PayPal vs Fiserv

A feature-by-feature comparison for ISVs integrating payments.

One of these companies already has a payment relationship with hundreds of millions of the buyers your merchants are trying to charge; the other owns the machinery that charges them. That is not a difference of features, and the usual head-to-head — which API, which rate — measures the wrong thing. A software platform is really choosing whether embedded payments should carry a demand network into the checkout or stay invisible rails behind it.

Feature Comparison

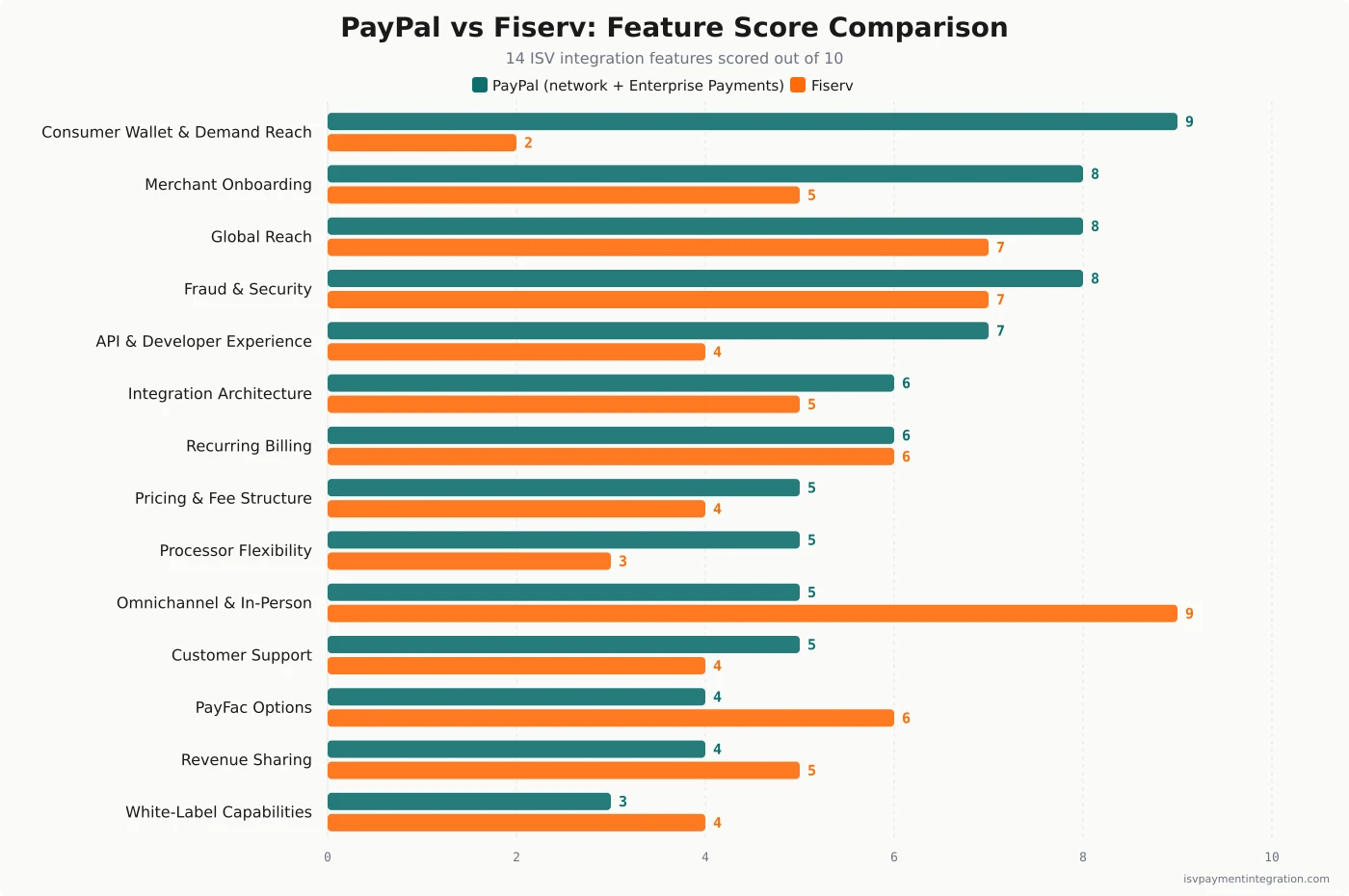

| Feature | PayPal | Fiserv |

|---|---|---|

| Consumer Wallet & Demand Reach | 9 | 2 |

| Merchant Onboarding | 8 | 5 |

| Global Reach | 8 | 7 |

| Fraud & Security | 8 | 7 |

| API & Developer Experience | 7 | 4 |

| Integration Architecture | 6 | 5 |

| Recurring Billing | 6 | 6 |

| Pricing & Fee Structure | 5 | 4 |

| Processor Flexibility | 5 | 3 |

| Omnichannel & In-Person Payments | 5 | 9 |

| PayFac Options | 4 | 6 |

| Revenue Sharing | 4 | 5 |

| White-Label Capabilities | 3 | 4 |

| Customer Support | 5 | 4 |

Get this comparison as a shareable PDF

We'll send the PayPal vs Fiserv breakdown to your inbox — ready to share with your team.

Best for

PayPal

Best for online-first platforms whose merchants' buyers are consumers — retail, marketplaces, events, subscriptions, donations — where the PayPal and Venmo buttons are a conversion lever rather than a brand you would rather hide. Accept that PayPal is visible to your merchant's customers and that splitting a transaction still requires a sales conversation.

Best for

Fiserv

Best for vertical SaaS in salons, restaurants, clinics and field services where the device on the counter is part of the product itself. Accept a negotiated rate you cannot benchmark and an integration that opens with a sales cycle rather than an API key.

