Square vs Adyen

A feature-by-feature comparison for ISVs integrating payments.

Two platforms built for different ISV segments. Square packages payments with POS hardware, business tools, and instant merchant onboarding under one aggregator model. Adyen separates acquiring, processing, and risk management into a single enterprise platform with local acquiring in 30+ markets and interchange-plus economics.

Feature Comparison

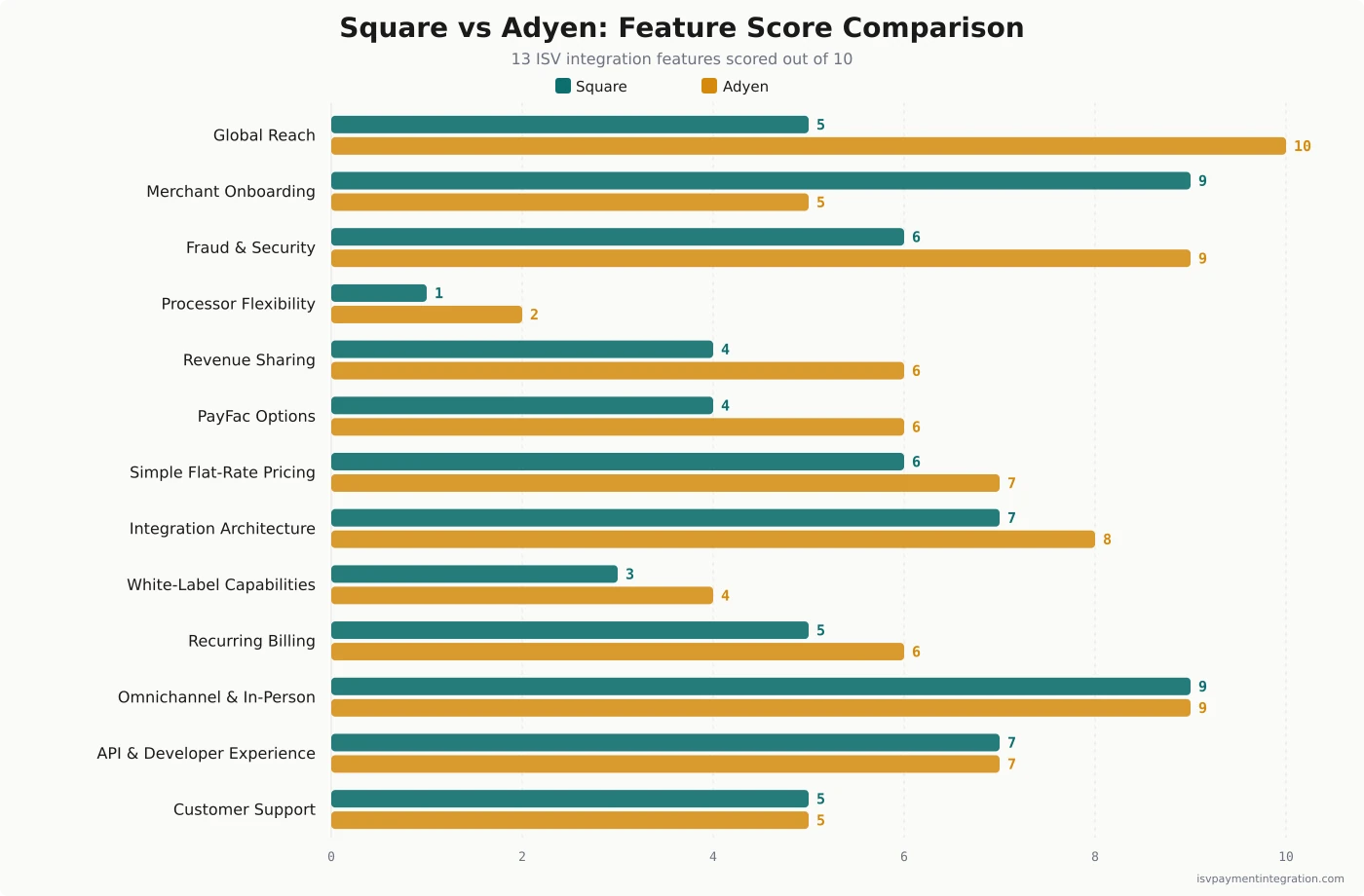

| Feature | Square | Adyen |

|---|---|---|

| Integration Architecture | 7 | 8 |

| API & Developer Experience | 7 | 7 |

| White-Label Capabilities | 3 | 4 |

| Processor Flexibility | 1 | 2 |

| Pricing & Fee Structure | 6 | 7 |

| Omnichannel & In-Person Payments | 9 | 9 |

| Fraud & Security | 6 | 9 |

| Revenue Sharing | 5 | 6 |

| Merchant Onboarding | 9 | 5 |

| Global Reach | 5 | 10 |

| Recurring Billing | 5 | 6 |

| Customer Support | 5 | 5 |

| PayFac Options | 4 | 6 |

Get this comparison as a shareable PDF

We'll send the Square vs Adyen breakdown to your inbox — ready to share with your team.

Best for

Square

ISVs serving SMB merchants in Square's core markets who need turnkey POS hardware and unified online/offline payments.

Best for

Adyen

ISVs building global enterprise platforms that need multi-country acquiring, local payment methods, and scalable infrastructure.

Square vs Adyen: What ISVs Need to Know

Square and Adyen sit at opposite ends of the payment platform spectrum. Square built its reputation on turnkey simplicity for small and mid-size businesses — instant onboarding, flat-rate pricing, and an integrated POS ecosystem that merchants can set up in minutes. Adyen built its reputation on enterprise-grade infrastructure — local acquiring in 30+ markets, interchange-plus economics, and a single platform connecting acquiring, processing, and risk management under one contract. For ISVs embedding payments into software, the choice between them shapes everything from merchant activation speed to long-term revenue economics.

Integration Architecture: SMB Platform vs Enterprise Stack

Square and Adyen take fundamentally different architectural approaches, and that difference defines the ISV integration experience.

