Stax vs NMI

A feature-by-feature comparison for ISVs integrating payments.

Stax and NMI both serve ISVs but operate from opposite corners of the payments stack. Stax bundles gateway, processing, and analytics into a flat monthly subscription with interchange passed through at cost — predictable economics, one contract, US-domestic focus. NMI sells only the gateway layer and lets the ISV pick from 200+ acquirers — acquirer flexibility, full white-label, two contracts to manage. The decision is architectural (subscription pass-through vs unbundled gateway), not feature-by-feature.

Feature Comparison

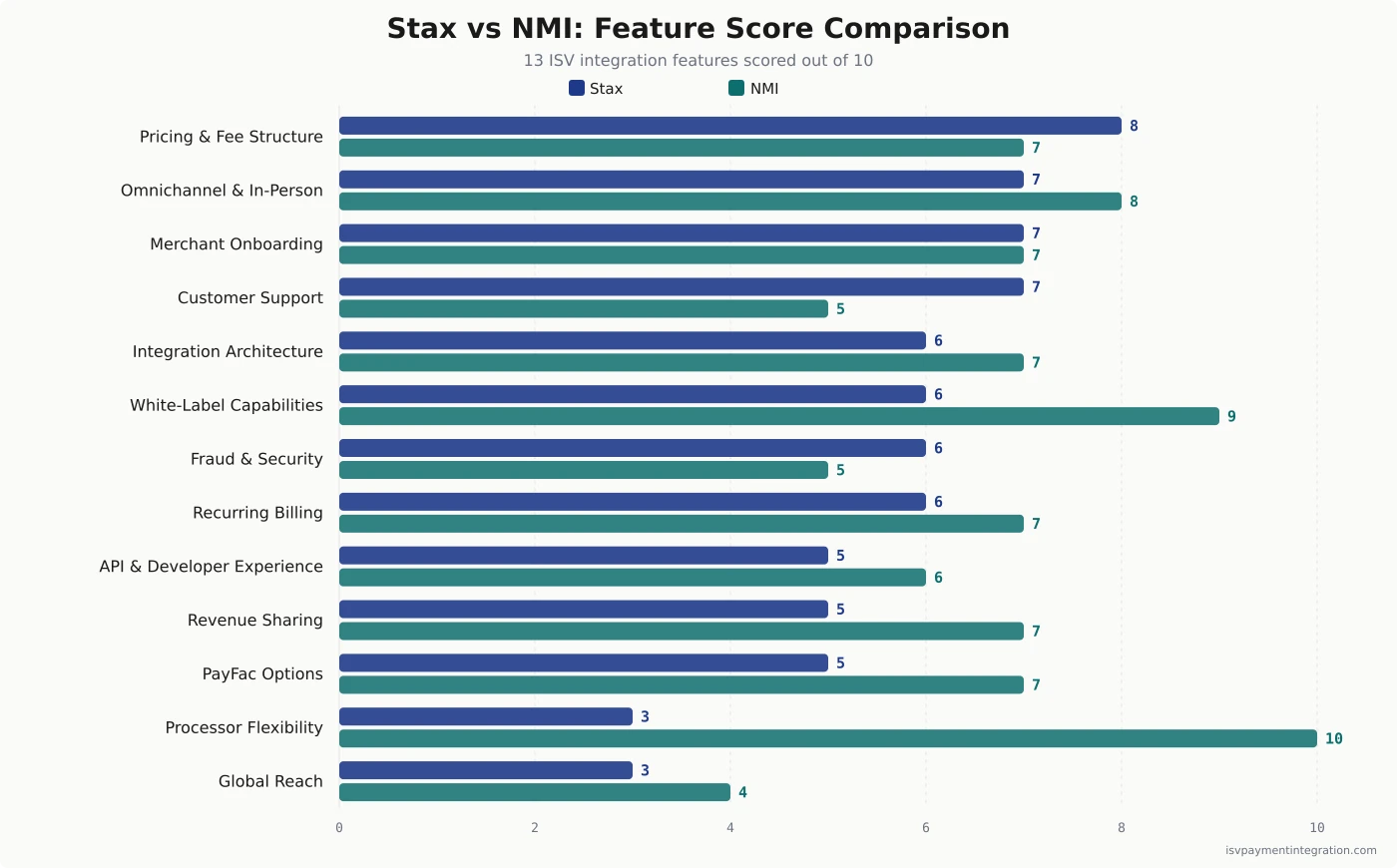

| Feature | Stax | NMI |

|---|---|---|

| Integration Architecture | 6 | 7 |

| API & Developer Experience | 5 | 6 |

| White-Label Capabilities | 6 | 9 |

| Processor Flexibility | 3 | 10 |

| Pricing & Fee Structure | 8 | 7 |

| Omnichannel & In-Person Payments | 7 | 8 |

| Fraud & Security | 6 | 5 |

| Revenue Sharing | 5 | 7 |

| Merchant Onboarding | 7 | 7 |

| Global Reach | 3 | 4 |

| Recurring Billing | 6 | 7 |

| Customer Support | 7 | 5 |

| PayFac Options | 5 | 7 |

Get this comparison as a shareable PDF

We'll send the Stax vs NMI breakdown to your inbox — ready to share with your team.

Best for

Stax

Best for ISVs serving SMB and mid-market merchants who each process $10K+/month, want predictable subscription cost over percentage-based pricing, and prefer one vendor for gateway, processing, and analytics. Less attractive for low-volume sub-merchants where the monthly fee dominates the unit economics.

Best for

NMI

Best for ISVs, ISOs, and PFaaS providers that want acquirer-independence, full white-label embedded payments, and 300+ EMV device coverage across unattended/self-service merchants. Best when the ISV is willing to manage two commercial relationships (gateway + acquirer) for arbitrage upside.

Stax vs NMI for ISVs

The cleanest way to see why Stax and NMI are not interchangeable is to run the same merchant through both. A vertical-SaaS sub-merchant processing $200,000 a year on cards pays roughly 3.9–4.4% all-in on Stax (subscription + per-transaction + interchange-at-cost) and somewhere between 4.5% and 5.2% on a partnered-acquirer setup behind NMI (gateway fee + acquirer interchange-plus + ISO markup), depending on which acquirer the ISO routes the merchant through and what rev-share the ISV negotiated. Drop that same merchant to $50,000 a year and the math inverts — Stax’s $99/month subscription doesn’t pay back at low volume, while NMI’s per-transaction gateway fee scales smoothly with whatever the merchant actually processes.