PayPal vs Fiserv: The Network and the Rail

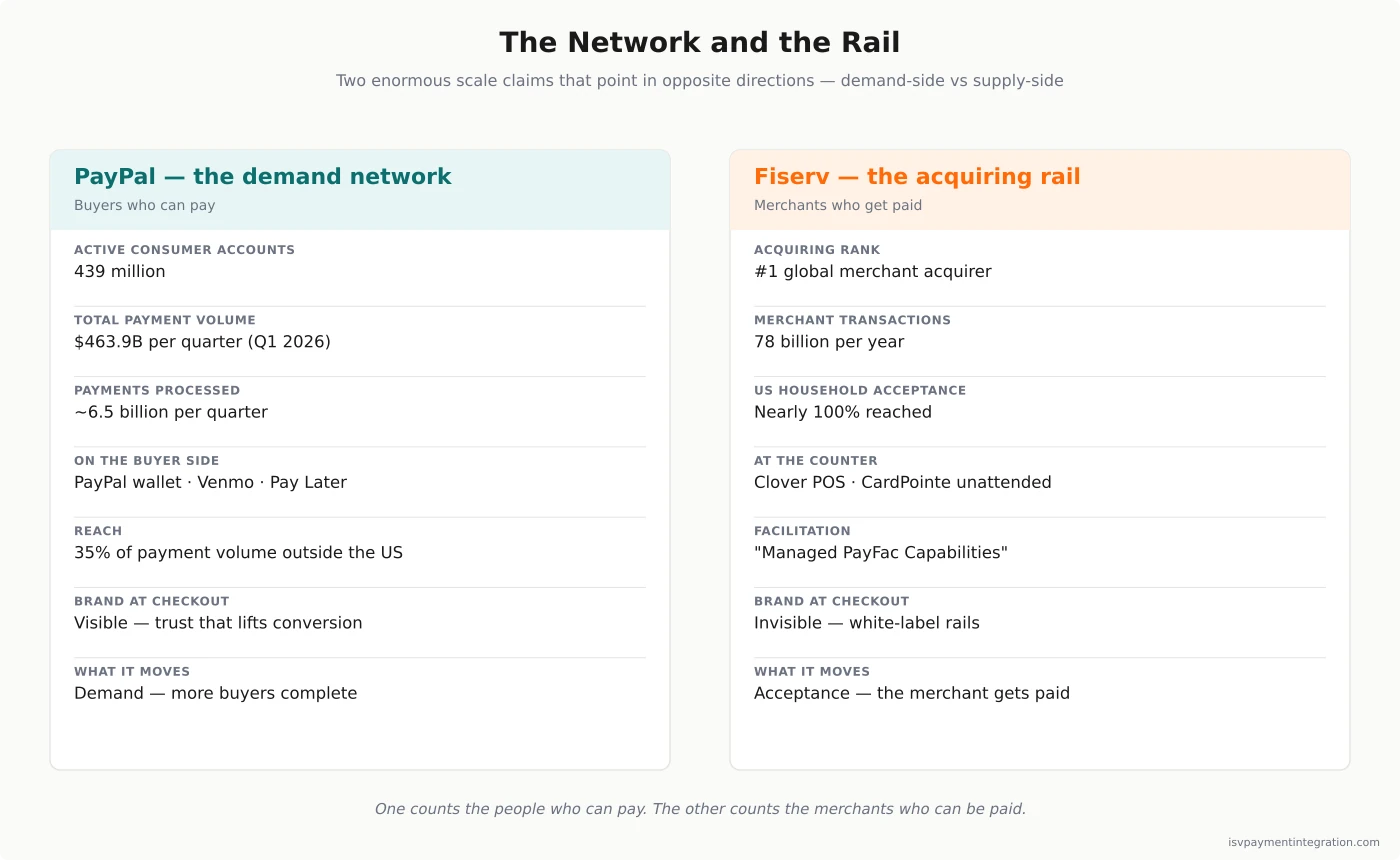

Put these two companies on the same page and the feature grid quietly misleads you, because they are not really the same kind of thing. Fiserv is the machinery of acceptance — the largest merchant acquirer in the world, the rails and the terminals that move a card payment from a buyer’s bank to a merchant’s account. PayPal is those rails too, through the acquiring business it now calls PayPal Enterprise Payments. But PayPal is also something Fiserv is not: a two-sided network with the buyer on the other end of the transaction. In PayPal’s Form 10-Q for the three months that ended March 31, 2026, the company reports 439 million active accounts and $463.9 billion in total payment volume in that single quarter, up 11% year over year, across roughly 6.5 billion payments. Fiserv’s own ISV page answers with a different kind of scale — it bills itself as the #1 global merchant acquirer, one that processes 78 billion merchant transactions a year and reaches nearly every U.S. household.

Both numbers are enormous. They point in opposite directions. One counts the people who can pay; the other counts the merchants who can be paid. For a software platform deciding where to anchor embedded payments, that is the whole comparison, and it resolves differently than the API checklist would.

Quick Take: A Demand Network and an Acquiring Backbone

PayPal reaches an ISV in two forms that share a brand. There is the wallet — the PayPal and Venmo buttons a platform adds to its merchants’ checkout so that hundreds of millions of already-registered buyers can pay in one tap, plus Pay Later for installments. And there is PayPal Enterprise Payments, the acquiring gateway formerly