in the contracts. Square pays no share of transaction revenue under standard API access; its App Partner Program does list “profit share eligibility” as a benefit, described only as “sharing in profit generated through the app partnership,” with no published rate, no threshold, and eligibility decided case by case. Braintree’s sub-merchant split product is sales-gated rather than self-serve, leaving the Beta-labeled Braintree Auth as the open path. So if your business model depends on earning the spread between what merchants pay and what the processor charges — the core of embedded payments economics — neither Square nor Braintree hands it to you on published terms. Compare the detail in the Square pricing and Braintree pricing breakdowns.

PayFac and Revenue Sharing: The ISV Limitation

This section is the one most comparison articles skip, and it is the most important for a software company. A true payment facilitator lets an ISV own the merchant relationship, set sub-merchant pricing, and keep the markup as payments revenue. Neither Square nor Braintree does that for ISVs. Square is the PayFac — your merchants are its sub-merchants, and you ride along through the API without setting their rates. That is not the same as earning nothing: Square’s Developer Integration and Marketing Agreement pays a 10% referral fee on net processing revenue for the first twelve months of merchants you refer. Braintree routes multi-party flows through PayPal as merchant of record; Braintree Marketplace is live and sales-gated, not discontinued, and PayPal’s newer Multiparty route is approval-gated too.

That is not a knock on either product for what they are; it is a scoping warning. If your goal is to add a convenience payment option to existing software, both are fine aggregators. If your goal is to build payments into a revenue engine — with your brand on the experience and margin on every transaction — you want PayFac-as-a-Service, not an aggregator. That is the lane occupied by Finix, Tilled, and partner-model providers like Xplor Pay, and it is worth weighing before you commit to Square or Braintree. The same trade-off shows up in our WePay vs Tilled comparison, where the independent PFaaS is the one actually courting ISVs.

Global Reach, Recurring Billing, and Fraud

Where Braintree pulls ahead is reach and subscriptions. It operates across 45-plus countries and 130-plus currencies on PayPal’s network (Braintree scores 7 to Square’s 5 on global reach), and its Vault and subscription tooling are built for recurring billing (7 to 5), making it the stronger fit for SaaS and membership models with international customers. Native PayPal and Venmo acceptance in the same integration also lifts checkout conversion for US consumer audiences, where Venmo in particular skews younger — a payment-method edge Square cannot match online. Square processes in only a handful of countries — the US, Canada, UK, Australia, and Japan — and its recurring tools are closer to invoicing than full subscription management.

On fraud and security the two are close, with Braintree slightly ahead (7 to 6). Both are Level 1 PCI DSS compliant. Braintree leans on PayPal’s network data plus add-ons like Chargeback Protection (from 0.40%) and Fraud Protection; Square bundles fraud detection and offers chargeback protection as an add-on. Neither is a differentiator on its own, but for a cross-border, subscription-heavy ISV, Braintree’s combination of currencies, vaulting, and PayPal-grade risk data is the more complete package.

Where Each Platform Wins

Support is a wash — both offer business-hours customer support without a dedicated ISV partner tier, so the quality of support should not swing the decision either way. Square wins for ISVs whose merchants sell in the physical world — retail, restaurants, services — and want a packaged commerce platform with the best hardware in the SMB market and onboarding measured in minutes. If speed-to-live and in-person coverage matter more than owning the payment economics, Square is the pragmatic choice, and its closest head-to-head is Square vs Adyen at the larger end.

Braintree wins for ecommerce-first and enterprise ISVs that need developer-grade APIs, native PayPal and Venmo acceptance, recurring billing, and global currencies — and that do not need a POS ecosystem their merchants run the day on. If your merchants are e-commerce or SaaS businesses and PayPal acceptance lifts conversion, Braintree earns its place; the Stripe vs Braintree angle is worth a look if developer ubiquity is the priority. For either path, remember the ceiling: if you want white-label control and margin you set yourself, look past both aggregators to a PayFac-as-a-service provider.