The choice between them is rarely about features. It’s about whether your ISV’s sub-merchant base is dense enough at the volume tiers where subscription pricing wins, whether you want acquirer-routing flexibility or single-vendor accountability, and how much of the merchant operations workload you want to hand to the platform versus run in-house. Most ISVs land definitively in one camp after they actually model their sub-merchant volume distribution against the breakeven curves.

This page is the version of that comparison written for ISVs who already know they need embedded payments and now have to choose which architectural path their platform sits on for the next five years. Both models are legitimate. Both have named ISV partners running production volume on them. The friction you inherit and the economics you capture are what differ.

The Quick Take: Who Each Platform Actually Is

Stax (formerly Fattmerchant, rebranded 2021) is a full-stack payments platform with subscription pricing — flat monthly fee plus per-transaction cost plus interchange passed through at cost, with no percentage markup. Founded in 2014 in Orlando, Florida by Suneera Madhani and Sal Rehmetullah, the company processes $23 billion annually for 39,000 merchants and 150+ integrated software partners through its Stax Connect ISV program (per the company’s October 2025 Stax Processing launch announcement). The major architectural shift for ISVs evaluating Stax in 2026: in October 2025, Stax launched Stax Processing, an in-house full-stack processor built on its acquisitions of Atlantic-Pacific Processing Systems (APPS) and BlockChyp. Stax now operates its own technology stack from origination through clearing and settlement, while remaining registered as an ISO/MSP under Fifth Third Bank, Synovus Bank, and Elavon (a U.S. Bancorp subsidiary) for card-network sponsorship — that is the standard registration model, since only banks can hold direct card-network membership. The control investor is Greater Sum Ventures (acquired controlling stake December 2020); the founders departed in March 2025 to launch a new fintech (Worth AI). John Cimba became CEO in February 2026, succeeding Paulette Rowe who led the Stax Processing launch.

NMI (Network Merchants, Inc.) is a pure payment gateway — it does not acquire transactions, hold a BIN, or settle funds. Founded in 2001 in Schaumburg, Illinois and now backed by Francisco Partners, Great Hill Partners, and Insight Partners, NMI processes $502B+ in annual transaction volume across 6.5B+ transactions, 6,000 channel partners, 1.2M+ active merchants, and 235,000 connected devices (per the company’s January 2026 year-end disclosure). The platform connects to 200+ pre-certified acquiring processors (Fiserv, Worldpay/Global Payments, TSYS, Elavon, Chase Paymentech, Barclaycard) and certifies 300+ EMV payment devices. Pricing is partner-negotiated, splitting a per-transaction gateway fee from the acquirer-side interchange-plus economics that flow through to whichever processor the merchant routes to. Steven Pinado became CEO in September 2025, succeeding Vijay Sondhi who led the platform through its 11x volume growth from 2018 to 2025.

The strategic philosophies are inverses. Stax bundles — one vendor, one contract, one settlement, with the entire economics legible from the Stax pricing page. NMI unbundles — gateway from one vendor, acquirer from another, two contracts, two relationships, and pricing that is genuinely negotiable on both sides because the layers are separable. Stax’s bet is that ISVs and SMB-to-mid-market merchants prefer simplicity; NMI’s bet is that ISVs and ISOs with leverage prefer optionality. Neither bet is wrong — they appeal to different ISV profiles, and the decision is more about institutional fit than feature parity.

What Stax and NMI Actually Are

The architectural difference between these two platforms is the most important thing to understand before reading any further. Most reviews skip it; almost every wrong decision starts there.

Stax: full-stack subscription processor with in-house tech and ISV arm

Stax operates a vertically integrated payments stack — its own gateway (originally built on Authorize.Net’s foundation, since heavily modified), its own processing tech (Stax Processing, launched October 2025 on the back of the APPS and BlockChyp acquisitions), its own merchant dashboard with built-in analytics and invoicing, and bank-sponsored ISO/MSP relationships with Fifth Third Bank, Synovus Bank, and Elavon for card-network access. The October 2025 Stax Processing launch announcement framed the shift as “freeing ourselves and our partners from the constraints of legacy third-party systems that many others in the industry still rely on” — a direct dig at gateway-only and pass-through-acquirer competitors.

For ISVs, the Stax stack arrives via a dedicated product called Stax Connect (launched 2020). Stax Connect is sold in three commercial flavors:

- Stax Connect Plus — the fully managed model where Stax’s own sales team handles pre-sales, merchant onboarding, terminal setup, and ongoing support; the ISV focuses on its core software while collecting revenue share. ClientTether (a franchise CRM platform) adopted Stax Connect Plus and reported a 67% merchant application close rate and 70% reduction in support tickets, per the ClientTether case study.

- Reseller Model — the ISV runs its own sales motion; Stax provides marketing and back-end support. Closer to a traditional ISO partnership in shape, with ISV-controlled merchant pricing.

- Custom Pricing — SaaS-friendly model where the ISV sets pricing for its merchants and Stax sits as the underlying platform. Common for vertical SaaS with established merchant pricing power.

A Forrester Total Economic Impact study commissioned by Stax estimated 141% ROI and ~$900K incremental revenue for ISVs running on Stax Connect — that’s a Stax-commissioned number, not an independent benchmark, so treat it as marketing telemetry rather than gospel, but it sets the order-of-magnitude expectation Stax pitches in sales conversations. Named Stax Connect partners include ChiroSpring (chiropractic practice management, launched ChiroSpring Pay), ClientTether (franchise CRM), and Sera (field-services platform). The vertical concentration is consistent: field services, legal, non-profit, professional services, education, and specialized healthcare — verticals where the merchant ticket size is high enough to make subscription pricing favorable and the ISV-led GTM motion is strong enough to justify Stax Connect Plus’s managed-services model.