Square operates as a vertically integrated aggregator. Payments, POS hardware, invoicing, payroll, and merchant dashboards all live inside one ecosystem. Square acts as the merchant of record — your merchants are technically sub-merchants under Square’s master account. This aggregator model is what enables instant onboarding: Square assumes the underwriting risk upfront, so merchants can start accepting payments within minutes of signing up. For ISVs, this means you can embed Square payments and give your users an extremely fast path to processing transactions. The trade-off is control. Square owns the merchant relationship, sets the pricing, and keeps its branding front and center.

Adyen operates as a single-platform acquirer and processor. Acquiring, processing, risk management, and settlement all run through Adyen’s infrastructure under one contract. Unlike Square, Adyen is not an aggregator — each merchant gets their own merchant account with direct acquiring relationships. Adyen for Platforms gives ISVs embedded payment capabilities with managed compliance and sub-merchant onboarding, but the setup is more involved. Integration requires more upfront engineering effort, and merchant activation takes longer because Adyen runs full KYC and underwriting.

The ISV implication: Square gives you a turnkey merchant experience with minimal integration effort. Adyen gives you enterprise-grade control over payment routing, risk rules, and multi-currency settlement — but you pay for that control in integration complexity and onboarding speed.

API and Developer Experience

Both platforms offer modern REST APIs, but the developer experience differs meaningfully.

Square’s API ecosystem is well-documented with SDKs in Python, Ruby, Java, PHP, .NET, and Node.js. The Square Developer Dashboard provides sandbox environments, API logs, and webhook management in a clean interface. Square’s documentation is organized around use cases — payments, orders, inventory, customers — making it straightforward for ISVs to find what they need. The Catalog API and Orders API handle complex retail scenarios well.

Adyen’s API documentation at docs.adyen.com is comprehensive but carries a steeper learning curve. Adyen’s APIs cover more ground — checkout, recurring, payout, platform, and terminal APIs each have their own integration patterns. The test environment requires more configuration than Square’s sandbox. Adyen’s client-side libraries (Drop-in, Components) offer pre-built UI elements, but customizing them takes more effort than Square’s Web Payments SDK.

Neither platform matches Stripe’s developer experience. Square comes closer for simplicity. Adyen comes closer for raw capability. ISVs should budget 2-4 weeks for a Square integration and 4-8 weeks for Adyen, depending on scope. For deeper analysis of each platform’s API capabilities, see our Square review and Adyen review.