branded Braintree; its landing page opens verbatim, “Braintree is now PayPal Enterprise Payments.” A software company can take one, the other, or both. What it is really buying with the first is access to PayPal’s buyer base; what it buys with the second is full-stack processing that happens to belong to the same company.

Fiserv courts software companies through its ISV Partner Program, and the proof points it leads with are all acquiring scale: it calls itself the world’s number-one merchant acquirer, cites 78 billion merchant transactions a year, and claims to reach nearly every U.S. household. The acceptance gateway is CardPointe; CoPilot manages the portfolio; and the program advertises “Managed PayFac Capabilities,” Fiserv’s term for payment facilitation it operates on a platform’s behalf. Running alongside is Clover, the point-of-sale ecosystem, and between them they are how most vertical software actually connects to Fiserv. Nowhere in the offering is a consumer wallet, and nowhere on the page is a price.

The distinction is not that one is bigger. It is that PayPal brings demand and Fiserv brings acceptance, and a platform’s merchants need both — which is why, more often than the comparison format admits, the honest answer is not “one of these” but “which of these is the anchor.”

What You’re Actually Buying: Buyers or Acceptance

Every embedded-payments decision eventually reduces to a question about your merchants’ customers. Are they consumers making discretionary purchases, where the friction of typing a card number is a real drag on conversion? Or are they paying because they have to — a clinic copay, a field-service invoice, a restaurant tab at the counter — where the payment happens regardless and the job is to accept it cleanly?