The trade-off is everything that comes with a full-stack platform: a higher commercial barrier per merchant (the subscription doesn’t pay back below a volume threshold), US-domestic concentration (no international acquiring), and the need to commit to one vendor for the foreseeable future. The acquirer-of-record under the hood is Stax itself (via its ISO/MSP registration with Fifth Third/Synovus/Elavon) — there is no acquirer-routing decision for the ISV to make, which is simplifying for some ISVs and limiting for others.

NMI: gateway-first platform with multi-acquirer routing

NMI’s positioning starts with a deliberate refusal to acquire. The platform sits between the merchant’s point of sale or website and any of 200+ acquiring processors — the same value proposition Authorize.Net popularized in the early 2000s, scaled to a global ISV/ISO partner network and modernized for embedded-payments use cases.

For ISVs, that gateway-first model produces a different set of strengths. One integration covers many acquirers — your software writes one API integration, and your merchants can be settled by First Data/Fiserv, Worldpay/Global Payments, TSYS, Elavon, Chase Paymentech, Barclaycard, or any of dozens of regional acquirers depending on geography, vertical fit, or commercial terms. The platform stays invisible — NMI’s white-label depth means the ISV’s brand owns the merchant relationship completely, with no NMI logo, document, or reference appearing in the sub-merchant flow. The 300+ EMV device estate spans Ingenico, ID TECH, Madic, Payter, FEIG, and LANDI hardware certified across ecommerce, in-person, mobile, and unattended/self-service environments — a footprint that’s structurally hard to replicate for ISVs serving parking, vending, transit, kiosk, EV-charging, or other self-service verticals.

The trade-off is that NMI is a gateway, not a one-stop shop. Your software platform still needs an acquirer relationship — direct or through an NMI-partnered ISO or PayFac — and the ISV ends up managing two commercial relationships (gateway and acquirer) instead of one.

Pricing & ISV Economics

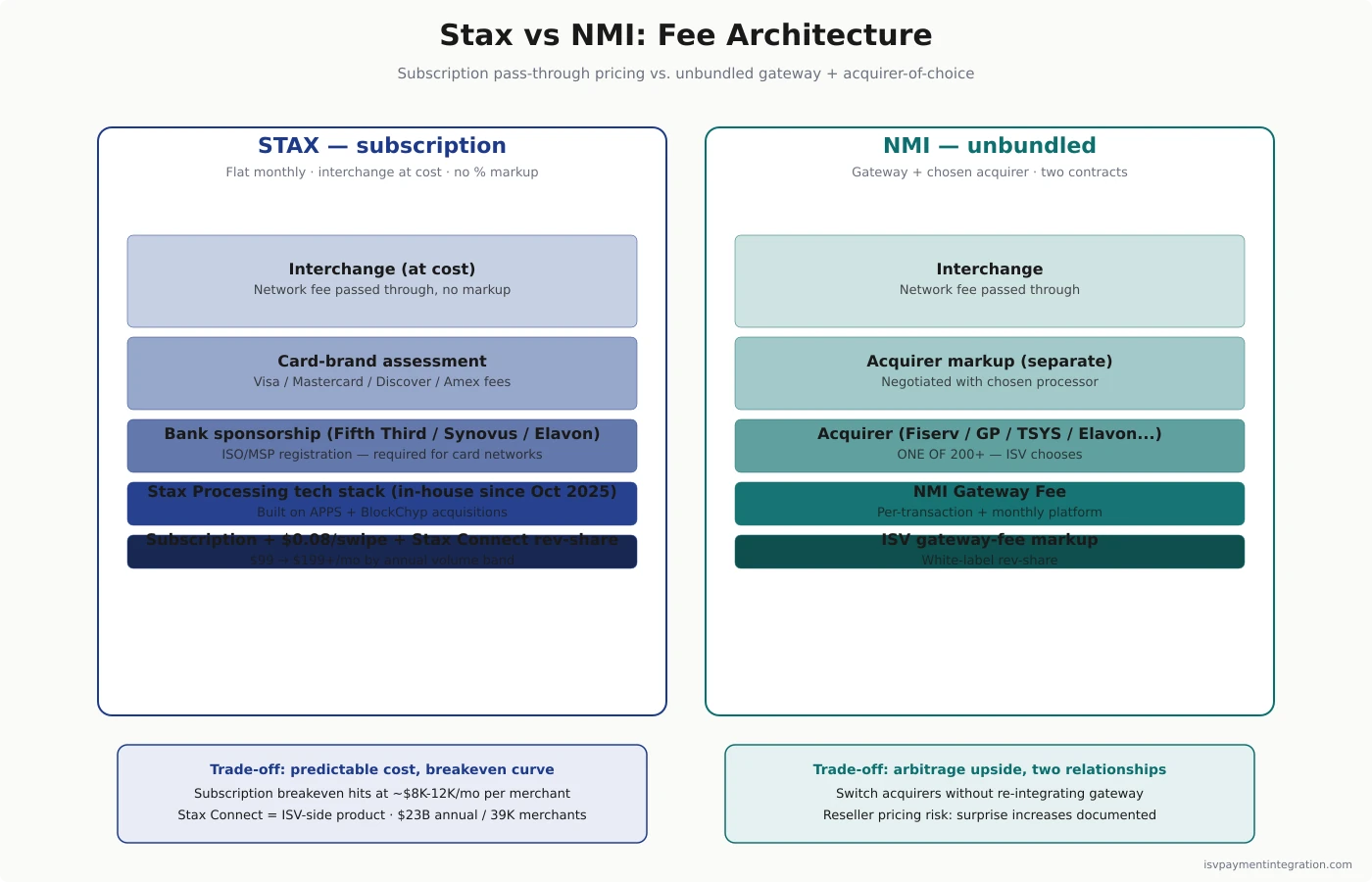

This is where the two platforms diverge most sharply. Stax publishes a rate. NMI doesn’t. That difference is downstream of the architectural choice each platform made about what to bundle.