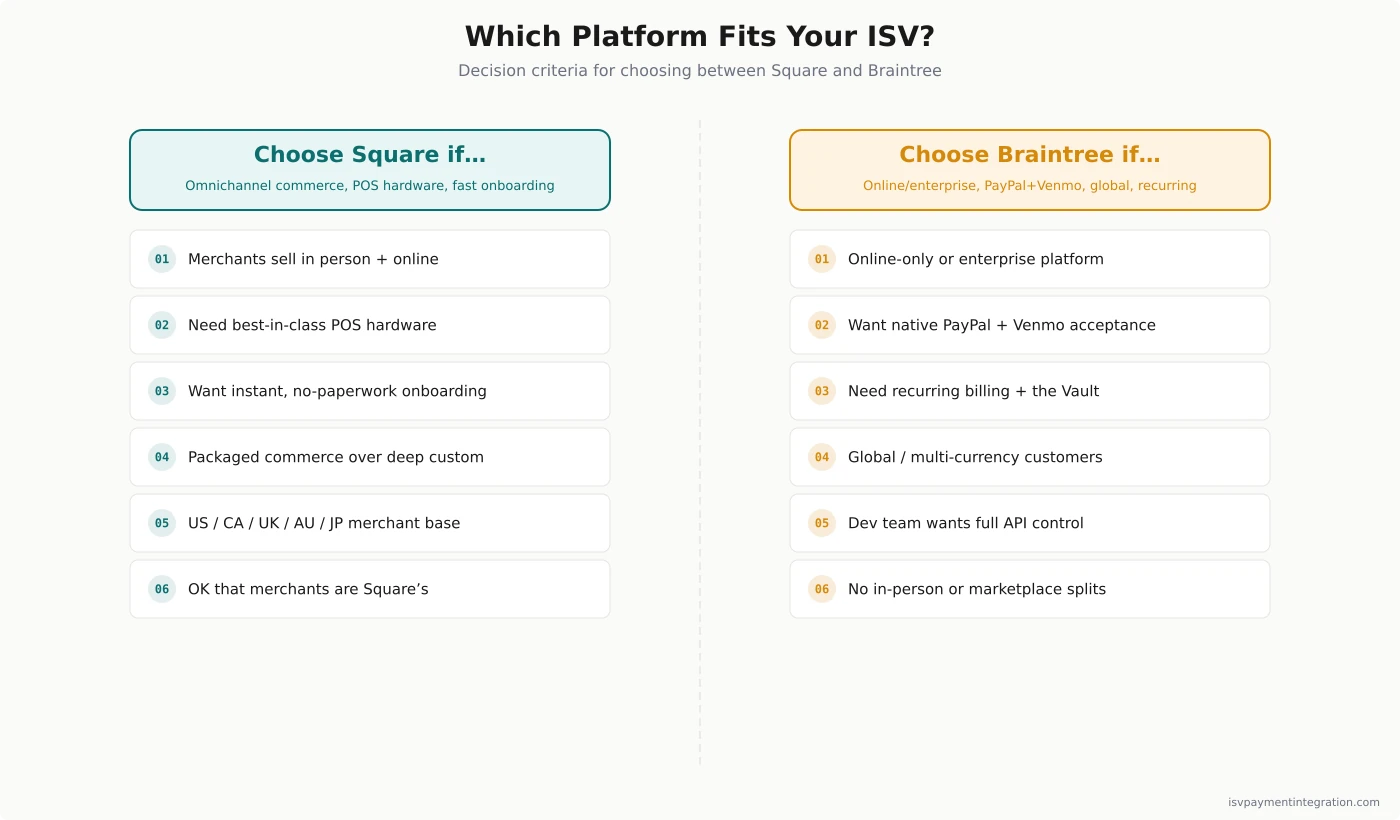

Square vs Braintree: ISV Decision Guide

Choose Square if your merchants sell in person and online, you want the best POS hardware and instant onboarding, and a packaged commerce platform beats deep payment customization for your product.

Choose Braintree if your merchants are online or enterprise, you want developer-first APIs with native PayPal and Venmo, recurring billing, and global currency support — and you do not need in-person hardware or marketplace splits.

If neither fits — because you want to own the merchant relationship, brand the experience, and earn revenue share on every transaction — that is a sign you should evaluate PayFac-as-a-Service instead. Get an ISV payments assessment and we will map your merchant base and monetization goals to the right model.

Frequently Asked Questions

Who is Square’s biggest competitor?

For small-business commerce, Square competes most directly with Clover, Toast, and Shopify on the POS and software side. For ISVs and platforms specifically, the more relevant competitor is Stripe — its Connect product publishes a platform rate and offers the white-label control Square’s aggregator model does not. Braintree’s card-present product is a Verifone-based extension of an ecommerce account, so the two overlap most where the transaction is online and least where the merchant runs the counter.

What is the downside of Square for an ISV?

Square is an aggregator, so its merchants are Square’s customers, not the ISV’s. There is no white-label option, no share of transaction revenue under standard API access, and Square can place holds on or terminate a seller’s account unilaterally — which disrupts the ISV’s product for that merchant with no contractual recourse. Square also processes in only a handful of countries, limiting international ISVs.

How much does Braintree charge per transaction?

Per Braintree’s official schedule (last updated May 2026), the standard rate is 2.89% + $0.29 for cards and digital wallets, 3.49% + $0.49 for Venmo, and 0.75% (capped at $5) for ACH Direct Debit. International cards and non-USD currencies each add 1%, and chargebacks are $15. There is no monthly or setup fee, and interchange-plus pricing is available on custom enterprise deals, generally above $100,000 a month.

Is Square or Braintree better for an ISV or platform?

It depends on where your merchants sell. Square is better for omnichannel and in-person businesses that want packaged commerce and fast onboarding. Braintree is better for ecommerce-first and enterprise platforms that want developer APIs, native PayPal and Venmo, and global currencies — it does ship a Verifone-based card-present product, but PayPal frames it as an extension of a web account rather than a point-of-sale ecosystem. For an ISV that wants to monetize payments with white-label control, neither is ideal — a PayFac-as-a-Service provider is the better fit.

Can an ISV earn revenue share or become a PayFac with Square or Braintree?

Not with a plain API key. Square pays no transaction revenue share under standard API access, and its App Partner Program advertises “profit share eligibility” without attaching a rate or threshold to it. Sign the Developer Integration and Marketing Agreement, though, and section 6(b) pays a 10% referral fee on net processing revenue for the first twelve months of merchants you refer — a real published number, in a public contract, that most write-ups miss. Square vs Fiserv works through what that clause is worth. Braintree’s dedicated marketplace sub-merchant product is no longer self-serve — PayPal routes new merchants to its sales team — and the alternative, Braintree Auth, is still labeled Beta in PayPal’s own documentation. ISVs that want to earn the payment markup and own merchant relationships should look at PayFac-as-a-Service providers like Finix, Tilled, or Xplor Pay, which are built specifically for that model.