If your merchants sell to consumers, PayPal’s core asset is directly useful. A buyer who is already logged into PayPal or Venmo skips the card-entry form entirely, and the consumer side of PayPal’s business rests on that removed friction converting more browsers into buyers. You are not primarily buying cheaper processing when you add PayPal; you are buying a demand-side network that shows up on the buyer’s side of your merchant’s checkout. Fiserv has no comparable consumer wallet to switch on here — its business is the acquiring and banking infrastructure underneath thousands of banks and merchants, and it stays invisible to the buyer at your merchant’s checkout.

If your merchants are paid because a service was rendered, the calculus inverts. The buyer’s willingness to complete the transaction is not in question, so a wallet’s conversion lift is worth less, and the value moves to the acceptance side: reliable settlement, a terminal that survives a busy Saturday, hardware that runs the register. That is the ground Fiserv was built on and where Clover has a decade-plus head start.

Neither company can credibly claim the other’s territory. PayPal cannot manufacture a counter-attached hardware ecosystem overnight, and Fiserv has no comparable consumer wallet network to switch on at your merchant’s checkout. The question is which side of the transaction your software needs to strengthen.

The Reach Each Advertises Points the Opposite Way

It is worth dwelling on the two scale claims, because they look comparable and are not. Fiserv says it reaches nearly 100% of U.S. households. PayPal says it has 439 million active accounts. A casual reader files both under “very large” and moves on. But Fiserv’s figure is a statement about acceptance distribution — through its bank relationships and merchant base, a card payment from almost any U.S. household can be processed on Fiserv rails. It is a supply-side fact. It does not mean those households bank with a brand called Fiserv — they bank with the institutions Fiserv powers, while Fiserv itself stays invisible behind them.

PayPal’s 439 million is the reverse: a demand-side fact. These are registered accounts that have transacted in the past twelve months, with a stored funding source and, often, a stored balance. When your merchant shows a PayPal button, some meaningful share of their buyers are one login from paying. Fiserv’s reach lets a merchant get paid; PayPal’s reach makes some buyers more likely to pay. An ISV that treats the two numbers as interchangeable evidence of “market leadership” will pick the wrong tool, because they are answers to different questions — and only one of them changes a checkout conversion rate.

There is a durability point folded in here too. PayPal’s network compounds: 35% of its payment volume is now generated outside the U.S., and Venmo and Pay Later extend the same account base into new behaviors. Fiserv’s advantage compounds differently, through switching costs — a merchant running its business on a Clover does not casually migrate. Both are real moats. They are just moats around different castles.

Whose Brand Owns the Checkout

The most underrated difference between these two is cosmetic until it is strategic: PayPal is a visible consumer brand, and Fiserv is deliberately not.

When a platform embeds the PayPal or Venmo button, the buyer sees PayPal. The trust that converts them is PayPal’s trust, and the account relationship — the stored card, the dispute process, the buyer protection — is substantially PayPal’s relationship. For a platform whose merchants sell to consumers, that borrowed trust is the point; it is exactly what lifts the conversion rate. But it is worth naming what you are trading for it: a third party’s brand sits inside your merchant’s checkout, and some of the customer relationship travels with it.

Fiserv sits at the opposite pole. Through CardPointe, the acceptance experience can be almost entirely your merchant’s own brand; the buyer need never learn that Fiserv exists. Clover is the exception — that hardware wears its own name on the counter — but the acquiring rail itself is white-label by design. Fiserv brings no consumer trust to lend, and asks for no brand real estate in return.

So the checkout question is a genuine fork, not a footnote. Do you want a demand network’s brand in front of your merchant’s customers, lifting conversion but owning a slice of the relationship? Or do you want invisible rails that leave the merchant’s brand — and the customer relationship — entirely with the merchant? This is the axis on which a lot of platforms actually decide, and it maps onto the ISV role you are really choosing to play in your merchant’s business.

Conversion Is the Product PayPal Is Selling

Follow the money from an ISV’s seat and PayPal’s pitch clarifies. A platform embedding payments earns from the spread between what it charges its merchants and what it is charged. PayPal offers two ways to improve that equation, and only one is about the rate.