Stax: volume-banded subscription with interchange at cost

Stax’s pricing page is unusually transparent. The current 2026 structure is volume-banded with no tier names — three subscription levels keyed to the merchant’s annual processing volume, plus per-transaction fees on top, plus interchange passed through at cost with zero percentage markup.

| Annual Processing Volume | Monthly Subscription |

|---|---|

| Up to $150,000/yr | $99/month |

| $150,000–$250,000/yr | $139/month |

| $250,000+/yr | $199+/month |

| Enterprise | Custom quote |

Per-transaction fees (charged on top of the subscription, always):

- Card present (swipe / dip / tap): $0.08 per transaction

- Card not present (keyed / online): $0.15 per transaction

- ACH: 1% per transaction, capped at $10

- Surcharging program: compliant credit-card surcharge passes the processing cost to the cardholder (merchant pays 0%); debit surcharge is 1.25% + $0.25 paid by the merchant

What Stax does not charge: no percentage markup on interchange, no setup fee for ISV partners, no separate gateway fee (the gateway is bundled into the subscription). What Stax does charge that’s worth budgeting for: chargeback protection at $25 per dispute, terminal protection plans at $19/month, and the per-transaction fee itself at the volume the merchant actually processes.

The economic logic is simple enough to model on a single line. A merchant processing $200,000/year on cards (call it ~17,000 transactions at $12 average ticket) on the $139/month tier pays $1,668 in subscription + $1,360 in per-transaction fees + roughly $4,800–$5,800 in interchange (at 2.4–2.9% blended interchange) — total ~$7,800–$8,800 on $200K of volume, or 3.9%–4.4% all-in. Compare that to a percentage-based processor at 2.9% + $0.30, where the same merchant would pay roughly $5,800 (2.9%) + $5,100 (transaction count × $0.30) = ~$10,900 on $200K, or 5.5% all-in. The Stax breakeven against a 2.9% + $0.30 processor lands somewhere around $90,000–$120,000 in annual volume, depending on average ticket size. Below that, percentage pricing is cheaper. Above that, the subscription model compounds savings as volume grows.

For ISVs, that math has a specific implication: Stax Connect economics work when sub-merchants are concentrated in the >$150K-annual-volume band where the subscription model genuinely beats percentage pricing. ISVs with SMB sub-merchant bases below that threshold will find merchants pushing back on the monthly fee. ISVs with mid-market sub-merchants find Stax Connect lands in the right zone — the $199+ enterprise tier scales well for $1M+ annual processors.

NMI: gateway fees plus acquirer-side interchange (separate)

NMI’s commercial model splits the economics across two layers that other platforms bundle. The gateway layer charges the ISV a per-transaction gateway fee plus monthly platform fees, both partner-negotiated and not publicly published. The actual interchange-plus economics live with whichever acquirer the merchant settles through — NMI does not take interchange itself, since it doesn’t acquire.

For ISVs, this produces a meaningful margin difference. The bundled-economics platforms (Stax’s full-stack model, Adyen for Platforms, Stripe Connect’s flat platform fee) give the ISV a single number to negotiate and a single contract to sign. NMI’s split-economics model gives the ISV genuine acquirer arbitrage — different acquirers, different geographies, different vertical specializations, all behind the same NMI integration — but requires managing two separate commercial relationships.

The trade-off shows up most acutely in price-stability risk. Multiple Trustpilot reviewers in NMI’s reseller and ISO tier — including one in January 2026 (“This is the 3rd or 4th time with surprised increased pricing, into the thousands… corporate decisions with people clients can not communicate with”) and another in early 2025 documenting “Mandatory Year End operating fees” that don’t appear on any published rate sheet — describe the same pattern: opaque pricing changes propagating down through partners. ISVs building on NMI need to model that residual risk explicitly in partner SLAs, since the rate-change clauses control whether merchant economics stay stable across renewal cycles.

For ISVs with sophisticated payments teams or multi-vertical merchant bases, the split-economics model is a feature. For ISVs that want one vendor, one contract, and a managed-services experience, it’s friction. Both pricing pages cover the model architecture rather than specific basis points: the Stax pricing breakdown and the NMI pricing model walk the structure for each platform.

Integration Architecture

For ISVs, the integration story isn’t just API quality — it’s the operational model the platform enforces around merchant onboarding, fund settlement, and dispute handling.

Stax Connect: managed onboarding under one vendor

Stax Connect exposes APIs for merchant creation, payment processing, and reporting, but the operational model is more managed than developer-self-serve. The Stax Connect Plus tier in particular is designed so the ISV doesn’t run its own merchant onboarding workflow at all — Stax’s sales team and merchant-success team carry the onboarding load, and the ISV’s role is largely to refer merchants and collect rev-share.

For ISVs that want to ship payments fast without building an internal payments team, this is a useful model. The trade-off is that Stax owns the merchant relationship in operational terms — Stax is the contracting entity for the merchant, the underwriting decision-maker (with sponsorship from Fifth Third/Synovus/Elavon), the funds-flow operator, and the support owner. ISVs trade integration speed and operational simplicity for less control over the underwriting decisions and merchant communications.

The technical integration surface is genuinely modest. Stax publishes REST APIs and a developer documentation site, with SDKs and a card-tokenization layer for ISVs that want to handle their own checkout UX. The vertical-SaaS use cases Stax is built for — field-service software, healthcare practice management, legal billing, education platforms — typically don’t need deep payments customization beyond the basics, which is why the managed model fits the customer base well.

NMI Merchant Central: the multi-acquirer ISO/PayFac console

NMI’s integration story for ISVs centers on Merchant Central — the residual management, agent payout, marketing automation, and merchant onboarding hub that lets an ISV (or its partnered ISO) run sub-merchant operations across multiple acquirer relationships from one interface. The case study on ISVPay, an Alpharetta, Georgia ISO focused on unattended-payments ISVs, describes how Merchant Central’s TurboApp portal centralized the entire merchant onboarding workflow through a single console.

Behind Merchant Central, ScanX/MonitorX runs the underwriting automation — 100+ risk checks per merchant application with risk-scored decisioning in minutes rather than days. That’s the engine that makes the NMI embedded-payments pitch operationally credible for ISVs that don’t want to register as their own payment facilitator.

The integration model gives the ISV more control over the underwriting decision (especially when working with a partnered ISO that can adjust risk thresholds per vertical) at the cost of a less opinionated workflow. ISVs that want a self-serve sub-merchant signup flow have to build it on top of NMI’s APIs; Stax Connect Plus’s managed onboarding is closer to ready out of the box.

