PayPal Pricing

Pricing model: Flat-rate (with PPCP revenue share for platforms). Based on publicly available information from PayPal's official site. Contact PayPal directly for ISV-specific pricing.

Fee Breakdown

| Fee Type | Details |

|---|---|

| Processing | PayPal Checkout 3.49% + $0.49; Standard Card 2.99% + $0.49; Venmo 3.49% + $0.49; Pay Later 4.99% + $0.49; QR 2.29% + $0.09 |

| Markup | Flat-rate (no interchange passthrough). PPCP platforms negotiate rev-share on aggregate volume. |

| Setup | No setup fee for standard accounts; PPCP onboarding negotiated |

| Monthly | $0 standard; PayPal Payments Pro $30/mo; Invoice Subscription $14.99/mo |

Hidden Costs to Watch

- ⚠ Cross-border surcharge: +1.50% on every international commercial transaction

- ⚠ Currency conversion: 3-4% spread above the mid-market exchange rate

- ⚠ Chargeback fee: $20 per dispute, regardless of outcome

- ⚠ Standard dispute fee: $15 (escalating to $30 for high dispute-rate accounts)

- ⚠ Pay with Venmo and Pay Later sit at 3.49-4.99% — well above standard card rates

- ⚠ PayPal can hold funds in reserve (rolling or fixed) on new or high-risk accounts

- ⚠ APMs (alternative payment methods) range 2.89-5.49% + fixed fee depending on provider

Alternatives

What ISVs Actually Pay PayPal in 2026

PayPal’s published rates look simple. The real cost rarely matches the headline.

If you’re an ISV embedding PayPal into your software, the number that matters isn’t the list rate your merchants see — it’s the all-in cost basis after cross-border surcharges, currency spreads, chargeback fees, and the rate gap between standard cards and the branded PayPal Checkout button. Get those wrong in your pricing model and you’ll either erode your margin or overcharge merchants who notice.

This page lays out every PayPal fee that touches an ISV deal in 2026, where the hidden costs hide, and how the PayPal Complete Payments (PPCP) platform changes the math for software companies sharing in payment revenue.