The first is the rate itself. Through PayPal Enterprise Payments, the published card rate for standard merchants is 2.89% + $0.29, dated May 7, 2026 on the fee page, with custom pricing available to established businesses based on business model and processing volume. That is a normal full-stack acquiring proposition, competitive with the field, and it is covered in depth on the Braintree pricing breakdown. It is not what makes PayPal different.

What makes PayPal different is the second lever: more of your merchant’s transactions succeed. A wallet that converts an extra few percent of checkouts raises your merchant’s revenue and therefore your payment revenue, without any change in the rate. That is a growth lever a pure acquirer structurally cannot offer, because a pure acquirer only ever touches the transaction after the buyer has already decided to pay. When PayPal’s 10-Q credits Braintree with roughly $410 million of transaction-revenue growth last quarter — more than its PayPal-branded and Venmo products managed to add together — it is describing a company monetizing the rail and the wallet at the same time. The rail is even the faster-growing half, which is exactly why an ISV should not treat “adding PayPal” as only a wallet decision. An ISV can plug into either engine.

The one discipline this requires: measure the lift, do not assume it. A wallet helps most where card-entry friction is highest — mobile, first-time buyers, higher-consideration purchases — and helps least where a merchant’s customers are repeat payers on file. Model it against your own funnel with the revenue calculator before treating the conversion story as free money.

What Fiserv Sells Instead: The Rail and the Counter

Fiserv’s value to an ISV is not a demand lever; it is depth on the acceptance side, and it comes in two forms.

The first is the rail. As the #1 global merchant acquirer processing 78 billion transactions a year, Fiserv offers the kind of settlement reliability, funding, and underwriting reach that a platform with heterogeneous or higher-risk merchants leans on. Its “Managed PayFac Capabilities” let a software company offer payment facilitation — fast sub-merchant onboarding, split funding, a branded acceptance experience — while Fiserv carries the compliance weight and the sponsor-bank relationship. For a platform that wants the economics of a facilitator without registering as one, that is a real product, even though the terms of it arrive through a sales conversation rather than a rate card.

The second is the counter. Clover is not a payment method bolted onto software; it is the system a restaurant or salon actually operates on all day — ringing up orders, running the register, printing tickets, and taking the card as just one of its jobs. A vertical SaaS product that integrates with Clover is integrating with its merchant’s operating system, and Fiserv has extended that surface to unattended acceptance through CardPointe as well; the Fiserv review walks the full CardConnect–Clover–Carat portfolio. No wallet a platform bolts on can substitute for that, because the value is physical presence in the merchant’s daily operation, not conversion at an online checkout.

What Fiserv will not do is put a platform number in front of you before the conversation, and it does not pretend otherwise: there is no published CardPointe rate and no ISV revenue-share figure on the ISV Partner Program page, which ends at a contact form. Anyone quoting you a specific Fiserv share is quoting something Fiserv did not publish. The Fiserv pricing breakdown explains how to negotiate against that opacity.