Revenue Sharing & PayFac Models

Both platforms support revenue share for ISVs — it’s the central monetization promise of any embedded-payments integration — but the mechanics are different.

Stax Connect offers what the company describes as “generous, tailor-made revenue-sharing programs” with no published rate card. Specifics are negotiated per ISV based on expected sub-merchant volume, vertical fit, and the chosen partnership tier (Connect Plus, Reseller, or Custom). The economics work cleanly because Stax owns the entire stack — there’s only one set of margins to split, and the ISV’s rev-share comes out of the spread between merchant pricing and Stax’s own cost basis. For ISVs at $10M+ in expected platform GMV, the Connect Plus model can produce ISV rev-share north of 20–30 basis points on volume; smaller ISVs typically settle into a referral-style revenue split closer to 10–15 basis points.

NMI’s partner model is more traditional ISO economics, dressed for the ISV era. The ISV (or its partnered ISO) earns a markup on the gateway fee plus a negotiated rev-share on the acquirer-side interchange. The economics are highly negotiable because they’re stitched together across two relationships, and ISVs with leverage on either side (high volume, vertical specialization, growth trajectory) can usually do better than the published partner-tier rates of bundled platforms.

The architectural difference is whether the PayFac-as-a-Service economics live with one vendor (Stax) or are assembled across two (NMI + acquirer). ISVs that want the simpler revenue accounting often pick Stax Connect. ISVs that want maximum negotiating leverage often pick NMI.

White-Label Control

This is where NMI most clearly outperforms Stax for ISVs that need brand invisibility.

Stax Connect offers white-label capability but ships with co-branded defaults. Stax’s brand surfaces in merchant documentation, merchant statements, support communications when escalations route to Stax’s team, and the underlying merchant dashboard if sub-merchants are given direct access to Stax-hosted reporting. The platform can be heavily customized to minimize Stax visibility, but the practical reality of running Stax Connect Plus is that Stax’s name appears in enough places that it’s effectively a co-branded experience for the sub-merchant. ISVs running Stax Connect Custom can push white-label deeper, but the managed-services tier where most ISVs land has Stax visibility baked in.

NMI ships with full white-label as the default. Partners can run an end-to-end embedded payments experience with NMI nowhere on the merchant-facing surface — no brand on checkout, no logo on settlement reports, no name on dispute notifications. The ISV’s brand owns the merchant relationship completely.

For ISVs whose competitive positioning depends on owning the merchant brand experience (vertical SaaS where the merchant has chosen the ISV as their primary platform; embedded payments where the payments experience must feel native), NMI’s white-label depth is a meaningful differentiator. For ISVs where the payments brand is less load-bearing (vertical SaaS where the customer already accepts that “powered by Stax” is a reasonable trust signal), Stax’s co-branded defaults are not a buying objection.

Geographic Reach

Both platforms are US-anchored. NMI has meaningfully more international footprint than Stax.

Stax operates as a US-domestic platform. The acquiring relationships with Fifth Third, Synovus, and Elavon cover US merchants only; there is no native acquiring outside the US. ISVs with international sub-merchants need a separate processing arrangement for those merchants, which negates the one-vendor benefit. For US-only ISVs, that’s a non-issue. For ISVs with even modest international expansion plans, it’s a structural ceiling.

NMI operates as a US-anchored gateway with explicit UK, EU, and Republic of Ireland coverage through its UK entity (Network Merchants Limited). The 300+ EMV device certifications cover all four geographies with locally certified hardware. Beyond US/UK/EU/ROI, NMI depends on its partnered acquirers for additional geographic reach — the gateway model means international expansion is an acquirer-relationship decision, not an NMI-platform decision.

The practical translation for ISVs: if your sub-merchants are concentrated in the US, both platforms work. If your sub-merchants need UK/EU/Ireland coverage, NMI’s gateway-first model handles it natively while Stax requires a parallel processing arrangement. If your sub-merchants are heavily international beyond Anglo markets, neither Stax nor NMI is the right primary platform — that’s the Adyen or Stripe Connect conversation.

Onboarding Friction & Sub-Merchant Approval

Both platforms run real KYC, AML, and MATCH-list checks — that’s not negotiable in regulated payments. The difference is in approval velocity and the ISV’s role in the underwriting decision.

Stax Connect runs underwriting through Stax’s own merchant operations team, with sponsorship-bank approval via Fifth Third/Synovus/Elavon. The Connect Plus tier’s managed-services framing means Stax handles the merchant communication during onboarding; the ISV’s job is to refer the merchant and let Stax run the workflow. ClientTether’s case study describes the operational improvement directly: the ISV’s merchant application close rate hit 67% and support ticket volume dropped 70% after adopting Connect Plus, because the ISV stopped owning the support-and-onboarding burden. Onboarding velocity is good but not differentiated from peer subscription processors — typical timelines are 1–5 business days for standard merchants, longer for higher-risk verticals.

NMI’s TurboApp through Merchant Central is engineered for fast decisioning. The published ISVPay case study reports a best-month performance of 98.2% approval rate, 91% same-day approval, 92.8% activation within 15 days, and 97.7% retention for sub-merchants flowing through TurboApp. ISVPay’s VP of Customer Experience Lacey Frenzl described the workflow shift directly: “We’re no longer sending PDFs back and forth or chasing down wet signatures — there are no delays. When the merchant submits their application through the ISV, it reaches us instantly. We review and audit the forms, then submit everything through TurboApp, with approvals often coming back within hours.” That data is filtered through an ISO intermediary rather than a direct ISV-to-NMI integration, but it’s the most concrete published evidence on either platform’s onboarding throughput.

For ISVs serving SMB-heavy sub-merchant bases, NMI’s TurboApp model is structurally faster on the published numbers. For ISVs serving mid-market sub-merchants where the activation path is more relationship-driven and the merchant is willing to wait a few days for sponsorship-bank review, Stax Connect Plus’s managed approach is the right shape.

Customer Support Reality

Both platforms carry support reputation patterns that ISVs need to underwrite honestly.