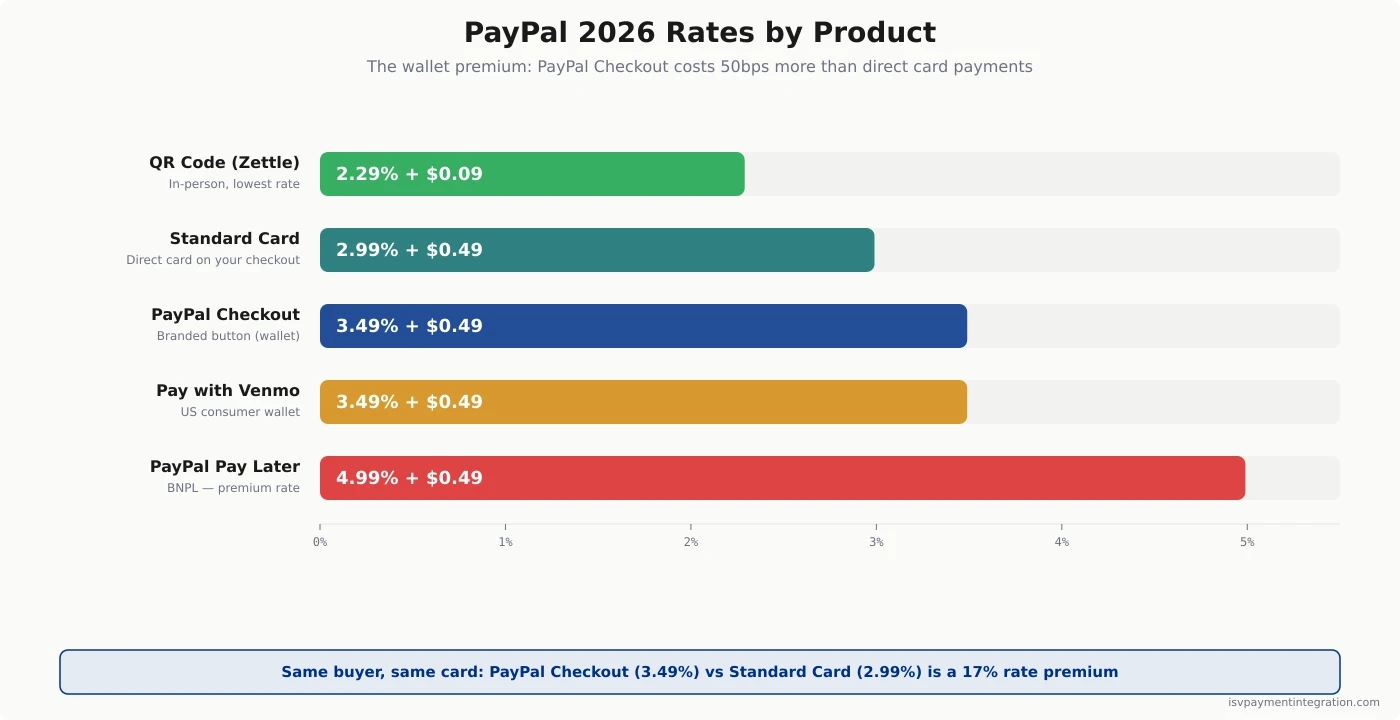

PayPal’s 2026 Processing Rates at a Glance

PayPal runs a flat-rate model across most products. There’s no interchange passthrough on standard plans — you pay the posted rate, regardless of card type or category.

| Product | Rate | Fixed Fee |

|---|---|---|

| PayPal Checkout (branded button) | 3.49% | $0.49 |

| Standard Credit/Debit Card | 2.99% | $0.49 |

| Pay with Venmo | 3.49% | $0.49 |

| PayPal Pay Later | 4.99% | $0.49 |

| QR Code (in-person, Zettle) | 2.29% | $0.09 |

| Send/Receive Goods & Services | 2.99% | varies |

| Alternative Payment Methods (APMs) | 2.89-5.49% | + fixed fee |

| International add-on | +1.50% | (on top of domestic rate) |

| Currency conversion | 3-4% spread | (above mid-market) |

Source: PayPal Merchant Fees (April 2026). Rates apply to US merchants; non-US accounts have their own schedules.

The line ISVs miss most often: PayPal Checkout costs 50 basis points more than direct card payments. That’s not a typo — the branded yellow button is meaningfully more expensive than the same buyer paying with the same card through your standard checkout.

PayPal Checkout vs Standard Card Rates: Why the Gap Matters

The 50-basis-point gap between Checkout (3.49%) and Standard Card (2.99%) is intentional. PayPal charges a premium for the wallet experience because the wallet drives conversion lift.

When PayPal Checkout fires

When a buyer clicks the PayPal button, they authenticate inside PayPal’s flow and can pay with their PayPal balance, a linked bank, or a stored card. The transaction routes through PayPal’s wallet stack and bills at 3.49% + $0.49.

Why standard cards are cheaper

When a buyer types a card number directly into your checkout form (using PayPal as the processor under the hood), the transaction routes as a standard card payment and bills at 2.99% + $0.49. Same network, same card, lower rate.

What this means for ISV pricing models

Most ISVs surface both options. The mix of Checkout vs Standard determines your blended rate. A merchant with a 60/40 split of Checkout to Standard Cards pays a blended 3.29% + $0.49 — not the 2.99% they thought they were getting.

Build your pricing model around blended rate, not headline rate. If you don’t know what your merchants’ blended rate looks like, pull six months of transaction-level data and segment by funding instrument before you quote anyone.