Revenue Economics for ISVs

Payment revenue is the primary financial motivation for ISVs embedding payments. The pricing model each platform uses directly determines how much margin you capture per transaction.

How ISVs Make Money from Embedded Payments

ISVs monetize embedded payments through three models: referral (earn a bounty per merchant), partner/revenue share (split the payment margin with the processor), and PayFac (set your own merchant pricing and keep the spread). Each model offers progressively more revenue but requires more compliance responsibility. For a full breakdown, see our PayFac-as-a-Service guide and the payment facilitator glossary entry.

Square and Adyen handle ISV revenue sharing differently, and the economics diverge significantly at scale.

Square Pricing and Revenue Sharing

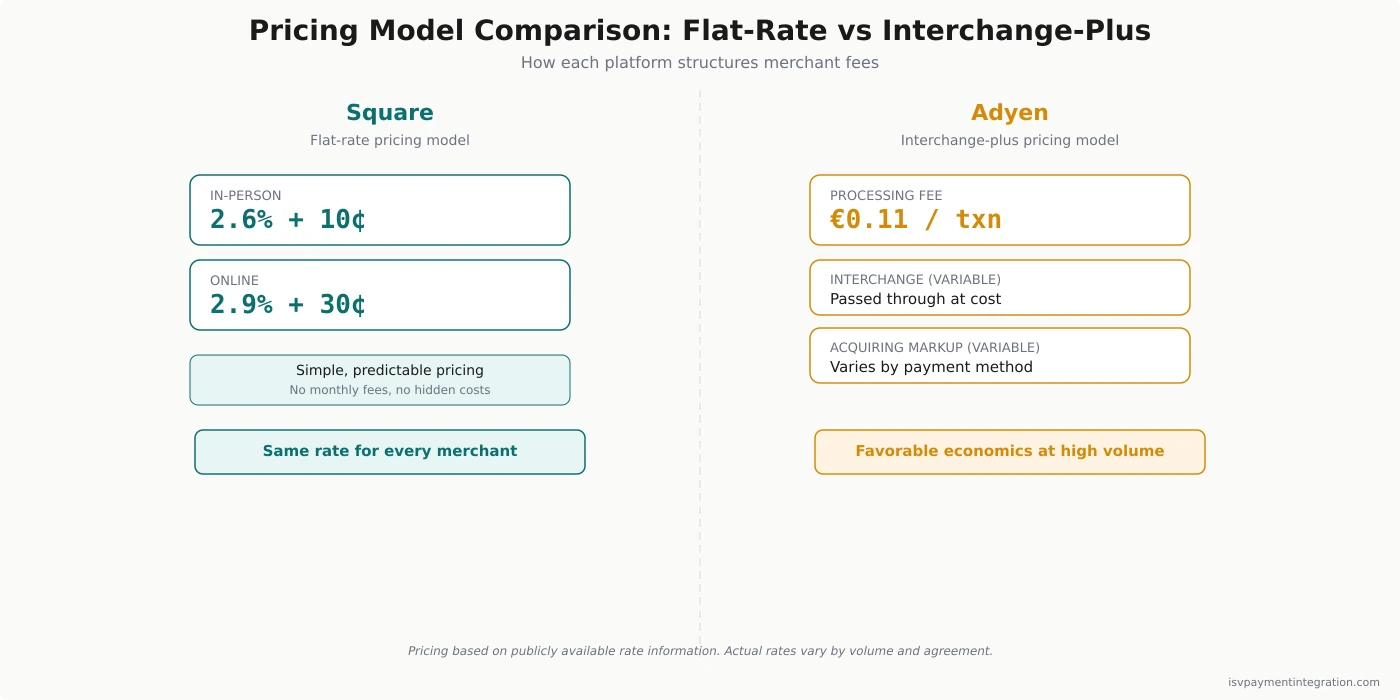

Square charges flat-rate pricing: 2.6% + 10 cents for in-person transactions and 2.9% + 30 cents for online transactions. This simplicity is Square’s selling point — merchants know exactly what they’ll pay, and there are no hidden fees or monthly minimums.