Stax runs a US-based support team with the marketing emphasis on a “white-glove” service model. The Connect Plus tier explicitly puts Stax’s own support team in front of merchant escalations, which is the source of ClientTether’s 70% support-ticket reduction — the ISV stops absorbing payment-support load and Stax does. Stax’s published customer-support hours and channels are reasonable for the SMB and mid-market verticals the platform serves. The constraint shows up at scale: as sub-merchant counts grow into the hundreds and thousands, the managed-support model gets stretched, and ISVs at that tier sometimes report longer response times than the brand promise.

NMI’s support quality varies significantly with the partnered ISO/PayFac. Direct merchants who reach NMI itself often report transferred-and-held experiences; merchants supported by their partnered ISO get a more personal touch but quality depends entirely on the partner. The unclaimed Trustpilot profile (2.0/16) shows recurring patterns around customer support unresponsiveness, surprise pricing changes, and billing-after-cancellation that ISVs need to plan support content for.

For ISVs running either platform, the same mitigation applies: position your own support team in front of every sub-merchant flow so merchants reach the ISV’s escalation path before they reach the gateway’s.

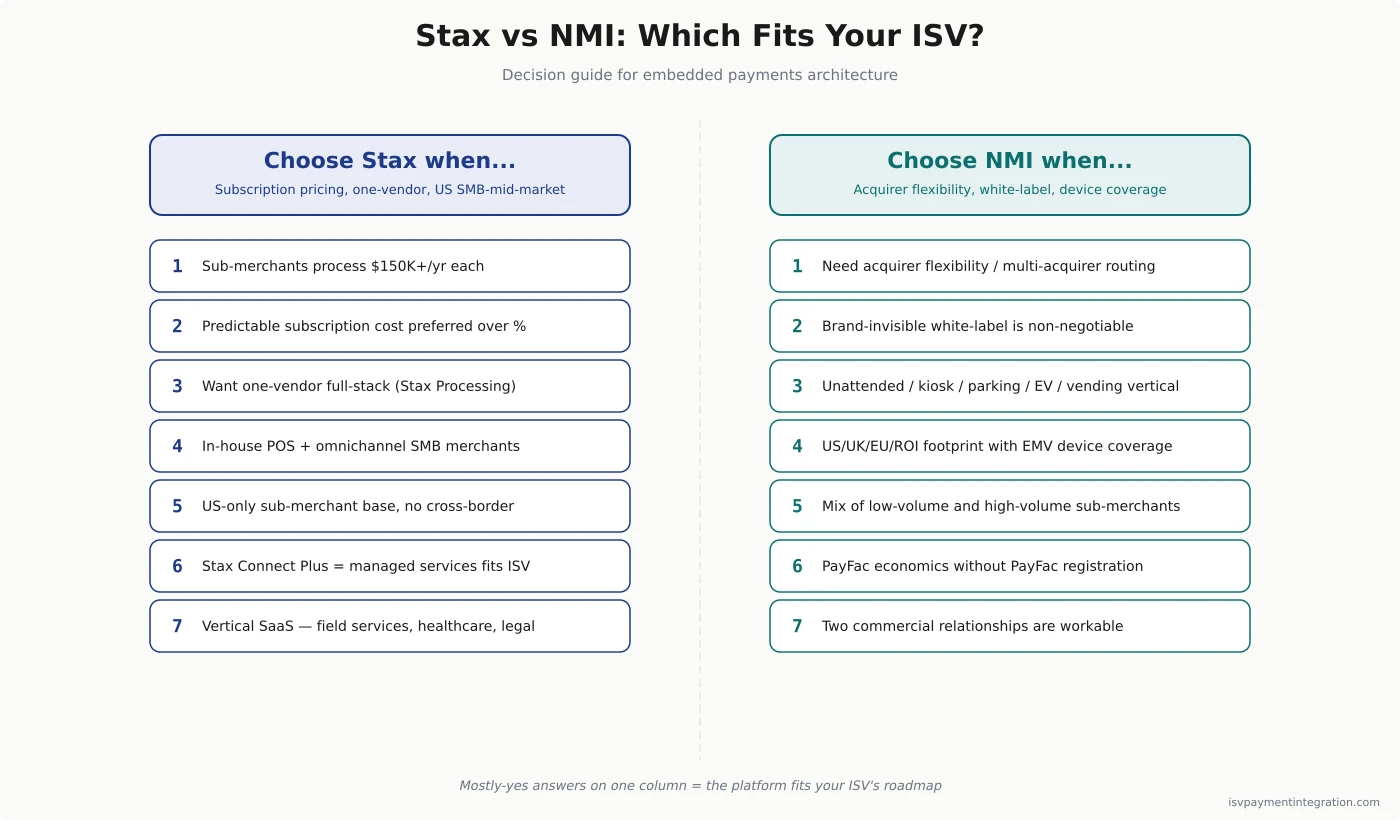

When Stax Wins for ISVs

Stax Connect is the right pick when the ISV’s profile matches what the platform is built for:

- Vertical SaaS with mid-market sub-merchants — field services, healthcare practice management, legal billing, education, professional services, non-profit. Stax Connect’s case studies (ChiroSpring, ClientTether, Sera) cluster in exactly this territory because the merchant ticket size and SaaS-led GTM motion fit subscription pricing

- Sub-merchant base concentrated above $150K annual processing volume where the subscription model genuinely beats percentage pricing

- US-domestic merchant base only — Stax’s acquiring relationships cover US merchants; there is no native international acquiring

- One-vendor accountability is required — finance teams that need a single statement, single contract, single point of escalation

- Managed-services preference — ISVs that want Stax’s own team running merchant onboarding and support rather than building an in-house payments operations function. Stax Connect Plus is built for exactly this profile

- Predictable cost is a sales asset — vertical SaaS where the merchant pricing pitch includes “no surprise rate increases, fully transparent monthly cost”

The post-October-2025 Stax Processing launch matters here. Before October 2025, Stax was a subscription processor riding pass-through acquirer infrastructure — a model that worked but had structural constraints. After the launch, Stax operates its own technology stack, which closes a gap with bundled platforms like Stripe Connect and Adyen for Platforms. For ISVs evaluating Stax in 2026, the architecture is more competitive than it was in 2024, and the Forrester-cited 141% ROI and ~$900K incremental revenue numbers reflect that updated picture (with the caveat that those are Stax-commissioned numbers, not independent benchmarks).