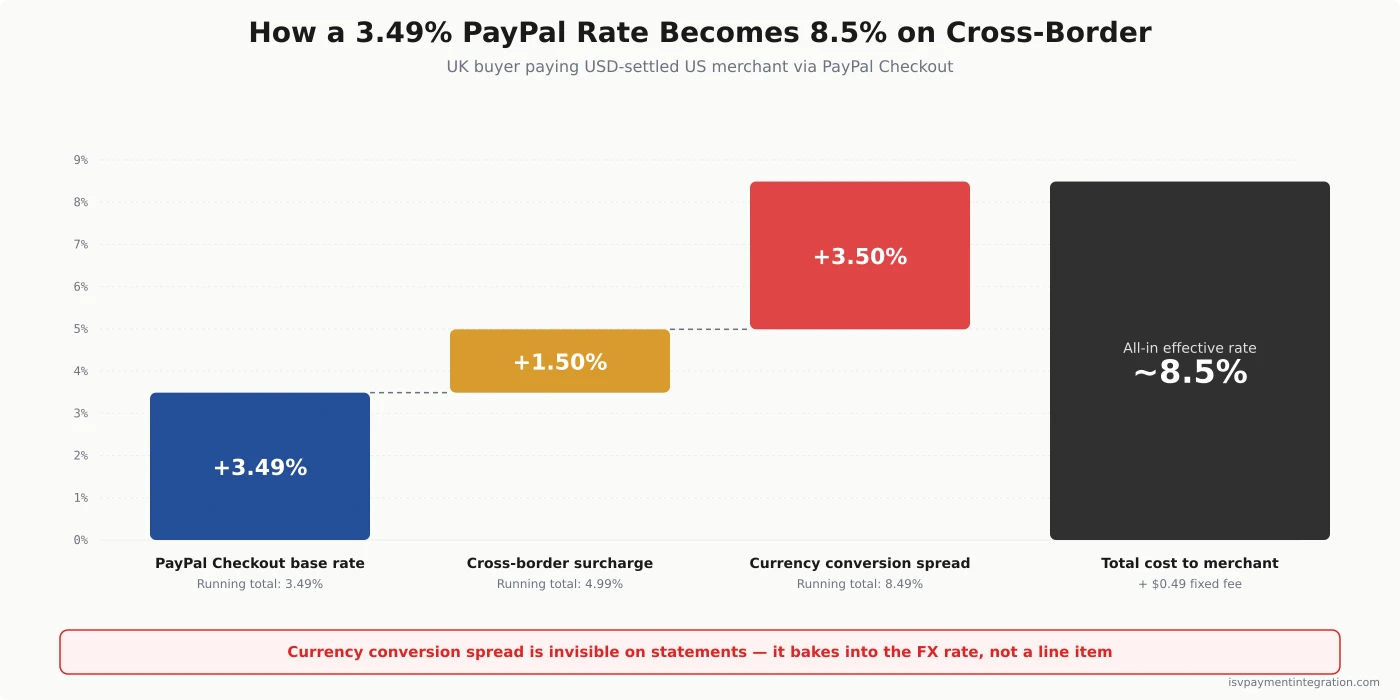

International & Currency Conversion Fees

Cross-border is where PayPal pricing turns from “expensive but predictable” to “easy to under-budget.” Two surcharges stack on top of the domestic rate.

Cross-border surcharge: +1.50%

Every commercial transaction where the buyer’s country differs from the merchant’s account country adds 1.50% to the rate. A US merchant taking a card from a UK buyer pays 2.99% + 1.50% + $0.49 = 4.49% + $0.49 on a standard card transaction. On PayPal Checkout, the same transaction bills at 4.99% + $0.49.

Currency conversion: 3-4% above mid-market

When PayPal converts the transaction currency to your settlement currency, it applies a spread of roughly 3% to 4% above the mid-market exchange rate. That spread is invisible on the statement — it shows up as an FX rate, not a line item.

A 100 GBP transaction settling to USD doesn’t convert at the Reuters spot rate. It converts at PayPal’s rate, and the 3-4% delta gets baked into the dollar amount you receive.

The spread is wider on emerging-market currency pairs. For USD↔INR and similar pairs, independent analyses document effective FX markups exceeding 8% once the cross-border surcharge stacks on top. ISVs serving merchants in South or Southeast Asia should model the actual currency-pair spread, not the 3-4% headline.

PayPal converts inbound foreign-currency payments to the account’s base currency by default. Merchants who don’t actively configure “hold balance in original currency” pay the spread on every inbound payment without a clear opt-out prompt at the transaction level.