For ISVs, the flat-rate model creates a problem. Square controls the merchant pricing, and there is limited room for ISV-specific revenue sharing. ISVs embedding Square payments primarily monetize through software subscriptions rather than payment margin. Square does offer partnership programs, but the economics are not structured around giving ISVs a meaningful cut of the processing spread.

At high volumes, flat-rate pricing becomes expensive. A merchant processing $500,000/month at 2.9% + 30 cents pays significantly more than they would on interchange-plus. This makes Square less attractive for ISVs whose merchants grow beyond the SMB tier. For full pricing details, see our Square pricing page.

Adyen Pricing and Revenue Sharing

Adyen uses interchange-plus pricing with acquiring markups — on Visa and Mastercard the published card rate renders as $0.13 + Interchange+ + 0.60% (Adyen’s Interchange++ pricing model). Adyen lists those markups on its pricing page but labels them indicative, and applies an unpublished minimum invoice that varies by industry, so the 0.60% is a negotiation anchor rather than a locked rate. For high-volume merchants, this model typically saves 20-40% compared to flat-rate pricing.

Adyen for Platforms includes an explicit revenue-sharing program. ISVs integrate once, and Adyen handles acquiring, risk management, and settlement. The platform includes managed sub-merchant onboarding with compliance handled by Adyen. Revenue sharing is negotiated based on volume commitments — ISVs processing more volume get better splits.

The catch: Adyen for Platforms is designed for ISVs processing significant volume, typically $10M+ annually. Smaller ISVs may not qualify or may receive less favorable terms. For full pricing details, see our Adyen pricing page.

Revenue Example: 50,000 Transactions/Month

Consider an ISV whose merchants collectively process 50,000 transactions per month at a $75 average ticket — $3.75M in monthly volume.

Square (flat-rate at 2.9% + 30 cents for online):

- Per-transaction cost: ($75 x 0.029) + $0.30 = $2.475

- Monthly total: 50,000 x $2.475 = ~$123,750/month in processing fees

- ISV payment revenue: minimal (Square controls pricing)

Adyen (interchange-plus at ~1.7-2.2% effective rate):

- Per-transaction cost: $75 x 0.017-0.022 = $1.275-$1.650

- Monthly total: 50,000 x $1.275-$1.650 = ~$63,750-$82,500/month in processing fees

- ISV payment revenue: negotiated rev-share on the acquiring markup

The difference is $41,000-$60,000 per month in processing costs alone. For ISVs with a revenue-sharing arrangement, the interchange-plus model creates more margin to split. Note: actual pricing is custom-negotiated with both platforms, and these figures are illustrative based on published rates.

Merchant Onboarding

Merchant onboarding speed directly affects ISV growth. Every day a merchant waits to start processing is a day of lost revenue for both the merchant and the ISV.