When NMI Wins for ISVs

NMI is the right pick when the ISV values acquirer flexibility, brand control, or device coverage above one-vendor convenience:

- ISOs and ISVs with multi-acquirer requirements — the ability to swap or layer acquirers behind a single gateway integration is operationally meaningful, especially for ISVs with merchants that have been impacted by acquirer M&A (Worldpay → Global Payments, First Data → Fiserv)

- Unattended, self-service, kiosk, transit, parking, EV-charging, vending verticals where NMI’s 300+ EMV device estate (Ingenico, ID TECH, Madic, Payter, FEIG, LANDI) is structurally hard to replicate

- Brand-critical embedded payments — vertical SaaS, white-label PFaaS, embedded-payments-as-a-feature where the ISV’s brand has to own the merchant relationship completely

- Multi-region without re-architecture — US/UK/EU/Republic of Ireland coverage from one gateway integration with locally certified device estates

- Partner-enabled PFaaS economics — NMI’s white-label embedded payments model lets ISVs earn rev-share without registering as their own PayFac, with named ISO references like Wind River Financial, ISVPay, and Anovia Payments

- Mixed sub-merchant volume profiles — NMI’s gateway fees scale with transaction count, not with subscription thresholds, so low-volume sub-merchants don’t get penalized by a monthly fee that doesn’t pay back

For an ISV that fits this profile, NMI is the gateway most likely to match the next five years of platform evolution — the multi-acquirer optionality compounds in value as the ISV’s merchant base diversifies. Steven Pinado’s appointment as CEO in September 2025 reinforces the direction: his background includes board seats at Helcim (a direct-to-merchant acquirer with strong SMB ISV tooling) and Browzwear (3D fashion software), plus prior roles at Billtrust and Constellation Payments. The Helcim seat in particular signals NMI’s intent to compete more aggressively for ISV software partners under the new regime, not just ISO resellers.

NMI’s January 2026 year-end disclosure also previewed the next product surface: Tap to Pay (NFC mobile acceptance), AI-powered fraud and risk tools, and Embedded Lending — the company’s direct response to Adyen Capital and Stripe Capital. The lending product lets ISVs offer merchant capital inside their own software, repaid against future payment volume.

How They Compare to Other Alternatives

Both Stax and NMI exist in a competitive set that ISVs should benchmark against at least one or two other platforms before committing.

vs Stripe Connect — Stripe Connect is the default for SaaS platforms that want bundled gateway/acquirer/risk and best-in-class developer ergonomics across the broadest geography. Stax wins on subscription-pricing economics for high-volume merchants and managed-services ISV onboarding through Connect Plus; Stripe Connect wins on developer self-serve speed, global reach, and the breadth of the platform’s product surface (Treasury, Capital, Issuing). NMI wins when acquirer flexibility, multi-acquirer routing, or unattended-payments device coverage matter more than developer-tooling polish. See NMI vs Stripe and Stripe vs Stax for the head-to-heads.

vs Adyen — Adyen is the enterprise-tier full-stack acquirer with 33+ countries of direct acquiring and an embedded-finance suite. Both Stax and NMI sit below Adyen’s volume floor — Stax wins the SMB-to-mid-market US-domestic ISV; NMI wins the multi-acquirer or unattended-vertical ISV. See Adyen vs Stax and Adyen vs NMI.

vs Authorize.Net — The other major US gateway brand, owned by Visa via the 2010 CyberSource acquisition. Authorize.Net’s product velocity has been described as steady-state under Visa stewardship, while NMI’s PE-backed acquisitive growth produces faster product churn. ISVs valuing stability often pick Authorize.Net; ISVs valuing modular growth pick NMI. Stax’s subscription model is closer to Helcim’s positioning than to Authorize.Net’s per-transaction gateway model.

vs Fiserv / Global Payments / Worldpay — Full-stack acquirers with their own embedded-payments products (Carat, Genius, Worldpay for Platforms). The choice between a full-stack acquirer and Stax depends on US-domestic vs international scope and vertical specialization; the choice between a full-stack acquirer and NMI is whether the ISV wants single-vendor accountability (the acquirer) or unbundled flexibility with an independent gateway (NMI). NMI also supports merchants settled by all three of these acquirers — the question is one of commercial structure, not technical compatibility.

vs Payrix / Tilled / Finix — Newer PayFac-as-a-Service platforms positioned for vertical SaaS embedded payments. Payrix is now owned by Worldpay (inside Global Payments) after the January 2026 Worldpay → Global Payments acquisition closed. Tilled is independent. Finix is platform-first with no minimum-invoice friction. Stax Connect competes most directly with these PFaaS platforms on the ISV-monetization story; NMI competes from the gateway-plus-acquirer side. See Payrix vs Stax for the closest peer comparison.

Final Verdict by ISV Use Case

For most ISVs, the decision between Stax and NMI comes down to four binary questions. Each one points decisively to one platform or the other.

| Question | If yes → | If no → |

|---|---|---|

| Are sub-merchants concentrated above $150K annual processing volume? | Stax (subscription pricing pays back) | NMI (per-txn gateway fits low-volume too) |

| Does the ISV want fully managed merchant onboarding and support? | Stax Connect Plus (Stax runs the workflow) | NMI (ISV or ISO owns the workflow) |

| Is the ISV’s brand expected to be invisible behind the merchant experience? | NMI (full white-label default) | Stax (co-branded acceptable) |

| Does the ISV need acquirer flexibility (multi-acquirer routing, unattended vertical)? | NMI (200+ acquirer connections) | Stax (single-vendor simpler) |

For ISVs that answer yes to the first two questions, Stax Connect is structurally the right platform — the subscription pricing economics and the managed-services tier are hard to replicate elsewhere. For ISVs that answer yes to the second two questions, NMI’s gateway-first model is the right fit — the multi-acquirer flexibility and white-label depth are hard to replicate with a bundled platform.