Worked example

A US ISV’s UK merchant takes a 200 GBP order via PayPal Checkout and settles to USD:

- Headline rate: 3.49% + $0.49

- Cross-border surcharge: +1.50%

- Currency spread: ~3.5% baked into the FX rate

- Effective all-in cost: roughly 8.5% of the transaction value

For ISVs serving merchants with meaningful international volume, this is the single biggest gap between PayPal’s marketing and PayPal’s reality.

Chargeback, Dispute & Refund Fees

PayPal charges per dispute, not per loss. Whether you win or lose, the fee applies.

- Chargeback fee: $20 per case, regardless of outcome

- Standard dispute fee: $15 (PayPal-mediated disputes, not card network chargebacks)

- High-volume dispute fee: $30 for accounts with elevated dispute rates (above ~1.5% of volume)

- Refund fee policy: PayPal returns the percentage portion of the original fee but keeps the fixed $0.49 per transaction

For ISVs in higher-risk verticals — events, travel, subscription services, digital goods — dispute exposure can exceed processing cost. A 1% dispute rate on $100 average tickets means $20 in fees per dispute, or 20% of the transaction value, on top of the original processing cost.

Build dispute fees into your merchant pricing if you serve any vertical above 0.5% chargeback rate. Otherwise the math eats your revenue share.

Monthly Plans: Payments Pro, Payflow, Invoicing

PayPal’s monthly subscription products are largely legacy at this point, but they still appear on direct-merchant statements.

PayPal Payments Pro: $30/month

The hosted virtual terminal and recurring billing add-on for direct merchants. Payments Pro doesn’t change the per-transaction rate — it adds capabilities (card-on-file, virtual terminal, recurring profiles) on top.

Payflow Pro

The legacy gateway product, still supported but rarely the right choice for new integrations. ISVs should look at PPCP or Braintree (PayPal’s developer-first acquirer) instead.

Invoice Subscription Service: $14.99/month

For merchants sending a high volume of invoices through PayPal. Removes the per-invoice fee cap and adds reporting features.

For ISVs: skip these. PayPal Payments Pro and the legacy Payflow products predate the modern platform offering. PPCP is the right starting point for any ISV building today.

In-Person & QR Code Rates (Zettle / PayPal POS)

PayPal’s in-person business runs through Zettle, the European POS company PayPal acquired in 2018.

- Zettle card-present: 2.29% + $0.09 per tap, dip, or swipe

- QR code payments: 1.90% + $0.10 (lowest published rate in PayPal’s stack)

- Manually-entered cards (in-person): 3.49% + $0.09 — same as keyed-not-present rates

- Hardware: Zettle terminals run $29 to $199 depending on model

For ISVs serving merchants with omnichannel needs (in-person + online), Zettle’s rates are competitive with Square (2.6% + $0.10 in-person) and Stripe Terminal (2.7% + $0.05). The integration is separate from PPCP — in-person and online sit on different stacks inside PayPal.

Hidden Costs ISVs Should Budget For

Beyond the per-transaction line, these are the costs that catch ISVs after the contract is signed.

Reserves on new or high-risk accounts. PayPal can hold a rolling reserve (typically 5-15% of volume held for 30-180 days) or a fixed reserve on accounts in higher-risk verticals or with limited processing history. For ISVs onboarding sub-merchants, expect reserve policies to apply on accounts under three months old or with elevated dispute rates.

PCI compliance scope. If your integration handles cardholder data (rather than tokenizing through PayPal’s hosted fields), your PCI scope expands. That means SAQ D instead of SAQ A, plus quarterly ASV scans and annual penetration tests. Budget $5-50K annually depending on scope.

Integration & maintenance. Initial PPCP integration runs 80-200 engineering hours depending on scope (cards-only vs full wallet + Pay Later + Venmo). Annual maintenance for SDK updates, API version migrations, and feature additions runs another 20-60 hours.

Pay Later and Venmo premium rates. These products bill at 4.99% and 3.49% respectively — well above the standard card rate. If your merchants enable them by default, your blended rate climbs without anyone deciding to make it climb.

Funds availability delays. PayPal can place transaction holds (typically 21 days) on new accounts or accounts with sudden volume changes. ISVs should communicate this clearly to sub-merchants — surprise holds drive churn.