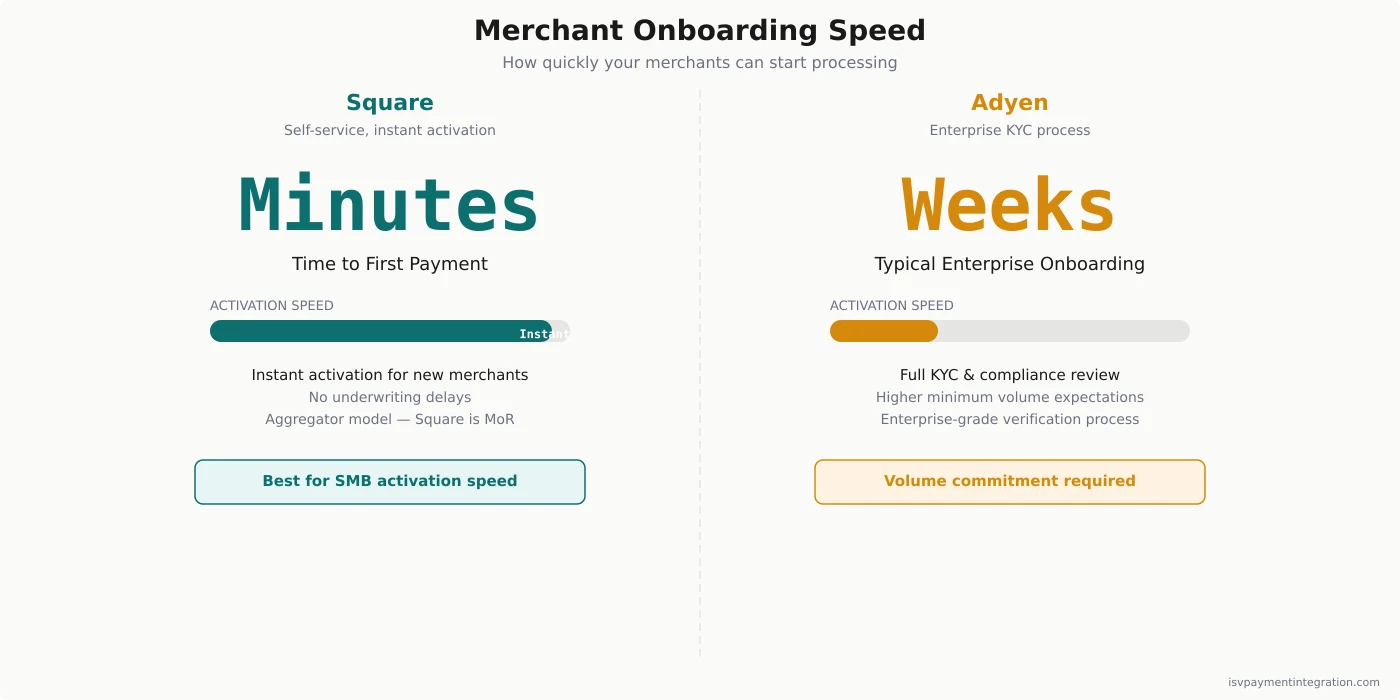

Square scores 9/10 here for good reason. The aggregator model means Square handles all underwriting risk upfront. Merchants sign up, connect a bank account, and start accepting payments — often within minutes. No paperwork. No waiting for manual review. For ISVs serving SMB verticals like restaurants, salons, or retail shops, this instant activation is a massive competitive advantage. Your merchants go from signup to first transaction in the same session.

Adyen scores 5/10 because enterprise-grade compliance takes time. Each merchant gets a proper merchant account, which means Adyen runs full KYC (Know Your Customer) verification, reviews business documentation, and sets volume limits. Onboarding cycles can take days to weeks depending on merchant complexity. Adyen also has minimum volume expectations that filter out very small merchants.

ISV implication: If your merchants are SMBs who need to start processing today, Square’s aggregator model is hard to beat. If your merchants are mid-market or enterprise businesses who expect proper merchant accounts and are willing to wait for better economics, Adyen’s onboarding process is appropriate for the segment.

Global Reach and Local Payments

For ISVs with international merchant bases, geographic coverage is often the deciding factor.