For ISVs in the middle — domestic US, mid-market merchants, brand-flexible, single-acquirer comfortable — the decision usually comes down to whether the ISV wants to run its own payments operations (NMI through a partnered ISO) or hand that operational load to the platform (Stax Connect Plus). That choice is more about institutional fit than technical capability.

Frequently Asked Questions

Who are Stax’s competitors?

Stax’s direct competitors are subscription-pricing payment processors and full-stack ISV platforms. The closest peers are Helcim (subscription-style direct-to-merchant acquirer with strong SMB ISV tooling), Payment Depot (now part of Stax’s competitive set under Greater Sum Ventures’ broader portfolio), and the emerging vertical-SaaS PayFac providers Payrix (now Worldpay for Platforms inside Global Payments), Tilled, and Finix. On the bundled-platform side — vendors that compete with Stax by offering a different model — the competitive set includes Stripe Connect, Adyen for Platforms, Square (for SMB), and the major full-stack acquirers (Fiserv/Clover, Global Payments/Genius, Worldpay/Worldpay for Platforms). For ISVs specifically, the Stax Connect vs Stripe Connect decision is the most common live evaluation.

Who are NMI’s competitors?

NMI’s direct competitors are other gateway-first platforms: Authorize.Net (Visa-owned, longest-tenured US gateway), Braintree’s gateway layer (PayPal-owned), and to a lesser extent Spreedly (which positions more as a payment orchestration layer than a gateway proper). On the bundled-platform side, NMI competes against Stripe Connect, Adyen for Platforms, Stax Connect, and the major full-stack acquirers offering ISV programs.

What is Stax Connect and how does it work for ISVs?

Stax Connect is Stax’s embedded-payments program for ISVs, launched in 2020. It sells in three commercial flavors — Stax Connect Plus (fully managed by Stax’s team), Reseller Model (ISV runs sales, Stax provides marketing and back-end support), and Custom Pricing (ISV sets merchant pricing on top of the Stax platform). Revenue share is negotiated rather than published, with Stax describing its rev-share programs as “tailor-made.” Named ISV partners include ChiroSpring, ClientTether, and Sera, with a Forrester-commissioned ROI study citing 141% ROI and ~$900K incremental revenue (Stax-commissioned, not independent). The program is best-fit for vertical SaaS with mid-market US-domestic sub-merchants in field services, healthcare, legal, non-profit, education, and professional services.

Is Stax its own processor or does it sit on Worldpay/Fiserv?

Both, depending on how you frame the question. As of October 2025, Stax operates Stax Processing, an in-house full-stack processing capability built on its acquisitions of Atlantic-Pacific Processing Systems (APPS) and BlockChyp. This means Stax now handles the technology stack from origination through clearing and settlement on its own infrastructure, with direct connectivity to Visa, Mastercard, Discover, and Amex OptBlue. However, Stax is not its own acquiring bank — only banks can hold direct card-network membership — so Stax remains registered as an ISO/MSP under Fifth Third Bank, Synovus Bank (Pinnacle Bank dba Synovus), and Elavon (a wholly-owned subsidiary of U.S. Bancorp). The accurate framing for ISVs: Stax owns the technology stack but operates under bank sponsorship for card-network access. That is the standard model for full-stack non-bank processors.

Can an ISV use both Stax and NMI?

Yes — and some ISVs do exactly this. The split usually maps to merchant tier or vertical: Stax Connect handles mid-market US-domestic sub-merchants where the subscription pricing pays back and the managed-services tier reduces operational load; NMI handles unattended-vertical merchants, multi-acquirer requirements, or merchants where the ISV’s brand has to own the experience completely. The trade-off is operational complexity — running two payments stacks doubles the integration surface, the reconciliation work, and the support training. For most ISVs, the right answer is to pick one and grow on it; the dual-platform approach makes sense only when the merchant base is large enough and bifurcated enough to justify the overhead.

Does NMI work outside the United States?

Yes, in the United Kingdom, the European Union, and the Republic of Ireland through NMI’s UK entity, Network Merchants Limited. The 300+ EMV device certifications cover all four geographies with locally certified hardware. Beyond US/UK/EU/ROI, NMI depends on its partnered acquirers for additional geographic reach. For ISVs with sub-merchants concentrated in Anglo markets, NMI’s coverage is sufficient. For ISVs with broader international exposure, the gateway-first model can still work but requires additional acquirer relationships.

What to Do Next

The verdict is already at the top of this page. The four-question table in the section above narrows the answer to one platform for most ISVs. What remains is execution. A short checklist for whichever direction the decision pointed.

If Stax is the answer, request a Stax Connect quote through the Stax Connect partner contact rather than the generic sales path — the Connect team handles ISV evaluations differently and will ask for sub-merchant volume projections, vertical mix, and your preferred partnership tier (Connect Plus, Reseller, or Custom Pricing) in the first call. Bring three numbers to the meeting: expected platform GMV in year one, the SMB-vs-mid-market split of your sub-merchant base, and your ISV’s appetite for managed services vs self-service. Specify which Stax Connect tier you want quoted, since the rev-share economics and the ISV-side operational load differ meaningfully across the three tiers. Reference the ChiroSpring, ClientTether, and Sera case studies as benchmarks for what your ISV’s outcome could look like at scale.

If NMI is the answer, the path is rarely direct. Most ISVs sign NMI through a partnered ISO or PFaaS provider — names worth contacting include Wind River Financial, Anovia Payments, or any of NMI’s named tier-1 ISO partners listed under Merchant Central case studies. Bring two questions to that conversation: what acquirer the ISO routes through for your sub-merchant profile, and what the rate-change notification clause looks like in the partner SLA. The reseller-tier surprise-pricing pattern documented in this comparison is real; the mitigation is contractual, not editorial.

If both should compete head-to-head, run the same 90-day evaluation against each: the same target sub-merchant cohort, the same volume assumptions, the same embedded-payments user story. Score against the feature comparison matrix at the top of this page and the decision guide above. The exercise usually surfaces a clear winner inside three sales conversations.

For deeper fee mechanics, see the Stax pricing breakdown and NMI pricing model. For the third option in this market, NMI vs Stripe, Stripe vs Stax, and Adyen vs NMI cover the major adjacent comparisons from each side.