APM premium pricing. Alternative payment methods (Klarna, iDEAL, Bancontact, Sofort) bill at 2.89% to 5.49% depending on the provider. If you enable APMs for international reach, audit the per-method rate before turning them on.

The micropayments plan is closed to ISV-onboarded merchants. PayPal’s micropayments rate (5% + $0.05, optimal for transactions under ~$12) is only available on accounts opened directly with PayPal. Business accounts created through a third-party platform — i.e., any merchant your ISV onboards via PPCP — are excluded entirely (source: PayPal micropayments help). For ISVs serving merchants with high-volume small-ticket transactions (digital goods, in-app purchases, tip jars), this is a structural cost ceiling competitors should know about.

Recent Fee Changes ISVs Should Know About

PayPal has raised rates twice in the last 14 months without advance notice windows for existing merchants:

- Jan 2025: Virtual Terminal jumped from 2.39% → 3.39% (a 42% relative increase). Advanced Credit/Debit went from 2.59% → 2.89%. (Value Added Resource analysis)

- Jan 2025: Pay Later jumped from 3.49% → 4.99% — a 43% increase, making it the most expensive line in PayPal’s fee schedule.

- Aug 2024: Dispute fees became permanent at $20 standard / $30 if the account exceeds 1.5% dispute rate AND processed >100 transactions in the prior 3 months. Once an account crosses into the high-volume dispute tier, certain fee exclusions available to standard accounts disappear too.

- Jul 2025: PayPal updated its User Agreement to allow account closure where personal accounts “primarily involve business or commercial activity” — a silent compliance risk for ISVs whose sub-merchants use personal PayPal accounts to receive payments.

For ISVs, the takeaway is contractual: PPCP agreements should include rate-lock provisions and 60-day written-notice requirements. Without them, your platform absorbs PayPal’s pricing changes without renegotiation.

PayPal Pricing for ISVs: Revenue Share & PPCP

This is where PayPal’s pricing gets ISV-specific.

PayPal Complete Payments (PPCP) is the platform product. Direct merchants pay list rates. ISVs negotiate.

How PPCP revenue share works

PPCP lets ISVs and marketplaces embed PayPal, Venmo, cards, and Pay Later into their software, then earn a share of the processing revenue from sub-merchants who transact through the platform. The exact split depends on aggregate platform volume, vertical mix, and the negotiated commercial terms.

In practice, ISVs at meaningful volume (typically $5M+ annual platform processing) negotiate effective rates 30-80 basis points below list. The margin between the rate PayPal charges your sub-merchants and your negotiated cost basis is your embedded payment revenue.

Volume tiers

PPCP rates step down at volume thresholds. The exact thresholds aren’t published, but typical tiers kick in around $10M, $50M, and $100M annual platform volume. ISVs forecasting growth should ask for forward-rate commitments tied to volume targets, not just current-volume pricing.

What to negotiate

- Rate floors, not just current rates — what does the rate look like at $25M, $50M, $100M?

- Cross-border treatment — can the +1.50% surcharge be reduced or capped for ISVs with predictable international mix?

- Chargeback fee structure — at volume, the per-dispute fee should drop or move to a tiered model

- Reserve policy for sub-merchants — get clarity on how reserves apply and how merchants graduate out of them

- PPCP exclusivity — PayPal sometimes asks for exclusivity in exchange for better rates; understand the cost before committing

- Settlement mechanics — partner fees settle daily, but revenue share pays on the 20th of each month per PayPal’s Partner Fee Report spec. Confirm the settlement currency matches your sub-merchants’ transaction currencies — currency mismatch creates silent reconciliation overhead for international platforms.

For ISVs evaluating multiple acquirers, see how PayPal stacks against NMI, Stripe, and Braintree on the dimensions that drive payment revenue, not just per-transaction cost.

How PayPal Pricing Compares on Cost

PayPal’s headline rates sit above the lowest-priced flat-rate processors. The cost gap is narrow on standard cards and widens on the branded wallet.

vs. Stripe: Stripe’s 2.9% + $0.30 edges out PayPal Standard Cards (2.99% + $0.49) on typical ticket sizes. PayPal Checkout (3.49%) is meaningfully more expensive than Stripe across the board.

vs. Square: Square’s 2.6% + $0.10 is the cheapest on per-transaction rate for both online and in-person. Square also absorbs chargeback fees (PayPal charges $20 each).

vs. Braintree: Braintree (PayPal-owned) prices at 2.59% + $0.49 for standard cards — actually below PayPal’s own 2.99% standard card rate. ISVs that want PayPal-stack benefits at lower headline rates often look at Braintree first.