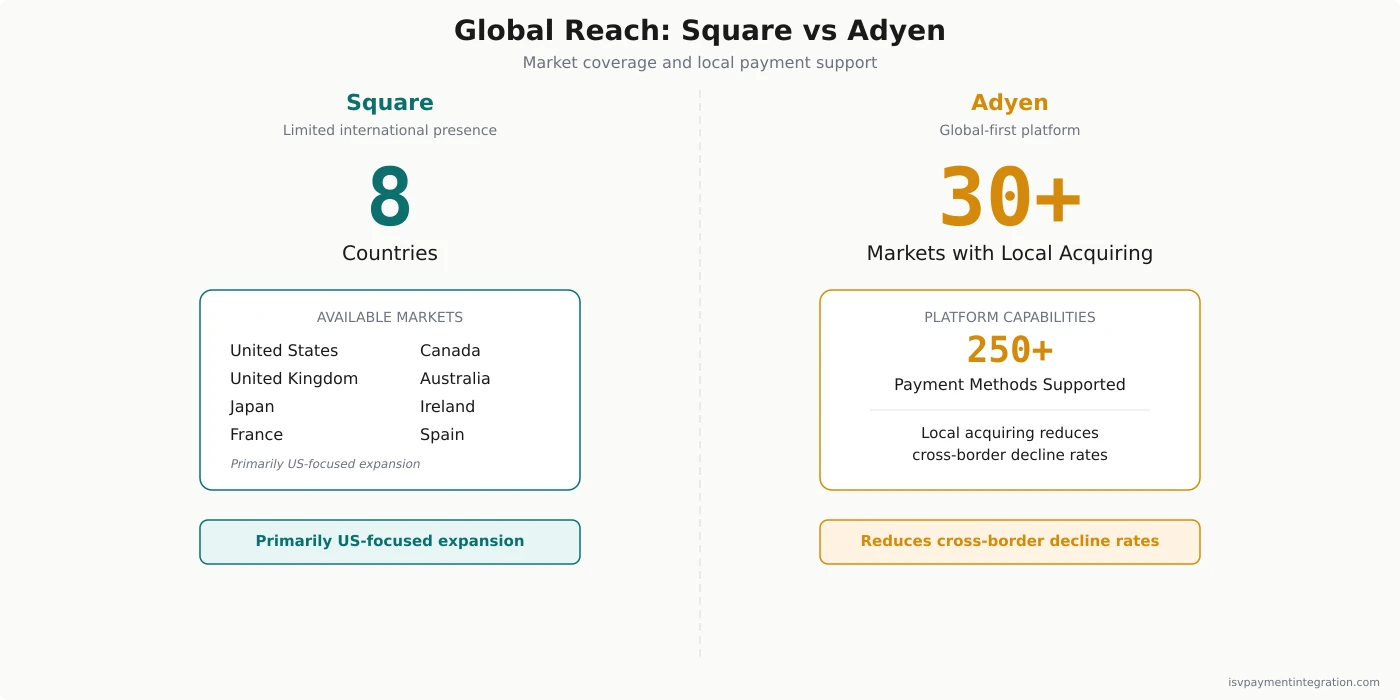

Square operates in 8 countries: the US, Canada, Australia, Japan, the UK, Ireland, France, and Spain. The platform is heavily US-focused, and international capabilities are limited. Cross-border transactions are not a strength. If your ISV’s merchants are primarily in the US or one of Square’s supported markets, this coverage may be sufficient. If you need to serve merchants across Europe, Asia, or Latin America, Square cannot support you.

Adyen holds local acquiring licenses in 30+ markets and supports over 250 local payment methods. Local acquiring means transactions are processed domestically in each market, which reduces cross-border decline rates and eliminates cross-border fees. Adyen supports iDEAL in the Netherlands, Boleto in Brazil, Alipay in China, and dozens of other region-specific payment methods that drive higher conversion rates.

For ISVs with merchants operating across 10+ countries, Adyen is the clear winner. The combination of local acquiring, local payment methods, and multi-currency settlement gives ISVs a global payment infrastructure that Square simply cannot match.

Fraud and Security

Fraud management capabilities differ substantially between the two platforms.

Square provides built-in fraud detection that runs automatically on every transaction. The system uses machine learning to flag suspicious activity, and Square offers chargeback protection as a paid add-on. For most SMB merchants, Square’s fraud tools are adequate — they handle common fraud patterns without requiring merchant configuration.

Adyen’s RevenueProtect is a significantly more sophisticated fraud engine. It combines machine learning with custom risk rules that ISVs and merchants can configure per transaction type. RevenueProtect includes network tokenization (replacing card numbers with network-level tokens for higher authorization rates), 3DS2 optimization (dynamically applying strong customer authentication only when required), and real-time risk scoring with adjustable thresholds.

For ISVs in high-risk verticals — travel, digital goods, marketplaces, or cross-border commerce — Adyen’s fraud management is a major differentiator. The ability to set custom risk rules per merchant segment, combined with Adyen’s cross-network intelligence from processing billions in transactions, gives ISVs tools that Square’s one-size-fits-all approach cannot match. Adyen scores 9/10 to Square’s 6/10 in this category.

Omnichannel and POS Hardware

Both platforms score 9/10 for omnichannel capabilities, but they serve different markets.

Square’s POS ecosystem is industry-leading for SMB merchants. The hardware lineup includes Square Reader (contactless + chip), Square Terminal (all-in-one portable device), Square Register (full countertop POS), and Square Stand (iPad-based POS). Each device works out of the box with Square’s software, and merchants can manage inventory, employees, and sales from a single dashboard. For ISVs in restaurant, retail, and beauty/wellness verticals, Square’s hardware ecosystem provides a complete merchant solution.