Most ISVs Run Both — So Decide Which Is the Anchor

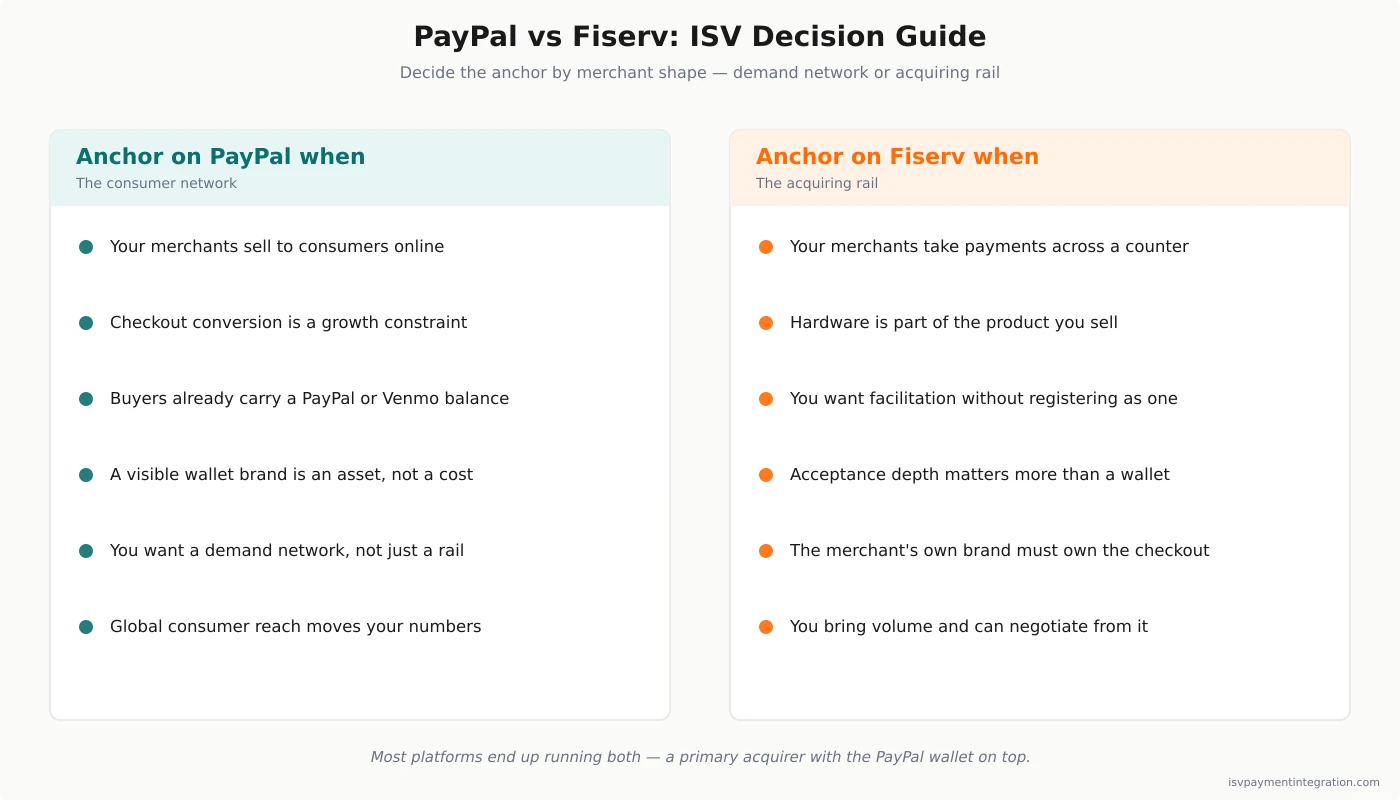

Here is the reframe that dissolves the false choice. In practice, a great many software platforms do not pick PayPal or an acquirer; they run a full-stack acquirer as their primary rail and add the PayPal wallet as an accepted method on top, because the two do different jobs. The comparison that matters, then, is rarely “PayPal versus Fiserv” as mutually exclusive processors. It is: which of them is your anchor, and which is the accessory?

If your merchants sell to consumers online and conversion is your growth constraint, PayPal is the anchor. You build on PayPal Enterprise Payments or a comparable gateway, switch on the wallet, and treat the demand network as the core of the value you sell your merchants. In-person, if it comes up, is a secondary channel.

If your merchants live behind a counter or need managed facilitation across a messy portfolio, Fiserv is the anchor. You build on CardPointe or Clover, take the acquiring depth and the hardware ecosystem as the core, and — if your merchants also sell online to consumers — you may still add a PayPal or Venmo button as the accessory that lifts those specific checkouts. The wallet does not compete with the rail; it rides on top of it.

The mistake is to run the API-and-rate bake-off, conclude that PayPal’s developer experience wins, and build a counter-attached vertical SaaS product on a stack that was never meant for the terminal — or, conversely, to choose Fiserv for its acquiring gravitas and leave a consumer-conversion lever unused because no one owns the wallet question. Decide the anchor by merchant shape first. Everything else is downstream of that. For the adjacent evaluations, Braintree vs Fiserv drills into the acquiring gateway on its own terms, Stripe vs Fiserv covers the API-first rail that publishes its platform economics, and PayPal vs Braintree disentangles the two PayPal products now sharing one brand.

PayPal vs Fiserv: ISV Decision Guide

- Do your merchants sell to consumers, or to obligated payers? Consumer discretionary purchases reward PayPal’s wallet; copays, invoices and counter tabs reward Fiserv’s acceptance depth. This one question predicts most of the rest.