For full feature and ISV-fit comparisons, see the dedicated comparison pages above.

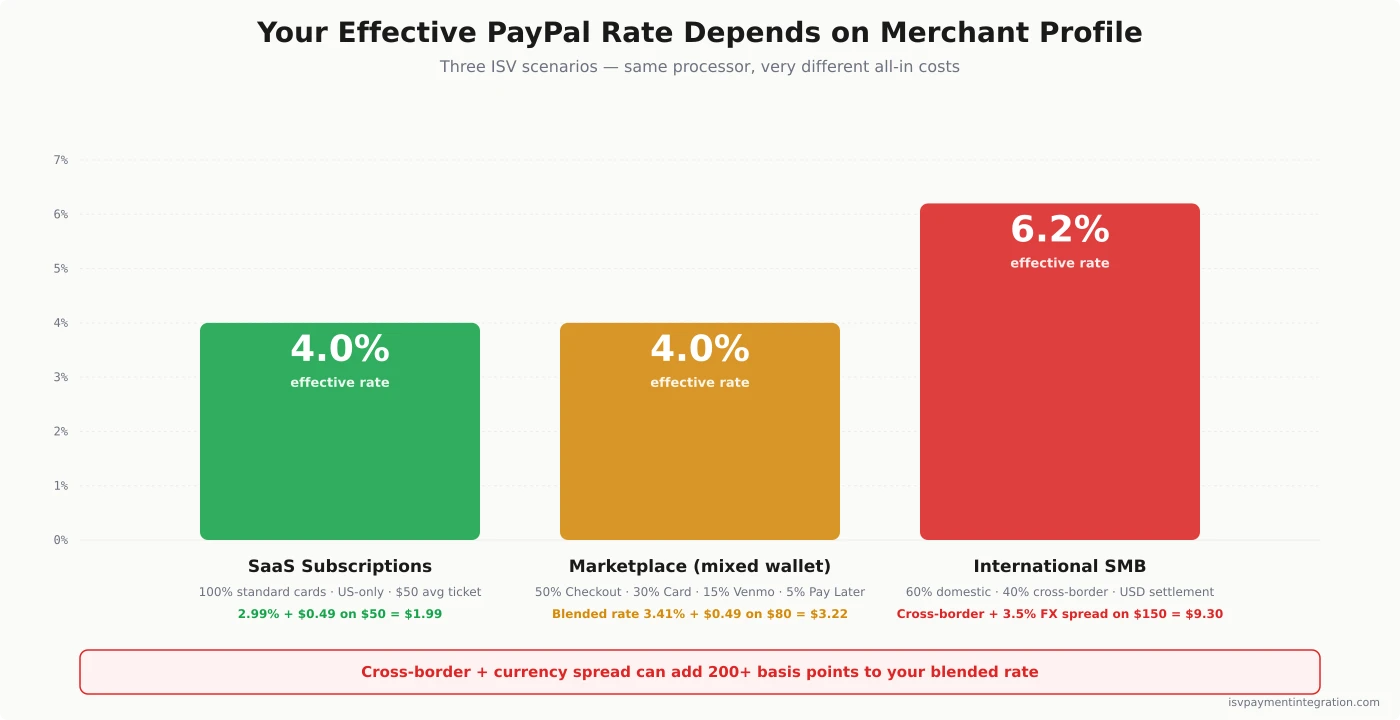

How to Estimate Your True PayPal Cost (Worked Examples)

Three ISV scenarios, three very different effective rates.

Scenario 1: SaaS subscriptions, US-only, $50 average ticket

100% standard card payments, no international, low chargeback rate (under 0.2%).

- Per transaction: 2.99% + $0.49 = $1.99 on a $50 charge

- Effective rate: ~4.0%

PayPal is competitive here, but Stripe (2.9% + $0.30 = $1.75) and Square (2.6% + $0.10 = $1.40) are cheaper on this profile. PayPal only wins if your buyers strongly prefer the wallet.