Adyen’s terminal fleet is purpose-built for enterprise unified commerce. Adyen terminals connect directly to the Adyen platform, giving merchants a single view of online and in-store transaction data. The terminals support custom configurations, fleet management, and centralized updates. Adyen’s in-person solution excels when merchants need consistent payment experiences across hundreds or thousands of locations.

The choice depends on your merchant profile. Square dominates SMB retail and food service. Adyen dominates enterprise chains and multi-location businesses. Both deliver strong omnichannel experiences — just for different market segments.

White-Label and Branding Control

Neither Square nor Adyen offers full white-label payment processing.

Square’s branding is visible on hardware, receipts, and merchant dashboards. ISVs embedding Square payments will have Square’s brand present in the merchant experience. Customization options are limited — you can embed Square’s payment form into your application, but merchants will see Square branding in multiple touchpoints.

Adyen offers a co-branded checkout experience with more customization than Square, but Adyen branding still appears in merchant-facing flows. Adyen’s Drop-in and Components allow ISVs to style the payment UI to match their application, but the underlying merchant onboarding and dashboard experience carries Adyen’s brand.

For ISVs that need full white-label control — your brand on everything the merchant sees — neither platform is the right choice. Platforms like NMI or Payrix offer deeper white-label capabilities. See our white-label solutions guide for alternatives.

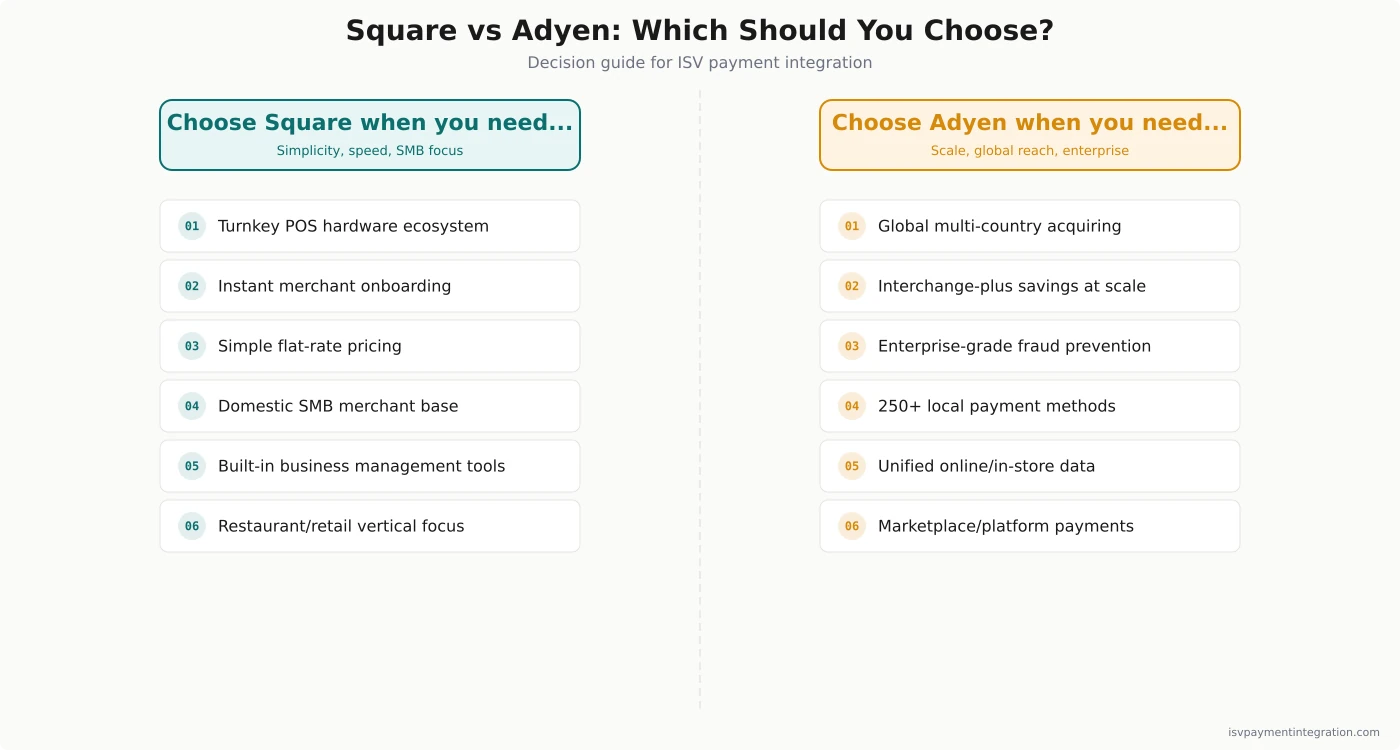

When to Choose Square

Square is the right embedded payments partner when your ISV meets these criteria:

- Domestic SMB merchants who need a turnkey POS and payment solution in Square’s 8 supported countries

- Low to medium transaction volumes where flat-rate pricing simplicity matters more than per-transaction optimization

- Restaurant, retail, beauty/wellness, and service verticals where Square’s integrated ecosystem (appointments, inventory, team management) adds value beyond payments

- Fast merchant activation is a competitive requirement — your merchants need to process payments the same day they sign up

- Limited engineering resources for payment integration — Square’s APIs and SDKs get you to production faster

- Software subscription revenue is your primary monetization — you are not depending on payment margin as a significant revenue stream

When to Choose Adyen

Adyen is the right embedded payments partner when your ISV meets these criteria:

- Global enterprise platforms needing multi-country acquiring with local payment methods across 30+ markets

- High-volume ISVs processing $10M+ annually where interchange-plus pricing saves 20-40% versus flat-rate

- Marketplace and platform businesses needing sophisticated fraud management with custom risk rules per merchant segment

- ISVs serving merchants in 10+ countries who need local acquiring to reduce decline rates and eliminate cross-border fees

- Revenue-sharing priority — your ISV wants to earn meaningful payment margin through Adyen for Platforms

- Enterprise merchants who expect proper merchant accounts, dedicated support, and customized payment experiences

Frequently Asked Questions

What is the main difference between Square and Adyen for ISVs?

Square is an aggregator platform optimized for domestic SMB merchants with turnkey POS hardware and instant onboarding. Adyen is an enterprise payment platform with local acquiring in 30+ markets, interchange-plus pricing, and sophisticated fraud management. The choice depends on your merchant base — domestic SMB favors Square, global enterprise favors Adyen.

Can ISVs earn revenue from embedded payments with Square?

Square’s ISV revenue sharing options are limited compared to dedicated PayFac platforms. ISVs can embed Square payments via APIs, but Square controls the merchant relationship and pricing. Revenue primarily comes through software subscriptions rather than payment margin. For ISVs prioritizing payment revenue, platforms with explicit revenue-sharing programs like Adyen for Platforms offer better economics.

How does Adyen for Platforms work for ISVs?

Adyen for Platforms provides embedded payment capabilities with managed compliance, sub-merchant onboarding, and revenue sharing. ISVs integrate once and Adyen handles acquiring, risk management, and settlement across 30+ markets. The program requires minimum revenue commitments and is designed for ISVs processing significant volume — typically $10M+ annually.

Which platform has better fraud prevention for ISVs?

Adyen’s RevenueProtect is significantly more sophisticated than Square’s fraud tools. RevenueProtect uses machine learning with custom risk rules, network tokenization, and 3DS2 optimization. Square offers built-in fraud detection with chargeback protection available as an add-on. For ISVs in high-risk verticals or processing cross-border transactions, Adyen’s fraud capabilities are a major advantage.

Is Square or Adyen better for in-person payments?

Both platforms score 9/10 for omnichannel capability but serve different markets. Square’s POS hardware ecosystem (readers, terminals, registers, Square Stand) is industry-leading for SMB merchants. Adyen’s terminal fleet is purpose-built for enterprise with unified online and in-store transaction data. Choose Square for SMB retail and restaurants, Adyen for enterprise unified commerce.

How do Square and Adyen compare on pricing for high-volume ISVs?

Square charges flat-rate 2.6% + 10 cents for in-person and 2.9% + 30 cents for online transactions — simple but expensive at scale. Adyen uses interchange-plus pricing with acquiring markups, which typically saves 20-40% versus flat-rate at high volumes. For ISVs processing over $1M monthly, Adyen’s pricing model usually delivers significantly better economics.