- Is checkout conversion a growth constraint you can measure? If lifting completion by a few points moves real revenue, the demand network is worth a visible button. If your merchants’ customers are repeat payers on file, the lift is small.

- Is the point of sale a physical counter? When the terminal matters more than the web checkout, a hardware operating system like Clover decides it, and the wallet question drops to secondary.

- Are you comfortable with a third-party consumer brand in your merchant’s checkout? PayPal is visible and owns a slice of the buyer relationship. Fiserv is invisible and leaves it with the merchant.

- Do you need facilitation economics without becoming a registered facilitator yourself? Fiserv names a Managed PayFac product; PayPal’s Marketplace and Multiparty routes are approval-gated aggregation models, not a facilitation offering.

- Might you move volume to another processor later? PayPal Enterprise Payments publishes orchestration guides to third-party processors including Adyen and Stripe; Fiserv publishes no comparable orchestration guide.

- Are you building one rail or two? Most platforms end with a primary acquirer plus the PayPal wallet on top. Decide which is the anchor before you optimize either.

Frequently Asked Questions

Is PayPal a payment processor or a consumer wallet, and which am I comparing to Fiserv?

Both, and that is the point of this comparison. PayPal is a two-sided network: it is a consumer wallet with 439 million active accounts, and it is a full-stack acquiring processor through PayPal Enterprise Payments, the gateway formerly branded Braintree. For an ISV, “adding PayPal” usually means embedding the PayPal and Venmo wallet buttons to lift checkout conversion, building on the Braintree gateway for end-to-end processing, or both. Fiserv, by contrast, is purely acceptance-side: the #1 global merchant acquirer, with no consumer wallet. So you are comparing a demand-and-acceptance network against a pure acquiring rail. See PayPal vs Braintree for how PayPal’s two products differ where they overlap.

Does adding PayPal mean replacing my acquirer or Fiserv?

Usually not. Many platforms run a full-stack acquirer as their primary rail and add the PayPal wallet as an accepted payment method on top, because the wallet’s job — converting more buyers — is different from the rail’s job of processing and settling. If Fiserv is your acquiring backbone for counter-attached or higher-risk merchants, you can still offer a PayPal or Venmo button on the checkouts where those merchants also sell to consumers online. The genuine either/or only appears when you would build your entire processing stack on one company; the wallet-versus-rail decision is more often about which is the anchor and which is the accessory.

Which has more reach, PayPal or Fiserv?

They lead on different axes and the numbers are not comparable. PayPal reports 439 million active consumer accounts and $463.9 billion in quarterly total payment volume — a demand-side measure of buyers who can pay. Fiserv advertises that it is the #1 global merchant acquirer, processes 78 billion transactions a year, and reaches nearly 100% of U.S. households — a supply-side measure of acceptance distribution. PayPal’s reach makes some buyers more likely to complete a purchase; Fiserv’s reach lets almost any merchant get paid. An ISV should decide which side of the transaction it needs to strengthen rather than ask which company is “bigger.”

Will my merchants’ customers see the PayPal brand at checkout?

Yes. The PayPal and Venmo buttons are visible consumer-facing brands, and that visibility is the mechanism — buyers convert because they trust and are already logged into PayPal, and part of the account relationship travels with it. That is an asset when your merchants sell to consumers and a cost when you want the checkout to be entirely your merchant’s own brand. Fiserv is the opposite: through CardPointe the acceptance experience can be almost fully white-labeled, and the acquiring rail is invisible to the buyer. Clover is the one Fiserv product that wears its own name, because it is the physical device on the counter.

Which is better for in-person and retail payments?

Fiserv, clearly, when the counter is central. Clover is a hardware operating system that runs a merchant’s register, order flow and receipts, with a large installed base and a decade-plus head start, and CardPointe adds unattended acceptance. PayPal has in-person options, but its structural strength is the wallet at online checkout, not the terminal. If your software serves restaurants, salons, clinics or field services where the device is part of the product, Fiserv’s omnichannel depth is the deciding factor; if your merchants are online-first with consumer buyers, PayPal’s demand network matters more than its hardware.