Scenario 2: Marketplace with mixed payment methods, $80 average ticket

50% PayPal Checkout, 30% standard cards, 15% Venmo, 5% Pay Later. Domestic only.

- Blended rate: (0.50 × 3.49) + (0.30 × 2.99) + (0.15 × 3.49) + (0.05 × 4.99) = 3.41%

- Plus $0.49 fixed = $3.22 on an $80 transaction

- Effective rate: ~4.0%

The wallet mix pushes the blended rate above 3.4%. ISVs running marketplaces with PayPal-heavy mix should model the blended rate explicitly when pricing merchants.

Scenario 3: International SMB, $150 average ticket, 40% cross-border

60% domestic standard cards, 40% cross-border via PayPal Checkout. UK and EU buyers, USD settlement.

- Domestic portion (60%): 2.99% + $0.49 = $4.97 on $150

- Cross-border portion (40%): 3.49% + 1.50% + $0.49 = 4.99% + $0.49 = $7.98 on $150

- Add 3.5% currency spread on the cross-border portion: another ~$5.25

- Blended effective rate: ~6.2%

The cross-border + FX stack turns a 3.49% headline into 6.2% effective. For international ISVs, this is the math that matters.

For a full assessment of PayPal’s strengths, weaknesses, and ISV fit beyond pricing, see the PayPal review.

Frequently Asked Questions

What does PayPal actually cost in 2026?

PayPal Checkout is 3.49% + $0.49 per transaction. Standard credit and debit card payments are 2.99% + $0.49. Pay with Venmo is 3.49% + $0.49. Pay Later is 4.99% + $0.49. QR code (in-person via Zettle) is 2.29% + $0.09. International transactions add 1.50% on top of the domestic rate. Currency conversion adds another 3-4% spread above the mid-market rate.

Why is PayPal Checkout more expensive than the standard card rate?

PayPal Checkout (the branded button) costs more because it routes through PayPal’s wallet, where buyers can pay with their PayPal balance, linked bank, or stored cards. PayPal charges a premium for the conversion lift the branded button delivers. If your buyers pay with a card directly through your site (not the wallet), you pay the lower 2.99% standard card rate.

How does PayPal pricing work for ISVs and platforms?

ISVs use PayPal Complete Payments (PPCP), the platform product that lets software companies embed PayPal, Venmo, cards, and Pay Later into their software and earn revenue share. PPCP rates are negotiated based on aggregate platform volume across all your sub-merchants. List rates apply to direct merchants — ISVs should always negotiate.

What hidden fees should ISVs budget for?

Cross-border (+1.50%), currency conversion (3-4% spread), chargeback fees ($20 each), dispute fees ($15-30), and held reserves on newer or higher-risk accounts. Pay Later and Venmo also carry premium rates above the standard card line. For sub-merchants in higher-risk verticals, expect rolling reserves of 5-15% held for 60-180 days.

How do PPCP rates compare to PayPal’s published list rates?

PPCP-negotiated rates typically run 30-80 basis points below list, depending on aggregate platform volume. ISVs at $5M annual processing usually see modest discounts; ISVs at $50M+ negotiate meaningful rate floors and tier step-downs. There’s no public PPCP rate card — every deal is custom. Always quote merchants based on your negotiated PPCP rate, not PayPal’s published 2.99% / 3.49% headlines.

Does PayPal Payments Pro still exist?

Yes, but PayPal has been steering merchants toward PayPal Complete Payments (PPCP) and Braintree (which PayPal owns). Payments Pro at $30/month is still listed for direct merchants who want hosted card-on-file and a virtual terminal. For ISVs, PPCP is the modern path — Payments Pro is rarely the right choice.

How can ISVs reduce PayPal fees for their merchants?

Negotiate PPCP rates based on aggregate platform volume rather than letting each merchant onboard at list rate. Offer the standard card path (2.99%) as the default and surface PayPal Checkout (3.49%) only when buyers benefit from wallet conversion. For international merchants, batch settlements in the merchant’s local currency to avoid the 3-4% conversion spread when possible.